Soft Payrolls, Sticky Wages: the Fed’s Dilemma in 2026

50 mins ago

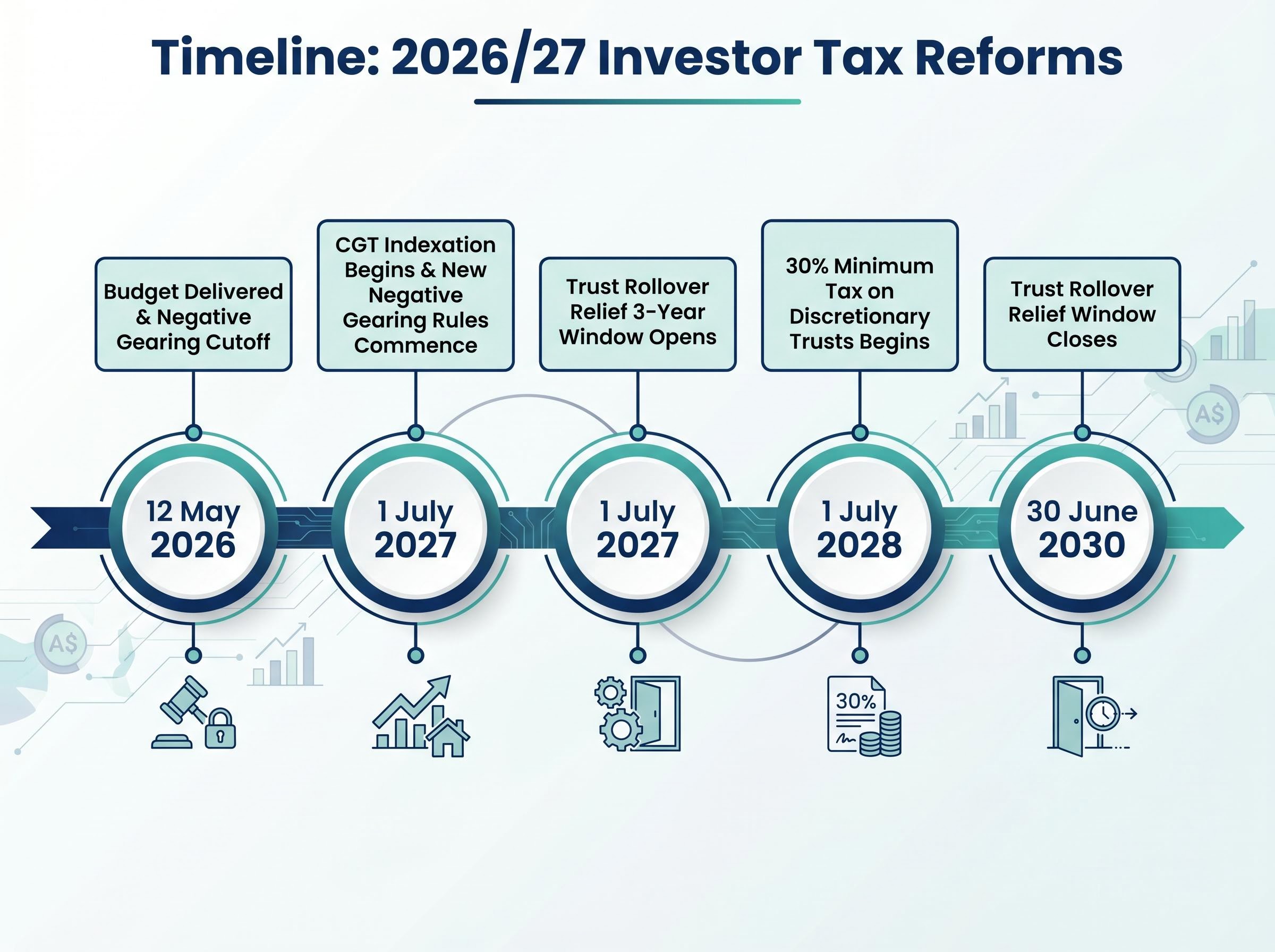

Three headline investment tax reforms announced in tonight’s Federal Budget will collectively reshape how Australian investors are taxed on property, shares, and trust distributions. Treasurer Jim Chalmers delivered the 2026/27 Federal Budget on Tuesday, 12 May 2026, framing the package around housing affordability and tax fairness. For investors, the immediate story is a generational reset: the 50% capital gains tax discount, open-ended negative gearing on established property, and low-rate trust distribution strategies are all being wound back in a coordinated $77 billion revenue package.

What follows breaks down each of the three reforms, explains the specific rules that apply from tonight, and translates the commencement dates and grandfathering provisions into plain terms so investors can assess what, if anything, they need to act on.

The scale arrived first. The three reforms, capital gains tax restructuring, negative gearing limits, and a minimum tax on discretionary trusts, will generate a combined $77 billion over the decade, according to official budget papers. That revenue underwrites the $6.4 billion Working Australians Tax Offset, which provides up to $250 per eligible worker annually from 1 July 2027.

The Albanese government positioned the package as a single coordinated intervention, not three separate announcements. PwC quantified the investor-facing cost sharply.

PwC characterised the reforms as a “$3.63 billion hit to investors, start-ups and entrepreneurs.”

The budget projects a headline deficit of approximately 1.6% of GDP. The three reforms touch:

Each has a different commencement date and a different grandfathering rule. The detail matters.

Since September 1999, Australian investors holding a capital gains tax asset for at least 12 months have been entitled to a flat 50% discount on the gain. That rule is being replaced.

From 1 July 2027, gains accruing after that date will be taxed under an inflation-adjusted indexation method, with a 30% minimum tax rate applied to real (inflation-adjusted) gains. Only the portion of a gain that exceeds cumulative inflation will be treated as taxable profit. The main residence exemption is retained.

The Australian Shareholders Association (ASA) offered measured support for the underlying principle.

“Investors should not be taxed on inflationary gains,” the ASA stated on 12 May 2026.

The grandfathering provision is straightforward. Gains accruing before 1 July 2027 retain the 50% discount. Only gains accruing after that date fall under the new indexation rules. The three asset categories affected under the new framework are:

Investors in new builds receive an additional option: they may elect either the 50% CGT discount or the new indexation arrangements, a concession designed to maintain incentives for housing supply.

Capital gains tax applies when an investor sells an asset for more than its purchase price. The 50% discount, introduced in 1999, was designed as a simplified proxy for inflation relief. Rather than calculating the actual inflation that eroded an asset’s value over the holding period, the government applied a flat halving of the gain. The logic was simplicity: one rule for all holding periods, regardless of actual price growth.

Critics argued the flat discount overcompensated investors during periods of low inflation and disproportionately benefited high-income earners, who received the same 50% reduction on gains that had little to do with inflation. The new indexation method addresses this by taxing only real gains, the amount by which the sale price exceeds the inflation-adjusted cost base.

A simple example illustrates the difference.

| Scenario | Old 50% Discount Result | New Indexation Result | Taxable Gain Difference |

|---|---|---|---|

| Asset sold for $100,000 gain; inflation accounts for $30,000 | Taxable gain: $50,000 | Taxable gain: $70,000 (at minimum 30% tax rate) | $20,000 higher under new rules |

In this scenario, the old discount reduced the gain by more than actual inflation warranted. Under indexation, the investor pays tax on the real gain only, but at a higher effective amount than the blanket discount would have produced.

For property investors, the grandfathering line is tonight. All properties held before 12 May 2026 (Budget night) are fully grandfathered under existing negative gearing rules. No changes apply to those holdings.

The new rules, commencing 1 July 2027, apply to established housing purchased after Budget night. Investors who buy established property after tonight can deduct rental losses only against residential property income, not against wages or other income. Unused losses are carried forward.

New builds retain full negative gearing. Losses on newly constructed properties remain deductible against all income, a deliberate policy lever designed to channel investment toward housing supply rather than competition for existing stock.

| Property Type / Purchase Timing | Negative Gearing Treatment | Loss Deductibility |

|---|---|---|

| Held before 12 May 2026 | Fully grandfathered | Losses deductible against all income |

| Established property purchased after 12 May 2026 | Ring-fenced | Losses deductible only against residential property income; unused losses carried forward |

| New build purchased after 12 May 2026 | Full negative gearing retained | Losses deductible against all income |

The distinction between “held before” and “purchased after” Budget night is the single most consequential line for property investors reading tonight’s budget papers.

From 1 July 2028, all discretionary trust distributions to beneficiaries will be taxed at no less than 30%. The reform targets a widely used strategy in which family and investment trusts distribute income to beneficiaries on lower marginal tax rates, reducing the overall tax burden on investment income.

The scope is broad. Family trusts and investment trusts are captured. Self-managed super funds (SMSFs) and fixed trusts are explicitly exempt, with further exemption details subject to consultation.

The rollover relief provision is where the tone shifts from concern to manageable complexity. Trustees have a three-year restructuring window commencing 1 July 2027, during which restructuring can occur without triggering CGT or other adverse tax consequences.

“Rollover relief will be provided for three years from 1 July 2027,” according to official budget papers published on budget.gov.au.

For trust holders, three steps apply during the relief window:

Taken together, the three reforms send a directional signal. Tax incentives are being redirected toward new housing construction and away from established property accumulation and high-income trust distribution strategies. ABC News coverage on 12 May 2026 noted the reforms could make shares more attractive relative to established property, as inflation indexation tends to favour non-property assets over long holding periods.

PwC Chief Economist Amy Lomas described the broader package as “structural economic reform” aimed at productivity, while flagging particular concern for startup share arrangements caught by the CGT changes. The ASA expressed support for the inflation indexation principle but noted investor uncertainty during the transition period.

Several details remain unresolved. No Australian Taxation Office (ATO) guidance has been issued immediately post-budget, and further consultation is expected. Investors should monitor three developments in the months ahead:

The grandfathering provisions across all three reforms mean no immediate action is required for existing holdings. That is the most consequential line in tonight’s budget for the majority of Australian investors. Complacency, however, carries its own risk: the transition windows are finite.

Three investor-specific action prompts apply:

The CGT and negative gearing reforms commence 1 July 2027. The discretionary trust minimum tax takes effect 1 July 2028. Further ATO guidance and legislation are expected through 2026 and 2027; investors can track progress via budget.gov.au and aph.gov.au.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Legislative details remain subject to parliamentary processes and further consultation; implementation specifics may change.

From 1 July 2027, the existing 50% CGT discount for assets held over 12 months will be replaced by an inflation indexation method, where only real gains above cumulative inflation are taxed, subject to a 30% minimum tax rate. Gains accruing before 1 July 2027 retain the 50% discount under grandfathering provisions.

Properties held before 12 May 2026 (Budget night) are fully grandfathered under existing negative gearing rules. For established properties purchased after that date, rental losses can only be deducted against residential property income, not wages or other income, while new builds retain full negative gearing against all income.

From 1 July 2028, all distributions from discretionary trusts, including family and investment trusts, must be taxed at no less than 30%, closing the strategy of distributing income to beneficiaries on lower marginal tax rates. SMSFs and fixed trusts are explicitly exempt, and trustees have a three-year rollover relief window from 1 July 2027 to restructure without triggering adverse tax consequences.

Property investors should first confirm whether any planned established property purchases fall before or after Budget night on 12 May 2026, as that date determines negative gearing eligibility under the new ring-fencing rules. Those with existing holdings can take comfort that all properties held before that date are fully grandfathered.

The capital gains tax restructuring and negative gearing changes both commence on 1 July 2027, while the 30% minimum tax on discretionary trust distributions takes effect from 1 July 2028. Further ATO guidance and legislation are expected through 2026-2027, and investors can track progress via budget.gov.au and aph.gov.au.