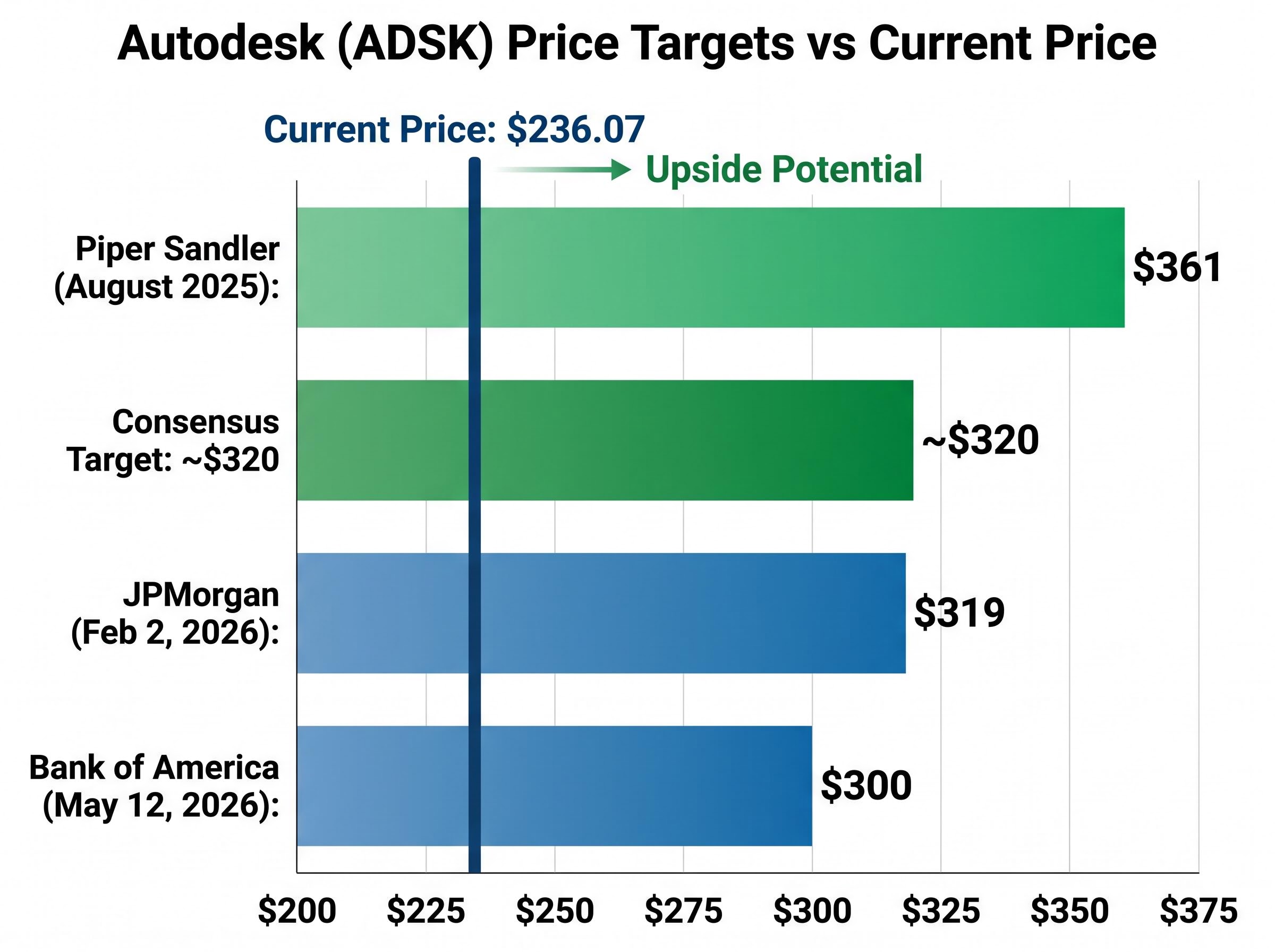

Bank of America reinstated coverage of Autodesk on 12 May 2026 with a $300 price target, calling investor fears about AI disruption “overblown.” The stock sat at $236.07, down roughly 20% year-to-date. A broad market narrative has taken hold that generalist AI tools from OpenAI, Google, and Anthropic will commoditise design software the way SaaS commoditised on-premise licensing. For a stock like Autodesk, that narrative has real consequences: it has suppressed the share price even as the company’s fundamentals have held up. BofA’s re-entry makes a structural counterargument that deserves stress-testing rather than acceptance at face value. What follows is an examination of whether Autodesk’s AI moat is genuinely defensible, what the early monetisation evidence actually shows, where the competitive threat is concentrated, and how to frame valuation in the context of an ongoing sales model transition.

Why investors are wrong to treat Autodesk like a generic software target

The selloff thesis rests on a specific assumption: that large language models can replicate Autodesk’s core functionality using publicly available design data. It is a reasonable fear for text-based or image-based software. It does not transfer to three-dimensional geometric design.

The broader context behind Autodesk’s selloff is a sector-wide repricing: AI disruption in SaaS erased more than $1 trillion in US enterprise software market capitalisation by February 2026, as autonomous AI agents began challenging the per-seat subscription economics that underpin most legacy software businesses.

The distinction is categorical, not incremental. Generalist AI and geometric AI diverge on three structural axes:

- Training data type. Text and image AI models train on vast public internet datasets. 3D geometric AI requires proprietary annotated design files, engineering constraints, and simulation outcomes that do not exist on the open web.

- Spatial reasoning requirements. Generating a paragraph or a flat image involves pattern completion across two dimensions. Generating a structurally valid 3D component involves physics-aware spatial reasoning that current generalist architectures are not optimised for.

- Domain-specific validation needs. A text output can be evaluated by a reader. A 3D design output must satisfy material science constraints, load-bearing calculations, and manufacturing tolerances, requiring domain-expert validation loops baked into the model.

BofA analyst Tomer Zilberman pointed to Autodesk’s approximately decade-long AI investment as the foundation of this separation. Autodesk’s own AI Jobs Trends Report (June 2025) recorded a 56.1% year-on-year increase in AI job mentions in US listings through April 2025, a signal that industry demand for domain-specific AI talent is outpacing what generalist models can supply.

Bloomberg characterised Anthropic’s Claude 3.5 integration with CAD workflows in May 2026 as “complementary” to Autodesk’s ecosystem, not disruptive.

That framing matters. When the most capable generalist AI firms are positioning themselves as add-ons rather than replacements, the disruption narrative loses its foundation.

When big ASX news breaks, our subscribers know first

Proprietary 3D Data: Autodesk’s Enduring AI Edge

Understanding the moat requires understanding what the data actually contains and why capital alone cannot reproduce it.

What the 3D dataset contains that public data does not

Autodesk’s proprietary datasets are not simply 3D models. They contain annotated geometric relationships, where every edge, face, and constraint carries metadata about engineering intent. They store simulation outcomes, recording how designs performed under stress, heat, and load. They preserve design iteration histories, capturing the decision logic of engineers refining components across hundreds of cycles.

This information is generated through paid customer workflows on platforms like Fusion 360, not scraped from the open web. Fusion 360 Generative Design, updated in Q4 FY2025 (February 2026), illustrates what this data enables at the product level: the system auto-generates structurally valid design variants informed by real-world manufacturing and simulation data that competitors cannot access.

Why reproducing this dataset takes longer than capital alone can solve

RBC Capital framed the barrier in February 2026 as “10+ years of curated 3D datasets” forming a low-disruption moat. The cold-start problem facing rivals is threefold:

- Data volume. Accumulating millions of annotated design files requires a paying customer base generating those files over years.

- Annotation quality. Labelling geometric relationships at scale demands domain expertise in mechanical engineering, architecture, and construction, not just compute resources.

- Domain-specific labelling expertise. The engineers who can annotate 3D constraint data are a scarce labour pool, and training new annotators is itself a multi-year process.

Dassault Systèmes is the only meaningful exception. Its 3DEXPERIENCE AI platform (Q1 2026) draws on comparable data depth, particularly in automotive applications. Yet Autodesk leads in cloud AI adoption according to the State of Design & Make 2025 report, which surveyed approximately 6,000 respondents and found 77% of business leaders prioritising AI skills investment. The customer base is actively demanding AI-native tools, and Autodesk’s cloud infrastructure positions it to deliver them faster than legacy on-premise architectures.

Reading the early monetisation signals before they show up in earnings

The moat argument is structural. The monetisation argument is forensic, and the evidence is still early.

The clearest available signal is AutoConstrain’s adoption rate. BofA’s May 2026 note cited a 60% adoption figure among eligible users as “early monetisation proof.” A necessary caveat: that figure comes from BofA’s analyst note, not from Autodesk’s public filings. It has not been independently verified.

BofA characterised AutoConstrain adoption as “early monetisation proof,” the first measurable signal that AI features are pulling through to user workflows.

The strategic logic behind the monetisation model matters as much as the adoption number. Autodesk is layering AI features as upsell tiers within existing subscriptions rather than releasing them as separate SKUs. This approach protects subscription revenue stability while expanding average selling price per seat. The anticipated next evolution is usage-based billing for premium AI workloads, which would tie revenue directly to feature consumption.

The financial trajectory supports the thesis directionally. FY2026 non-GAAP EPS guidance of $10.18-$10.25 (reported at Q3 FY2026 earnings on 25 November 2025) came in above prior consensus of approximately $9.95. BofA projects free cash flow of $2.4 billion in FY2026 rising to $2.8 billion in FY2027.

Autodesk’s Q3 FY2026 earnings beat, reported on 25 November 2025, delivered non-GAAP EPS above prior consensus estimates and prompted shares to rise, providing the fundamental backdrop against which BofA’s May 2026 reinstatement was framed.

The three-step monetisation progression to monitor:

- AI feature release and integration into existing subscription tiers

- Adoption rate signals confirming user pull-through (AutoConstrain being the current proof point)

- Pricing tier expansion, including usage-based billing for premium AI workloads

Q1 FY2027 earnings on 28 May 2026 represent the next verification moment. Updated adoption metrics and forward billings guidance will either confirm or challenge this trajectory.

Sizing the competitive threat realistically

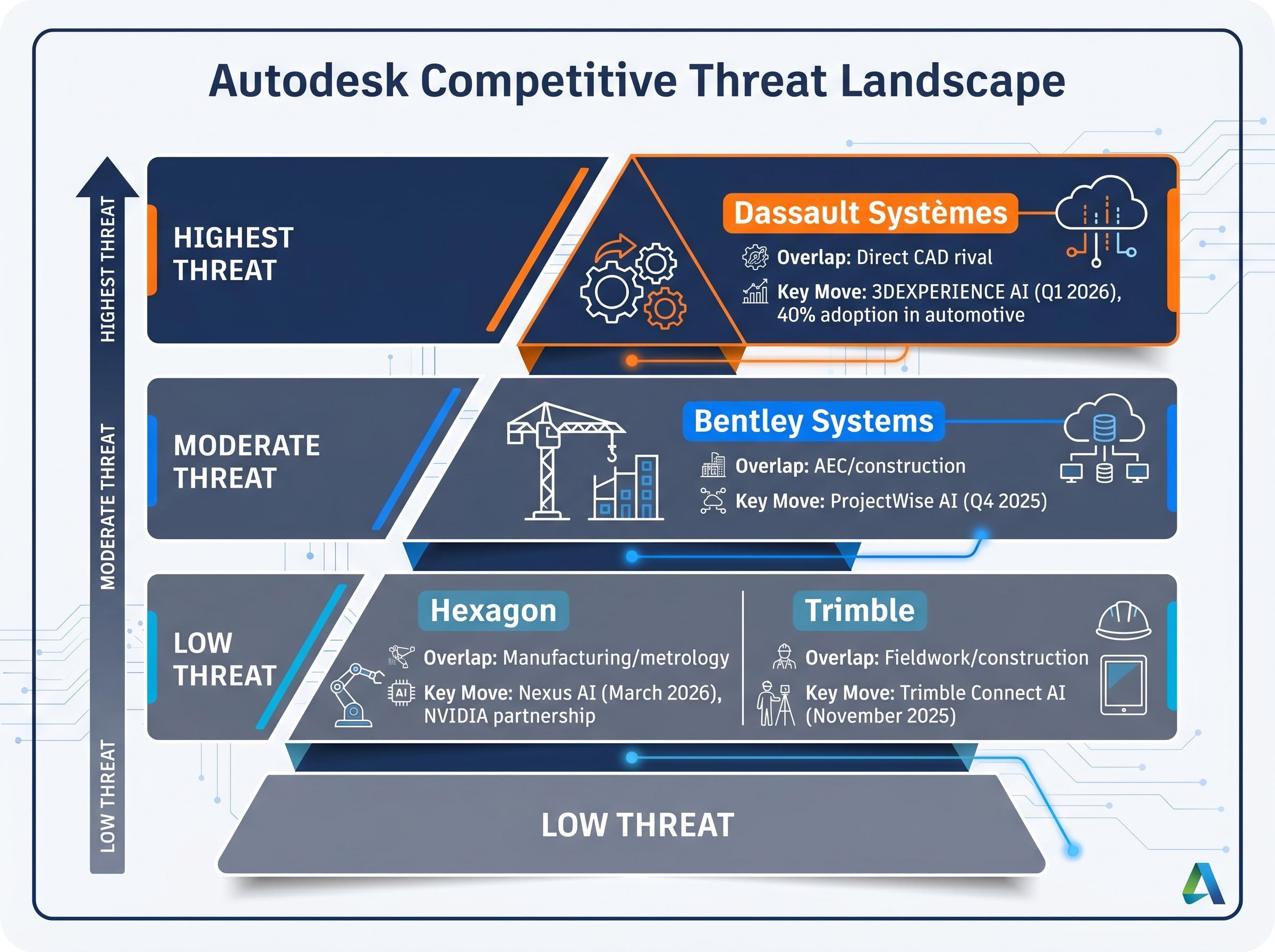

The competitive risk is real, but concentrated in a narrower set of rivals than the market narrative implies.

Generalist AI players are positioning as complements, not competitors. The actual threat surface sits within domain-specific CAD and AEC software firms, and even there, the risk is tiered.

Alphabet’s AI investment case illustrates why generalist AI platforms have attracted the capital rotation that has weighed on domain-specific software stocks: Google Cloud grew 63% year-over-year in Q1 2026, giving investors a high-growth AI narrative that does not require distinguishing between geometric and text-based model requirements.

| Competitor | Key AI move (2025-2026) | Overlap area | Threat level |

|---|---|---|---|

| Dassault Systèmes | 3DEXPERIENCE AI (Q1 2026): virtual twin generative AI; 40% adoption in automotive | Direct CAD rival | Highest; comparable data depth, but Autodesk leads in cloud AI adoption |

| Bentley Systems | ProjectWise AI (Q4 2025): generative infrastructure modelling | AEC/construction | Moderate; overlaps in infrastructure but smaller data scale |

| Hexagon | Nexus AI (March 2026): NVIDIA partnership for geometric AI | Manufacturing/metrology | Low; focused on measurement, not broad design |

| Trimble | Trimble Connect AI (November 2025): construction site optimisation | Fieldwork/construction | Low; niche in field operations, not design core |

Dassault is the only platform-level competitor with data depth approaching Autodesk’s, and even its 40% automotive sector adoption has not translated into gains across the broader AEC market where Autodesk’s cloud-native position is strongest. Bentley, Hexagon, and Trimble represent niche overlaps rather than platform-level threats.

Short interest data corroborates the receding fear. Short positions fell from approximately 3.2% in January 2026 to approximately 2.45-2.5% by 15 April 2026, suggesting the most aggressive bearish bets have been unwound.

The valuation case and where the thesis could still break

BofA’s $300 price target is built on a 21x CY2027 free cash flow multiple. The peer group trades at approximately 23x EV/FCF, meaning the target already prices in a modest discount. Closing that gap would require visible evidence that AI monetisation is additive to revenue rather than embedded within existing subscription pricing.

| Metric | BofA estimate | Peer group average |

|---|---|---|

| EV/FCF multiple | 21x (CY2027) | ~23x |

| Revenue growth (YoY) | 13%, then 10% | Varies by peer |

| Free cash flow | $2.4B (FY2026) → $2.8B (FY2027) | N/A |

JPMorgan upgraded Autodesk to Overweight with a $319 price target on 2 February 2026, corroborating the FCF growth thesis from a second major institution.

Workforce reduction adds near-term complexity. BofA cited approximately 15% headcount reduction over the twelve months prior to May 2026, though the publicly announced figure from January 2026 alone was approximately 7% (roughly 1,000 roles). The gap between these figures suggests additional attrition or phased cuts beyond the single announced event. Either way, H1 billings are expected to carry the drag, with a Q4 enterprise renewal cluster positioned as the recovery catalyst.

Where the bull case is most exposed

Three conditions must hold for the $300 target to be realised:

- H2 billings recover as the enterprise renewal cluster materialises in Q4

- Visible AI upsell revenue appears by Q1 FY2028, demonstrating that AI features expand average selling price rather than simply supporting retention

- Enterprise retention remains stable through the sales model transition, with no meaningful customer losses to Dassault or other rivals

Failure on any single condition does not collapse the thesis, but it resets the timeline for the peer discount to close.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The structural case holds, but the next 90 days are the proof point

The analytical case resolves into a clear shape. Autodesk’s moat, built on proprietary 3D data, geometric AI requirements, and a decade of domain investment, creates barriers that generalist AI cannot cross on a short timeline. Early monetisation signals point in the right direction, though they remain unverified at the public filing level. The competitive threat is concentrated in Dassault Systèmes rather than distributed across the broader AI market.

The current valuation gap (stock at $236 versus a consensus target of approximately $320 and 80% Buy ratings) reflects execution uncertainty, not fundamental doubt about the AI moat itself. Piper Sandler’s Overweight rating with a $361 price target (August 2025) marks the bull case upper bound.

Barron’s noted in its May 2026 preview coverage that Autodesk’s AI signals “warrant multiple expansion.”

Q1 FY2027 earnings on 28 May 2026 represent the verification moment. Three specific metrics deserve attention:

- AI feature adoption disclosures, particularly any update to the AutoConstrain figure or new Fusion 360 Generative Design metrics

- H1-to-H2 billings guidance revision, which will indicate whether the enterprise renewal cluster is materialising on schedule

- Premium tier pricing announcements, which would signal the transition from AI-as-retention to AI-as-revenue-expansion

Short interest at approximately 2.45-2.5%, down from 3.2% in January, suggests the market is drifting toward the bull case. The May 28 call will determine whether that drift is justified.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

—