Barclays Warns of Prolonged Market Volatility Under New Fed Reality

Jun 27, 2026

CSL shed A$9.48 billion in market capitalisation on 11 May 2026, closing at A$100.75 after a 15.96% single-day collapse that dragged the stock to a nine-year low. The fall followed a fourth guidance downgrade in approximately two years, delivered not through a scheduled results release but via an ASX filing tied to a 90-day interim CEO review. Both FY26 revenue and net profit after tax and amortisation (NPATA) were revised below prior-year figures, meaning CSL is no longer forecasting slower growth; it is forecasting an absolute decline. What follows breaks down the operational drivers behind the downgrade, the deep disagreement among brokers over what the stock is worth, and what the valuation picture looks like at the lowest multiple since 2017.

The mechanism of the announcement matters. This was not a quarterly earnings release. It was an ASX filing attached to interim CEO Gordon Naylor’s 90-day operational review, a format that signals unusual urgency from a board still searching for a permanent chief executive.

Revised FY26 guidance now sits at approximately US$15.2 billion in revenue and approximately US$3.1 billion in NPATA, both below the prior financial year. A non-cash impairment of approximately US$5 billion, spanning FY26 and FY27, was flagged across the Vifor iron deficiency portfolio. These are not marginal adjustments.

“Our growth initiatives are working, but the financial benefits will take longer than previously anticipated to materialise.” — Gordon Naylor, Interim CEO, ASX announcement, 11 May 2026

Placed in sequence, the pattern is stark. Goldman Sachs has characterised CSL’s trajectory as one of “repeated forecasting failures.” Four downgrades in roughly two years erodes more than earnings estimates; it erodes the institutional credibility that once made CSL a conviction holding across Australian portfolios.

Three distinct operational problems contributed to the revision, each with its own cause and scale.

US plasma collections grew modestly but fell short of internal targets. Labour shortages and under-utilisation of newly opened collection centres produced an estimated US$100 million revenue shortfall. The infrastructure exists; the throughput does not.

Hemgenix, CSL’s gene therapy for haemophilia B (co-developed with uniQure), delivered approximately US$150 million less revenue than forecast. Slower-than-expected US uptake and revised patient eligibility assumptions are the cited drivers.

The Vifor iron deficiency business, however, is the most acute wound. Acquired for US$11.7 billion in 2022, the portfolio now carries an approximately US$5 billion non-cash impairment driven by competition in iron deficiency treatments, Middle East supply disruption, and broader portfolio underperformance. That is roughly 43% of the original acquisition price written down in under four years.

| Business Segment | Estimated Impact | Primary Driver |

|---|---|---|

| US Plasma Collections | ~US$100M revenue shortfall | Centre under-utilisation, labour shortages |

| Hemgenix (Gene Therapy) | ~US$150M revenue impact | Slower US uptake, revised patient eligibility |

| Vifor / Iron Deficiency | ~US$5B non-cash impairment | Competition, supply disruption, portfolio underperformance |

| China Pricing (Immunoglobulins) | Not separately disclosed | Government tenders, reimbursement cuts |

JPMorgan flags China pricing pressure as an ongoing risk, though no standalone quantum has been disclosed. The impact is bundled into the broader CSL Behring growth deferral.

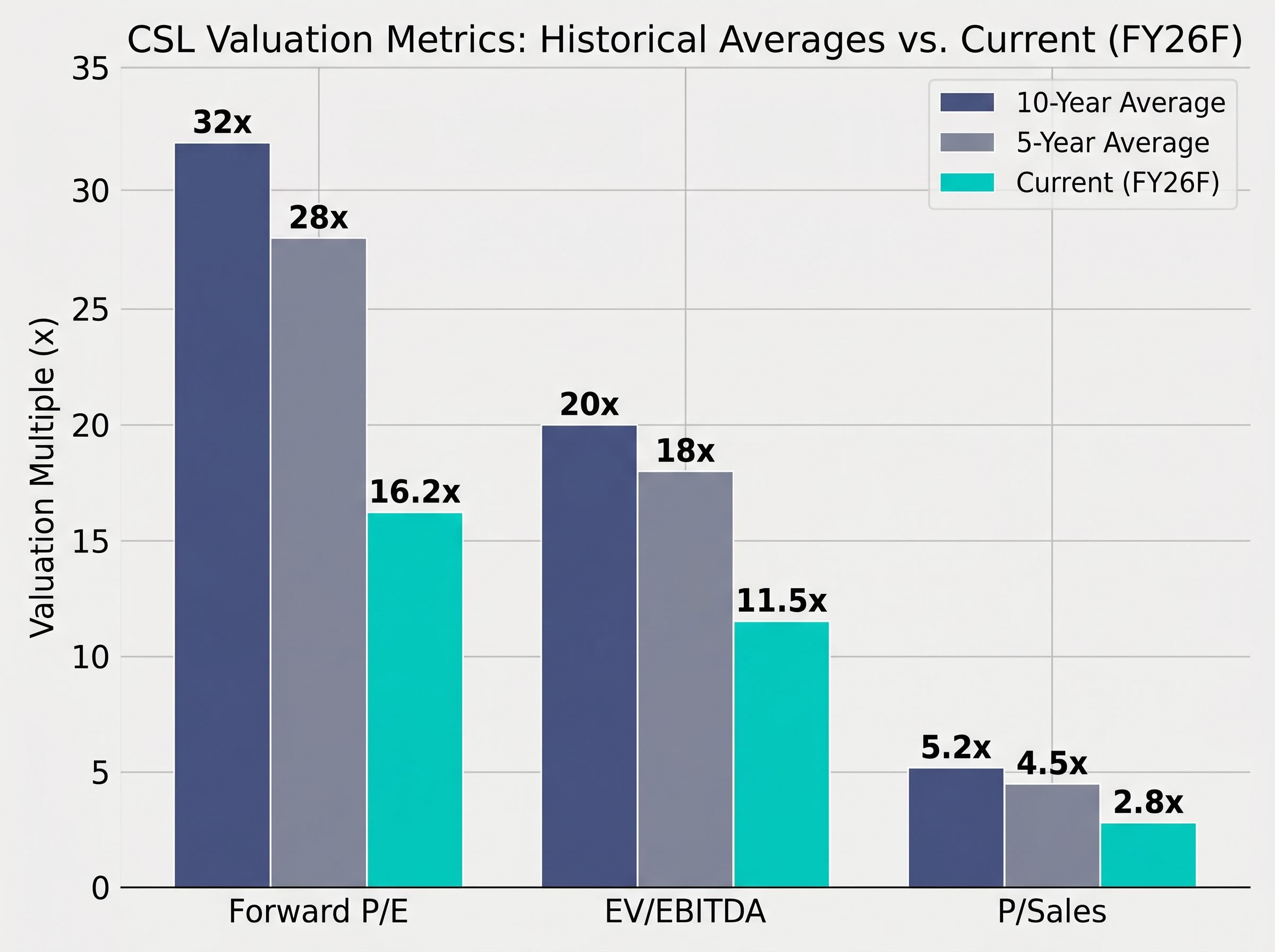

At A$100.75, CSL trades at approximately 16.2x forward price-to-earnings, a 40-50% discount to its five-year average of 28x and its ten-year average of 32x. The compression is visible across every valuation metric.

| Metric | Current (FY26F) | 5-Year Average | 10-Year Average |

|---|---|---|---|

| Forward P/E | 16.2x | 28x | 32x |

| EV/EBITDA | 11.5x | 18x | 20x |

| P/Sales | 2.8x | 4.5x | 5.2x |

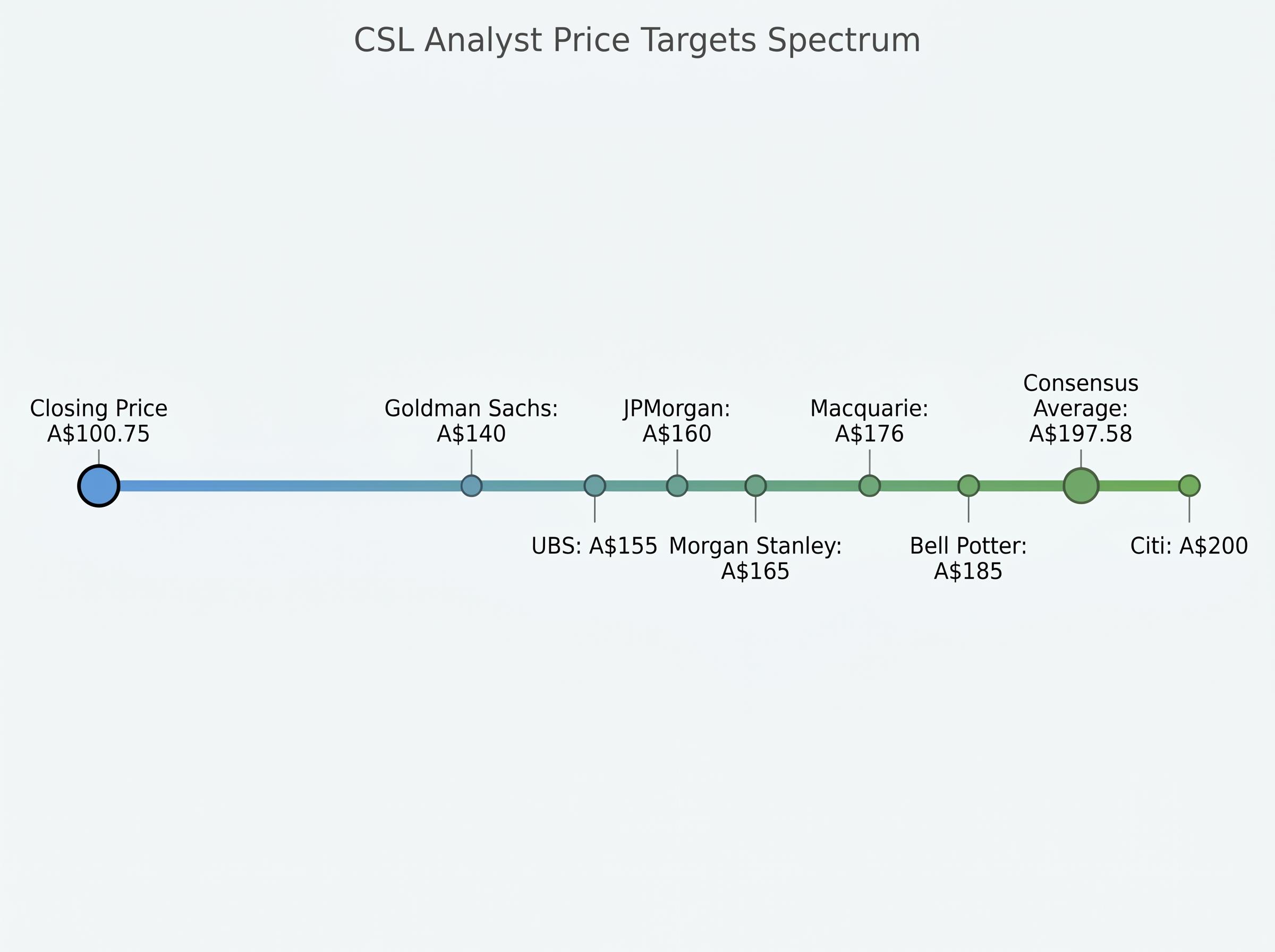

The consensus average broker price target sits at approximately A$197.58, implying roughly 96% upside from today’s close. The 12-month share price decline now stands at approximately 50%. Those numbers frame the debate, but they do not resolve it.

Citi maintains a Buy rating with a A$200 target, characterising the sell-off as a “buying opportunity” on a depressed valuation. Bell Potter holds a Speculative Buy at A$185, pointing to the durability of the plasma franchise moat and Seqirus outperformance. Both argue that 16x forward P/E on a business with 30% global plasma market share represents the most attractive entry point in nearly a decade.

Goldman Sachs, downgraded to Sell with a A$140 target (from A$190), cites “repeated forecasting failures” and Vifor “value destruction.” UBS maintains its Sell rating at A$155, highlighting margin compression and plasma underperformance. Macquarie describes an “information void” on growth drivers, while the interim CEO status introduces leadership uncertainty that makes forward estimates harder to anchor.

Plasma-derived therapies include immunoglobulins (used to treat immune deficiencies), albumin (used in critical care), and clotting factors (used for haemophilia). These products are manufactured from human blood plasma, which must be physically collected from donors, processed in specialised facilities, and approved through lengthy regulatory pathways.

Three features create the competitive barrier:

CSL holds approximately 30% global market share in plasma therapies and operates one of the largest US collection networks. That network cannot be replicated quickly.

Whether the moat is still intact is testable. Grifols reported Q1 2026 results showing plasma collections up approximately 15% year-on-year with full-year guidance maintained; shares rose approximately 2%. Takeda’s most recent guidance reaffirmation indicated mid-single-digit plasma revenue growth. The category itself is not in decline. CSL’s underperformance appears company-specific, rooted in execution lags rather than structural deterioration of the plasma market.

Seven brokers published updated positions following the 11 May announcement. The consensus rating remains Buy, but the target range of A$140 to A$200 against a A$100.75 close represents an unusually wide analytical dispersion.

| Broker | Rating | Price Target | Key Rationale | Prior Target |

|---|---|---|---|---|

| Citi | Buy | A$200 | Buying opportunity, depressed valuation | A$200 |

| Bell Potter | Speculative Buy | A$185 | Oversold; plasma moat intact | A$185 |

| Macquarie | Neutral | A$176 | Information void on growth drivers | Trimmed |

| Morgan Stanley | Equal-weight (downgraded) | A$165 | FY26 EPS cut 18% to US$5.80 | A$210 |

| JPMorgan | Underweight | A$160 | China pricing ongoing risk | Slight trim |

| UBS | Sell | A$155 | Margin compression, NPATA US$3.05B | A$172 |

| Goldman Sachs | Sell (downgraded) | A$140 | Repeated forecasting failures | A$190 |

Morgan Stanley’s downgrade from Overweight to Equal-weight stands as the most significant rating change, accompanied by an 18% EPS cut to US$5.80 and a target reduction from A$210 to A$165.

The retrospective analysis is clear. The forward question is harder: does a nine-year low on one of the ASX’s most widely held stocks represent a buying opportunity or a warning?

Three specific outcomes would begin to resolve the debate:

The next definitive data point: CSL’s August 2026 full-year results will either partially restore management credibility or confirm a fifth consecutive downgrade.

The superannuation dimension adds urgency. CSL typically represents approximately 1-2% of major Australian super fund portfolios, including AustralianSuper and peers. The 15.96% fall carries direct relevance for retail investors even if they do not hold the stock directly. Total ASX turnover in CSL on 11 May 2026 reached approximately A$2.5 billion across roughly 4.94 million shares.

The ASX healthcare sector index fell 6.47% on the session, though smaller names including 4DMedical (+7.2%), Neuren Pharmaceuticals (+4.6%), and Cochlear (+1.2%) posted gains as apparent rebalancing beneficiaries.

Four guidance downgrades in two years is not just a CSL problem. It is a signal that institutional investors may reprice leadership credibility and forecasting accuracy more aggressively across large-cap healthcare names.

The underlying franchise has not collapsed. The plasma collection network, Seqirus vaccine operations, and CSL Behring’s core immunoglobulin business remain structurally intact. This is an execution and credibility crisis, not a fundamental business failure. The Vifor acquisition, purchased for US$11.7 billion in 2022 and now carrying an approximately US$5 billion impairment, stands as the most visible evidence of capital allocation failure, a factor Goldman Sachs labelled “value destruction.”

The 6.47% fall in the ASX healthcare sector index on 11 May demonstrates CSL’s weight on the broader sector. When a single stock can drag the index that far, its trajectory becomes a sector-level event.

Consensus average broker price target: approximately A$197.58, implying roughly 96% upside from A$100.75. That target is only credible if the August 2026 results mark a genuine inflection rather than a fifth downgrade.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

CSL issued its fourth guidance downgrade in approximately two years via an ASX filing tied to interim CEO Gordon Naylor's 90-day operational review, revising FY26 revenue and NPATA below prior-year figures, alongside a roughly US$5 billion non-cash impairment on the Vifor iron deficiency portfolio.

Plasma-derived therapies are medicines manufactured from human blood plasma, including immunoglobulins, albumin, and clotting factors; CSL holds approximately 30% global market share in this category, creating a significant competitive moat due to the high cost and time required to build donor networks and fractionation facilities.

Broker price targets range from A$140 (Goldman Sachs, Sell) to A$200 (Citi, Buy), with a consensus average of approximately A$197.58, implying roughly 96% upside from the A$100.75 close, though Goldman Sachs and UBS remain sellers citing repeated forecasting failures and margin compression.

At A$100.75, CSL trades at approximately 16.2x forward price-to-earnings, a 40-50% discount to its five-year average of 28x and its ten-year average of 32x, representing the lowest valuation multiple since 2017.

Investors should monitor plasma utilisation rates recovering in H2 FY26, improving Hemgenix uptake data, a permanent CEO appointment, and CSL's August 2026 full-year results, which will either partially restore management credibility or confirm a fifth consecutive downgrade.