Woolworths: Strong Sales, Shrinking Profits, Slim Upside

14 mins ago

Palantir reported the strongest quarter in its public company history on 4 May 2026, then watched its stock fall nearly 6% the next day, erasing roughly $20 billion in market value. The disconnect demands more than a shrug.

A company posting an 85% year-over-year revenue increase, a 46% GAAP operating margin, and a Rule of 40 score of 145% is not stumbling. It is compounding at a rate that very few software businesses at this scale have achieved. Yet the market’s response, a swift $20 billion repricing, signals something more structural than a single day of profit-taking. At approximately 40x forward revenue, even a genuinely exceptional quarter may already be embedded in the price.

This analysis unpacks why Palantir stock delivered extraordinary numbers, what the sell-off reveals about valuation risk at extreme growth multiples, and what forward indicators are worth monitoring before drawing conclusions from either the bull or bear case.

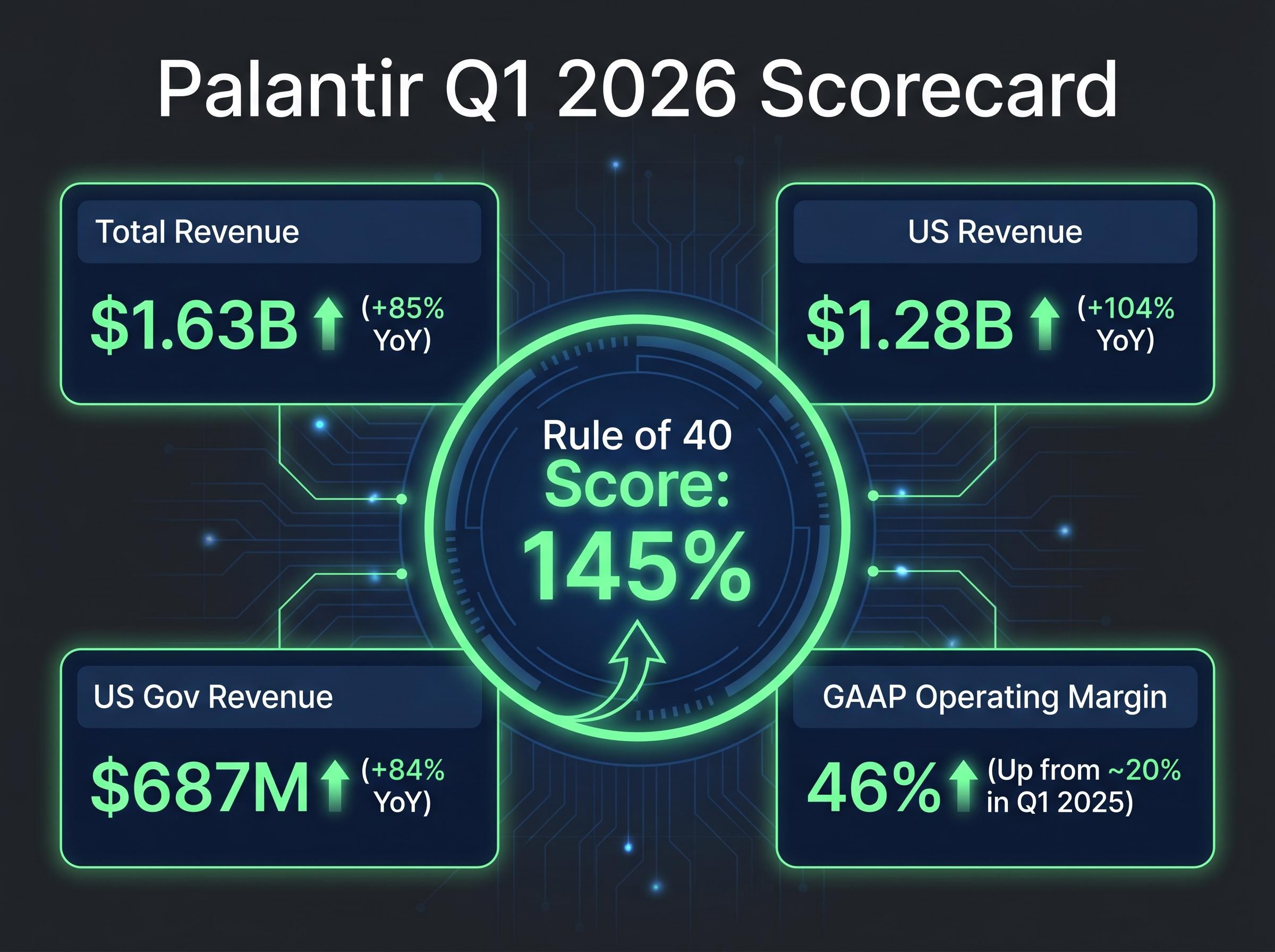

The headline figures speak for themselves. Palantir posted $1.63 billion in total revenue for Q1 2026, up 85% year-over-year. US revenue reached $1.28 billion, a 104% increase that reflects both new customer additions and deepening spend from the existing base.

US government revenue hit $687 million, up 84% year-over-year. US commercial customer count climbed to 615, a 42% year-over-year increase. Remaining performance obligations stood at $4.45 billion ($1.75 billion short-term, $2.70 billion long-term), providing considerable revenue visibility regardless of new bookings pace.

GAAP operating margin jumped to 46%, up from approximately 20% in Q1 2025. That is not incremental improvement. It is operating leverage compressing costs at the same time revenue is accelerating, a combination that rarely sustains at scale. GAAP earnings per share came in at $0.34, beating the $0.28 consensus estimate by 21.4%.

Management raised FY 2026 guidance to 71% total revenue growth, with US commercial guidance lifted to 120% year-over-year growth.

| Metric | Q1 2025 | Q1 2026 | Y/Y Change | vs. Consensus |

|---|---|---|---|---|

| Total Revenue | $884M | $1.63B | +85% | Beat |

| US Revenue | ~$627M | $1.28B | +104% | Beat |

| US Gov. Revenue | ~$373M | $687M | +84% | Beat |

| GAAP Operating Margin | ~20% | 46% | +26 ppts | Record |

| GAAP EPS | — | $0.34 | — | +21.4% beat |

Rule of 40 score: 145%. The Rule of 40, a widely used software industry benchmark that sums revenue growth and operating margin, typically considers a score above 40 as healthy. Palantir’s 145% is more than triple the threshold, placing it among the strongest readings any publicly traded software company has reported in a single quarter.

Palantir shares dropped from $146.03 to $137.43 on 5 May, a decline of approximately 5.9%, erasing roughly $20 billion in market capitalisation. The stock was already down approximately 22.47% year-to-date as of 10 May 2026, meaning the post-earnings dip was not an isolated event but part of a multi-month repricing of the growth premium.

The central variable is the forward revenue multiple. At approximately 40x forward revenue with a market capitalisation of roughly $330.35 billion, the current price embeds expectations so far ahead of reported results that even a blowout quarter can arrive as priced in. For context, Palantir traded at approximately 7x revenue during its 2023 trough and reached approximately 100x at peak.

Historical data adds a sobering frame: companies trading at or above 30x revenue have historically delivered below-average investor returns over subsequent five-year periods. Even the most optimistic long-term scenarios struggle to generate outsized returns from the current entry price.

The answer to why the stock fell on record earnings is that valuation, not fundamentals, is doing the most work in the near-term price signal.

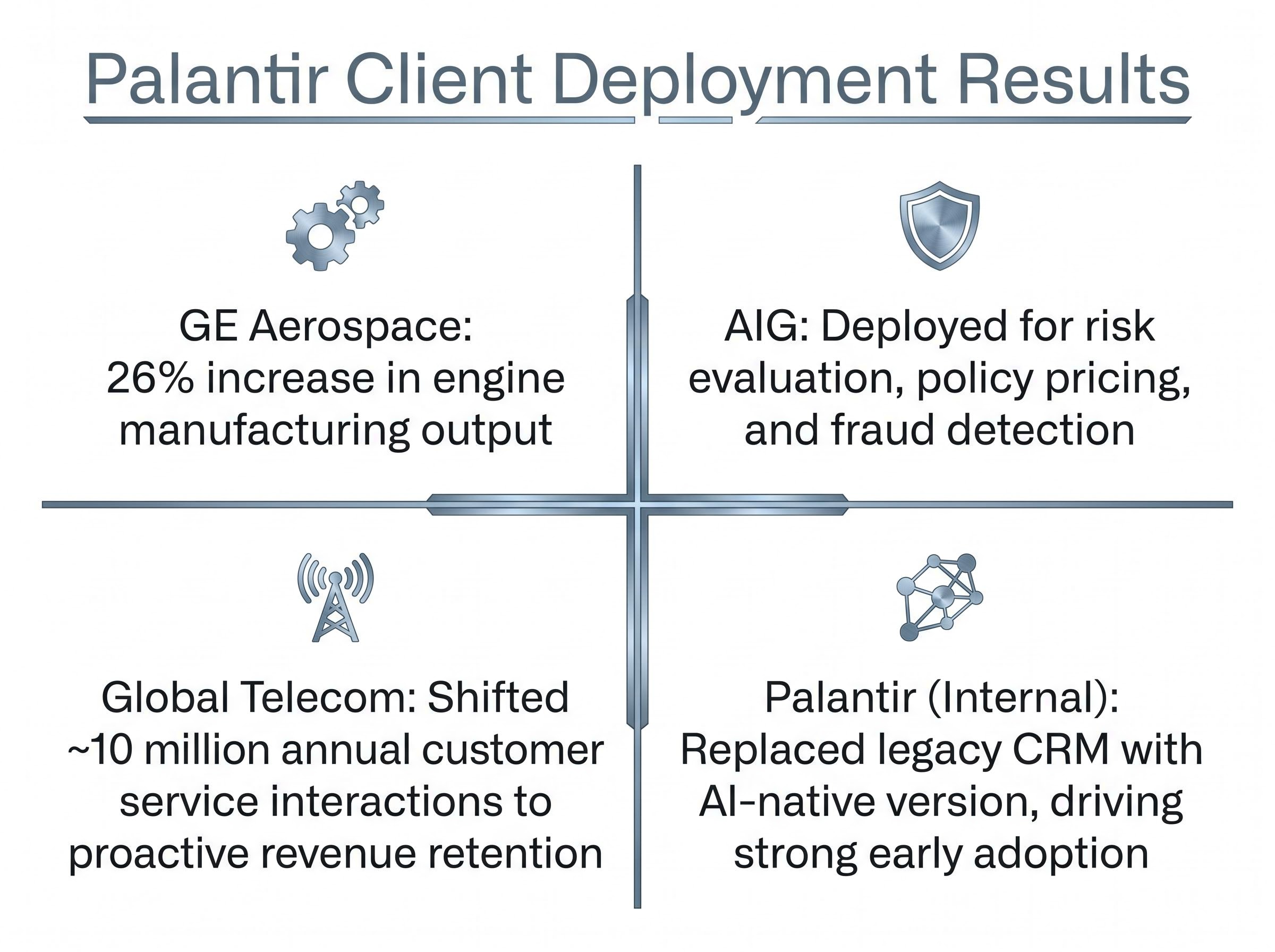

Palantir does not sell a chatbot or a model wrapper. The company builds what it calls an ontology layer: software that embeds itself into a client’s data architecture, access permissions, and workflow logic. Rather than sitting on top of existing systems as a generic AI application, it becomes the integration and governance infrastructure through which an organisation’s data is organised, permissioned, and acted upon.

The target customer profile is deliberate. Palantir focuses on load-bearing institutions in military, energy, healthcare, and financial sectors, organisations where switching costs are high, audit requirements are strict, and the consequences of a failed deployment are severe. Management has argued that deploying an OpenAI or Anthropic model does not replace what Palantir does, because the value sits in the integration layer and governance infrastructure, not the underlying AI model itself.

The client results offer a window into how that argument translates operationally:

Growth rate contrast: Accenture, a comparable enterprise technology partner, is growing at approximately 8%. Palantir’s US commercial business is growing at 104% year-over-year. The divergence underscores the velocity of adoption, though whether it can sustain at this pace remains the open question.

The concern that OpenAI and Anthropic are competing directly for Palantir’s enterprise contracts has become a recurring theme in post-earnings commentary, contributing to sentiment headwinds even as the operational results accelerate. The logic is straightforward: if foundation model providers begin offering enterprise deployment tools, the integration work Palantir specialises in could eventually face commoditisation pressure.

As of 10 May 2026, however, no specific named enterprise deal lost to OpenAI or Anthropic has been independently verified. The threat is a credible long-term concern rather than a documented short-term loss. A related bear case sub-argument suggests that once Palantir completes an initial AI deployment for a client, lower-cost consultants could maintain the transformed operations, reducing the platform’s ongoing value.

Michael Burry held PLTR put options in 13F filings covering 2024. His Q1 2026 13F filing (covering positions as of 31 March 2026) was not yet public as of 10 May, with the SEC deadline of approximately 15 May 2026 approaching. No media coverage or SEC disclosures in the May 2026 window confirm a notable position change.

Peer performance provides useful context. The broader AI sector did not share Palantir’s sell-off: the BOTZ AI infrastructure ETF was up approximately 0.96% on 5 May, reinforcing that PLTR’s decline is largely idiosyncratic.

| Company | YTD Performance | Forward Multiple | Key Risk Factor |

|---|---|---|---|

| Palantir (PLTR) | -22.47% | ~40x revenue | Premium multiple compression |

| Snowflake (SNOW) | ~-35.7% | ~25x revenue | AI monetisation slowdown |

| C3.ai (AI) | ~-35% | ~30x revenue | Severe valuation reset |

Snowflake and C3.ai have experienced steeper year-to-date declines than Palantir, suggesting Palantir has held up relatively better among comparable AI software names despite its post-earnings dip.

The analyst consensus reflects a market that is broadly constructive but genuinely divided. Of 19 analysts covering Palantir, 13 rate it Buy, 4 Hold, and 2 Sell, producing a Moderate Buy consensus with an average price target of $187.56. The range between the $70 floor and $255 ceiling reflects a real methodological disagreement about how to discount a high-growth AI platform at this scale.

Rosenblatt Securities analyst John McPeake raised his price target from $200 to $225 on 5 May, maintaining a Buy rating and calling it “one of the strongest quarters in Palantir’s public history.”

No new downgrades were issued in the 48-72 hours following the earnings release. The two existing Sell-rated analysts were not newly initiated post-earnings.

The analytical variable dividing bulls and bears is not revenue growth; both sides largely accept Palantir is growing fast. The disagreement centres on the appropriate forward multiple at which that growth should be capitalised.

Bull case pillars:

Bear case pillars:

Retail sentiment mirrors the split: approximately 60% characterise the dip as a buying opportunity, while roughly 40% cite valuation and AI commoditisation risk as justifying the correction.

Palantir’s operational performance is objectively exceptional by almost any software industry benchmark. An 85% revenue growth rate, a 46% GAAP operating margin, and a 145% Rule of 40 score at $1.63 billion in quarterly revenue place the company in rare company. But exceptional performance and exceptional stock returns are not the same thing when the entry price already embeds extreme expectations.

Three forward variables will determine whether the current multiple is justified or not over the next two to three years:

Two near-term filings are worth tracking:

FY 2026 guidance of 71% total revenue growth and RPO of $4.45 billion provide near-term revenue visibility, but the stock’s direction hinges on the variables above, not on whether the next quarter beats consensus.

The sell-off on record earnings is not evidence that markets are broken or that Palantir is overrated. It is evidence that at 40x forward revenue, the margin for pricing in future disappointment is extremely narrow, even for genuinely exceptional businesses.

The most common analytical error in high-growth technology investing is conflating “is this a great company?” with “is this a great stock at this price?” Palantir’s Q1 2026 results make a strong case for the former. The latter depends on variables that a single quarter, however strong, cannot resolve.

The coming quarters, particularly Q2 2026 results, will test whether the raised guidance was conservative or aspirational. Investors tracking Palantir stock should review the Q1 2026 10-Q and monitor the upcoming Scion 13F for additional context before drawing conclusions about near-term price direction.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Rule of 40 is a software industry benchmark that adds a company's revenue growth rate to its operating margin; a score above 40 is considered healthy. Palantir's score of 145% in Q1 2026 is more than triple that threshold, placing it among the strongest readings any publicly traded software company has ever reported in a single quarter.

Palantir shares fell approximately 5.9% on 5 May 2026 because the stock was trading at roughly 40x forward revenue, a valuation so elevated that even a record-breaking quarter was already priced in, leaving little room for upside surprise.

Palantir's ontology layer is software that embeds itself into a client's data architecture, access permissions, and workflow logic, acting as integration and governance infrastructure rather than sitting on top of existing systems as a generic AI application. This approach targets high-switching-cost institutions in sectors like defence, energy, and healthcare.

Key indicators to watch include the Q1 2026 10-Q filing due around 10 May 2026, the Scion Asset Management 13F due around 15 May 2026, the durability of US commercial revenue growth at 104% year-over-year, and whether the 46% GAAP operating margin holds or compresses under competitive pressure.

At approximately 40x forward revenue, Palantir trades at a significant premium; historical data shows that companies trading at or above 30x revenue have typically delivered below-average investor returns over subsequent five-year periods, even when their underlying businesses perform well.