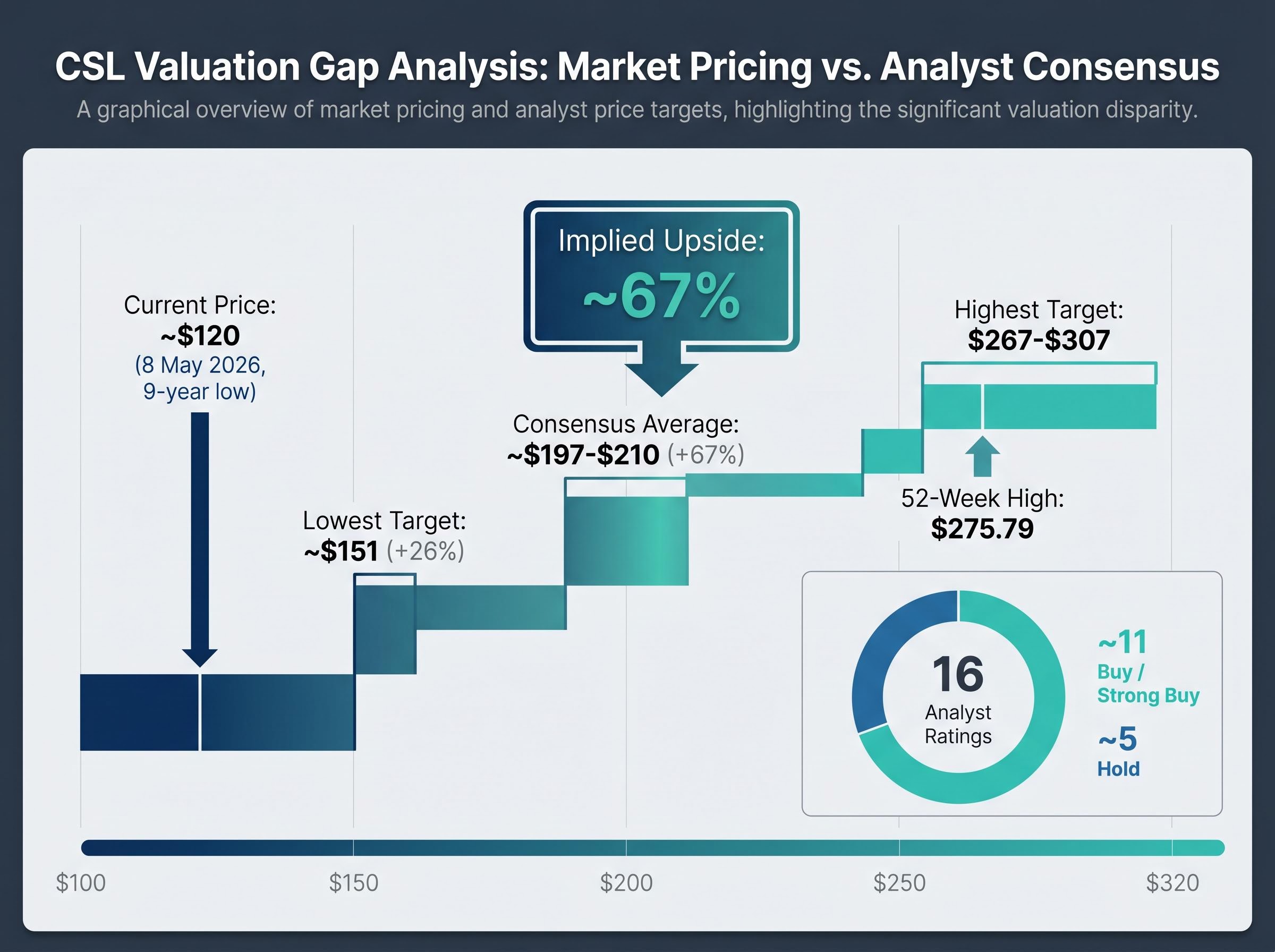

CSL shares closed at approximately $120 on 8 May 2026, a 9-year low. The analyst consensus price target sits near $200, implying roughly 67% upside from a stock that has lost more than half its value from its peak of $275.79.

That gap between where the market is pricing CSL and where analysts believe it should trade is either the clearest buying opportunity on the ASX or a sign that consensus has not yet fully repriced a business facing compounding headwinds. The answer carries weight: CSL remains one of Australia’s largest healthcare companies by market capitalisation, and its trajectory over the next 12-18 months will be shaped by the resolution of at least four simultaneous pressures, from divisional performance divergence and a leadership vacuum to restructuring execution and guidance compression.

This analysis maps each of those pressures against available data, surfaces the specific conditions under which the bull case holds, identifies where the bear risks are most credible, and provides a structured framework for evaluating the stock ahead of the August 2026 full-year results.

The valuation gap that defines the current investment case

The arithmetic is striking. CSL trades at approximately $120, down roughly 56% from its 52-week high of $275.79 and approximately 24% year-to-date. The company’s market capitalisation has compressed to approximately $58-$59 billion. Against that, the analyst consensus average price target ranges from approximately $197 to $210, implying upside of roughly 67% from current levels. The most bullish targets stretch to $267-$307, or 120-155% above the current price. Even the lowest tracked target of approximately $151 implies 26% upside.

The core statistic: Analyst consensus implies approximately 67% upside from a share price that just hit a 9-year low, the widest gap between market pricing and sell-side conviction CSL has seen in over a decade.

Across tracked analyst panels, approximately 11 analysts maintain Buy or Strong Buy ratings, against 5 Holds. No explicit large-house downgrades have been confirmed since January 2025, though broker-specific reports from Macquarie, UBS, and Morgan Stanley were not accessible for verification.

| Rating Category | Number of Analysts | Price Target Range | Implied Upside from $120 |

|---|---|---|---|

| Buy / Strong Buy | ~11 | $197-$307 | ~67%-155% |

| Hold | ~5 | $151-$189 | ~26%-58% |

The size of this dislocation determines the analytical work required. If consensus is correct, CSL at $120 represents one of the more asymmetric setups on the ASX. If consensus is anchored to a business model that has durably changed, the gap is noise. The sections that follow test which reading the evidence supports.

The macro and structural headwinds in ASX healthcare extend beyond the currency and rate factors that dominate most analyst commentary; CSL’s approximately 45% weighting in the S&P/ASX 200 Health Care Index means its vaccine franchise deterioration from declining US vaccination rates represents an index-level risk, and the distinction between cyclically reversible headwinds and structurally permanent ones determines whether current consensus price targets are anchored to a recoverable baseline.

When big ASX news breaks, our subscribers know first

What CSL Behring’s plasma franchise actually represents for the recovery thesis

The majority of analysts have not abandoned their Buy ratings despite a sustained sell-off, and the reason is a single division: CSL Behring, the company’s plasma-derived immunoglobulin franchise and the structural foundation of the long-term bull case.

The global plasma-derived therapies market was estimated at approximately $52 billion in 2025, with projections indicating it could reach approximately $104 billion by 2033, representing a compound annual growth rate (CAGR) of roughly 8-9%. CSL Behring is described as the global leader in plasma-derived immunoglobulins, the products at the centre of that growth.

Three structural characteristics differentiate plasma-derived therapy demand from most pharmaceutical revenue streams:

- Chronic disease dependency: The patient base relies on ongoing, repeat infusions for conditions such as primary immunodeficiency, where treatment is lifelong rather than episodic.

- Limited therapeutic substitutes: Plasma-derived immunoglobulins have no widely available synthetic or biosimilar equivalents, creating a supply-constrained market with durable pricing characteristics.

- Recurring volume growth: An ageing global population and improving diagnosis rates in emerging markets contribute to consistent year-on-year volume increases.

PMC research on immunoglobulin replacement therapy confirms that treatment for primary immunodeficiency disorders is ongoing rather than episodic, with patients unable to produce sufficient immunoglobulin requiring continuous infusion regimens that cannot be substituted by biosimilar equivalents under current regulatory licensing frameworks.

CSL Behring’s historical plasma franchise growth rate of approximately 15-20% is the primary basis analysts cite for maintaining a normalised price-to-earnings (PE) ratio of roughly 25x. That historical growth rate is also the benchmark against which future results will be measured; if the plasma franchise can sustain even mid-single-digit growth through the current headwind cycle, it provides the earnings trajectory that justifies current consensus targets.

A US tariff exemption for plasma therapies, confirmed under the Section 232 pharmaceutical import proclamation with an effective date of 29 September 2026, removed one potential headwind from the franchise’s near-term revenue trajectory, while CSL Seqirus’ Fluad vaccine faces a residual 10% tariff from UK manufacturing that is expected to reduce to zero.

Understanding why Seqirus has become the pivot point for near-term sentiment

Seqirus, CSL’s influenza vaccine division and the world’s second-largest influenza vaccine producer, is the specific mechanism through which the company’s 2025-2026 underperformance becomes legible. The division’s trajectory traces a clear chain of accumulating pressure.

The sequence unfolded in four stages:

- US vaccine demand softness emerged through the 2024-2025 period, reducing volume expectations for the division.

- Pricing pressure compounded the volume shortfall, compressing revenue per dose.

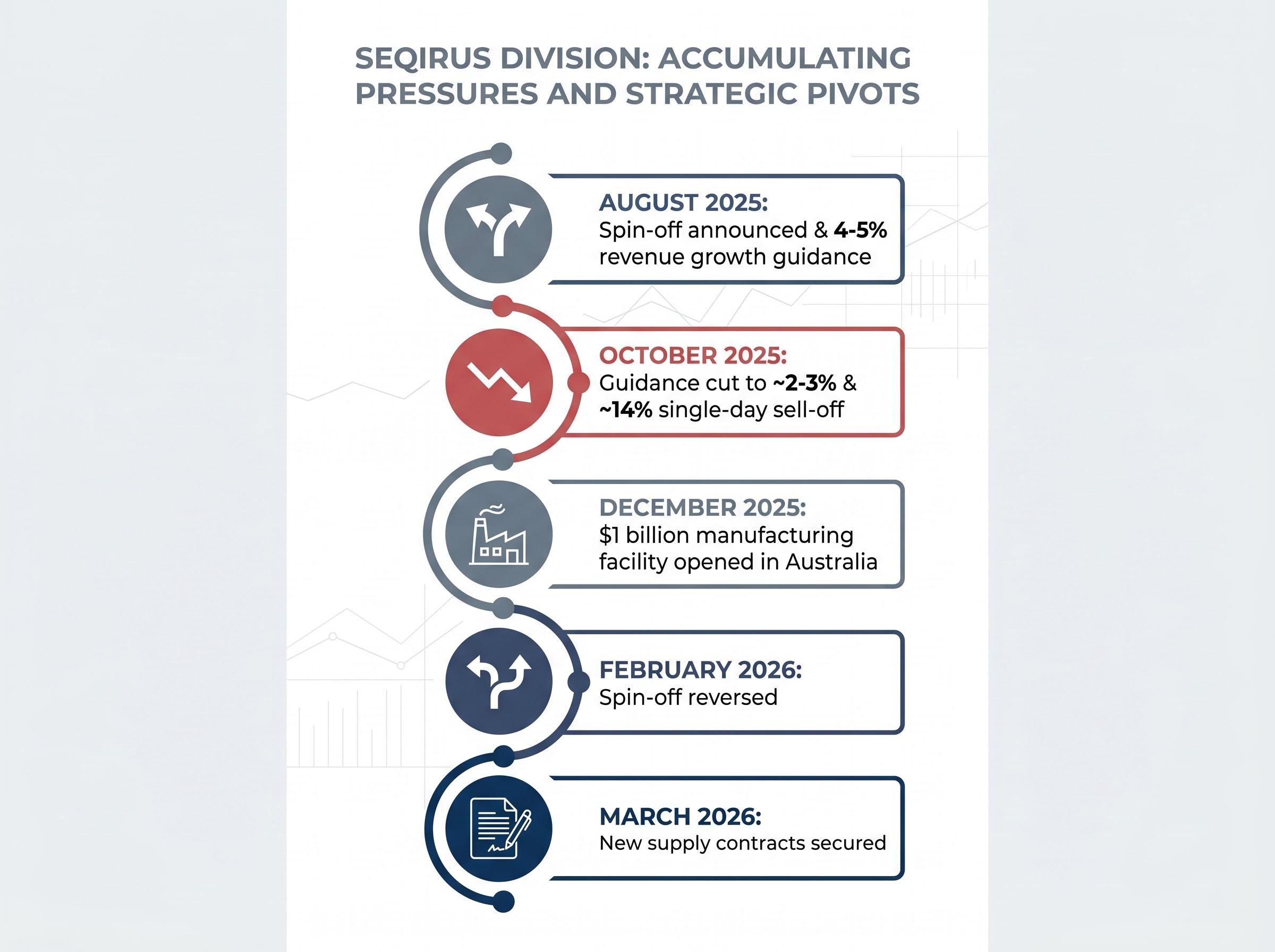

- The October 2025 guidance cut revised CSL’s revenue growth outlook to approximately 2-3%, down from the 4-5% guidance issued in August 2025. The market’s response was immediate: a single-day sell-off of approximately 14%.

- The spin-off reversal in February 2026 scrapped the Seqirus separation that had been announced just six months earlier in August 2025, introducing strategic uncertainty about the division’s role within the group.

The October 2025 guidance revision: Revenue growth cut to approximately 2-3% (from 4-5%), with NPATA growth falling materially below the original 7-10% target. This single data point triggered the sharpest single-day decline in CSL’s recent history.

Against this backdrop, CSL has doubled down rather than retreated. A new $1 billion manufacturing facility opened in December 2025 in Australia, producing influenza vaccines and antivenom. New supply contracts were secured in March 2026. These capital commitments carry a dual interpretation: they signal strategic conviction in Seqirus’s long-term value, or they represent capital allocation risk if US vaccine demand does not stabilise.

The division’s trajectory is the most direct variable investors can monitor in the months ahead.

The cost programme and leadership change: restructuring risk or recovery catalyst?

CSL announced a US$550 million cost reduction programme in August 2025, accompanied by a workforce reduction of up to 15%. By the first half of FY26, approximately 60% of targeted savings had been achieved, with an approximate $100 million savings goal set for FY26.

| Metric | Target | Status (H1 FY26) | Investor Implication |

|---|---|---|---|

| Total cost savings | US$550M | ~60% achieved | Execution on track; final 40% is the test |

| FY26 savings target | ~$100M | In progress | Narrow relative to earnings guidance compression |

| Workforce reduction | Up to 15% | Underway | Restructuring headwinds reported as easing |

The $100 million FY26 savings target, while a positive execution signal, is narrow relative to the scale of the earnings guidance compression. Whether the programme delivers enough to visibly improve margins by full-year results remains the open question.

The leadership transition

Paul McKenzie retired as CEO on 10 February 2026. Gordon Naylor, former President of Seqirus, was appointed interim CEO effective immediately. Naylor’s operational background across both major divisions provides relevant credentials, though the timing of the transition, ahead of scheduled earnings, amplified investor concern.

No permanent CEO appointment had been confirmed as of early May 2026. This matters because an active restructuring phase, combined with the strategic reversal on the Seqirus spin-off, requires capital allocation decisions that interim leadership may be less willing to make decisively. Investors monitoring CSL through its August 2026 full-year results should watch for two signals: the cost programme’s final-year execution rate, and whether a permanent CEO appointment crystallises before or alongside the results announcement.

Naylor’s appointment as interim CEO was structured with performance-linked equity vesting, aligning his incentives with shareholder outcomes through the transition period and signalling that the board prioritised continuity over external disruption at a moment when the cost programme and Seqirus strategic reset both required sustained execution focus.

Bull case versus bear case: what each side needs to be right

The strongest version of the bull case rests on three conditions. The strongest version of the bear case requires three specific failure modes. Neither side needs to be entirely right for the stock to move materially.

| Bull Case Conditions | Bear Case Conditions |

|---|---|

| Plasma franchise growth reaccelerates toward historical 15-20% rate in FY27 | Seqirus drag persists beyond FY26, compressing group revenue growth below 3% |

| Cost programme delivers full US$550M savings on schedule, visibly improving margins | $100M FY26 savings prove insufficient to offset earnings guidance compression |

| Valuation floor holds at ~25x normalised PE, supported by analyst consensus near $200 | Interim leadership creates execution gaps during a period requiring decisive capital allocation |

The number that separates the two cases: FY26 revenue growth guidance of approximately 2-3%. If the August results confirm growth at or above the top end of that range, the recovery thesis gains credibility. If growth lands below the bottom end, further analyst downgrades become likely.

The financial backdrop provides context for both sides. CSL reported FY25 revenue of approximately US$15.56 billion (+5.12% year-on-year) and net earnings of approximately US$3.00 billion (+13.63%). The balance sheet carries a 62.8% debt-to-equity ratio, which limits the company’s ability to respond aggressively to further deterioration, a constraint the bear case emphasises. Return on equity sits at 14.6%, and the dividend yield has averaged approximately 1.5% over the past five years.

The clazakizumab licensing deal with Eli Lilly, which delivered a $100 million upfront cash injection while preserving CSL’s exclusive cardiovascular development rights in end-stage kidney disease, illustrates the balance sheet lever available to the company: non-dilutive capital that supports ongoing Phase 3 development without adding to a debt-to-equity ratio already sitting at 62.8%.

The asymmetry of the setup (approximately 67% upside implied by consensus, but material downside if the growth reacceleration thesis fails in FY27) means the entry decision is less about whether CSL is a quality business and more about timing and risk tolerance relative to the August 2026 results.

What the August 2026 results will need to show for the recovery thesis to hold

The next scheduled results, approximately 18 August 2026, represent the clearest near-term evidence point for Australian investors evaluating CSL at current levels. Four specific metrics will confirm or challenge the recovery thesis:

- Plasma volume growth rate: The historical benchmark of 15-20% is the standard against which FY26 actuals will be measured. Even mid-single-digit growth would signal the franchise’s structural demand is intact.

- Seqirus revenue trajectory: Stabilisation in US vaccine demand, or evidence that the new manufacturing facility and March 2026 supply contracts are contributing to revenue, would reduce the division’s drag on sentiment.

- Cost programme execution: Confirmation that the approximately $100 million FY26 savings target was achieved, with visibility on the remaining 40% of the broader programme.

- Permanent CEO appointment: Whether a permanent successor to Paul McKenzie is named before or alongside the results will signal the board’s confidence in its strategic direction.

Analyst consensus remains predominantly bullish, with the majority of Buy ratings and an average target near $200 intact as of May 2026 despite the sustained sell-off. FY26 NPATA growth guidance has been indicated in the range of 4-7%, though this figure has not been precisely confirmed across all available sources and should be verified against CSL’s investor relations filings.

FY26 NPATA growth guidance has been indicated in the range of 4-7%, and the CSL investor relations filings covering the Half Year Results to December 2025 confirm the company’s maintained revenue growth guidance of 2-3%, providing the primary reference point against which August full-year actuals should be measured.

The thesis does not require perfection. It requires the data to confirm that the worst of the guidance compression is behind the company, not still ahead of it. Investors with a short time horizon face a different risk profile than those willing to hold through FY27, where the plasma market’s structural growth trajectory should be more visible in earnings.

A 9-year low and a 67% consensus upside: what that gap is really telling investors

CSL at $120 is not obviously cheap, and it is not obviously a trap. It is a high-quality business at a genuine inflection point where the outcome depends on specific, observable variables: whether the plasma franchise’s structural growth reasserts itself in FY27, whether Seqirus stabilises or continues to drag, whether the cost programme’s final execution delivers margin improvement, and whether permanent leadership is installed to steer capital allocation decisions.

The 67% upside implied by analyst consensus reflects conviction that the franchise value is intact beneath the current noise. The 56% decline from peak reflects a market that has spent months repricing a business whose near-term earnings trajectory has materially deteriorated. Both readings carry evidence.

For investors assessing whether to initiate a position at current levels, the August 2026 full-year results are the nearest catalyst that could validate or challenge the thesis. For those already holding, the question is whether the structural case, anchored in the plasma market’s projected doubling to $104 billion by 2033, remains sufficient to justify patience through the current uncertainty.

Readers are encouraged to monitor the ASX announcements page for the permanent CEO appointment and the August 2026 results release, and to verify specific financial figures against CSL’s investor relations filings given the data verification caveats noted throughout this analysis.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.