Tesla at $390: a Framework for Valuing Transformation-Stage Stocks

4 mins ago

A stock trading at 188 times forward earnings is either the opportunity of a decade or one of the most expensive mistakes an investor can make. With Tesla sitting at approximately $412 per share in May 2026, the answer depends entirely on which future materialises. Tesla’s Q1 2026 earnings beat, with revenue of $22.4 billion and gross margin of 21.7% against a 17% consensus estimate, triggered renewed debate about whether the stock is priced for perfection or priced for transformation. Analyst price targets range from $220 to $600, one of the widest dispersions for any large-cap stock in the U.S. market. That gap is not noise. It reflects a genuine, unresolved disagreement about what kind of company Tesla actually is.

This article uses Tesla’s specific numbers as a live case study to teach a broadly applicable methodology for stock valuation analysis: how to construct bull and bear scenarios, how to stress-test return outcomes across different assumptions, and why the price paid at entry is one of the most consequential variables in any investment decision.

Tesla sits at the intersection of two valuation regimes. One is a traditional automotive business, measurable and facing margin pressure. The other is a speculative AI and robotics platform, unproven at commercial scale but potentially enormous. The stock’s current price cannot be justified by the car business alone, which means investors buying today are paying for a future that has not yet appeared on an income statement.

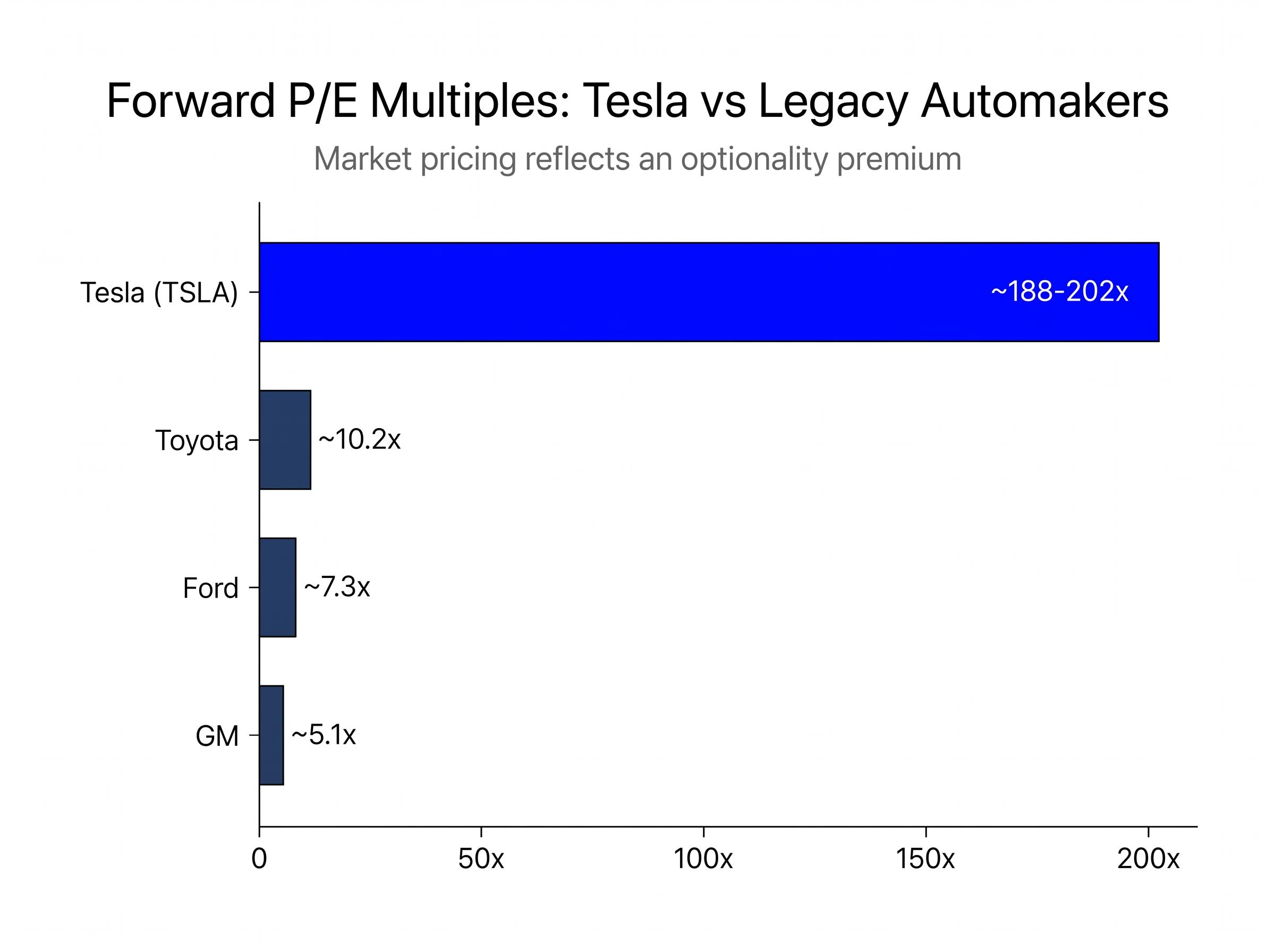

The gap between Tesla and its peers makes this visible immediately.

| Company | Forward P/E | EV/Sales |

|---|---|---|

| Tesla (TSLA) | ~188-202x | ~16.2x |

| Toyota | ~10.2x | N/A |

| GM | ~5.1x | N/A |

| Ford | ~7.3x | N/A |

| Rivian | N/A | ~2x |

A forward P/E of 188-202x against Toyota at 10.2x and GM at 5.1x is not a comparison of similar businesses. It is evidence that the market is pricing Tesla as something other than a car company. The question is whether the “something other” will materialise.

Optionality premium in practice: ARK Invest’s valuation model attributes approximately 60% of Tesla’s enterprise value to the robotaxi segment, a business that does not yet generate meaningful revenue. This is the optionality premium: the portion of a stock’s price that reflects future businesses rather than current earnings.

Tesla reported FY2025 revenue of $94.8 billion, down 3% year-over-year, its first-ever annual revenue decline. The auto segment faced margin pressure from competition and price cuts. Yet the stock trades at a $1.45 trillion market capitalisation. Understanding why this gap exists, and how to evaluate whether it is justified, is the skill this article teaches. That skill applies to any company where current earnings vastly understate the market’s expectations: SaaS platforms, biotech firms, clean energy infrastructure.

Growth stock valuation discounts of the kind measured across the broader 2026 equity market illustrate the flip side of the Tesla problem: where Tesla’s multiple prices in outcomes that have not arrived, a broad growth stock discount implies the market is pricing in outcomes worse than underlying fundamentals suggest, and recognising which regime a given stock occupies is the prerequisite to applying any scenario framework correctly.

Valuation multiples are not answers. They are encoded assumptions about a company’s future, compressed into a single number. Reading them correctly requires understanding what each one normalises for and, more importantly, what growth rate and margin trajectory the number demands.

Three multiples matter most in practice:

Tesla’s forward P/E of 188-202x and EV/EBITDA of approximately 125.6x are not irrational on their face. A 200x P/E can be justified if the earnings base is expected to grow by 10-20x over the next decade. But the assumptions embedded in that number must be made explicit, and that is where most investors fail to do the work.

Analysts attempting to reconcile Tesla’s automotive revenue with its AI premium often reach for sum-of-the-parts methodology, which assigns separate valuation multiples to each business segment and aggregates them — a technique that makes the implicit assumptions about robotaxi and Optimus contributions explicit rather than burying them inside a blended multiple.

Here is the mechanism that catches investors most often. If a stock trades at 200x earnings and the multiple contracts to 30x as growth normalises, the investor can lose money even if earnings triple.

Consider a simplified example: a company earning $1 per share at a 200x multiple trades at $200. Over five years, earnings triple to $3 per share. If the market re-rates the stock to a 30x multiple (reflecting a mature growth profile), the share price falls to $90. Earnings tripled. The stock lost 55%.

This is directly relevant to Tesla. Analyst EPS estimates for the company declined more than 90% from their peak before recovering in forward projections following the Q1 2026 beat of $0.40 per share. Even the moderate bear case assumes multiple contraction as the AI narrative either proves out or loses momentum. Understanding what multiples embed, rather than just what they report, is the difference between a valuation that gives false precision and one that is genuinely diagnostic.

Scenario analysis forces an investor to state their assumptions in writing, which is where most valuation errors originate. The method rests on three variables that drive nearly every long-term outcome: revenue growth rate, net profit margin, and exit valuation multiple. Applied across a ten-year horizon, these three levers produce the full range of plausible results.

The process follows three steps:

| Variable | Bull Case | Bear Case |

|---|---|---|

| Revenue Growth (Annual) | 20-35% (midpoint ~27%) | 6-12% (midpoint ~9%) |

| Net Margin at Maturity | 20-30% | 8-14% |

| Exit P/E Multiple | 25-35x | 18-22x |

| Projected Annualised Return (10yr) | 11-35% | Negative |

The bull case, if fully realised, delivers annualised returns of 11-35% over ten years. The bear case, at an entry price of approximately $375-$412 per share, produces negative returns across every projection. FY2026 revenue consensus sits at approximately $105-106 billion (this figure awaits independent verification), which serves as the bear case baseline for near-term growth.

The investor who cannot state the growth and margin assumptions embedded in their price target does not yet understand their own thesis. The scenario method makes implicit assumptions explicit, and that is where its value lies.

The same company can be a good or a terrible investment depending solely on when and at what price the investor buys. Tesla itself demonstrates this more clearly than almost any other large-cap stock.

An investor who purchased shares at approximately $100 a few years prior to May 2026 faces an entirely different return distribution than an investor buying at $412 today, even holding the bull and bear scenarios constant. At $100, even partial execution of the AI thesis produces strong returns. At $412, partial execution may produce flat or negative outcomes.

This is the concept of margin of safety: the gap between the price paid and the estimated intrinsic value under a range of scenarios. The wider this gap, the more wrong an investor can be about assumptions while still generating acceptable returns.

At $412, the cushion is thin. The average analyst target sits at approximately $398, implying the stock is approximately fairly valued to slightly overvalued on a 12-month basis absent AI catalysts. The low-end analyst target of $220 implies approximately 47% downside from the current price, a quantifiable stress-test reference point for the investor evaluating worst-case exposure.

At current prices, the bear scenario generates no positive outcome, while the bull scenario requires a low-probability transition (successful robotaxi scale, Optimus commercialisation) to materialise. This asymmetry is the core risk management insight: the downside is concrete, the upside is conditional.

At the other extreme, Elon Musk’s $10 trillion valuation vision (approximately $3,500 per share) and ARK Invest’s expected case of $4,600 per share represent the upper bound. These targets require full realisation of the robotaxi, Optimus, and energy platforms simultaneously.

Entry price is the one variable entirely within the investor’s control. Every other variable, execution, competition, regulation, macroeconomics, involves uncertainty that cannot be eliminated. Getting the entry price right is the only reliable way to create a structural advantage, and at $412, the margin for error is narrow.

The scarcity of genuine margin-of-safety opportunities across US equities in 2026 makes the entry price discipline described in this framework harder to practise in real portfolios, because the broader market environment shapes which stocks are available at prices that leave adequate cushion below intrinsic value estimates.

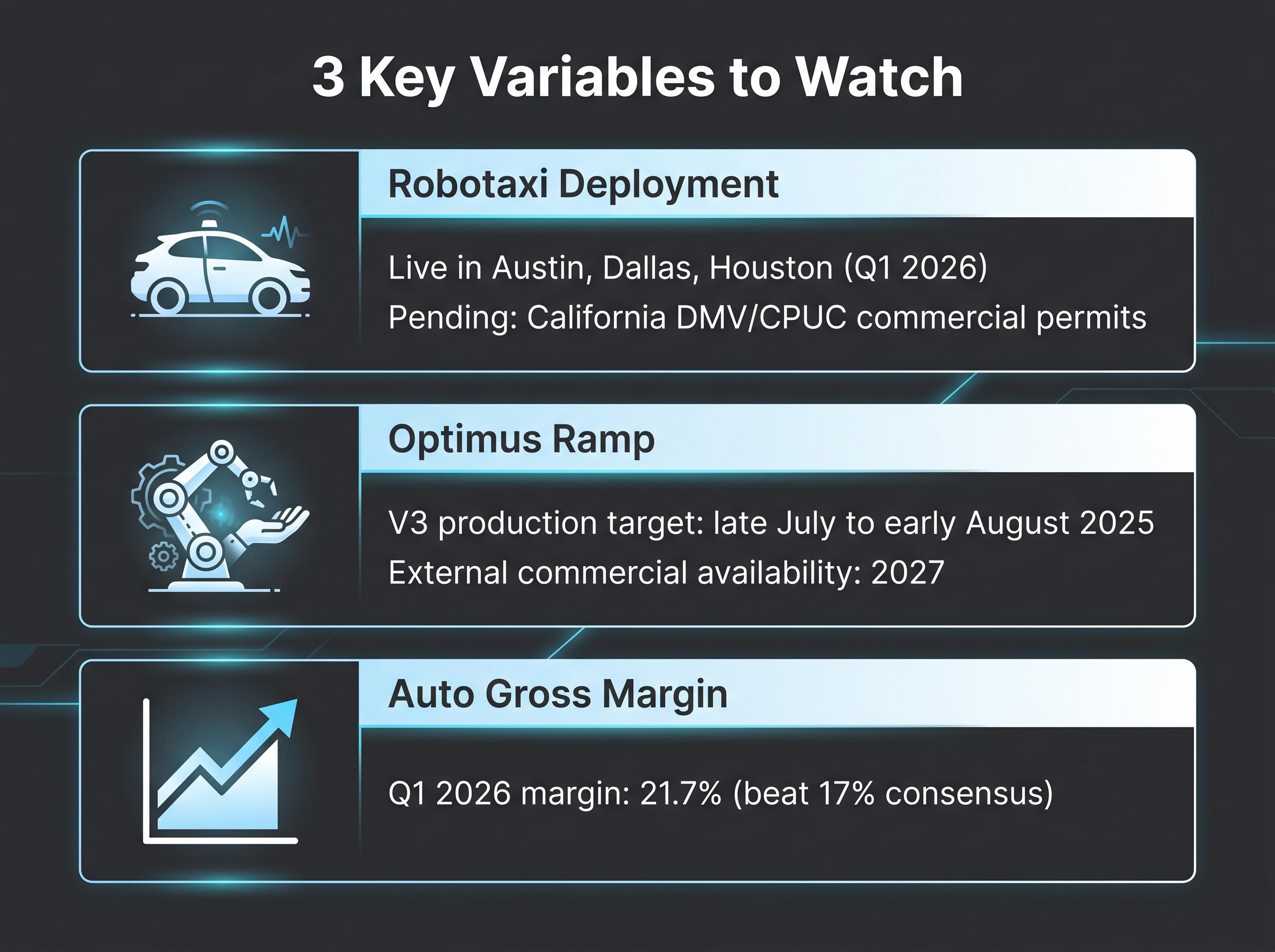

Knowing how to build scenarios is only half the skill. The other half is knowing which specific, observable indicators will reveal, in real time, whether the bull or bear case is materialising.

Three variables carry the highest leverage for Tesla’s outcome:

The CPUC autonomous vehicle deployment programs set out the specific application and authorisation requirements any operator must satisfy before conducting commercial driverless passenger service in California — the market analysts most frequently cite as the critical revenue catalyst in Tesla’s robotaxi bull case.

The timeline pattern investors should weigh: Musk committed to one million robotaxis by end of 2020, Optimus deployment-ready in 2022, and full autonomous hardware in all vehicles as of 2016. Each of these targets was missed by years. This documented history of delayed delivery must be incorporated into probability-weighting for any bull scenario that depends on specific deployment timelines.

Tesla’s CFO has indicated 2026 capital expenditure is expected to exceed $25 billion, spanning robot manufacturing, AI chip infrastructure, and Cyber Cab production. This level of simultaneous investment will generate substantial negative free cash flow, creating a time cost that bears directly on probability-weighted expected returns. The longer the payoff takes, the more the discount rate erodes the present value of the bull case.

Full Self-Driving (FSD) data adds context: Tesla’s fleet has accumulated 10 billion cumulative FSD miles as of approximately 4 May 2026, with an estimated 1.1 million paid subscribers at $99 per month (subscriber count awaits verification). Higher cumulative miles strengthen the data-advantage narrative, but subscription revenue remains modest relative to the valuation premium the market assigns.

Tesla is a single company. The methodology it illustrates applies to any stock whose price is front-running a future that has not yet arrived.

The process is transferable:

For Tesla specifically, the probability of full bull case materialisation sits at an estimated 5-10%. Most experienced investors target the base case reality: partial execution, with some robotaxi revenue, a gradual Optimus ramp, and stabilising auto margins rather than the full bull or full bear outcome. The question is whether $412 adequately compensates for the risk that even partial execution takes longer than the market expects. The consensus Hold rating and approximately $398 average analyst target suggest the answer, on a 12-month basis, is no.

The investor who disciplines themselves to state explicit assumptions, growth rate, margin, exit multiple, probability weight, before buying will make structurally better decisions than the investor who anchors to narrative alone.

For investors who have worked through the scenario framework and concluded that current prices leave insufficient margin of safety, our dedicated guide to market correction positioning covers how to build a pre-researched watchlist with pre-calculated buy prices, how to monitor the Berkshire deployment signal in SEC filings, and how to hold cash defensively while maintaining readiness to deploy when conditions improve.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Scenario analysis is a method where investors explicitly state their assumptions about revenue growth, profit margins, and exit valuation multiples under both optimistic and pessimistic outcomes, allowing them to stress-test potential returns before committing capital at a given entry price.

A high forward P/E ratio, such as Tesla's 188-202x, signals that investors are paying for future earnings that have not yet materialised, meaning the stock price embeds assumptions about future businesses like robotaxi or Optimus rather than current profitability.

Multiple compression occurs when a stock's valuation multiple falls as growth normalises; for example, a stock at 200x earnings that re-rates to 30x can lose over 50% in value even if underlying earnings triple over the same period.

Entry price is the only variable entirely within an investor's control; buying at a lower price relative to intrinsic value creates a margin of safety, meaning the investor can be wrong on growth or margin assumptions and still generate acceptable returns.

Investors should watch Tesla's California robotaxi commercial permit applications, Optimus confirmed production unit counts and first commercial contracts, and quarterly auto gross margin prints relative to analyst consensus estimates.