How Many Westpac Shares You Need for $10,000 in Income

6 hrs ago

The notification hits your phone: a company you own just reported earnings, the stock is already moving in after-hours trading, and you have no plan. Do you sell? Hold? Buy the dip? For most investors, the next 30 minutes will determine whether they make a disciplined decision or an expensive mistake. Q1 2026 is proving that distinction matters more than usual. With 84% of reporting S&P 500 companies beating EPS estimates, the season looks strong on paper, yet Palantir crashed after posting 85% revenue growth, and Monday.com dropped more than 20% on soft guidance despite a revenue beat. Strong results do not guarantee positive price reactions. This guide delivers a concrete three-part decision framework (hold, trim, or wait) to apply the moment a report lands, including the cognitive bias traps that derail disciplined thinking and how to pre-empt them before the next earnings release arrives.

By the time an earnings report lands, the market has already placed its bet. Analyst estimates, whisper numbers, and institutional positioning have baked expectations into the share price weeks before the actual results arrive. A beat only matters if it exceeds what was already priced in, and in Q1 2026, that bar has been unusually difficult to clear.

The reason is structural. Pre-season analyst estimates did not drift lower as they typically do in preceding quarters, a pattern that historically gives companies an easier hurdle. Instead, estimates held firm. As Natixis strategist Jack Janasiewicz noted, this means Q1 2026 reactions hinge less on reported numbers and more on what companies say about the quarters ahead.

“Market reaction likely to hinge more on outlook than results.” Jack Janasiewicz, Natixis

The aggregate numbers reinforce the disconnect. Mid-season, with 63% of S&P 500 companies reported, the blended EPS growth rate stood at 27.1% year-over-year, more than double the pre-season estimate of 13.2%. Revenue beat rates hit 81%. Yet individual stock reactions have defied those headline figures repeatedly.

The Q1 2026 earnings season produced an aggregate EPS surprise of 20.7%, nearly three times the five-year average of 7.3%, driven by analysts who entered the period with estimates that proved far too conservative relative to actual mega-cap technology outperformance.

The FactSet Earnings Insight for Q1 2026 places the blended EPS growth rate at 27.1% year-over-year, more than double the 13.2% pre-season estimate, with revenue beat rates reaching 81% across reporting S&P 500 companies.

Palantir reported 85% revenue growth, 104% U.S. revenue growth, and beat consensus on both EPS and revenue. The stock crashed post-earnings.

The lesson is not about Palantir’s business quality. It is about what happens when a stock’s price has already absorbed the optimism the report confirms. Investors who understood the expectations-versus-reality mechanic before the release could separate the business outcome from the price outcome. Those who did not were left asking the wrong question: why is my stock down on a good report?

The right question is different: did this report move the expectations needle?

When a report drops, most investors default to a binary instinct: sell or stay. That binary collapses the decision into an emotional reaction rather than an analytical one. A more effective approach treats the moment as a triage with three distinct options, each tied to observable triggers.

The foundational question, per Fidelity, is simple: does the report change the original reason for purchasing this stock, or does it leave the thesis intact? That single diagnostic separates noise from signal.

From there, the decision branches into three paths.

| Decision | Primary Trigger | Supporting Signal | Red Flag That Changes It | Current Season Relevance |

|---|---|---|---|---|

| Hold | Original thesis intact | Guidance maintained or raised; consistent revenue growth | Company-specific deterioration masked by broad market rally | 84% beat rate supports aggregate position maintenance |

| Trim | Thesis weakened but not broken | Forward guidance lowered or softened; margin compression visible | Price drop is macro-driven, not guidance-driven | Guidance matters more than EPS given firm pre-season estimates |

| Wait | Insufficient information to act | Report is mixed; need earnings call detail or peer context | Clear directional signal emerges in call or follow-up filings | Geopolitical volatility amplifies short-term moves, rewarding patience |

The fourth implicit option is reacting immediately, and in the current environment it is generally the most costly. Interactive Brokers framed the Q1 2026 season as a “balancing act,” urging investors to avoid both FOMO on beats and panic on dips. The 84% EPS and 81% revenue beat rates reflect underlying corporate health; they do not mean every stock that beats will rise, or that every stock that falls post-earnings deserves an exit.

Hold signals worth identifying before acting:

Holding is not inaction. In a season where oil price spikes, geopolitical tensions from the Iran conflict, and record-high index levels are all operating simultaneously, holding through a post-earnings dip is an active, disciplined choice, not a passive one.

The conditions that support it are specific. The original investment thesis remains intact. Guidance was maintained or raised. The price drop, if there is one, traces back to macro sentiment rather than company-specific weakness.

J.P. Morgan Private Bank made this case explicitly in its Q1 2026 review, noting that “valuations contracted” due to oil and geopolitics despite intact business outlooks. The firm advised long-term investors to hold through volatility and maintain a constructive 2026-2027 outlook despite Q1 challenges. The aggregate data supports that posture: Q1 2026 is on track for the sixth consecutive double-digit EPS growth quarter.

A single earnings report is a data point, not a verdict. Several quarters of data provide far more meaningful insight than any individual release. Before deciding that one report has changed a thesis, run these three diagnostic questions against the multi-quarter trend:

A company that misses on one quarter but shows improving revenue trajectory and expanding margins over the prior four quarters looks fundamentally different from one posting a single strong beat inside a deteriorating trend. The multi-quarter lens is what distinguishes a temporary setback from a thesis-breaking development.

Trimming a position is not an admission of failure. It is portfolio discipline applied to a thesis that has weakened but not fully broken. The distinction matters: a full exit signals a broken thesis, while a partial trim reflects a recalibrated risk assessment.

In Q1 2026, the primary trim trigger is not the headline EPS number. It is the forward guidance language. Both Natixis and J.P. Morgan identified guidance as the dominant signal this season, precisely because pre-season estimates did not drift lower. Without that typical “reduced bar” cushion, any guidance miss lands harder than usual.

The April 29 session illustrated in concrete terms how forward guidance drives price outcomes independent of reported results: Centene surged nearly 9% on a raised full-year EPS outlook while Spotify fell 12-14% despite beating its current-quarter estimate, with the divergence explained entirely by the direction of each company’s forward language.

The specific signals that warrant a trim:

Monday.com beat on both Q4 2025 EPS and revenue, then dropped more than 20% on 9 February 2026. The trigger was entirely soft 2026 guidance. The headline numbers were irrelevant to the price outcome.

J.P. Morgan Private Bank advised trimming overvalued technology and energy positions where guidance disappoints. The Information Technology sector’s 45-46% EPS growth and 27.4% revenue growth set an extremely high bar. Beats that fall short of that implied trajectory can still trigger sell-offs, making guidance language the only reliable trim signal in a sector where the numbers already look strong on the surface.

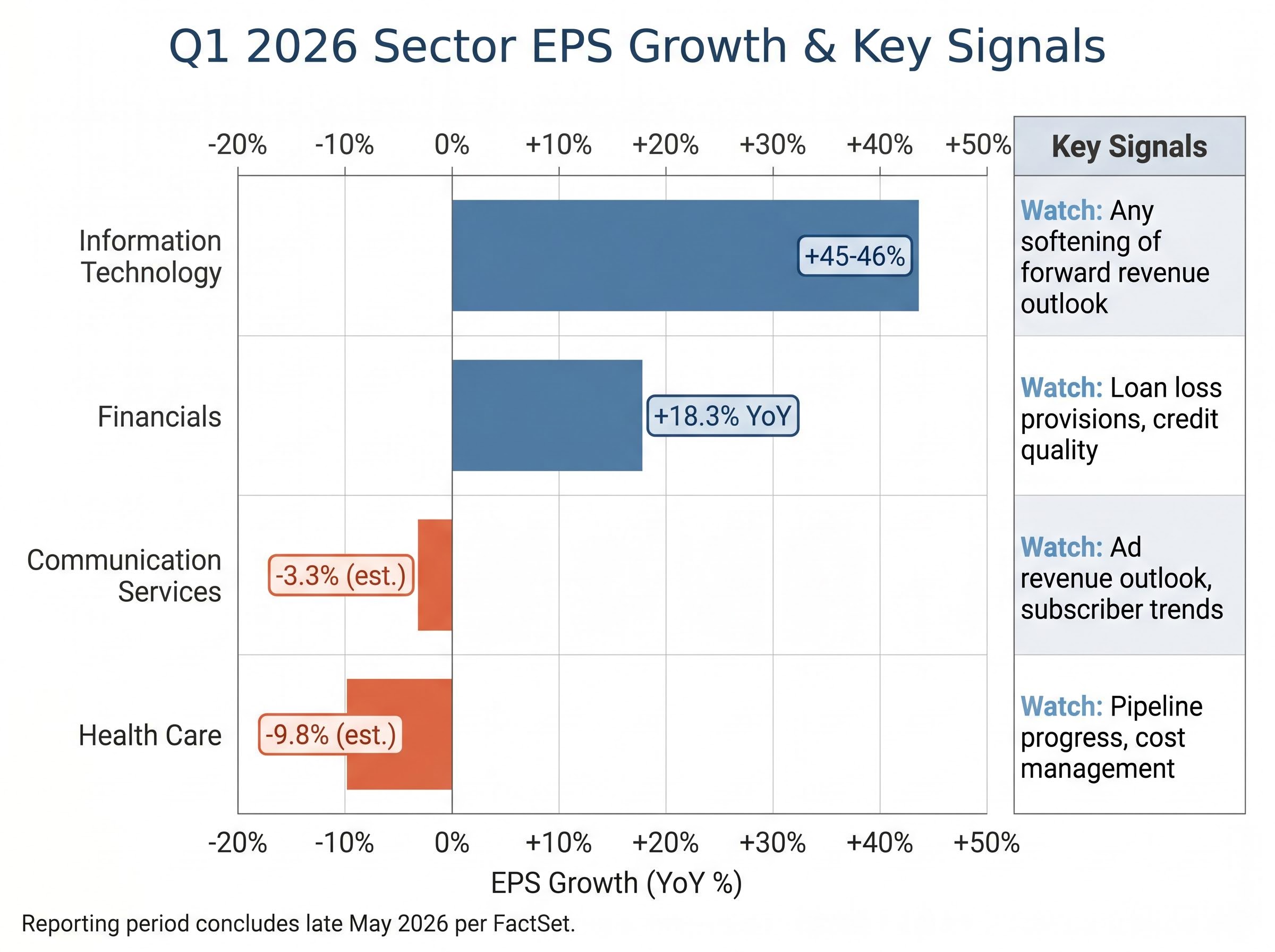

The Q1 2026 reporting period is projected to conclude by late May 2026, per FactSet. The remaining weeks offer a live testing ground for the hold, trim, and wait framework, provided investors know which sectors and signals to prioritise.

| Sector | EPS Growth (Est./Actual) | Key Risk | Guidance Signal to Watch | Framework Implication |

|---|---|---|---|---|

| Information Technology | +45-46% | Bar too high; beats may disappoint | Any softening of forward revenue outlook | Trim if guidance misses elevated expectations |

| Financials | +18.3% YoY | Consumer demand sustainability | Loan loss provisions, credit quality language | Hold if consumer resilience narrative holds |

| Health Care | -9.8% (est.) | Overshoot sell-offs; Gilead Sciences flagged | Pipeline progress, cost management updates | Wait for post-earnings dips as entry opportunities |

| Communication Services | -3.3% (est.) | Negative growth expectations | Ad revenue outlook, subscriber trends | Wait; assess whether misses are priced in |

| Energy | Lagging | Oil price volatility from Iran conflict | Capital expenditure plans, hedging guidance | Trim if guidance reflects sustained cost pressure |

J.P. Morgan Private Bank flagged post-earnings dips in laggard sectors as potential “repricing” opportunities where sell-offs may overshoot. Health Care, with its estimated -9.8% EPS decline, is the clearest candidate for that dynamic.

FactSet’s S&P 500 earnings season update from May 2026 projects the reporting period to conclude by late May, with Health Care among the sectors most exposed to estimate misses given its estimated -9.8% EPS decline, making it a candidate for overshooting post-earnings sell-offs.

For the remaining weeks, a three-step monitoring habit keeps the framework practical:

Every investor knows they should stay disciplined during earnings season. The problem is not knowledge; it is the specific biases that hijack decision-making in the 30 minutes after a report drops. Naming each one is the first step to recognising it in real time.

| Bias | What It Feels Like During Earnings | The Decision It Drives | The Cost | The Pre-Plan Antidote |

|---|---|---|---|---|

| Loss Aversion | Watching the position drop in after-hours and feeling compelled to stop the pain | Selling on emotion rather than analysis | Locking in realised losses on sentiment-driven moves | Pre-set a threshold: “I will only sell if guidance is lowered, not if the price drops X%” |

| FOMO | Seeing a stock surge post-earnings and rushing to buy before it goes higher | Chasing post-earnings surges at elevated prices | Purchasing at inflated levels after the move has already occurred | Pre-set a buy trigger: “I will add only if price pulls back to [level] within 5 days” |

| Overconfidence | One strong quarter convincing you the thesis is bulletproof | Increasing position size based on a single data point | Over-concentration risk if subsequent quarters disappoint | Require three consecutive quarters of thesis-confirming data before adding |

| Reactive Selling | Feeling urgency to act simply because everyone else appears to be acting | Exiting a position within hours of the report | Missing the recovery when the sell-off proves to be a macro-driven overreaction | Enforce a 48-hour cooling period before executing any post-earnings trade |

Interactive Brokers framed the Q1 2026 environment as requiring a deliberate “balancing act” between the pull of FOMO on beats and the push of panic on dips. The season’s amplified volatility from geopolitical events makes bias-driven decisions more likely and more costly than in calmer periods.

The structural countermeasure is not willpower. It is pre-planning. Deciding in advance what triggers a trim, hold, or wait removes real-time emotional processing from the equation. An investor who has already written down “I will trim if forward guidance is lowered by more than 5%” before the report drops is executing a plan, not fighting an impulse.

In a season where 84% of companies beat EPS estimates yet individual stocks still crash on guidance misses, the quality of the earnings report is not the primary driver of investor outcomes. The quality of the decision process is.

The framework distils to three pre-set commitments, made before the next report arrives:

Q1 2026 reporting concludes by late May 2026. That window is narrow enough to be actionable. Before the next stock in a portfolio reports, write down the specific trigger for each of the three decisions. The investors who outperform this earnings season will not be the ones with the best stock picks. They will be the ones who decided what to do before the notification arrived.

For investors who have applied the hold, trim, and wait framework through the Q1 reporting period and want to think through what comes next, our full explainer on what Q1 2026 earnings mean for the rest of the year examines the capital rotation from mega-cap tech into small-caps and value, the $700 billion hyperscaler capex debate, and the forward P/E constraints that narrow the margin for error in Q2 and beyond.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

An earnings season strategy is a pre-planned set of decision rules that tells you whether to hold, trim, or wait when a company you own reports results, based on specific triggers like guidance changes or thesis shifts rather than emotional reactions to price moves.

Stocks fall after beating estimates when the reported results only confirm expectations that were already priced into the share price, a dynamic known as selling the news, as illustrated by Palantir's post-earnings crash despite 85% revenue growth in Q1 2026.

In Q1 2026, investors should prioritise forward guidance language over headline EPS numbers, because pre-season estimates did not drift lower as usual, meaning any softening of the outlook lands harder and is the primary driver of post-earnings price moves.

Investors can avoid panic selling by writing down specific decision triggers before a report drops, such as committing to trim only if forward guidance is lowered by more than a defined threshold, which removes real-time emotional processing from the decision.

Trimming means reducing a position size because the thesis has weakened but not fully broken, while a full exit signals the original investment thesis is no longer valid; trimming reflects a recalibrated risk assessment rather than a complete change of view on the company.