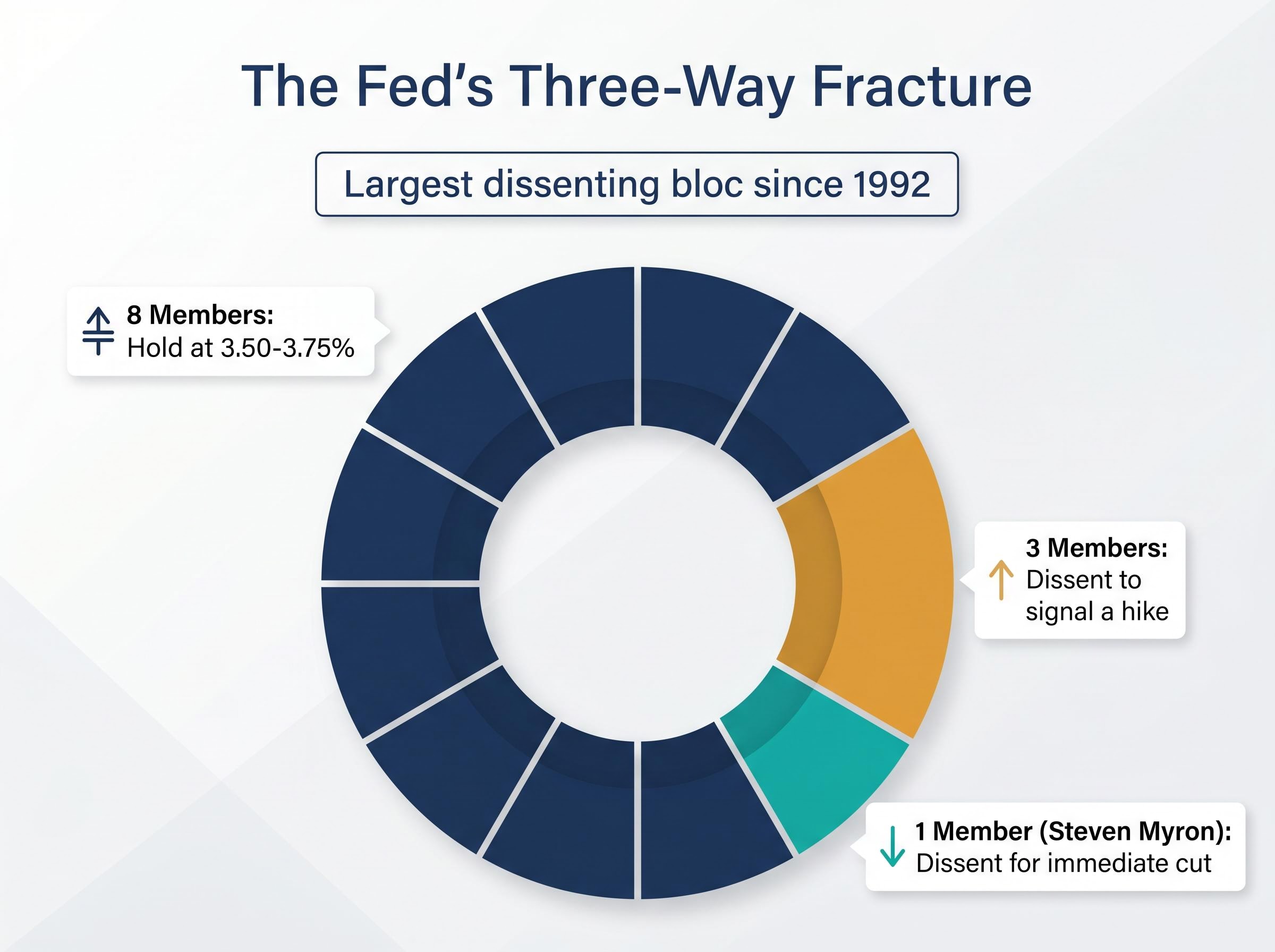

The Federal Reserve’s most recent meeting ended in an 8-4 vote, the largest dissenting bloc since 1992. The disagreement was not about whether to hold rates. It was about what direction the next move should be: at least one dissenter voted for an immediate cut, while three others wanted the official statement to signal that a hike remained on the table. That is not a normal policy disagreement; it is a fractured institution at the edge of a leadership handoff. Jerome Powell’s chairmanship ends on 15 May 2026. Kevin Warsh, confirmed by the Senate Banking Committee on a 13-11 party-line vote, is expected to take the chair imminently. He will inherit a Fed holding at 3.50-3.75%, inflation running at 3.3% against a 2% target, and a committee that cannot agree on which direction risk runs. What follows is a breakdown of exactly why the Fed is paralysed, what the 8-4 vote signals about internal fault lines, what Warsh is likely to prioritise, and why the combination of a new chair, a contested inflation framework, and unusual political pressure makes this one of the more consequential Fed transitions in decades.

How the four dissenting votes revealed a committee split in opposite directions

Eight members voted to hold rates at 3.50-3.75%. Four dissented. The last time the Federal Open Market Committee (FOMC) produced a dissenting bloc that large was 1992, more than three decades ago.

The composition of the dissent matters more than the count. The four opposing votes did not point in the same direction:

- Pro-cut dissent: Fed Governor Steven Myron voted for an immediate rate reduction, arguing current policy was already too restrictive given softening demand signals.

- Pro-hike-signal dissenters: Three members voted against the statement because it failed to include language acknowledging a rate increase as a genuine possibility for the next meeting.

- Majority hold position: The eight remaining members voted to maintain the current rate and statement language, holding the line between both camps.

That three-way split is the signal. A committee divided between members who want to cut and members who want to signal a hike is not experiencing a pace disagreement. It is experiencing a directional fracture.

Powell acknowledged that the majority favouring a cut as the next move could shift to a majority favouring hike signalling by the June meeting, an extraordinary admission of committee instability.

That statement alone reframes the hold as something closer to a temporary ceasefire than a consensus position.

When big ASX news breaks, our subscribers know first

Why the Fed cannot move: the competing forces boxing in the committee

The paralysis is not abstract. It is the product of specific, identifiable forces pulling rates in opposite directions simultaneously, with no single variable dominant enough to break the deadlock.

Tariff-driven goods inflation is the most direct upward pressure. Import taxes function as a levy passed through to consumers at the point of sale, but the inflation channel extends beyond tariffed goods. Non-tariffed competitors facing reduced price competition can raise their own prices into the gap, broadening the inflationary impulse across categories. Standard economic theory holds that tariff-driven price increases are one-time level adjustments rather than sustained inflation. The Fed has not acted on that theory because it is waiting for actual evidence of price rolloff before cutting.

Energy prices added a second complicating variable. The US national average for petrol reached approximately $4.30 per gallon prior to the most recent data, having risen by roughly $1 per gallon during March 2026 alone. Delta Air Lines projected approximately $2 billion in additional Q2 fuel costs, illustrating how energy price spillovers transmit through freight, logistics, and operating costs into broader price levels.

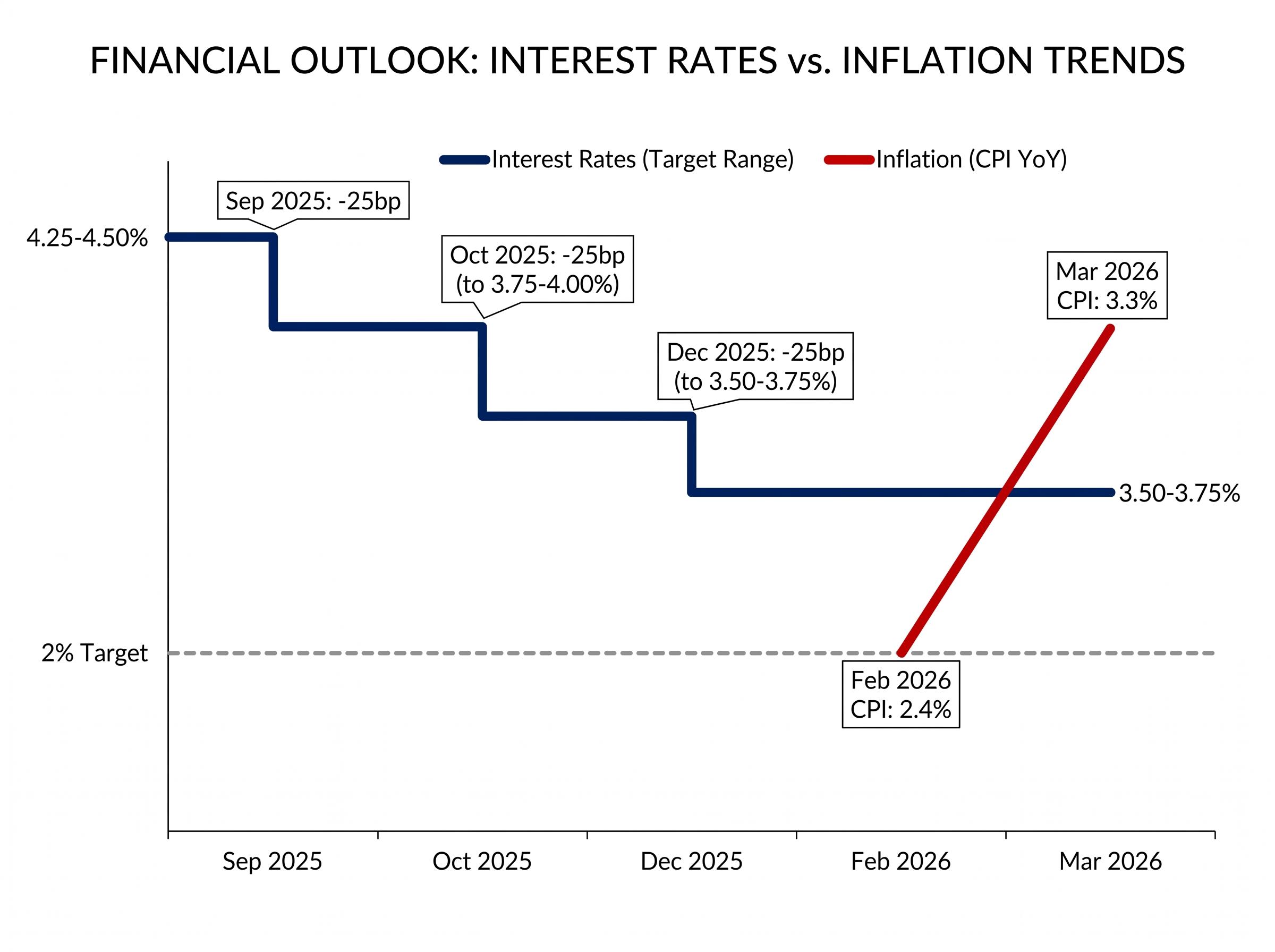

March 2026 CPI came in at 3.3%, up from 2.4% in February. Inflation has now run above the 2% target for five consecutive years, confirmed through March 2026 PCE data. That duration raises the probability that consumers begin accepting higher inflation as the new normal, which would unanchor expectations and make the problem structurally self-reinforcing.

The Fed executed three 25 basis point cuts in 2025:

- September 2025: 25bp cut

- October 2025: 25bp cut (rate to 3.75-4.00%)

- December 2025: 25bp cut (rate to 3.50-3.75%)

Those cuts brought rates down from 4.25-4.50% to the current level. No further movement has followed.

| Force | Direction of pressure on rates | Current status |

|---|---|---|

| Tariff-driven goods inflation | Upward | Active |

| Energy price spillovers | Upward | Partially moderated |

| Labour market strength | Upward / hold | Stable |

| Expectations unanchoring risk | Upward | Monitoring stage |

| Weak hiring rate | Downward | Latent |

The table illustrates why neither direction commands a majority. Every force pushing rates higher has a counterweight, and the single downward pressure, weak hiring, has not yet produced enough deterioration to override the inflation concerns.

Five years above target: how the 2% goal became a credibility question

Where the 2% target came from

The 2% inflation target was not derived from a theoretical model of optimal price stability. It was chosen because it reflected where inflation naturally settled during the stable periods of the 1990s and early 2000s, when supply chains were globalising, goods prices were falling, and monetary policy operated in a relatively benign environment. Peer central banks converged on roughly the same number for roughly the same reason: it described what already worked.

Pre-pandemic US inflation was running slightly below 2%, reinforcing the target’s credibility. The problem is that the conditions which produced sub-2% inflation, particularly expanded trade with lower-cost producers, created a deflationary tailwind on goods prices. Reversing that trade openness through tariffs and supply chain restructuring removes the tailwind, potentially making 2% structurally harder to achieve even if individual supply shocks are temporary.

Why five consecutive years above target is a different problem

A single year of above-target inflation is a miss. Five consecutive years is a credibility test. Inflation peaked at approximately 9% in 2022 and has since fallen to roughly 3%, a meaningful decline. But the cumulative effect of successive overlapping supply shocks, pandemic disruptions, energy price spikes, tariff-driven goods inflation, has kept the price level compounding above the target’s trajectory for half a decade.

If inflation runs at 3% for long enough, 3% becomes the functional anchor regardless of the stated target. That is the expectations unanchoring mechanism: businesses set prices and negotiate wages around the inflation rate they actually experience, not the one printed on the Fed’s website.

Debating whether to adjust the 2% target while missing it carries the perception of moving the goalposts, which is itself a credibility problem. Any framework review under Warsh will have to navigate this tension directly.

Warsh’s documented interest in a new inflation framework and productivity dynamics signals a potential conceptual shift under new leadership. Whether that shift includes revisiting the target number itself, or redefining how the target is measured and pursued, remains an open question.

What Warsh inherits: a committee divided on direction and unable to move

The instinct is to treat a new chair as a reset. The institutional mechanics argue otherwise.

The Fed chair drives agenda-setting and maintains constant communication with all committee members, but holds only one of twelve votes at each meeting. The Board of Governors has seven seats; the remaining five votes rotate among twelve regional bank presidents. Consensus-building in a deliberative institution takes time, and Warsh inherits a committee that is not merely cautious but actively divided on direction.

The Federal Reserve is a deliberative institution that changes course slowly outside of crisis conditions. A new chair sets the agenda, but the committee sets the pace.

The sequential constraints Warsh faces are specific and cumulative:

- Building consensus in a committee that currently contains both pro-cut and pro-hike factions

- Inheriting above-target inflation at 3.3% with no clear downside catalyst in view

- Navigating a framework review without creating the perception of moving the goalposts on the 2% target

- Operating under political scrutiny from a party-line confirmation (Senate Banking Committee, 13-11, approximately 29 April 2026)

Powell’s decision to remain as a governor through January 2028 rather than departing entirely has been framed as a deliberate act to protect institutional continuity and independence, not a routine administrative choice. Quantitative tightening ended effective 1 December 2025, removing one source of policy complexity, but the rate question remains fully unresolved.

The labour market’s deceptive calm and what it means for the rate decision

What the headline numbers say

Unemployment at 4.3-4.4% is historically low and has held stable since autumn 2025. The layoff rate remains very low. Unemployment insurance claims are subdued. By traditional metrics, the labour market is healthy and consistent with an older, more educated workforce demographic that naturally produces lower unemployment.

The Fed views these conditions as broadly appropriate. They do not, on their face, argue for emergency easing.

What the structural picture suggests

The calm surface conceals an unusual structure. Hiring rates are low relative to both the pandemic period and longer historical norms. Companies are neither hiring aggressively nor laying off workers, producing a low-hire, low-fire dynamic that protects currently employed workers but leaves anyone seeking re-entry facing a very difficult market.

The asymmetric risk is the vulnerability: if companies begin layoffs, unemployment could rise rapidly with no offsetting hiring activity to absorb displaced workers.

Immigration deceleration compounds the problem. The effective elimination of labour supply growth means the threshold for what counts as a strong jobs number is now close to zero, making positive payroll prints harder to interpret as genuine strength. Approximately 40% of monthly payroll reports since the start of the prior year showed payroll declines, a frequency historically associated with recessionary conditions, even though no recession has been declared. The Sahm Rule triggered in summer 2024 without a recession, driven by immigration-fuelled labour force expansion rather than rising joblessness.

Surface indicators versus structural vulnerabilities:

- Surface: Low unemployment, low layoffs, low insurance claims

- Structural: Low hiring rate, near-zero labour supply growth, 40% negative payroll print frequency, asymmetric downside risk if layoffs begin

A labour market that looks stable in headline terms but is structurally unusual removes one of the clearest signals the Fed would normally use to justify a cut.

Independence under pressure: the institutional stakes running beneath the rate decision

The rate decision dominates headlines. The institutional question underneath it carries longer-term consequences.

Efforts to remove Governor Lisa Cook and a reported criminal investigation involving Powell’s oversight of building renovations represent direct institutional pressure on the Fed, qualitatively different from the rhetorical disagreements between administrations and central banks that have occurred periodically throughout Fed history. These are personnel actions and legal measures directed at sitting officials.

- Personnel actions: Efforts to remove Governor Cook

- Legal pressure: Investigation into Powell’s building renovation oversight

- Political confirmation dynamics: Warsh confirmed on a 13-11 party-line vote

The practical economic stakes of Fed independence are concrete. If the market perceives that rate decisions are politically driven, the credibility of inflation targeting erodes. Long-term yields rise to compensate for the uncertainty, and the real cost of borrowing increases regardless of where the fed funds rate is set.

The 10-year Treasury yield at approximately 4.30-4.40% and the 30-year approaching 5.0% may already reflect some degree of that uncertainty about the long-term fiscal and monetary trajectory. Powell’s decision to remain as governor through January 2028 functions as one institutional continuity signal, but the combination of a fractured committee, a leadership transition under political pressure, and five years of above-target inflation creates a compounding institutional test rather than a set of separable problems.

The rule of law and functional institutions are foundational to long-term economic performance. Their erosion represents a systemic risk, not a cyclical one, and it is priced over years rather than quarters.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

What the next six months will actually tell us about where rates go

The June 2026 FOMC meeting will be the first under Warsh’s chairmanship. It functions as a real-time test of committee cohesion: the statement language, the vote count, and the press conference will reveal whether the directional fracture has widened or narrowed.

The inflation trajectory is the dominant variable. The scenarios are distinct enough to map:

| Scenario | Inflation trajectory | Rate direction | Signal to watch |

|---|---|---|---|

| Tariff inflation rolls off | Moderating toward 2.5% | Cut in late 2026 | Monthly CPI prints declining through summer |

| Inflation holds at 3%+ | Sticky above target | Hike signalling from committee majority | June statement language shift |

| Energy shock escalates | Rising on supply disruption | Extended hold with hike bias | Oil sustained above $100-115/barrel |

| Labour market deteriorates sharply | Secondary to employment crisis | Emergency cut regardless of inflation | Unemployment rising above 5% rapidly |

In December 2025, Powell explicitly stated that further rate cuts were “far from a foregone conclusion.” That framing has not been walked back.

Warsh’s framework review will take months, not weeks. Early public statements should be read as agenda-setting rather than immediate policy signals. CME FedWatch probabilities for the May to July 2026 meetings are not available from current research sources; live market-implied probabilities can be monitored at cmegroup.com.

Financial projections and rate scenarios are subject to change based on incoming economic data and evolving market conditions. Past performance does not guarantee future results.

A fractured committee, a contested framework, and a leadership handoff unlike any in recent memory

Three conditions are operating simultaneously rather than sequentially: a record dissent that contains members pulling in opposite directions, a contested inflation framework after five years above target, and direct institutional pressure on sitting officials during a leadership handoff. Each alone would complicate policy. Together, they make the next six months genuinely binary in a way the rate decision rarely is. The same committee that just held at 3.50-3.75% contains members advocating both cuts and hikes. The resolution depends on data arriving over the next 60-90 days.

The rate decision matters for the next meeting. The credibility of the Fed’s independence and inflation-targeting framework matters for the next decade. Those two questions are now entangled in a way they have not been since the Volcker era.

The June 2026 FOMC statement and Warsh’s inaugural press conference will be the earliest real signals of committee direction. The CME FedWatch Tool at cmegroup.com provides live market-implied probability updates between meetings for those tracking the rate path in real time.

—