BofA Cuts EUR/USD Target as Three Fed Hikes Drive Dollar Bull Case

2 hrs ago

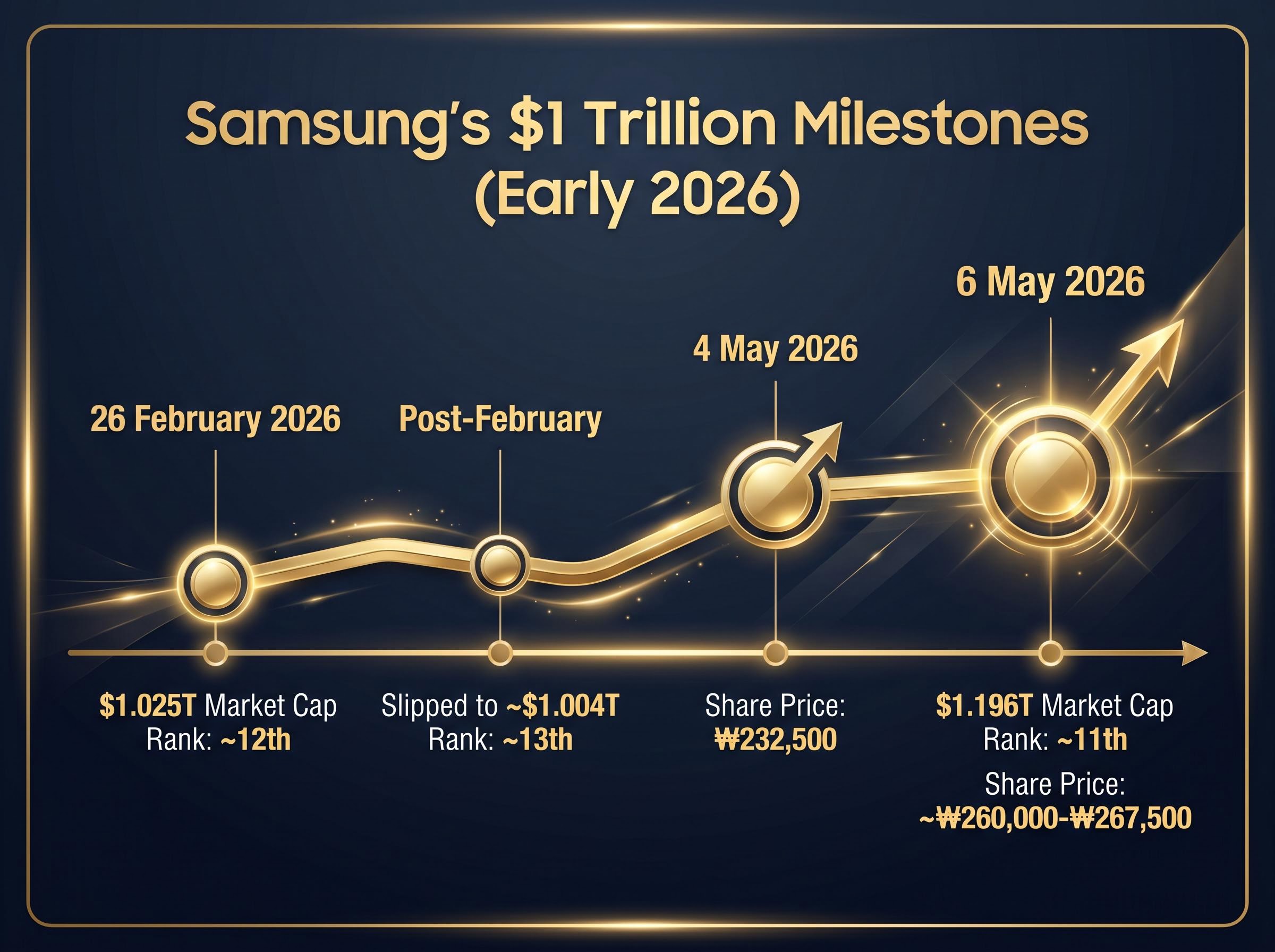

On 5 May 2026, Samsung Electronics shares surged more than 11% in a single session to a record ₩261,500, vaulting the company past the $1 trillion market capitalisation mark for the second time this year. The milestone makes Samsung the first Korean company to join the trillion-dollar club, arriving at the intersection of three powerful forces: a global memory chip upcycle, accelerating artificial intelligence (AI) infrastructure demand, and a Bloomberg report that Apple has held preliminary talks with Samsung and Intel about manufacturing main processors for its devices in the United States. What follows is an examination of what drove the record session, what the Apple chip talks mean for Samsung’s foundry ambitions, how the high-bandwidth memory (HBM) market is reshaping semiconductor competition, and whether the rally’s underlying fundamentals justify its scale.

The weight of the number is hard to overstate. Samsung is now valued at approximately $1.196 trillion as of 6 May 2026, ranking 11th globally by market capitalisation, behind Nvidia (~$4.8 trillion), Apple (~$4.0 trillion), Alphabet (~$3.8 trillion), and Microsoft, but ahead of Berkshire Hathaway.

Samsung is the first Korean company to cross the $1 trillion market capitalisation threshold.

Yet this was not the first crossing. Samsung initially breached the mark on 26 February 2026, when its market cap reached approximately $1.025 trillion. The stock then slipped back to roughly $1.004 trillion in the weeks that followed, making the latest surge feel both historic and hard-won.

The share price moved from a close of ₩232,500 on 4 May to approximately ₩260,000-₩267,500 on 6 May, with one source citing ₩266,000 and a +14.41% intraday gain. The year-to-date advance of approximately 115%-125% reflects a re-rating of the business rather than a speculative run-up, a distinction the sections that follow will examine in detail.

TrendForce reporting on Apple’s foundry diversification corroborates the Bloomberg account and adds supply chain context, noting that TSMC capacity constraints are among the structural pressures motivating Apple to explore alternative US-based manufacturing partners for its core processors.

| Date | Share Price | Market Cap | Global Ranking |

|---|---|---|---|

| 26 February 2026 | First $1T crossing | ~$1.025T | ~12th |

| Post-February | Slippage | ~$1.004T | ~13th |

| 4 May 2026 | ₩232,500 | Below $1.196T | — |

| 6 May 2026 | ~₩260,000-₩267,500 | ~$1.196T | ~11th |

The immediate catalyst arrived on 5 May 2026, when Bloomberg reported that Apple has held preliminary discussions with Samsung and Intel about producing main processors for Apple devices in the United States, as part of a strategy to diversify away from TSMC.

Apple shares rose approximately +2.66% to $284.18 on the session, on volume of roughly 43.79 million shares. But the larger market reaction centred on what the talks could mean for Samsung’s foundry division, which has long trailed TSMC in advanced logic chip manufacturing.

The word to hold onto is “exploratory.” No confirmed orders, official statements, or timelines have emerged from Apple, Samsung, or Intel.

Apple’s foundry diversification talks have produced sharply divergent market reactions: Intel fell approximately 3.85% on the day the Bloomberg report broke, while Samsung surged, a split that reflects how investors are weighting execution risk and capital costs differently for each potential manufacturing partner. Samsung’s Taylor, Texas facility was approximately 90% mass production ready as of April 2026, making it the more physically advanced US option for Apple to consider.

The opportunity is real, but conditional. For investors, the Apple talks are a catalyst to monitor rather than one to price as certain.

Beneath the headlines about Apple sits a structural story that predates the Bloomberg report by months. The memory chip market is experiencing a supply-demand dislocation driven by AI infrastructure demand, and the numbers are striking.

Overall DRAM prices have risen approximately 180% since early 2026, according to TrendForce and Digitimes data.

The surge centres on HBM, the specific category of memory chip that sits at the heart of AI accelerators. HBM is not commodity DRAM. It is a high-value, supply-constrained product that AI chip manufacturers, including Nvidia, require in large volumes to power data centre hardware. The HBM market is projected to grow from $2.93 billion to $16.72 billion by 2033, according to Yole Group research, while overall DRAM revenues are forecast to reach approximately $400 billion by 2027.

Three forces are converging to sustain the upcycle:

Hyperscaler AI infrastructure spending reached a qualitatively new scale in 2026, with the four largest cloud operators projecting a combined $650 billion in capital expenditure for the year, roughly 75% of which flows toward physical hardware, creating a durable order book that sits underneath memory and foundry pricing regardless of any single catalyst such as an Apple chip partnership.

One complication: HBM3E average prices are declining approximately 28% year-over-year in 2026 (from ~$15/GB to ~$10/GB) as competition intensifies. HBM4 premiums are expected to partially offset that erosion. The question for investors is whether the volume growth and next-generation pricing power can outpace the compression in current-generation products.

Samsung’s $1 trillion valuation prices in future dominance. The present picture is more nuanced.

SK Hynix leads the HBM market and has been Nvidia’s primary HBM3E supplier. Micron has, at times, overtaken Samsung in HBM share, and Samsung’s qualification challenges with Nvidia for HBM3 and HBM3E products have been a documented headwind.

| Company | Estimated HBM Share | Primary AI Customer | HBM4 Status |

|---|---|---|---|

| SK Hynix | ~35%-62% | Nvidia (primary HBM3E supplier) | Ramping production in 2026 |

| Samsung | ~32%-38% | Competing for Nvidia qualification | Ramping production in 2026 |

| Micron | ~21%-33% | Diversified AI infrastructure | Ramping production in 2026 |

Share ranges reflect differing methodologies across Counterpoint Research and Astute Group analyses.

The competitive battleground is shifting to HBM4 in 2026, and all three vendors are increasing production. For Samsung, a successful HBM4 qualification with Nvidia would be a material re-rating event. A continued share loss to SK Hynix or Micron would put pressure on margins and the stock’s premium multiple. The trillion-dollar milestone reflects upside optionality as much as current dominance.

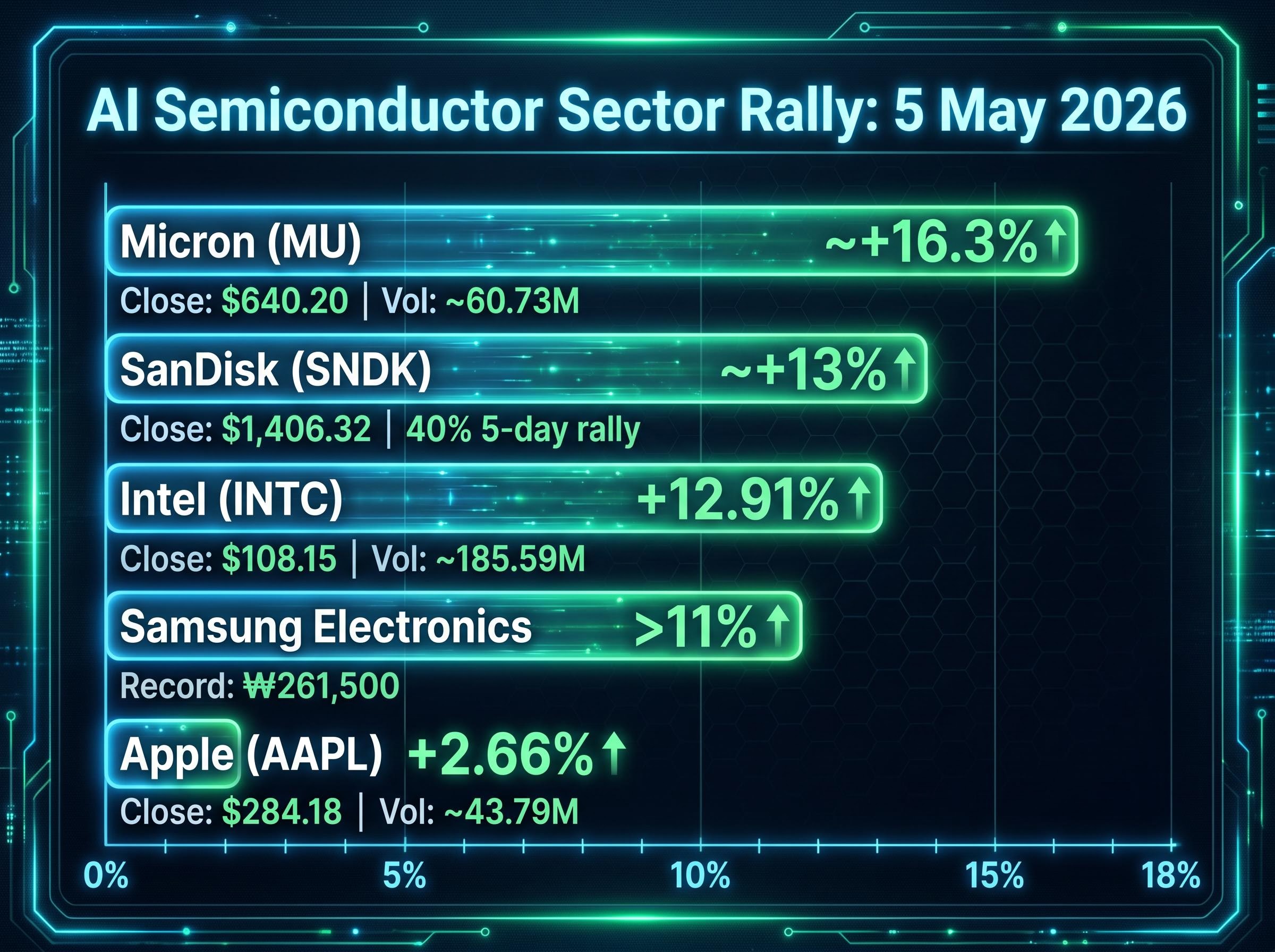

Samsung’s surge did not happen in isolation. The 5 May session produced a coordinated rally across AI-exposed semiconductor equities that signalled institutional capital rotating into the sector as a macro-level allocation.

| Company (Ticker) | Session Gain (%) | Closing Price | Approx. Volume |

|---|---|---|---|

| Intel (INTC) | +12.91% | $108.15 | ~185.59M shares |

| Micron (MU) | approximately +16.3% | $640.20 | ~60.73M shares |

| SanDisk (SNDK) | approximately +13% | $1,406.32 | 40% five-day rally |

| Apple (AAPL) | +2.66% | $284.18 | ~43.79M shares |

SanDisk, which now trades as a standalone entity following its spin-off from Western Digital, posted a 40% five-day rally alongside its single-session gain, underscoring that the momentum was building before the Apple catalyst crystallised it. Micron reached an intraday high reflecting a +16.3% gain before settling at the close figure.

The shared catalysts, Apple’s foundry diversification discussions and HBM demand acceleration, connected these moves. A sector-wide rally of this scale in a single session suggests institutional investors are treating AI semiconductor exposure as a thematic allocation, not a collection of isolated stock picks.

A 115%-125% year-to-date gain and a $1.196 trillion valuation invite scrutiny. The question is not whether the recent past was real, but whether the conditions that created it persist.

The risk case accumulates across several dimensions:

MarketScreener has characterised the post-milestone risk as a potential “morning-after hangover,” while ainvest.com analysis frames the $1 trillion mark as a possible “temporary rally” subject to post-milestone volatility.

Additional watch items include TSMC’s competitive response to Apple’s diversification talks, Chinese competitor advancement in memory and logic chips, and the impact of the broader macroeconomic rate environment on growth multiples. None of these risks have materialised as confirmed headwinds, but each represents a variable that could test the current valuation.

Investors wanting to stress-test the bull case more rigorously will find our full explainer on the AI hardware bubble thesis, which examines derivative market complacency, escalating inference costs that are making generative AI applications unprofitable, and the specific conditions under which hyperscaler capex deceleration could trigger a correction in semiconductor multiples.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Samsung’s re-crossing of the $1 trillion mark rests on three structural drivers: the HBM upcycle, Apple foundry optionality, and a sector-wide institutional rotation into AI semiconductor equities. The first is confirmed by pricing data; the second remains conditional on discussions that may or may not produce a formal agreement; the third is visible in a single session’s peer performance but untested over a longer horizon.

The forward indicators that will determine whether this valuation holds are specific:

Samsung crossing $1 trillion is a signal about where semiconductor capital is flowing globally. Whether the company stays above that line depends on execution, not sentiment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

As of 6 May 2026, Samsung Electronics has a market capitalisation of approximately $1.196 trillion, ranking it 11th globally and making it the first Korean company to cross the $1 trillion threshold.

The surge was driven by a Bloomberg report that Apple held preliminary talks with Samsung and Intel about manufacturing main processors in the United States, combined with accelerating global demand for high-bandwidth memory chips used in AI infrastructure.

High-bandwidth memory (HBM) is a specialised, high-value category of DRAM chip used at the core of AI accelerators; the HBM market is projected to grow from $2.93 billion to $16.72 billion by 2033, making it a critical revenue driver for Samsung's semiconductor division.

SK Hynix leads the HBM market with an estimated 35%-62% share and is Nvidia's primary HBM3E supplier, while Samsung holds approximately 32%-38% and is competing for Nvidia qualification, with Micron holding around 21%-33%.

The main risks include HBM3E price compression of approximately 28% year-over-year, the Apple foundry talks remaining exploratory with no confirmed agreement, geopolitical semiconductor tensions, and uncertainty over whether hyperscaler AI infrastructure spending will continue at current levels.