Vanguard VIHY Declares First Distribution at 49.49 Cents per Unit

1 hr ago

On 5 May 2026, two ASX-listed gold miners announced a deal that analysts broadly called strategically sound. Within 48 hours, the market had wiped roughly 14% off Regis Resources and 8.4% off Vault Minerals.

The proposed all-scrip merger between Regis Resources (ASX: RRL) and Vault Minerals (ASX: VAU) would create Australia’s third-largest ASX-listed gold producer, with combined output exceeding 700,000 ounces per annum, at a moment when AUD gold is trading near A$6,400 per ounce. The disconnect between analyst endorsement and investor punishment raises a question worth unpacking: is the market wrong, or is it seeing something analysts are choosing to downplay?

What follows is a dissection of the deal’s strategic logic, the valuation mechanics behind the EV/FCF case, and the specific structural features of the scrip exchange that explain the negative price reaction. The aim is to give readers a framework for assessing merger-of-equals transactions in the ASX gold sector.

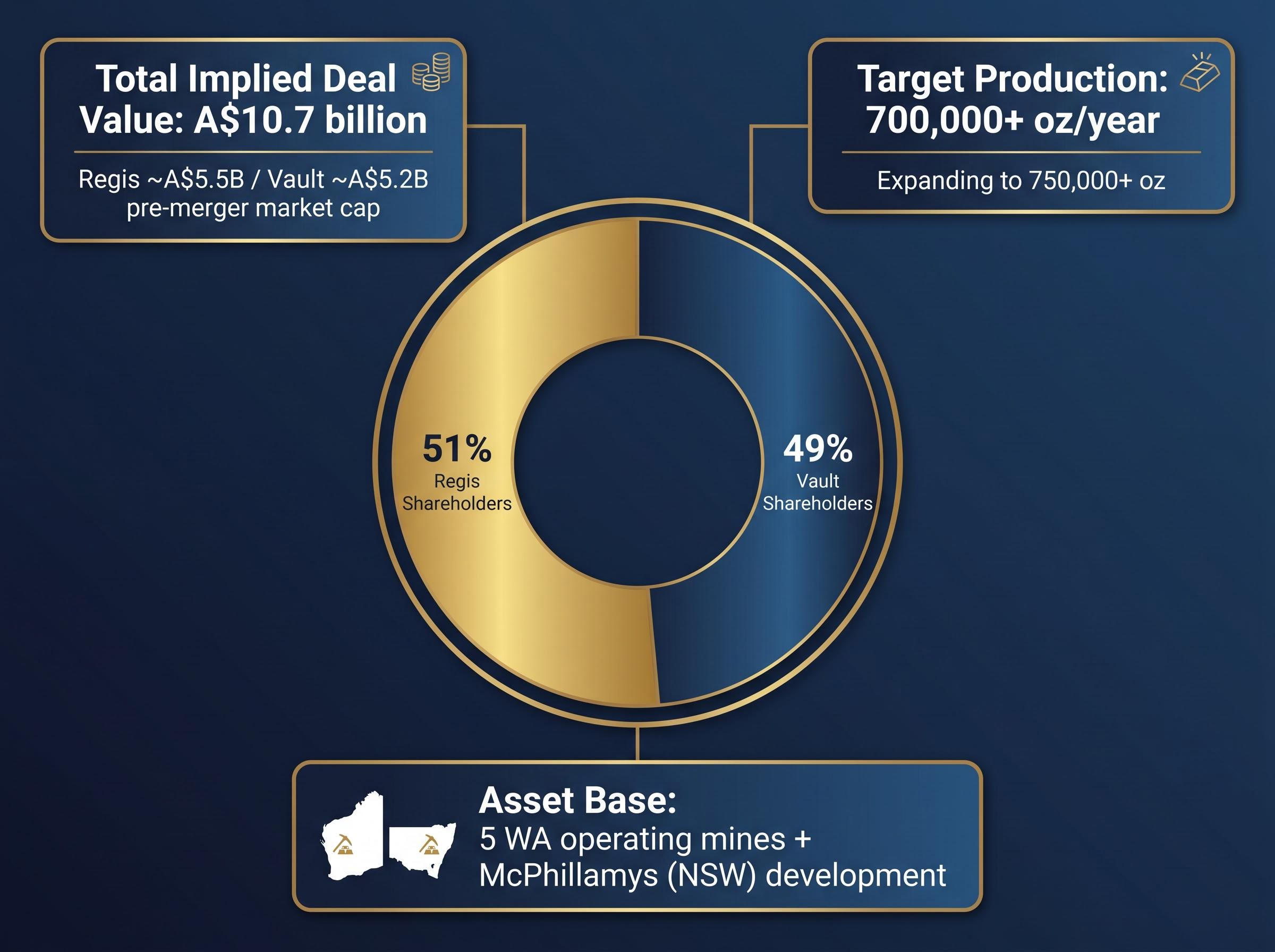

The transaction is structured as a scrip-for-scrip scheme of arrangement. Each Vault Minerals share converts into 0.6947 new Regis Resources shares, producing an ownership split of approximately 51% Regis shareholders and 49% Vault shareholders in the combined entity. At announcement, the implied deal value sat at approximately A$10.7 billion.

The combined group brings together five Western Australian gold operations under a single corporate umbrella. Production is targeted at 700,000+ ounces annually, with planned expansions lifting that figure toward 750,000+ ounces. Vault itself is a relatively recent creation, formed through the 2024 merger of Red 5 and Silver Lake Resources, meaning its asset base has already undergone one round of integration.

Key characteristics of the combined entity:

| Metric | Regis Resources (pre-merger) | Vault Minerals (pre-merger) | Combined Entity |

|---|---|---|---|

| Approximate market cap contribution | ~A$5.5 billion | ~A$5.2 billion | ~A$10.7 billion |

| Production profile | Mid-tier producer (WA assets + McPhillamys development) | Mid-tier producer (WA assets via Red 5 + Silver Lake) | 700,000+ oz/year |

| Key asset geography | Western Australia, New South Wales | Western Australia | Primarily Western Australia |

| Ownership stake in merged entity | ~51% | ~49% | 100% |

The strongest argument for the deal starts with scale. Neither Regis nor Vault, as standalone mid-tier producers, commands the capital market access, index weighting, or breadth of institutional coverage that a 700,000+ ounce producer attracts. The jump to third-largest ASX-listed gold producer changes the combined entity’s visibility in a way that neither company could replicate organically in the near term.

Institutional appetite for ASX gold exposure has been building well beyond the Regis-Vault deal itself, with the L1 Gold Fund IPO raising approximately A$900 million in commitments in March 2026 and the Broker Firm Offer closing early due to demand, a signal that the investor base for large-scale ASX gold positions was already expanding before this merger was announced.

The second pillar is financial engineering. The combined group carries in excess of A$500 million in carry-forward corporate tax losses (cited in merger materials; independent verification against financial filings is recommended). At a gold price of A$6,400/oz, free cash flow generation is substantial, and the ability to shelter that cash flow from corporate tax for an extended period represents a quantifiable, material benefit.

Tax loss context: At a sustained gold price of A$6,300/oz or above, the combined entity’s reported A$500 million+ in carry-forward tax losses could shield a meaningful portion of near-term free cash flow from corporate tax, a benefit that compounds over multiple reporting periods.

The three strategic pillars, in order of financial certainty:

Regis’s McPhillamys gold project in New South Wales adds a fourth dimension: development-stage optionality that could extend the combined group’s production life and growth trajectory beyond the existing Western Australian asset base.

The analyst consensus was positive. The share price reaction was not. That gap is not irrational; it reflects the specific mechanics of how scrip deals redistribute value and risk.

In a scrip-for-scrip merger, no cash changes hands. Instead, new shares are issued to the target’s shareholders, immediately diluting existing holders of the acquiring entity. The value of those new shares is then exposed to the combined entity’s price performance from day one, removing the certainty premium a cash component would provide. For Regis shareholders specifically, the 0.6947x exchange ratio means Vault shareholders receive 49% of the combined entity, a figure some institutional and retail investors viewed as generous relative to perceived asset contributions.

Academic research on acquirer share price reactions in scrip mergers consistently finds that the announcement-period return for the issuing company is negative on average, a result driven by the market interpreting new equity issuance as a signal that management considers its own shares fairly or fully valued at current prices.

RRL declined approximately 14% over two trading days, reaching an intraday level around A$6.24 on 6 May 2026. VAU fell approximately 7-8.4% over the same period, from A$4.640 to approximately A$4.315 on 5 May. The differential in selling pressure tells its own story: the market treated Regis as the party giving up more than it received. Net institutional selling in RRL was estimated at approximately A$45 million on 5 May (this figure is indicative and has not been independently verified).

Retail sentiment on platforms such as HotCopper reflected similar frustration, with an estimated 60% of posts on 5 May threads characterising the exchange ratio as unfavourable to RRL holders (unverified; consistent directionally with the price action).

Retail investor sentiment on gold had already shown signs of rotation before this deal was announced; gold buying activity fell below 70% of total gold-related trades on the Selfwealth by Syfe platform by Q1 2026 as capital shifted toward international ETFs and financial equities, providing context for why the HotCopper reaction to the Regis-Vault exchange ratio landed so sharply negative.

The arithmetic of a scrip exchange creates perceived winners and losers even when the underlying deal is value-neutral:

The Regis-Vault sell-off, while sharp, follows a pattern that has repeated across ASX gold M&A in recent years. That pattern is worth understanding before drawing conclusions about this specific deal.

A “merger of equals” designation signals that no control premium is being paid. Both sets of shareholders absorb deal risk symmetrically, and the combined entity’s re-rating depends entirely on operational delivery rather than a premium already locked in at announcement. This structure reliably produces initial selling pressure in the acquirer.

The most directly relevant precedent is the formation of Vault Minerals itself. The 2024 combination of Red 5 and Silver Lake Resources followed a similar pattern: initial scepticism about the exchange terms, a period of share price weakness, and subsequent performance that tracked gold price movements rather than deal-specific catalysts. The Ramelius Resources combination with Spartan Resources (announced March 2025) provides a second verified ASX mid-tier gold M&A comparable, where the acquirer experienced an initial dip before gold-price-correlated recovery.

| Transaction | Initial share price reaction | Subsequent performance driver |

|---|---|---|

| Vault Minerals (Red 5 + Silver Lake, 2024) | Initial acquirer weakness on dilution concerns | Gold price trajectory post-completion |

| Ramelius + Spartan Resources (March 2025) | Acquirer dip in 7-12% range | Gold price and operational delivery |

| Regis + Vault (May 2026) | RRL ~14%, VAU ~7-8.4% decline | Pending: gold price, IER outcome, integration |

The general pattern from verified ASX gold M&A: acquirer share prices typically experience initial dips of 7-12% on dilution concerns, with subsequent performance heavily correlated to gold price trajectory in the six months post-completion. Regis’s 14% decline sits at the outer edge of that range, which may reflect the additional uncertainty around the exchange ratio’s perceived fairness.

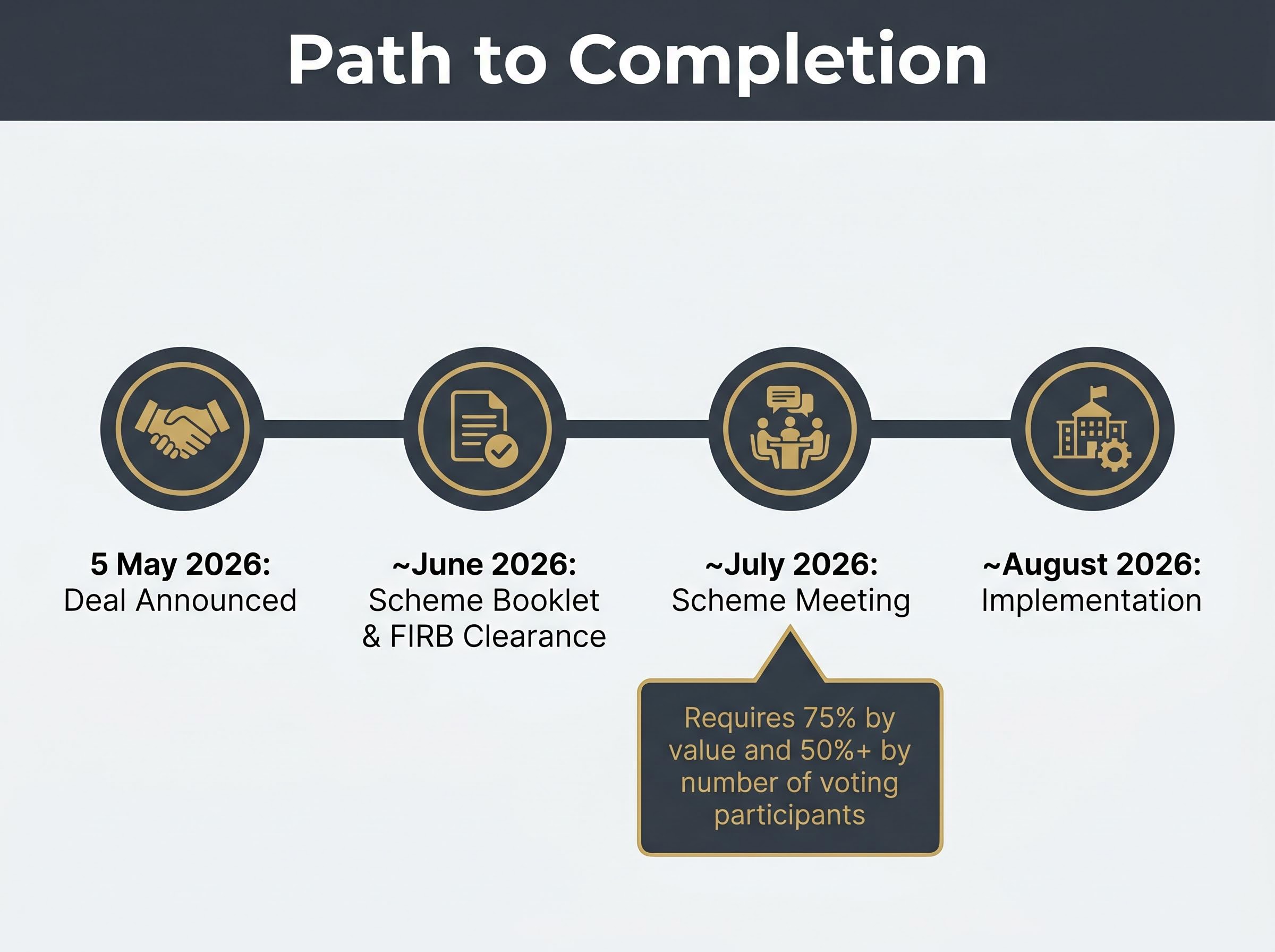

Approval threshold: Australian schemes of arrangement require approval by 75% by value and 50%+ by number of voting scheme participants. This dual threshold means a small number of large institutional holders can block a deal even if the majority of retail shareholders vote in favour.

Enterprise value to free cash flow (EV/FCF) measures how much investors are paying for each dollar of cash a company generates after all operating and capital expenses. For a gold producer sitting on A$500 million+ in tax losses, this metric captures something that the more commonly cited EV/EBITDA does not: the benefit of sheltered cash flows that reach shareholders without a corporate tax haircut.

At the combined entity’s post-announcement pricing, the indicative EV/FCF multiple sits at approximately 5.2x for 2026, declining to approximately 4.0-5.5x by FY28 under a sustained A$6,300/oz gold price assumption. These figures are broker-indicative and heavily gold-price-assumption-dependent.

The three variables that most affect the combined entity’s free cash flow:

The declining multiple trajectory implies that free cash flow is expected to grow materially post-merger. That growth is front-loaded by the tax loss shield rather than by operational cost synergies, which analysts acknowledge are limited given the assets’ similar geographic and operational characteristics. Combined free cash flow is estimated at approximately A$1.71 billion at the A$6,300/oz base case, against a deal value of approximately A$10.7 billion.

The question for investors is whether the post-sell-off entry point (implied 5.2x EV/FCF) adequately compensates for execution risk in a deal with limited near-term synergy upside beyond the tax benefit.

Mining sector valuation benchmarks show major gold and diversified miners currently trading at roughly 7-8x EV/EBITDA, compared to approximately 14x during the 2008-2010 commodity boom, which puts the combined entity’s post-sell-off EV/FCF multiple in a broader context of where institutional capital is pricing resource exposure today.

The deal follows the standard Australian scheme of arrangement pathway: Scheme Booklet publication (including the Independent Expert Report), followed by a Scheme Meeting where shareholders vote, and then implementation if approved. The indicative timeline from announcement to vote is approximately 10-12 weeks, placing the Scheme Meeting around July 2026.

Regulatory risk appears contained. ACCC opposition is considered unlikely given minimal overlap in producing assets. FIRB review is triggered by Vault’s offshore shareholder base (approximately 15% foreign ownership) but is assessed as low-risk given the domestic nature of the assets. Both boards have provided unanimous support, and no institutional dissent has been publicly flagged.

Three specific watch points for shareholders:

Investors wanting to see how these regulatory and voting milestones play out in practice will find our detailed coverage of the National Storage scheme approval process instructive; it traces the FIRB clearance, Independent Expert conclusion, and dual-threshold vote mechanics from a recently completed ASX scheme of arrangement, with specific focus on how board recommendations and proxy deadlines interact when large institutional holders are involved.

| Milestone | Indicative timing |

|---|---|

| Scheme Booklet publication (incl. Independent Expert Report) | Approximately 4-6 weeks post-announcement (~June 2026) |

| FIRB clearance deadline | Expected prior to Scheme Meeting (~June 2026) |

| Scheme Meeting (shareholder vote) | Approximately 10-12 weeks post-announcement (~July 2026) |

| Implementation (if approved) | Approximately 2-3 weeks post-vote (~August 2026) |

The market’s negative reaction and the analysts’ strategic endorsement are both rational responses to different time horizons and different risk tolerances. Neither is definitively wrong at this stage.

The deal’s thesis gets validated under specific conditions: gold holds at or above A$6,300/oz, the Independent Expert Report endorses the exchange ratio as fair and reasonable, and the combined entity executes on its production growth trajectory toward 750,000+ ounces. At the post-sell-off pricing, the implied 5.2x EV/FCF multiple represents a potential entry point for investors with a multi-year horizon on ASX gold exposure. It is not a deal designed to reward those seeking near-term re-rating catalysts.

Key risk: If AUD gold pulls back materially below A$6,300/oz before the Scheme Meeting, the deal’s financial rationale weakens significantly. The base case assumptions are conservative relative to current spot (A$6,401/oz), but that margin of safety is thinner than the headline numbers suggest.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced in this article are subject to market conditions, gold price movements, and various risk factors. Past performance does not guarantee future results.

The Regis Vault merger is an all-scrip scheme of arrangement announced on 5 May 2026, where each Vault Minerals share converts into 0.6947 new Regis Resources shares, creating a combined entity with an implied deal value of approximately A$10.7 billion and ownership split of roughly 51% Regis shareholders and 49% Vault shareholders.

Regis Resources shares fell approximately 14% in two trading days because scrip mergers dilute existing shareholders immediately, with no cash premium to offset the risk, and many investors viewed the 0.6947x exchange ratio as overly generous to Vault Minerals holders relative to perceived asset contributions.

The combined entity carries in excess of A$500 million in carry-forward corporate tax losses, which can shield a substantial portion of near-term free cash flow from corporate tax at the current elevated gold price of around A$6,400 per ounce, materially improving the effective cash returns to shareholders.

The indicative timeline places Scheme Booklet publication around June 2026, the shareholder vote at approximately 10-12 weeks post-announcement in July 2026, and implementation if approved around August 2026, subject to FIRB clearance and independent expert approval.

Australian schemes of arrangement require approval by 75% by value and more than 50% by number of voting scheme participants, meaning a small number of large institutional holders can block the deal even if most retail shareholders vote in favour.