Brent Crude Falls 4.5% as US-Iran Nuclear Talks Collapse

9 mins ago

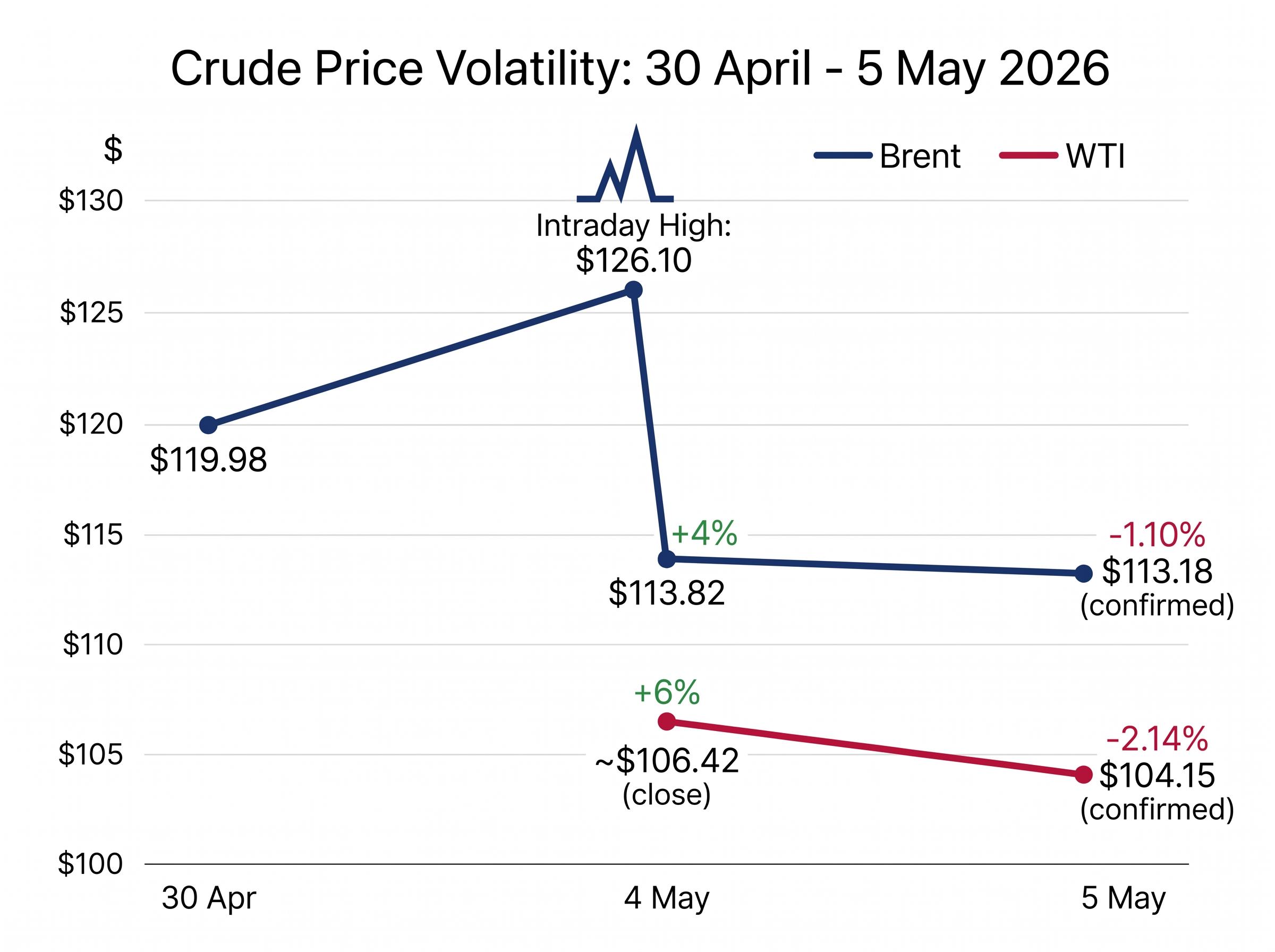

Brent crude swung more than 5% in a single session on 4 May 2026, reaching an intraday high of $126.10 per barrel before retreating to $113.18 the following morning as the United States denied Iranian claims of a frigate strike. That 24-hour arc captures the volatility now defining global oil prices.

Escalating military confrontations between US and Iranian forces in and around the Strait of Hormuz have ended a fragile ceasefire, threatening flows through a waterway that carries roughly 20% of global seaborne oil trade. The conflict has broadened beyond the Strait itself, with Iranian strikes on UAE energy infrastructure at Fujairah adding a new dimension to regional supply risk. What follows explains what happened in the past 24 hours, why it moved prices so sharply, what the Hormuz disruption means in quantitative terms, how OPEC+ has responded, and what the current price retreat does and does not signal about near-term direction.

The numbers tell the story before the narrative does. Brent crude fell to $113.18 per barrel on 5 May, down 1.10%, after closing at $113.82 the previous session. WTI crude dropped harder, falling to $104.15 per barrel, a decline of 2.14%. Both contracts had surged sharply on 4 May, with Brent climbing more than 4% and WTI finishing approximately 6% higher as renewed hostilities drove buying across both benchmarks.

The reversal came during Asian trading hours. The US denied Iranian claims of striking a US frigate, and the premium that had built on unverified military reports began to unwind. By 20:10 ET on 5 May, Brent sat at $113.93 and WTI at $105.05.

| Benchmark | 30 Apr close | 4 May close | 5 May (Asian session) | 5 May confirmed |

|---|---|---|---|---|

| Brent | $119.98 | $113.82 (+4%) | $113.93 | $113.18 (-1.10%) |

| WTI | — | ~$106.42 (+6%) | $105.05 | $104.15 (-2.14%) |

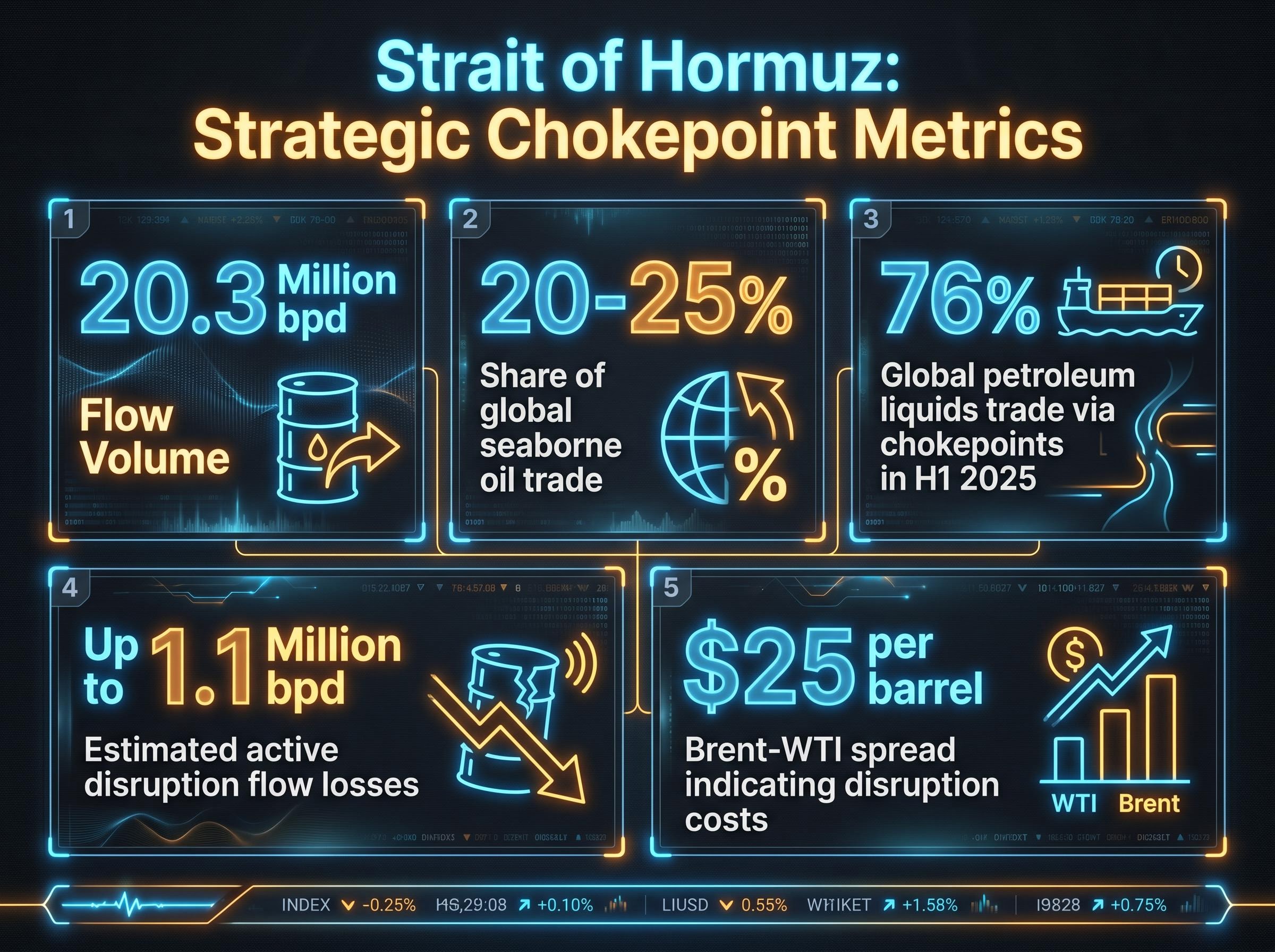

Brent-WTI spread: approximately $25 per barrel. This widened spread serves as a real-time proxy for Hormuz disruption costs, reflecting elevated shipping expenses, higher insurance premiums, and reduced flow volumes through the Strait.

Oil markets are now trading directly on military information flow. Unverified claims moved prices by several dollars before corrections occurred, a dynamic that energy investors and commodity traders need to account for when contextualising intraday swings.

The sequence began with Iran’s Revolutionary Guard Corps (IRGC). On 4 May, the IRGC launched cruise missiles at US warships and commercial vessels in and around the Strait of Hormuz, an action that ended what had been a tenuous ceasefire arrangement.

The 4-5 May price arc did not emerge in isolation; it followed the initial Hormuz closure on 30 April that drove Brent above $125 for the first time in approximately four years and removed an estimated 13 million barrels per day from global circulation, a supply shock the IEA described as unprecedented in modern scale.

The strikes then broadened beyond the Strait corridor. Iranian forces hit the Fujairah port oil terminal in the UAE, prompting the UAE to issue missile warnings following tanker drone strikes. Earlier reports of a South Korean cargo ship strike remain unconfirmed.

The widening of targets to UAE energy infrastructure carries different implications from Strait-only disruptions. Fujairah sits outside the Strait itself, and strikes on its terminal signal a willingness to target downstream infrastructure across the Gulf.

US Central Command (CENTCOM) reported successfully repelling Iranian drones, missiles, and small boat attacks while escorting two US-flagged vessels through the Strait under “Project Freedom.” The initiative aims to guide commercial shipping through safer Hormuz corridors, addressing the logistical challenge of transiting the waterway under active threat. The programme addresses shipping logistics, however, not the underlying geopolitical conflict, leaving markets exposed to further escalation regardless of escort success.

Approximately 20.3 million barrels per day transit the Strait of Hormuz, representing roughly 20-25% of global seaborne oil trade.

That figure represents a baseline. In the first half of 2025, approximately 76% of global petroleum liquids trade moved through major maritime chokepoints, and Hormuz is the largest single bottleneck in that system.

The current disruption translates that strategic significance into measurable cost. Active conflict has produced flow losses estimated at up to 1.1 million barrels per day, depending on the trajectory of escalation. The disruption operates across multiple layers simultaneously:

The Brent-WTI spread at $25 per barrel is the market’s quantitative read-out of these combined costs. For investors evaluating whether current price levels are proportionate to the supply threat, the specific barrels-at-risk figure, up to 1.1 million per day, provides a concrete framework. Even partial disruption to a chokepoint of this scale carries outsized global price effects.

The retreat from $126 intraday highs to the $113 range is not explained by the US frigate denial alone. OPEC+ has introduced a genuine supply-side counterweight.

Eight member countries, Saudi Arabia, Russia, Iraq, Kuwait, Kazakhstan, Algeria, and Oman, agreed to boost production by 411,000 barrels per day in May 2026. Separately, OPEC+ announced a 188,000 barrels per day output increase for June 2026, framed as a stabilisation signal to global markets.

The UAE departure from OPEC+ on 1 May 2026 adds a structural dimension to the supply picture that the production increase figures do not fully convey; with ADNOC now targeting 5 million barrels per day independently, the alliance’s enforcement architecture has weakened at precisely the moment coordinated output management carries the most market weight.

| Supply factor | Volume (barrels per day) | Direction |

|---|---|---|

| Estimated Hormuz flow disruption | Up to 1,100,000 | Supply reduction |

| OPEC+ May production increase | 411,000 | Supply addition |

| OPEC+ June production increase | 188,000 | Supply addition |

The arithmetic is clear: OPEC+ increases do not fully offset the disruption volume. They do, however, change the narrative from a straightforward supply shock to a contested dynamic. Saudi Arabia and other Gulf producers with pipeline and Red Sea export alternatives are positioned to partially bypass Hormuz-dependent routes, adding supply that does not require Strait transit. This contested balance is the primary reason prices have pulled back from peak levels rather than consolidating above $120.

The 5 May pullback was triggered by one thing: the US denial that Iran struck a US frigate. It was an informational correction, not a diplomatic breakthrough.

No verified ceasefire signals, no diplomatic progress, and no State Department statements have been confirmed as of 5 May 2026. The underlying conflict remains active, with CENTCOM continuing escort operations and Iranian forces having demonstrated willingness to strike UAE infrastructure beyond the Strait itself.

The geopolitical risk premium embedded in Brent does not require a physical blockade to hold; even where transit remains technically open, the threat of interdiction sustains elevated prices, as Goldman Sachs and JPMorgan’s approximately $30 per barrel divergence in year-end Brent forecasts illustrates the scale of institutional uncertainty around whether this premium persists.

General analyst consensus holds that upside risk remains the dominant scenario while US-Iran tensions persist and Hormuz transit remains threatened. Markets have already demonstrated the capacity to price Brent at $126.10 intraday.

The conditions that would drive a return toward those levels are specific and identifiable:

For energy investors and commodity traders, the distinction matters. A price pullback driven by a denied claim carries different positioning implications from one driven by genuine de-escalation. The structural risk premium embedded in crude remains intact.

The variables that will determine whether the $110-$114 Brent range holds or breaks are specific enough to monitor directly:

The downstream effects of sustained Brent in the $113-$126 range extend beyond energy markets. Analysts have flagged potential impacts on global inflation, consumer fuel prices, and equity market stress. The Brent-WTI spread at $25 per barrel signals elevated shipping costs that reach beyond crude oil into broader commodity logistics, adding pressure to supply chains already sensitive to energy input costs.

BIS research on oil supply shocks estimates that a 10% rise in oil prices driven by reduced global supply lowers GDP for the average advanced economy by around 0.5% over two years, a transmission mechanism that gives the current Hormuz disruption implications well beyond energy sector pricing.

The 5 May price pullback reflects a specific informational correction, not de-escalation. The structural risk premium in crude oil remains intact as long as three forces remain unresolved: military developments in the Strait, the scale and compliance of the OPEC+ supply response, and any verified diplomatic progress between Washington and Tehran. The next CENTCOM statement and any confirmed diplomatic contact are the immediate variables with the capacity to move prices in either direction.

For investors wanting to contextualise current crude levels against long-run equity outcomes, our full explainer on historical oil shock patterns examines S&P 500 returns across the 2008, 2011, and 2022 episodes when Brent crossed $100, covering Goldman Sachs supply deficit estimates, Morgan Stanley and JPMorgan positioning guidance, and the academic evidence on why reactive retail trading during oil volatility has historically underperformed patient strategies.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and these forward-looking assessments are subject to change based on market developments and conflict dynamics.

The Strait of Hormuz is the world's most critical oil shipping chokepoint, with approximately 20.3 million barrels per day transiting it, representing roughly 20-25% of global seaborne oil trade. Any disruption to flows through the Strait causes immediate and outsized effects on global crude prices.

Brent crude surged more than 4% on 4 May 2026 after Iran's Revolutionary Guard Corps launched cruise missiles at US warships and commercial vessels near the Strait of Hormuz, then retreated when the US denied Iranian claims of striking a US frigate, unwinding the geopolitical risk premium built on unverified reports.

Active military conflict in and around the Strait of Hormuz has produced flow losses estimated at up to 1.1 million barrels per day, with OPEC+ production increases of 411,000 barrels per day in May and 188,000 barrels per day in June only partially offsetting that disruption.

The Brent-WTI spread widened to approximately $25 per barrel, serving as a real-time proxy for Hormuz disruption costs that reflects elevated shipping expenses, higher insurance premiums, and reduced flow volumes through the Strait.

Further confirmed strikes on commercial vessels near the Strait, verified damage to additional Gulf export terminals, failure of US escort operations under Project Freedom, or escalation of Iranian strikes to additional Gulf state targets could all drive prices back toward the $126.10 intraday peak recorded on 4 May 2026.