The Monthly Reset Framework That Reduces Couples’ Money Fights

just now

One-third of couples cite money as a primary source of conflict, yet most never establish a shared financial system before the first argument begins. The disconnect is striking: income level has almost no bearing on whether couples fight about money. How partners manage finances together, the conversations they have, the systems they build, and the assumptions they leave unspoken, determines whether money becomes a source of partnership or a source of erosion. Financial conflict is not a personality flaw. It is a systems problem, and systems can be built.

This guide covers the psychology behind why money fights happen, the three conversations that prevent most of them, and a clear comparison of the main expense-splitting models so couples can choose the structure that fits their circumstances. Whether partners are combining finances for the first time or rebuilding trust after years of unspoken tension, what follows is a practical framework for turning money from a recurring argument into a shared project.

Financial arguments are rarely about the dollar amount on a receipt. They function as proxy conflicts for deeper tensions around control, trust, and life priorities, tensions that money makes visible but does not cause.

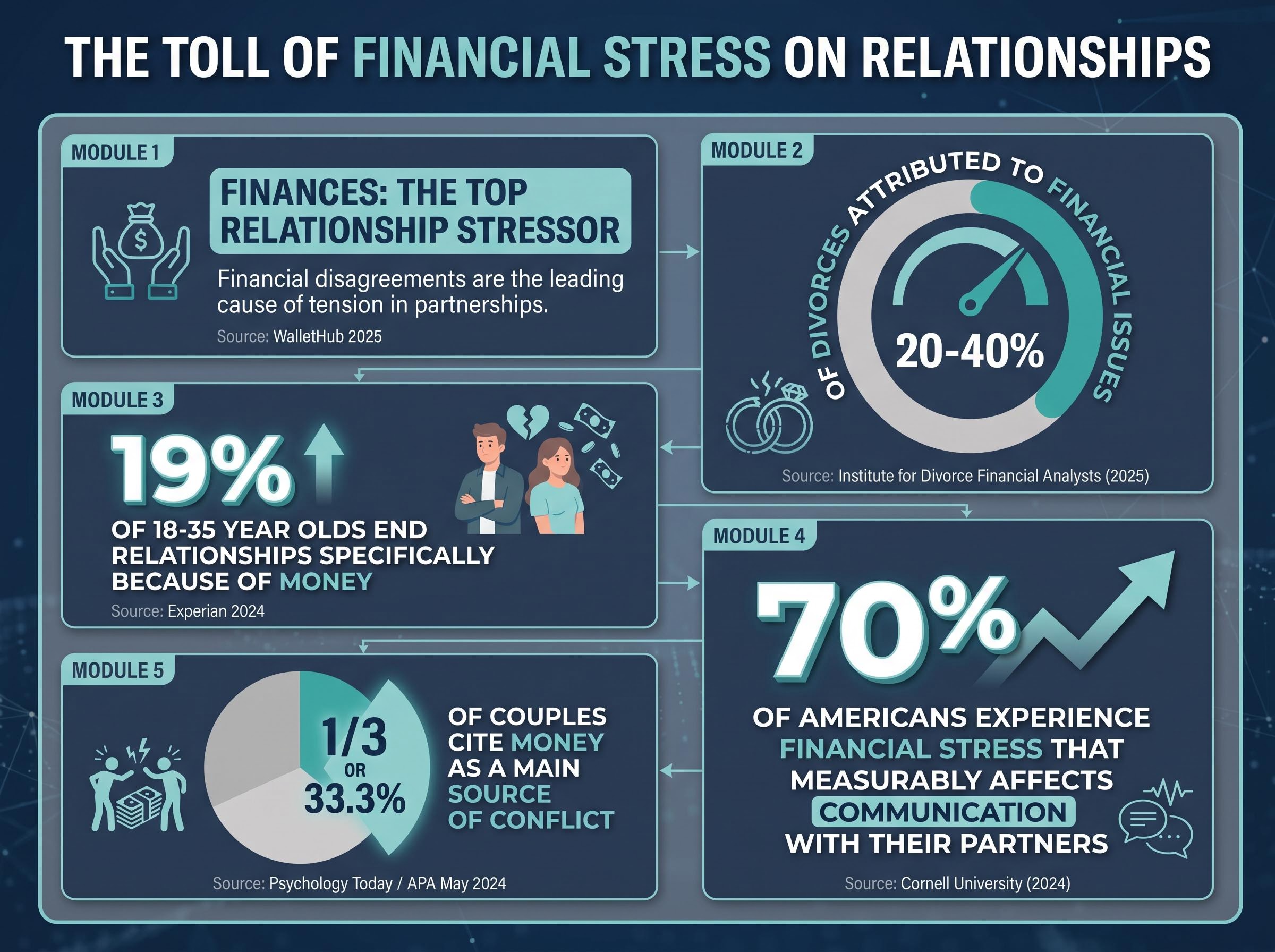

A WalletHub 2025 survey identified finances as the top relationship stressor among couples. The Institute for Divorce Financial Analysts (2025) attributes 20-40% of divorces to financial issues. Among younger adults, the pressure is sharper still: Experian’s 2024 survey found that 19% of 18-35 year olds report ending relationships specifically because of money.

Cornell University (2024): 70% of Americans experience financial stress that measurably affects communication with their partners. The worse the financial pressure, the less likely couples are to discuss it openly, creating a compounding cycle where the problem becomes harder to address the longer it persists.

That compounding cycle is where the real damage occurs. Financial stress does not just cause arguments; it actively suppresses the communication needed to resolve them. Partners stop talking, assumptions fill the silence, and resentment builds without an outlet.

Underneath most recurring money conflicts sit three categories of tension:

Recognising these patterns reframes the problem. Couples who have assumed they are fundamentally incompatible may instead recognise that they have an incompatible system, a far more solvable problem.

The most common household tension is not about budgets or bank balances. It is about two people with different relationships to money’s purpose, each convinced their instinct is the rational one.

Research referenced in Psychology Today (May 2024), drawing on APA data, confirms that approximately one-third of couples cite money as a main source of conflict. Much of that friction traces back to a single dynamic: the saver-spender divide.

A partner who grew up watching parents struggle to cover rent may carry that anxiety into a household earning six figures. The fear is not about the current balance; it is about the feeling that security can vanish.

Journal of Financial Therapy research on couple financial communication links parental financial socialization directly to financial self-efficacy in adult relationships, providing empirical grounding for the observation that deeply held money beliefs formed in childhood shape how partners communicate about finances decades later.

Neither orientation is wrong. The Financial Therapy Association, the primary professional body for financial therapy, combines financial planning knowledge with therapeutic technique to help couples address exactly these deep-seated patterns. Financial therapy is distinct from both couples therapy and financial advising; it specifically targets money anxiety and attachment-related money behaviour.

The research-supported goal is not to convert a saver into a spender or vice versa. It is to find a system that accommodates both, so disagreements become information rather than attacks.

Three conversations, held before the pressure builds, prevent most recurring money arguments. They are ordered here from easiest to most revealing, so couples build momentum rather than dread.

“The most effective financial arrangement is whichever one both partners perceive as equitable.”

That principle, supported consistently across financial therapy research, means there is no universally correct answer. What works is what both partners experience as fair given their circumstances. Couples who revisit these arrangements periodically, as incomes change, children arrive, or career breaks occur, experience fewer resentment-driven conflicts than those who set a system once and never revisit it.

No single model works for every couple. What follows is a comparison of the three most common approaches, each suited to different circumstances and life stages.

| Model | How it works | Best suited for | Key advantage | Key limitation |

|---|---|---|---|---|

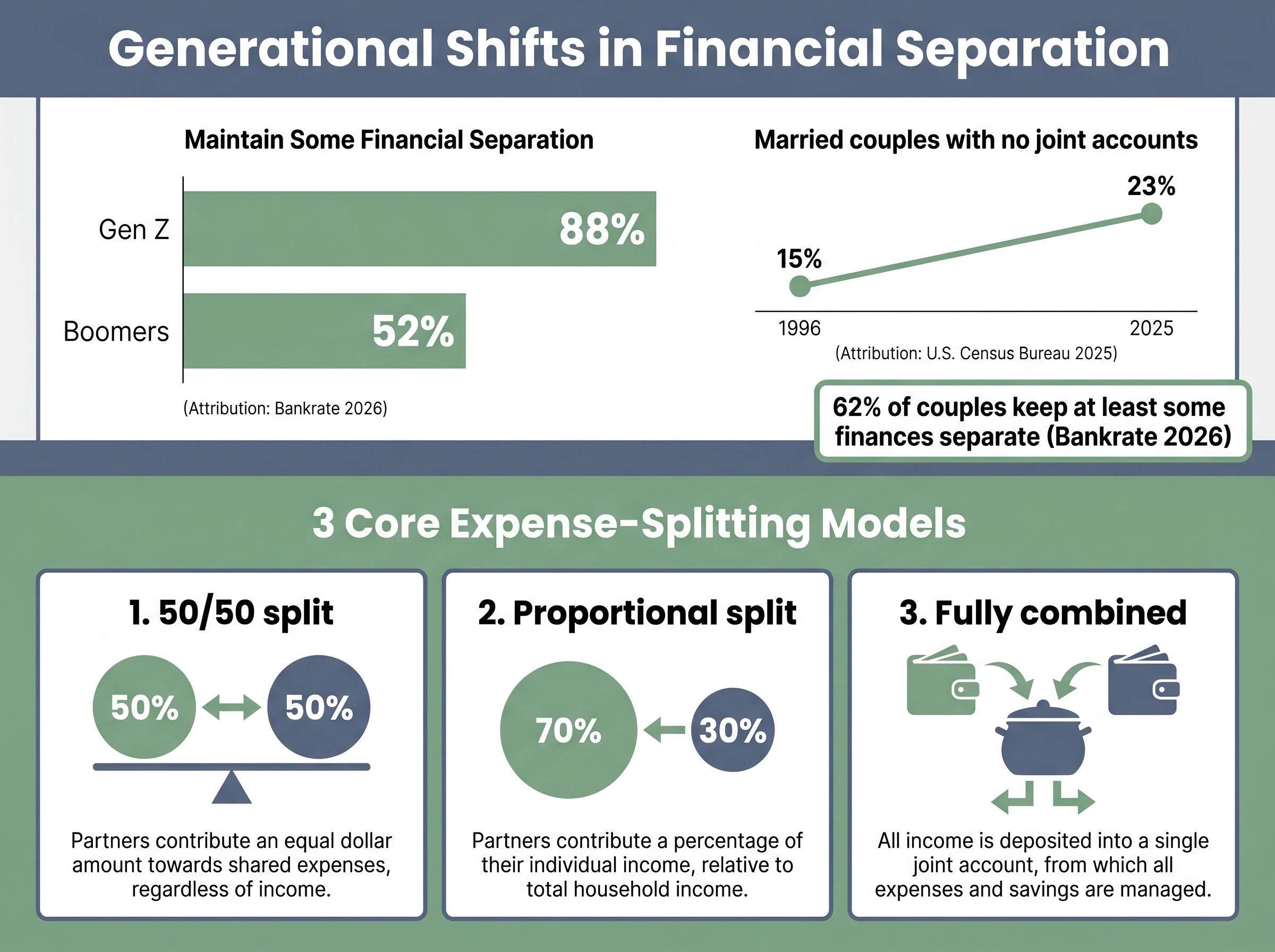

| 50/50 split | Each partner contributes equally to all shared expenses | Couples with similar incomes | Simple, perceived as fair when earnings are comparable | Can create hardship when one partner earns significantly less |

| Proportional split | Each partner contributes a percentage of their income to shared costs | Couples with meaningful income differences | Adjusts for earning disparity; often perceived as more equitable | Requires income transparency and periodic recalculation |

| Fully combined | All income flows into a shared account; individual discretionary spending is allocated from the whole | Couples with high mutual trust and shared long-term goals | Simplifies household financial management; reinforces partnership | Can feel restrictive if discretionary allowances are not clearly defined |

It is normal for couples to move through several models over the course of a relationship. A 50/50 split may work when both partners earn similar salaries, then shift to proportional when one takes a career break, then evolve toward fully combined when shared assets and children make separation impractical.

The generational data confirms that no single model dominates. According to U.S. Census Bureau 2025 data, 23% of married couples maintain no joint accounts, up from 15% in 1996. Bankrate’s 2026 survey found that 62% of couples keep at least some finances separate, with approximately 88% of Gen Z couples maintaining some separation compared to approximately 52% of boomers.

For some individuals, maintaining separate finances is not merely a preference but a protective measure. An emerging strand of 2025 discourse, including analysis published by The Guardian, frames financial autonomy as a safeguard against financial abuse or coercive control within relationships.

Mandatory financial merging or allowance-controlled spending where one partner holds decision-making power can, in extreme cases, constitute financial abuse. Readers who suspect financial control is a factor in their relationship should seek professional support. The point is not to stigmatise the majority of couples for whom joint finances work well; it is to acknowledge that a single model does not fit every situation.

NNEDV guidance on financial abuse identifies tactics such as withholding money, controlling access to shared assets, and assigning an allowance as recognised forms of economic abuse, providing a clear framework for distinguishing a mutually agreed financial system from one that functions as coercive control.

A system only works if couples use it. The most reliable approach, recommended consistently by financial therapists and relationship experts, is a structured monthly review that takes approximately 30 minutes.

One individual discovered, through regular spending review, that duplicate car insurance charges had gone unnoticed for three years. A business owner identified $40,000 in annual dining spend that prompted a reassessment of the household’s discretionary budget. These are the kinds of patterns that only surface with routine examination.

When a month of overspending occurs, a no-spend or low-spend month can serve as a calibration tool: restrict discretionary categories (dining out, clothing, entertainment) and identify free or low-cost substitutes. This is not a punishment; it is a practical rebalancing mechanism.

Several budgeting tools are designed specifically for couples. When selecting one, the features that matter most include:

Among current options, Honeydue was highlighted by Forbes Advisor 2026 as a top pick for shared budgeting. YNAB (You Need a Budget) and EveryDollar were both ranked by U.S. News 2025 among leading options for couples managing budgets together.

Some financial conflicts resist practical solutions because they are not really about money. When a couple has a good system in place and still finds money conversations triggering recurring conflict, the issue may sit deeper than any spreadsheet can reach.

Three types of professional support address different dimensions of the problem:

| Type | What it addresses | Best for | Typical format |

|---|---|---|---|

| Couples therapy | Relational dynamics, communication patterns, emotional safety | Couples whose money conflicts reflect broader relationship tension | Regular sessions with a licensed therapist |

| Financial therapy | Money scripts, financial anxiety, attachment-related money behaviour | Couples who have a working system but still feel stuck or triggered | Sessions combining financial planning with therapeutic technique |

| Financial advising or coaching | Practical budgeting, debt management, goal-setting | Couples who need a structural plan but not psychological support | Consultations focused on financial planning and accountability |

Financial therapy, facilitated through the Financial Therapy Association, is the most targeted intervention when money conflict feels irresolvable despite having a practical system in place. It specifically addresses root causes: financial fears, attachment patterns, and childhood money scripts that shape how each partner relates to money at an unconscious level.

Research consistently links both couples therapy and financial therapy with reduced risk of relationship breakdown when financial conflict is severe or chronic. Seeking professional help is not evidence of failure. It is recognition that some patterns require more than a budget to resolve.

Financial harmony is not a function of compatibility or income. It is the product of deliberate shared systems, ongoing communication, and periodic adjustment as life circumstances change.

The progression is straightforward: understand the psychology behind money conflict, have the three conversations that replace assumption with agreement, choose the expense-splitting model that fits current circumstances, establish a monthly review routine, and know when to call in professional support.

None of this requires perfection. It requires a first step. That step might be scheduling a money conversation this week, downloading a budgeting app, or looking up a financial therapist. The specific action matters less than the decision to stop treating money as something that happens to a relationship and start treating it as something two people build together.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The three main models are a 50/50 split (best when incomes are similar), a proportional split based on each partner's income (better when earnings differ significantly), and a fully combined approach where all income flows into a shared account. The most effective model is whichever both partners genuinely perceive as fair given their current circumstances.

Financial arguments are rarely about specific dollar amounts; they are proxy conflicts for deeper tensions around control, trust, and differing life priorities. Research shows that income level has almost no bearing on whether couples fight about money, while the systems and communication habits couples build together are the primary determining factors.

Couples should set a shared savings goal with a concrete number and timeline, agree on individual discretionary spending allowances that require no justification, and explicitly choose an expense-splitting model together rather than leaving it as an unspoken assumption.

Financial therapy, facilitated through the Financial Therapy Association, combines financial planning knowledge with therapeutic technique to address money scripts, financial anxiety, and attachment-related money behaviour. Unlike couples therapy, which focuses on broader relational dynamics, financial therapy specifically targets the root causes of money conflict at a psychological level.

Financial therapists and relationship experts consistently recommend a structured monthly review of approximately 30 minutes, covering household income, total expenditure, progress toward shared savings goals, and any upcoming irregular expenses for the following month.