Approximately 67% of investors worldwide use dollar-cost averaging as of 2026. Yet decades of historical data show lump-sum investing outperforms it roughly 68-73% of the time across every major market studied. The tension between mathematical optimality and behavioural reality sits at the heart of one of investing’s most persistent debates, and with elevated market volatility through 2025-2026 and retail investors adding over $302 billion to U.S. stocks in 2025 alone, the practical stakes have rarely been higher. What follows is a precise breakdown of how dollar cost averaging works at a mechanical level, what the research actually says about its performance relative to lump-sum investing, and how to determine which strategy fits a specific situation and temperament.

How dollar-cost averaging actually works: the mechanics behind the method

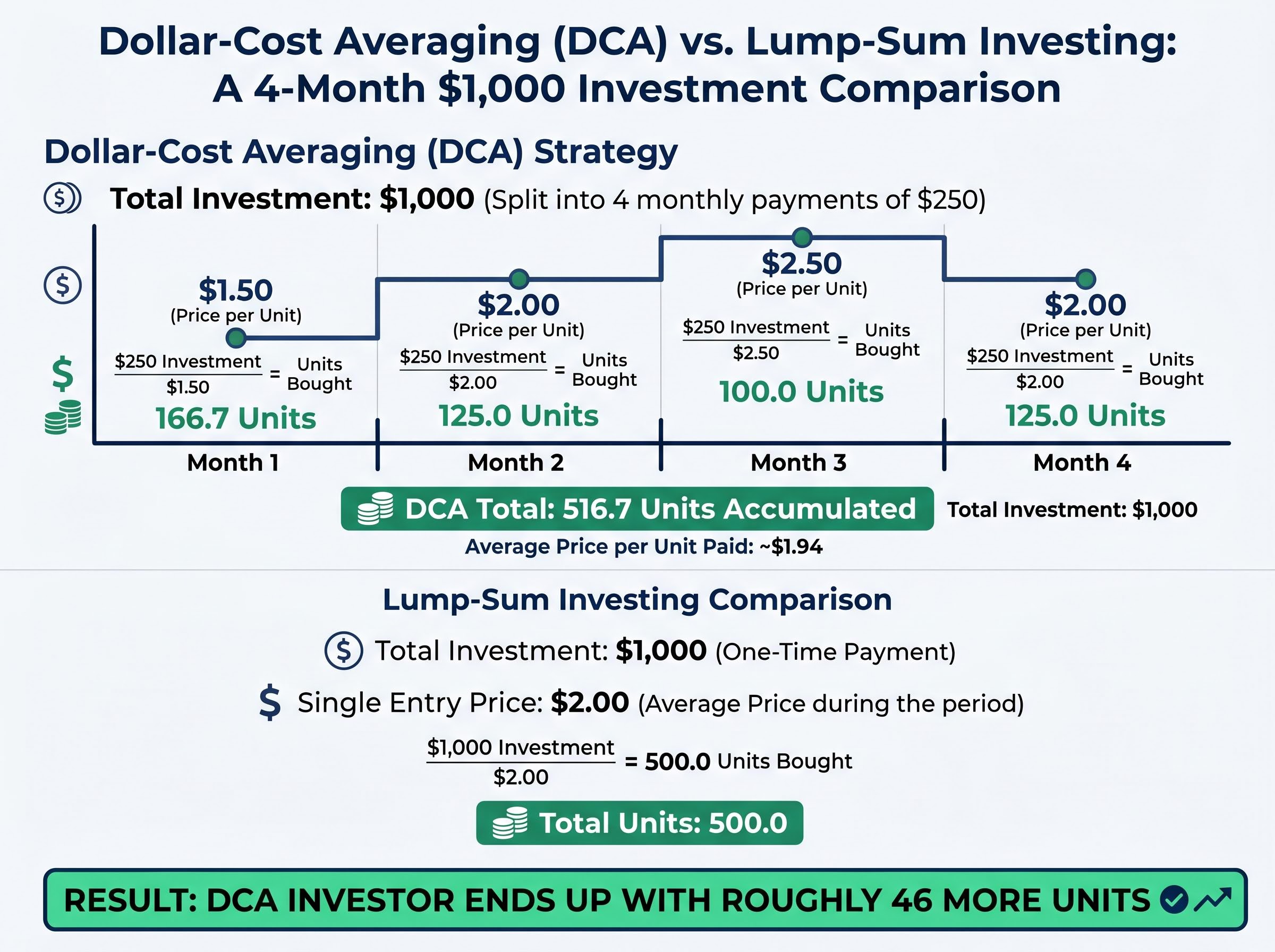

Consider an investor with $1,000 to deploy over four months, investing $250 each month into the same asset. The unit price moves: $1.50 in month one, $2.00 in month two, $2.50 in month three, and $2.00 in month four.

| Month | Unit Price | Units Purchased ($250) | Cumulative Units |

|---|---|---|---|

| 1 | $1.50 | 166.7 | 166.7 |

| 2 | $2.00 | 125.0 | 291.7 |

| 3 | $2.50 | 100.0 | 391.7 |

| 4 | $2.00 | 125.0 | 516.7 |

| Lump-sum comparison | $2.00 (average) | 500.0 | 500.0 |

The DCA investor ends up with 516.7 units, roughly 46 more than the lump-sum investor who deployed the same $1,000 at the average price of $2.00. The insight is not about predicting price direction. Fixed-dollar purchases create an asymmetric unit-acquisition effect: the same amount buys disproportionately more units when prices are low and fewer when prices are high, pulling the average cost per unit below the simple average of the prices paid.

Three mechanical rules define the strategy:

- Invest a fixed monetary amount each interval, not a fixed number of units.

- Maintain a fixed schedule (weekly, fortnightly, monthly) regardless of market conditions.

- Remain price-agnostic: the commitment is to the schedule, not to a view on where prices are heading.

When big ASX news breaks, our subscribers know first

What the research actually says: lump-sum vs. DCA performance data

The data is consistent, and it does not favour DCA. Across multiple independent studies spanning different markets, time horizons, and methodologies, lump-sum investing outperforms dollar-cost averaging in a clear majority of historical periods examined.

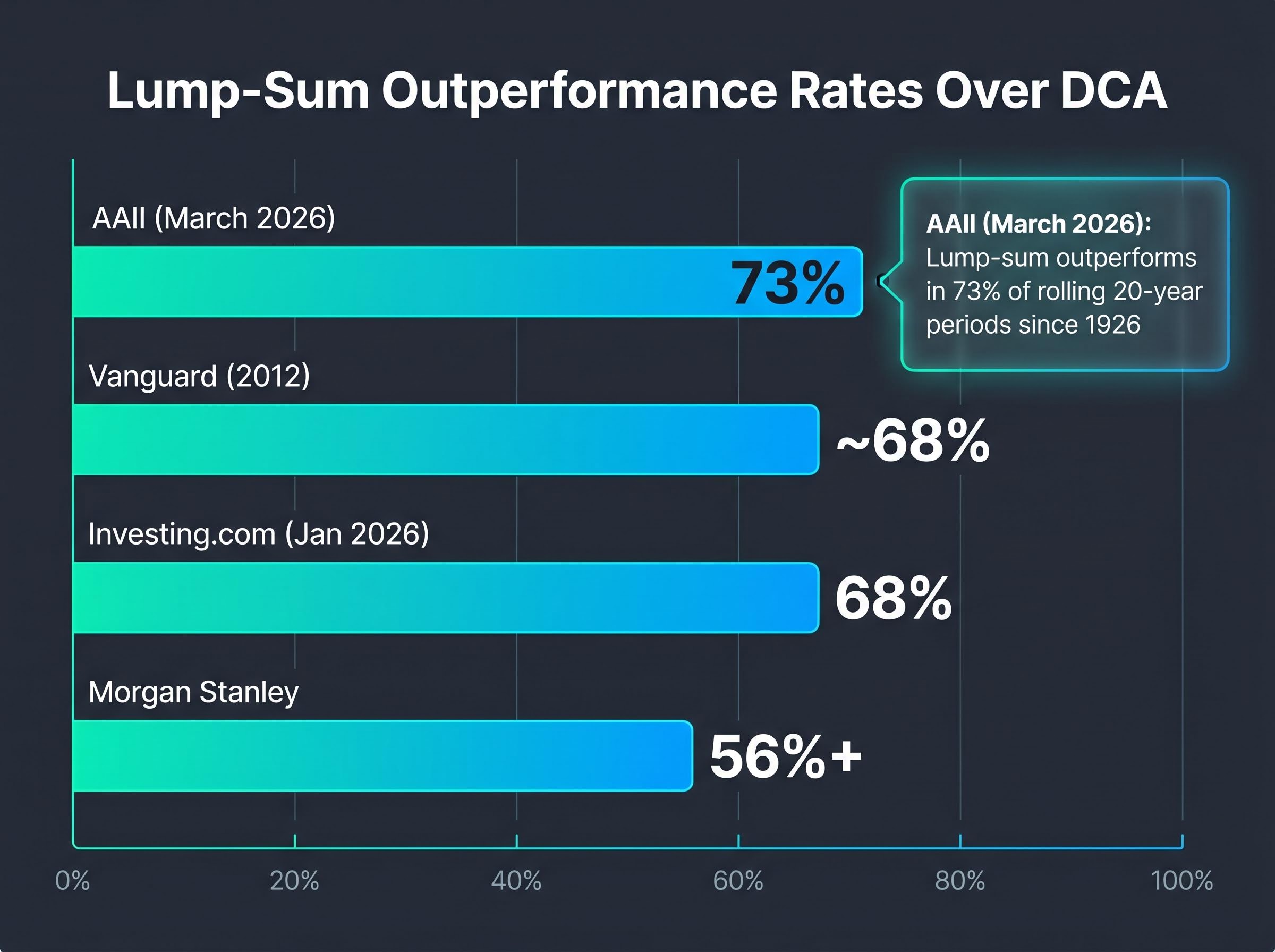

Vanguard’s 2012 research on lump-sum vs. DCA examined rolling 10-year periods across the U.S., U.K., and Australian markets and found lump-sum investing outperformed approximately two-thirds of the time, establishing the foundational dataset that subsequent studies have consistently replicated.

| Study / Source | Market Examined | Time Horizon | Lump-Sum Outperformance Rate |

|---|---|---|---|

| Vanguard (2012) | U.S., U.K., Australia | 10-year rolling periods | ~68% |

| AAII (March 2026) | U.S. | Rolling 20-year periods since 1926 | 73% |

| Investing.com (January 2026) | U.S. | 10-year periods (12-month DCA) | 68% |

| Morgan Stanley | U.S. | 1,000+ overlapping 7-year periods | 56%+ (0.42% annualised edge) |

According to AAII’s March 2026 analysis, lump-sum investing outperforms dollar-cost averaging in 73% of rolling 20-year periods since 1926.

The explanation is structural rather than mysterious. Equity markets deliver positive returns in approximately 70-75% of 12-month periods. Cash held on the sidelines during a DCA deployment schedule earns less than the equity market it has not yet entered. For a 60/40 portfolio over a 10-year horizon assuming an 8% average return, Vanguard’s modelling showed a lump-sum growing $2 million to approximately $4.3 million, while a 2-year DCA approach reached approximately $4.1 million, a gap of roughly $200,000.

Extending the DCA window compounds the cost. A 36-month DCA schedule pushes lump-sum outperformance to approximately 90% of historical periods. The longer capital waits, the more upside it forfeits.

The behavioural case for DCA: why the “inferior” strategy often wins in practice

If the maths favours lump-sum investing so consistently, the question becomes why 67% of investors still use DCA. The answer is not that they misunderstand the data. It is that mathematical optimality assumes an investor who executes perfectly, and most investors do not.

Lump-sum investing requires deploying all available capital at once and then holding through whatever follows. In practice, that creates specific failure modes:

Kahneman and Tversky’s prospect theory established that losses loom psychologically larger than equivalent gains, a finding that directly explains why investors who deploy a full lump sum before a sharp correction experience disproportionate pressure to sell, even when their long-term thesis remains intact.

- Panic-selling during drawdowns: An investor who deployed a full lump sum days before a 10-15% correction faces acute psychological pressure to sell at a loss.

- Indefinite delay: Waiting for a “better entry” often means never investing at all, as every price feels too high or too uncertain.

- Emotional market timing: Attempting to pick the optimal entry point introduces the very timing risk that long-term investing is supposed to avoid.

- Over-monitoring during volatile periods: A large single-entry position amplifies the temptation to check daily returns and react to short-term noise.

DCA neutralises each of these. The schedule removes the decision from the moment. Retail traders added approximately $302 billion to U.S. stocks in 2025, up 53% from 2024, with automatic contribution plans such as 401(k) and superannuation schemes structurally embedding DCA into participation. That structural commitment kept capital flowing through the interest rate uncertainty and inflation swings of 2025-2026, periods when manual lump-sum investors faced genuine behavioural headwinds.

Behavioural return drag is not merely a theoretical concept: global behavioural finance research estimates a cost of approximately 1.5% per annum attributable to emotionally driven decisions, and the Australian CGT structure amplifies this figure further for investors who sell within the 12-month discount threshold, compounding the cost of every poorly timed exit.

The middle-ground option: combining both strategies

Johnson Investment Counsel noted in September 2025 that a partial lump-sum approach, deploying a significant portion immediately while DCA-ing the remainder over a defined window of 6-12 months, offers a rational compromise. This hybrid reduces the mathematical cost of pure DCA (less capital sitting idle) while limiting the behavioural risk of full lump-sum exposure at a potentially volatile entry point.

When DCA genuinely outperforms: specific scenarios where the maths flips

DCA is not merely a behavioural crutch. Under specific market conditions, it produces genuinely superior returns.

- Sustained market declines. The 2008 financial crisis remains the canonical example. Investors who began deploying capital near the 2007-2008 peak and continued purchasing on a fixed schedule bought progressively cheaper units throughout the decline. Their average cost basis fell well below any single-entry point available in the 12 months prior to the trough.

- Peak-entry environments. Investors during the COVID era who applied DCA across the 2020 drawdown and subsequent recovery benefited from lower average entry prices compared to a single lump-sum deployed at the 2021 peak. The same mechanism applies to any period where an investor’s available capital coincides with a market high they cannot identify in real time.

- Highly volatile asset classes. El Salvador’s government-backed Bitcoin DCA strategy, initiated following legal tender adoption in 2021, accumulated holdings steadily through extreme crypto volatility through 2025. The strategy’s capacity to reduce average cost basis during significant drawdowns demonstrated DCA’s practical value in assets with price swings too wide for most investors to time.

A $100,000 lump-sum invested at end-2008 grew to approximately $1,049,000 by end-2025, a multiplier of roughly 10.49x. That figure illustrates the compounding power of immediate entry in a sustained bull market, and equally illustrates the cost if a lump-sum investor had entered at the 2007 peak instead.

The counterpoint is equally instructive. Stretching a DCA schedule to 36 months raises lump-sum outperformance to approximately 90% of historical periods. Longer DCA windows compound the timing cost in normally functioning markets.

Which strategy fits your situation: a practical investor profile guide

The Bogleheads community consensus holds that lump-sum is mathematically optimal unless volatility triggers panic selling that causes the investor to abandon their strategy entirely.

That principle frames the matching function below. The right strategy is not determined by what the market is doing. It is determined by what the investor will actually execute.

| Investor Profile | Recommended Strategy | Rationale |

|---|---|---|

| Long horizon (10+ years), high risk tolerance, large lump sum available | Lump-sum | Markets trend upward in ~70-75% of 12-month periods; delayed entry costs expected return |

| Risk-averse, near retirement, emotionally sensitive to drawdowns | DCA | Behavioural protection outweighs expected return cost; capital preservation priority |

| Regular payroll investor (401(k), superannuation, pension) | DCA (structural default) | DCA is already embedded in the contribution structure; no switch needed |

| Investing in cryptocurrency or highly volatile assets | DCA | Extreme price volatility makes single-entry timing risk disproportionately high |

| Windfall or inheritance recipient, uncertain about near-term direction | Partial lump-sum + DCA hybrid | Deploy a portion immediately, DCA the remainder over 6-12 months to balance both risks |

For regular payroll investors, the verdict deserves particular emphasis. Automatic contributions to a 401(k), superannuation fund, or pension scheme already constitute a DCA strategy by structure. Understanding that this approach is appropriate, not suboptimal, should reduce unnecessary second-guessing.

Getting DCA into practice: tools, automation, and how to start

Automation is the operational mechanism that makes DCA’s behavioural benefits real. Manual execution reintroduces the emotion and inconsistency the strategy is designed to eliminate.

The behavioural benefit of DCA depends entirely on removing discretion from the process: automated DCA implementation through platforms like Interactive Brokers and Betashares Direct enforces the schedule at the moment of maximum emotional pressure, which is precisely when manual investors are most likely to pause, delay, or abandon the commitment.

For equity and fund investors:

- Vanguard auto-invest schedules regular automatic investments into funds

- Fidelity and Schwab offer automatic investment scheduling for equities and managed funds

- Payroll-linked plans (401(k), superannuation, pension contributions) represent the most widely used automated DCA by structure

For cryptocurrency investors:

- Gainium, 3Commas, and Cryptohopper rank among the leading purpose-built crypto DCA automation platforms

- OctoBot provides open-source DCA bot capabilities

- Pionex offers exchange-integrated DCA bot functionality

- Binance Futures DCA Bot handles DCA strategies within futures trading

Emerging platforms such as MoneyFlare and broader AI-assisted tools are integrating DCA scheduling with dynamic rebalancing features, though these remain in earlier adoption stages.

Setting up your DCA schedule

Three decisions define every DCA implementation:

- Contribution amount. Determine the fixed sum per interval. This should reflect disposable income or the total investable amount divided across the chosen deployment window.

- Schedule frequency. Choose weekly, fortnightly, or monthly intervals. Research suggests the specific frequency matters less than the consistency of execution; the behavioural benefit comes from commitment to the schedule.

- Target asset or fund. Select the investment vehicle, whether a broad index fund, sector-specific ETF, individual equity, or cryptocurrency. The asset choice determines the volatility profile the DCA strategy must absorb.

Consistency matters more than optimisation. An investor who automates $500 monthly into a diversified index fund and holds for a decade will almost certainly outperform one who spends months calibrating the perfect interval and never begins.

The strategy debate settles on one principle: match the method to the investor, not the market

Lump-sum investing wins on average in historical data. That finding is consistent across every rigorous study published to date. DCA wins for the investor who needs behavioural structure to stay invested through volatility, and the research shows that investor describes a significant majority of the market’s participants.

The right strategy is the one a reader will actually execute consistently over the full intended horizon. In the 2025-2026 environment of elevated volatility, rate uncertainty, and geopolitical disruption, DCA’s practical appeal is well-founded, even for investors who understand the mathematical tradeoff.

What matters is not which strategy looks better in a backtest. What matters is which one keeps capital in the market long enough for compounding to do its work.

For investors wanting to move beyond the DCA versus lump-sum decision and structure a complete portfolio around systematic discipline, our dedicated guide to portfolio construction in volatile markets covers a three-layer framework using cash, income bonds, and diversified equities, with worked examples drawn from the March 2026 ASX selloff where ETF inflows reached $5.6 billion even as the index fell 7.8%.

This article is for informational purposes only and should not be considered financial advice. Past performance does not guarantee future results. Investors should conduct their own research and consult with a qualified financial adviser before making investment decisions.