3 ASX Blue Chips Built for Long-Term Compounding

14 hrs ago

As of April 2026, Australian consumer prices have accelerated to 4.6%, forcing individuals to confront the reality that cash left idle actively loses value. The current economic environment demands a strategic approach to inflation investing, where understanding price escalation becomes a practical requirement for capital preservation.

Geopolitical shocks are currently disrupting global supply chains, pushing domestic energy and housing costs higher across the nation. In response, the Reserve Bank of Australia (RBA) has maintained a restrictive cash rate of 4.10% to deliberately slow economic activity.

These stringent monetary conditions mean that traditional savings accounts struggle to keep pace with the rising cost of living. This guide explains central bank policy mechanics and provides clear methods for positioning portfolios defensively in a high-yield environment. Evaluating these macroeconomic shifts allows investors to protect their wealth from compounding erosion before structural damage occurs to their purchasing power.

According to standard economic models, advanced nations generally target an annual price expansion of approximately 2%. This baseline growth stimulates healthy economic activity, encouraging immediate capital deployment rather than the hoarding of cash reserves. Uncontrolled escalation beyond this target severely punishes uninvested capital, silently reducing what money can buy year after year.

The official RBA monetary policy framework establishes a flexible target between two and three percent, operating on the principle that maintaining steady consumer expectations over the medium term provides the strongest foundation for full employment.

There are distinct fundamental drivers of rising costs that dictate how economic conditions evolve. Demand-pull scenarios occur during strong economic periods when consumer purchasing power drastically exceeds the availability of goods. Conversely, raw material expenses rise due to supply chain failures, creating cost-push pressure regardless of baseline consumer demand.

A third variable involves currency depreciation, which makes imported goods more expensive overnight. This transfers offshore pricing issues directly to domestic consumers and further complicates central bank responses.

Demand imbalances stem from high employment and aggressive consumer spending. Cost-push pressures arise from raw material shortages and logistical disruptions. * Currency depreciation inflates the price of imported merchandise and offshore services.

Cost-push scenarios present specific challenges for economic authorities attempting to stabilise pricing. Historical context shows the petroleum crisis of the 1970s and the 2022 Eastern European conflict as prime examples of supply-driven spikes. These supply shocks cause cyclical dangers, particularly wage-price spirals across broad sectors of the economy.

In a wage-price spiral, preemptive employee compensation requests force commercial enterprises to continually elevate consumer pricing. This creates a self-fulfilling loop that permanently alters the cost basis of basic goods.

Economic Output Impact The International Monetary Fund notes that economic output faces a reduction in real Gross Domestic Product growth for each percentage point that price escalation exceeds the threshold.

Understanding the difference between demand and supply-driven escalation helps investors anticipate the duration of elevated costs. Readers must grasp exactly how their wealth degrades over time before they can effectively evaluate protective financial instruments.

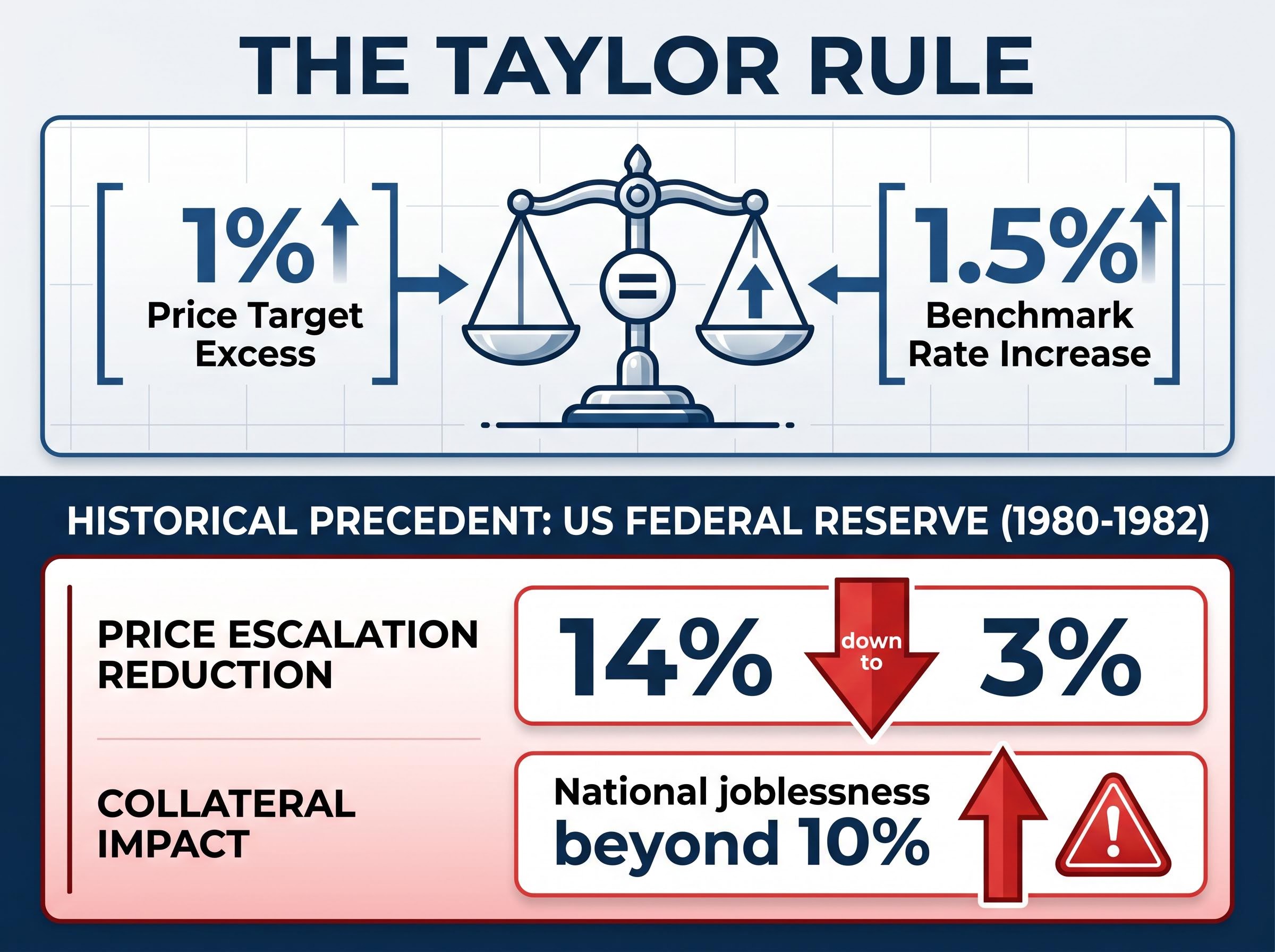

Institutions like the RBA manipulate benchmark lending costs to either restrict consumer spending or stimulate borrowing activity. This manipulation forms the core of modern monetary policy, acting as the primary lever for cooling overheated markets. The mathematical framework guiding many of these monetary interventions is known as the Taylor Rule.

According to standard economic models, the Taylor Rule dictates that monetary authorities must elevate lending benchmarks by roughly 1.5% for each 1% that prices exceed desired targets. This formula removes emotion from the process, forcing central banks to inflict necessary collateral damage through aggressive monetary tightening.

Authorities are often willing to induce recessions and joblessness to anchor public expectations. Preventing a secondary wave of widespread cost increases takes precedence over short-term corporate profitability.

The sequential steps of how raising benchmark rates cascades through the economy include:

Historical data highlights the stark contrast between modern gradual approaches and past aggressive tightening. According to historical data, between 1980 and 1982, the US Federal Reserve successfully reduced price escalation from 14% to 3% to break a severe inflationary cycle.

However, according to historical data, this aggressive action pushed national joblessness beyond 10%, demonstrating the severe economic cost of regaining price stability. Modern central banks attempt to avoid this level of unemployment by broadcasting their rate intentions months in advance.

By understanding the historical precedent and mathematical formulas guiding central banks, investors can stop guessing about upcoming rate cuts. Instead, they can objectively analyse the same employment and pricing data that drives institutional policy decisions. Maintaining anchored public expectations remains the absolute primary objective for any monetary authority. If the public believes prices will continue to rise, consumer behaviour shifts to accelerate purchases, effectively creating the exact economic conditions central banks are trying to prevent.

For readers wanting to master the fundamental concepts of monetary depreciation, our comprehensive walkthrough of how inflation erodes wealth explains the exact mechanisms central banks use to manipulate demand and how everyday assets respond to broad price increases.

The current Australian macroeconomic environment features acute consumer price spikes and subsequent RBA interventions that demand immediate investor attention. The Australian Consumer Price Index rose to 4.6% annually in March 2026, heavily driven by a 6.5% surge in domestic housing costs. This acceleration reverses months of gradual cooling, signaling that restrictive policies must remain in place longer than initially projected.

In response to this sustained pressure, the RBA raised the cash rate to 4.10% on 17 March 2026. Official monetary forecasts now expect headline inflation to hit 4.2% by mid-2026 before any meaningful relief occurs.

This upward pressure stems significantly from the 2026 Iran conflict, which continues to disrupt global oil supplies. The blockade of the Strait of Hormuz has created an energy shock that directly elevates domestic electricity and diesel expenses across Australia.

This disruption to vital shipping lanes illustrates how temporary energy shock impacts can swiftly bypass domestic policy, forcing local markets to price in an extended period of elevated borrowing costs.

| Month | CPI Rate | RBA Cash Rate Action | Primary Driver |

|---|---|---|---|

| January 2026 | Services and Utilities | ||

| February 2026 | 3.7% | Raised to 3.85% | Housing and Rents |

| March 2026 | 4.6% | Raised to 4.10% | Energy Shocks and Housing |

Institutional Consensus Australia’s Big Four banks unanimously supported the RBA rate hike to 4.10%, citing escalating global economic pressures and domestic capacity constraints.

While geopolitical conflicts elevate costs, emerging deflationary forces are acting as potential economic counterweights in the background. The Australian artificial intelligence market is projected to exceed $80 billion by 2033, driving massive workflow efficiencies. AI automation is actively reducing operational overhead for Australian businesses, a technological shift that may eventually lower end-consumer merchandise prices.

Forward-looking commodity indicators also provide context on when supply constraints might ease. Petroleum futures are currently exhibiting backwardation, a market condition where near-term contracts trade at premiums to longer-dated deliveries. This curve signals that traders expect immediate resource scarcity to resolve naturally over time.

Furthermore, diverted Chinese exports offer another potential deflationary force for the Asia-Pacific region. However, the RBA continues to attribute domestic inflation primarily to internal capacity constraints rather than shifting global merchandise flows.

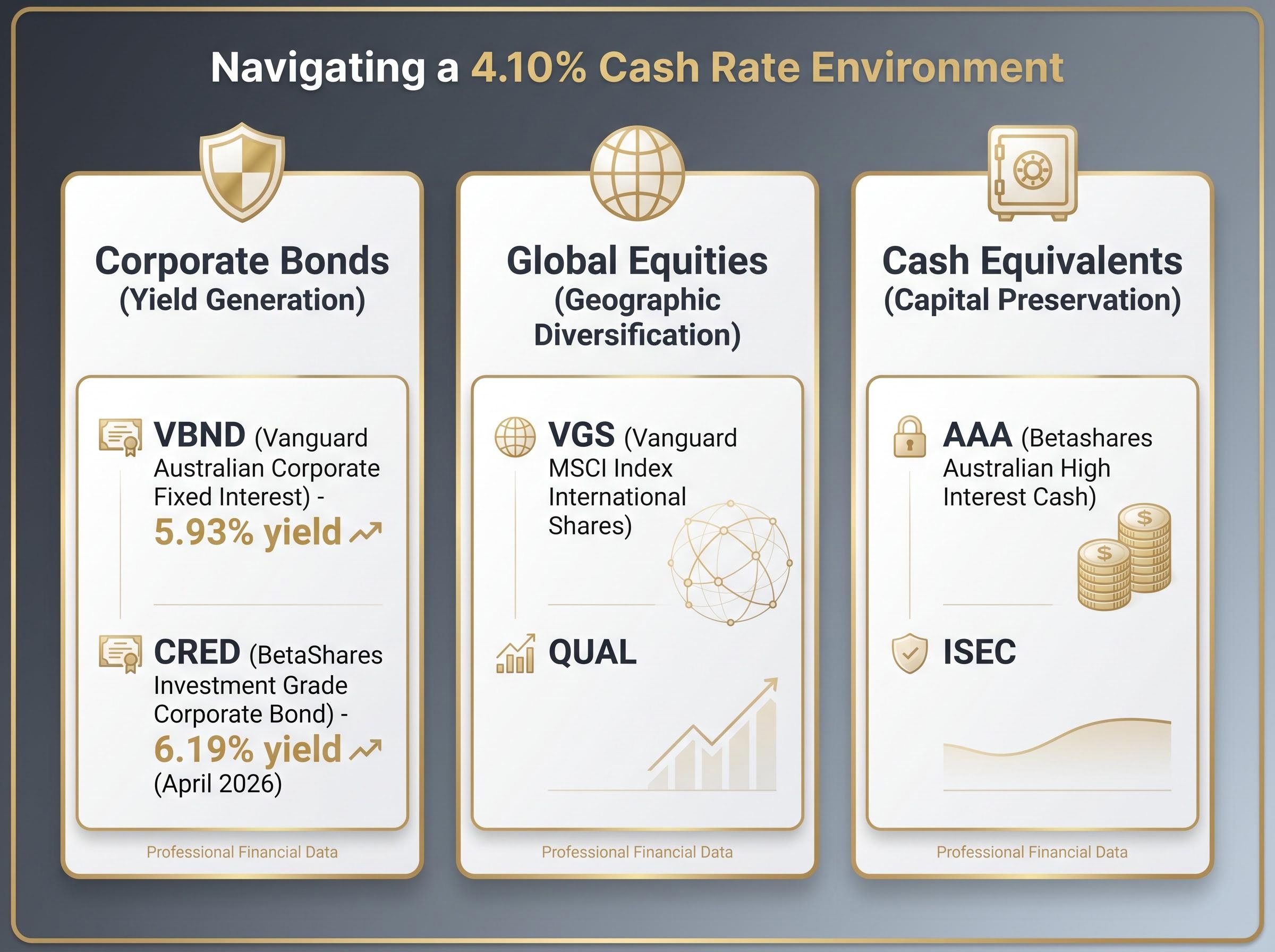

The institutional consensus on defensive portfolio positioning emphasises moving capital away from highly leveraged, rate-sensitive assets. With sticky 2026 pricing pressures dictating market conditions, capital allocators are directing funds toward specific Exchange Traded Funds offering compelling revenue generation. High-yield cash equivalents also play a valuable role in maintaining portfolio liquidity while safely capturing elevated interest rates.

Leading financial institutions advise careful consideration of asset allocation in a 4.10% cash rate environment. Major strategic shifts recommended by financial institutions include:

Janus Henderson favours inflation-protected assets to preserve purchasing power amid tight supply chains and geopolitical risks. BNP Paribas advises deploying balanced portfolios to navigate geopolitical uncertainty and manage diversified downside risk. * Macquarie suggests focusing on assets with strong economic momentum that can successfully weather current inflation dynamics.

These recommendations highlight a broader shift away from aggressive growth equities toward defensive, income-generating vehicles.

The published Macquarie Bank macroeconomic outlook reinforces this institutional pivot, noting that portfolios must actively rotate toward high-yield corporate credit to survive structurally higher borrowing costs.

| Ticker | Fund Name | Asset Class | 2026 Strategy Fit |

|---|---|---|---|

| VBND | Vanguard Australian Corporate Fixed Interest | Corporate Bonds | Yield Generation |

| CRED | BetaShares Investment Grade Corporate Bond | Corporate Bonds | Yield Generation |

| VGS | Vanguard MSCI Index International Shares | Global Equities | Geographic Diversification |

| AAA | Betashares Australian High Interest Cash | Cash Equivalent | Capital Preservation |

Corporate bond funds provide a direct mechanism for capturing current institutional yields. The Vanguard Australian Corporate Fixed Interest Index ETF (ASX: VBND) currently offers an annual distribution yield of 5.93%. Similarly, the BetaShares Australian Investment Grade Corporate Bond ETF (ASX: CRED) reported a yield to worst standing at 6.19% per annum as of April 2026.

There is an established inverse relationship between underlying security valuations and elevated fixed-income yields. When central banks hold rates high, newly issued bonds offer superior payouts, making them highly attractive defensive instruments.

Broad geographic distribution through international equity funds captures regional economic recoveries to offset domestic weaknesses. Instruments like VGS and QUAL provide exposure to global markets that may not be experiencing the exact same capacity constraints as Australia. Alongside domestic cash equivalents like AAA and ISEC, these instruments offer evaluateable options for protecting wealth from ongoing monetary friction.

Transitioning from a passive observer of purchasing power erosion to an active portfolio manager requires definitive, strategic action. While monetary authorities may eventually prioritise growth support within a 6-12 month horizon, immediate defensive positioning remains a pressing requirement.

Investors face a mathematical reality where avoiding market participation guarantees systematic wealth degradation. Reviewing current asset allocations against the realities of a 4.10% cash rate environment allows individuals to construct proper financial defences.

Allocating capital toward high-yield corporate debt, geographically diverse equities, and inflation-protected assets directly counteracts the erosion of living standards. The current economic cycle severely penalises hesitation, making proactive portfolio realignment the most effective response to sticky consumer pricing.

Executing a resilient asset allocation strategy requires investors to systemically capture these international equity discounts while securing high domestic yields, ultimately bridging the gap between current geopolitical volatility and future market stabilisation.

Past performance does not guarantee future results. Financial projections regarding macroeconomic trends and central bank policies are subject to market conditions and various risk factors. This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Inflation investing involves strategically allocating capital to assets designed to preserve or grow purchasing power during periods of rising prices, which is crucial in Australia due to accelerated consumer prices and a restrictive RBA cash rate.

Investors can protect portfolios by allocating to high-yield corporate bonds, diversifying globally with international equity funds, and utilising high-interest cash equivalents to capture elevated rates and maintain liquidity.

The RBA's current cash rate is 4.10%, a restrictive level designed to slow economic activity and curb consumer spending, which ultimately helps to reduce inflation.

The Taylor Rule is a mathematical framework suggesting central banks should raise lending benchmarks by 1.5% for each 1% that prices exceed desired targets, guiding monetary authorities to aggressively tighten policy when inflation is high.

Recommended ETFs include VBND for Australian corporate fixed interest, CRED for investment-grade corporate bonds, VGS for global equities diversification, and AAA for high-interest cash equivalents.