A $15 trillion corporate refinancing wall stands between 2026 and 2028, casting a shadow over the entire domestic corporate debt ecosystem. This impending maturity schedule coincides with distress ratios hitting a three-year high in March 2026. The United States credit environment is demonstrating marked deterioration this month, forcing institutional capital to search aggressively for alternative yields.

Investors navigating the leveraged finance market are witnessing a profound structural shift as traditional fixed-income strategies shed value. Surging default rates are driving credit funds away from standard broadly syndicated loans and pushing them toward highly speculative artificial intelligence ventures. This rotation represents a fundamental change in institutional risk appetite. Asset managers are attempting to engineer their way out of a mounting debt crisis by underwriting the exact technologies expected to disrupt the broader economy.

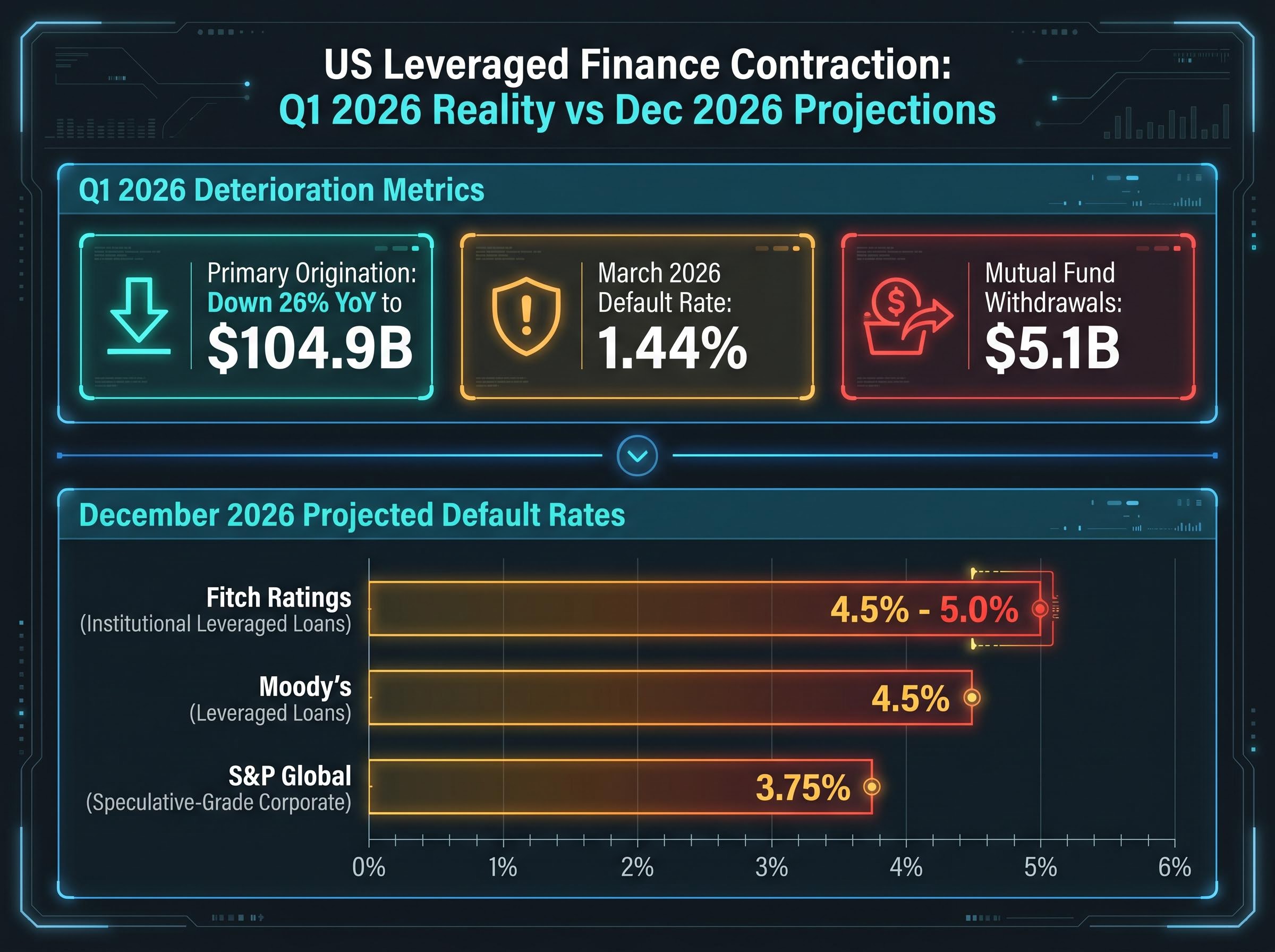

The Q1 2026 Contraction of the US Leveraged Finance Market

The quantitative reality of the current credit deterioration exposes a widening gap between stable macroeconomic sentiment and the acute distress felt by low-rated debt issuers. Actual defaults accelerated through the close of the first quarter. The domestic leveraged loan default rate rose to 1.44% by amount in March 2026, confirming a sustained upward trajectory.

According to Fitch Ratings, the trailing twelve-month default rate for leveraged loans reached 4.9% by the end of the quarter. This statistical deterioration is compounding at the systemic level, with the distress ratio for loans trading under 80% of face value climbing sharply. Traditional fixed-income investments are currently shedding value under the weight of these defaults, forcing institutional panic across previously stable portfolios.

The recent Fitch Ratings default monitor report provides empirical evidence of this systemic deterioration, highlighting how the volume of distressed corporate debt continues to expand ahead of the looming maturity wall.

Primary origination volumes have contracted severely due to sluggish merger and refinancing activity. According to industry data, first-quarter primary loan origination volumes fell 26% year-over-year to $104.9 billion. This contraction signals that traditional borrowers are unwilling or unable to accept current underwriting terms.

| Rating Agency | Asset Class | Projected Default Rate | Target Date |

|---|---|---|---|

| Moody’s | US Speculative-Grade Bonds | 3.5% | December 2026 |

| Moody’s | Leveraged Loans | 4.5% | December 2026 |

| Fitch Ratings | Institutional Leveraged Loans | 4.5% – 5.0% | December 2026 |

| S&P Global | Speculative-Grade Corporate | 3.75% | December 2026 |

Deteriorating Index Valuations

Secondary market pricing dispersion provides the clearest signal of this institutional retreat. The Morningstar LSTA US Leveraged Loan 100 Index stood at 97.27 in late April 2026, reflecting persistent valuation pullbacks across prime assets. According to industry data, capital withdrawals reached $5.1 billion as mutual funds systematically retreated from the asset class entirely.

When big ASX news breaks, our subscribers know first

Educational Foundation: How Refinancing Walls and Hidden Leverage Compound Distress

Note: This section simplifies complex financial mechanisms for readability and informational purposes.

A refinancing wall occurs when a massive volume of corporate debt reaches maturity at the same time, forcing companies to secure new loans to pay off the old ones. The estimated $15 trillion refinancing wall looming over the next two years poses an existential threat to heavily indebted corporations. These companies originated their loans during periods of near-zero borrowing costs and must now refinance under significantly harsher economic conditions.

The Federal Reserve maintained an effective Federal Funds rate of 3.64% and a target range of 3.5% to 3.75% as of April 2026. This tight monetary posture directly restricts the ability of middle-market companies to service complex debt obligations. Moody’s has repeatedly warned that hidden leverage mechanisms are severely amplifying these downturn risks by masking the true financial strain on low-rated issuers.

Parallel Federal Reserve Bank of Boston research corroborates these regulatory concerns, warning that the extensive overlapping credit lines between traditional banks and private alternative lenders create obscured channels of systemic risk.

Three distinct types of hidden leverage are currently weakening loan covenants across the sector:

Payment in Kind (PIK) Mechanisms: These structures allow borrowing companies to pay their interest obligations using additional debt rather than cash. This preserves immediate liquidity but compounds the total principal owed upon maturity. Net Asset Value (NAV) Lending: Investment funds borrow money against the theoretical value of their entire portfolio rather than individual cash-generating assets. This creates overlapping layers of debt that can collapse simultaneously if portfolio valuations drop. * EBITDA Add-Backs: Accounting provisions that permit companies to calculate their earnings based on projected future savings rather than actual current cash flow. This artificially inflates the borrower’s apparent ability to repay the loan.

By understanding these mechanisms, investors can see exactly why prolonged elevated interest rates trigger sudden institutional defaults. Companies employing these tools often appear financially stable on paper until the exact moment they face their refinancing obligations.

The Institutional Pivot Toward Hybrid Artificial Intelligence Debt

Institutional momentum is shifting from defensive portfolio preservation to offensive capital deployment. Asset managers are actively swapping traditional broadly syndicated loans for complex hybrid technology debt to offset legacy portfolio depreciation. Late-stage venture debt for artificial intelligence startups hit a decade high in the first quarter of 2026, confirming this structural migration of capital.

Credit funds are executing these allocations through hybrid capital solutions rather than standard lending agreements. The median artificial intelligence deal size currently sits at $10.8 million, with average deals scaling rapidly to $68.2 million. This aggressive funding of artificial intelligence infrastructure contrasts sharply against the tightening underwriting standards currently restricting traditional software and healthcare services.

The ongoing AI disruption in tech has fundamentally altered enterprise value models, forcing capital to abandon headcount-dependent software platforms in favor of highly efficient synthetic infrastructure.

FTI Consulting Survey Insight “Over 75% of market respondents expect loan workouts and defaults to increase in 2026 compared to the previous year, driving the immediate institutional necessity for alternative yield generation.”

Institutional managers are effectively attempting to underwrite their way out of a deteriorating credit environment. The capital supporting these technology ventures is sourced directly from the liquidity pulled out of traditional middle-market lending.

The Rise of Hybrid Capital Solutions

Funds focused on technology infrastructure are structuring deals that actively blend private credit with equity warrants. This hybrid approach provides credit funds with standard interest payments while granting them the right to purchase company shares at a set price in the future. Managers rely on these equity upside mechanisms to offset the massive depreciation occurring within their legacy syndicated loan portfolios.

Case Study: Oxford Square Capital’s Q1 Portfolio Reallocation

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Severe asset depreciation forces immediate operational pivots in real time, a dynamic clearly illustrated by Oxford Square Capital during the recent reporting period. The Business Development Company reported a highly disappointing first quarter, demonstrating how surging investment deficits within legacy portfolios destroy capital. The market severely punished the firm following the release of these metrics.

Management made an explicit executive decision to deploy fresh capital into specific cutting-edge technology enterprises despite severe quarterly losses across their broader portfolio. The company directed new capital deployments primarily into undisclosed ventures, seeking aggressive alternative yields. The financial community reacted immediately to the structural weakness in the underlying legacy assets.

The severity of the capital destruction was evident across multiple core financial metrics:

First-quarter earnings missed expectations. Per-share net asset value plummeted. Combined realised and paper portfolio losses expanded. Pre-market trading pushed shares down immediately following the earnings release.

This failure provides a tangible blueprint of how specific Business Development Companies manage legacy credit deterioration. By issuing new equity and chasing technology yields while their core assets depreciate, these entities prove the broader macroeconomic thesis that traditional lending models are currently fracturing.

For readers wanting a complete breakdown of this specific asset deterioration, our deep-dive into the Oxford Square Capital earnings explores the sustainability of its dividend yield and the exact scope of its realized portfolio deficits.

Trading One Systemic Threat for Another: The AI Rotation Risk

These statements contain speculation regarding emerging market trends and are subject to change based on macroeconomic developments.

The institutional pivot toward technology debt creates a profound tension between two distinct vulnerabilities. Markets must now balance the known danger of macroeconomic default against the speculative threat of an artificial intelligence investment bubble. Rating agencies are issuing rising warnings regarding the fragility of this new tech-heavy credit rotation, categorising the shift as a dangerous escalation of risk profiles rather than a cure for the credit crisis.

According to survey data from FTI Consulting, 21% of respondents view an “AI investment crash” as the most underestimated market risk in 2026. Moody’s formally categorised emerging artificial intelligence-related credit concerns as significant long-term vulnerabilities that keep overall market sentiment fragile. The structural vulnerability of hybrid financing is already producing visible casualties across the broader alternative lending space.

Recent high-profile bankruptcies serve as cautionary tales for funds relying on complex structured debt. The Tricolor Holdings Chapter 7 filing in late 2025 and the First Brands Chapter 11 plan initiated in April 2026 demonstrate how quickly hybrid financing structures can unravel during operational stress. Consequently, only 21% of market participants report strong confidence in current market oversight.

The top three emerging risks in the 2026 credit market highlight this evolving threat matrix:

- Persistent macroeconomic default pressure driven by the upcoming corporate refinancing wall.

- The structural weakness and high failure rate of complex hybrid capital solutions.

- The compounding threat of an artificial intelligence investment bubble collapsing under unmet commercialisation targets.

Deploying capital into speculative tech debt to offset legacy losses could trigger an entirely new class of institutional defaults if these infrastructure investments fail to commercialise.

Navigating the Convergence of Distressed Debt and Technological Speculation

The traditional credit market is permanently fracturing under the combined weight of sustained interest rates and massive maturity walls. Asset managers are no longer operating in an environment where standard syndicated loans provide safe, reliable yield. The institutional pivot toward artificial intelligence ventures is an act of necessity driven by severe portfolio depreciation rather than pure technological innovation.

Whether hybrid technology debt will save legacy portfolios or simply accelerate their collapse by the end of the year remains the central question for the domestic financial sector. Institutional capital is currently trading the certainty of macroeconomic distress for the volatility of early-stage venture financing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.