Two months into an escalating Middle Eastern conflict, global energy markets are signalling severe distress. Crude oil has broken past $100 a barrel, yet a striking paradox defines US equity markets in April 2026. Almost half of retail market participants believe stock prices will continue to rise, demonstrating a level of investor sentiment that appears completely detached from physical market realities.

This optimism collides directly with global supply chain fractures and surging domestic energy costs. Record equity valuations are currently resting on a fragile foundation of depleted household savings and severely strained logistical networks. While algorithms maintain their upward momentum, the physical economy is absorbing a massive inflationary shock, leaving the industrial sector to face compounding margin pressures.

The following analysis examines the psychological drivers behind this market resilience. It outlines why current equity positioning diverges so sharply from institutional risk modelling, identifying the hidden macroeconomic vulnerabilities that could force a sudden correction. By evaluating the gap between retail exuberance and infrastructural strain, market participants can better understand the catalysts poised to test this extended rally.

The Optimism Paradox: Dissecting the Spring 2026 Rally

The gap between surging retail optimism and institutional risk modelling has widened to historic extremes. According to data from the American Association of Individual Investors (AAII) for the week ending April 22, 2026, bullish expectations spiked to 46.0%. This represents a dramatic increase from pre-conflict levels and sits well above the historical long-term average of 37.5%.

In direct contrast to this retail exuberance, prominent institutional strategists are issuing severe warnings about the underlying health of the economy. Marc Chaikin of Chaikin Analytics projects potential equity losses of 20%, noting a fundamental deterioration in market breadth that began materialising in March 2026. Similarly, Mark Newton at Fundstrat predicts a 15% to 20% correction for US stocks, while Citadel founder Ken Griffin forecasts an impending economic recession.

| Source | Current Stance | Market Projection |

|---|---|---|

| AAII Retail Survey | Highly Bullish | Continued upward trend (46.0% expecting gains) |

| Marc Chaikin (Chaikin Analytics) | Bearish | 20% equity losses materialising from March 2026 |

| Mark Newton (Fundstrat) | Bearish | 15% to 20% US stock correction |

Historical data frequently positions this elevated level of retail enthusiasm as a standard contrarian indicator. When crowd psychology diverges this sharply from institutional risk management, it often precedes significant equity corrections. Retail buyers tend to aggressively purchase equities at the exact moment institutional capital begins to distribute its holdings.

Institutional Disconnect “Retail participants are pricing in a perfect soft landing, entirely disregarding the geopolitical risk premium that institutional models are currently flashing.”

This divergence provides a critical lens for evaluating portfolio confidence. Institutional capital is quietly preparing for a contraction, while retail capital continues to fund an increasingly fragile rally.

These institutional defensive strategies increasingly involve reducing fixed income duration risk and building larger cash allocations, indicating a structural rotation away from equities despite headline market indices pushing higher.

When big ASX news breaks, our subscribers know first

Educational Breakdown: Why Markets Fail to Price Geopolitical Risk

Financial markets frequently fail to price in geopolitical volatility until the physical damage directly impacts corporate earnings. Two months after the Iran conflict escalated in mid-February 2026, equity traders continue to ignore surging petroleum prices. This complacency is not necessarily a product of foolishness, but rather a structural limitation in how modern finance calculates risk.

Institutional trading algorithms and human portfolio managers rely on historical data, standard deviation metrics, and predictable cash flows to value assets. Wartime volatility lacks these clear mathematical frameworks. When faced with unpredictable regional conflicts, market participants often disregard the complications entirely until a direct financial impact is proven on a corporate balance sheet.

Craig Johnson, Chief Market Technician at Piper Sandler, notes that extended equity projections frequently blind participants to immediate threats. When existing models cannot quantify the probability of a geopolitical shock, the default institutional response is simply to maintain the current market direction. Algorithms are programmed to follow the trend until mathematical support levels are definitively broken.

The underlying low-latency infrastructure powering these algorithmic trades prioritises immediate execution over qualitative risk assessment; consequently, automated systems continue buying into momentum until physical supply chain disruptions finally force a quantitative recalibration.

The Psychology of Unquantifiable Threats

This behavioural finance dynamic creates a delayed reaction mechanism across major indices. Traders default to existing bullish trends when confronted with data they cannot mathematically model. The inability to price abstract risk leads to dangerous algorithmic blind spots, leaving equities highly exposed to sudden shifts in physical realities.

Traditional valuation models fundamentally struggle to process binary variables that lack historical precedent. These unquantifiable threats typically include:

Sudden maritime blockades that halt regional shipping traffic instantly. Spontaneous conflict escalations involving previously neutral state actors. Targeted destruction of energy infrastructure that permanently removes supply. Rapid political embargoes that bypass standard diplomatic timelines.

Understanding these modelling limitations ensures investors do not mistake temporary market silence for long-term safety. The absence of a price drop merely reflects the absence of a mathematical framework for pricing the current crisis.

The Consumer Reality Check: Inflation at the Pump vs Retail Resilience

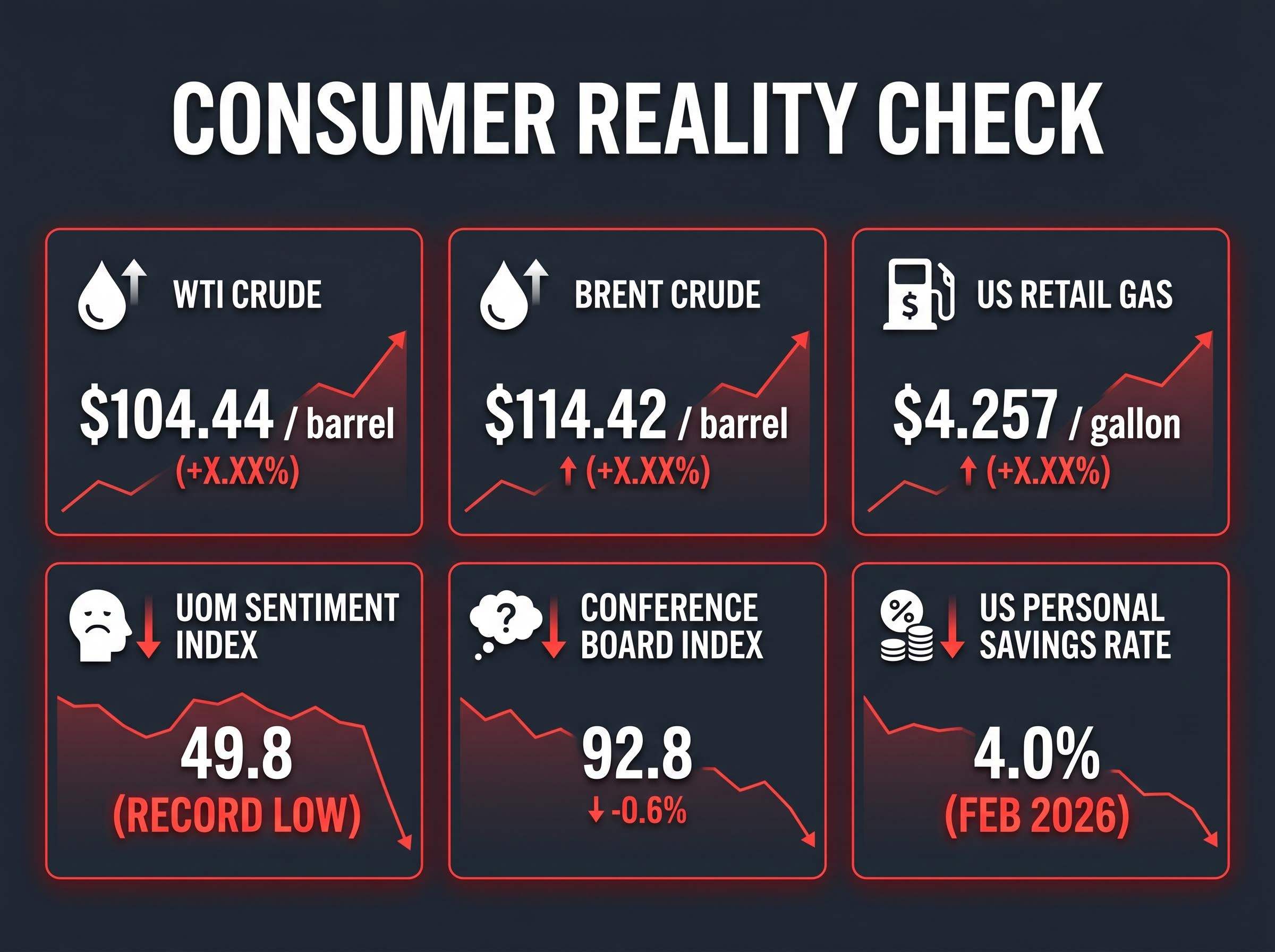

The mathematical blind spots of Wall Street stand in stark contrast to the physical reality of the US consumer. Domestic energy costs have surged dramatically over the past eight weeks. West Texas Intermediate (WTI) crude is trading at approximately $104.44 per barrel, while Brent crude has reached $114.42. Consequently, the US national average for retail gasoline has climbed to $4.257 per gallon.

This severe energy inflation is creating a fractured, bifurcated economy. Wealthier demographics continue to drive overall expenditure growth, masking the acute financial distress of lower-income brackets crushed by fuel costs. According to Bank of America metrics, aggregate consumer outlays are currently accelerating, creating a misleading aggregate picture of economic health.

However, consumer sentiment metrics reveal a vastly different underlying truth. The University of Michigan consumer sentiment index has plummeted to a record low of 49.8, driven heavily by compounding energy and food inflation. In stark contrast, the Conference Board index, which often reflects higher-income sentiment, registered a surprisingly resilient 92.8.

Economic Reality Check “Consumers are maintaining their nominal spending habits while failing to recognise that their actual purchasing capacity has severely diminished.”

The Savings Depletion Trap

The current acceleration in aggregate consumer spending is fundamentally unsustainable. Shoppers are actively diminishing their personal financial reserves to sustain accustomed consumption levels despite rising prices. The US personal savings rate dropped to 4.0% in February 2026, confirming an ongoing, dangerous depletion of post-pandemic cash reserves.

The official BEA savings metrics confirm this rapid downward trajectory, highlighting how quickly households are burning through their remaining liquidity to manage escalating daily living costs.

Once these reserves hit absolute zero, the downstream risks to non-fuel retail categories will multiply rapidly. Consumers will be forced to make difficult trade-offs, slashing discretionary purchases to cover basic utility and transport costs. This energy inflation is silently eroding the foundational driver of the US economy, threatening corporate earnings across the entire consumer discretionary sector.

Strait of Hormuz Vulnerabilities and Global Supply Chains

The most immediate infrastructural risk to this fragile economic equilibrium lies in the Strait of Hormuz. Middle Eastern hostilities are forcing a fundamental rethinking of long-term supply chains, directly contradicting claims from some top strategists that markets have moved past peak fear. Volatility in this specific maritime corridor threatens to rapidly disrupt 20% to 40% of the global nitrogen and liquefied natural gas (LNG) trade.

Recent EIA reporting on LNG prices confirms that closures in this critical maritime corridor immediately threaten a substantial portion of global energy distribution, leaving major import markets scrambling for viable alternatives.

A potential blockade scenario is already creating logistical bottlenecks that impact domestic infrastructure. US Gulf Coast ports are experiencing substantial surges in activity as domestic energy producers attempt to bridge massive global supply gaps. This rapid pivot stretches local shipping capacity and significantly increases operational costs for domestic industrial firms.

This geographic vulnerability serves as the exact trigger that could force the stock market to finally price in geopolitical reality. The cascading effects of a supply chain disruption follow a highly predictable sequence:

- A localised maritime blockade traps transport vessels in the Persian Gulf.

- Global markets experience an immediate shortage of LNG and agricultural fertilisers.

- US energy producers divert domestic supply to international allies at premium rates.

- Domestic utility and agricultural production costs spike simultaneously.

- Corporate profit margins compress, forcing a rapid equity market repricing.

Monitoring these physical logistical fracture points provides investors with clear indicators of when the current optimism will dissipate.

The Breaking Point: Catalysts That Will Force a Market Repricing

The market resilience observed in April 2026 is built on a precarious foundation of depleted consumer savings and unpriced geopolitical risk. Retail exuberance continues to push equity valuations higher, but the physical constraints of global energy supply and domestic purchasing power are tightening rapidly. Wall Street is currently treating a structural supply shock as a temporary inconvenience.

Analysts warn that several specific catalysts will eventually shatter this complacency. Worsening Iranian conflict conditions, potential Strait of Hormuz blockages, and the broader macroeconomic fallout from regional instability all represent immediate threats. The longer these physical realities remain ignored by algorithmic trading models, the sharper and more severe the eventual correction is likely to be.

Investors should view the coming months with strict objectivity, monitoring the divergence between sentiment surveys and actual logistical data. Maintaining protective portfolio positioning is vital when crowd psychology aggressively ignores macroeconomic gravity.

Investors exploring how extreme energy prices will ultimately transmit into corporate earnings will find our deep-dive into US recession risk modeling useful, as it outlines specific crude oil price thresholds that significantly elevate the probability of an economic contraction.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.