Lululemon Fundamental Analysis: the Price of Brand Dilution

2 hrs ago

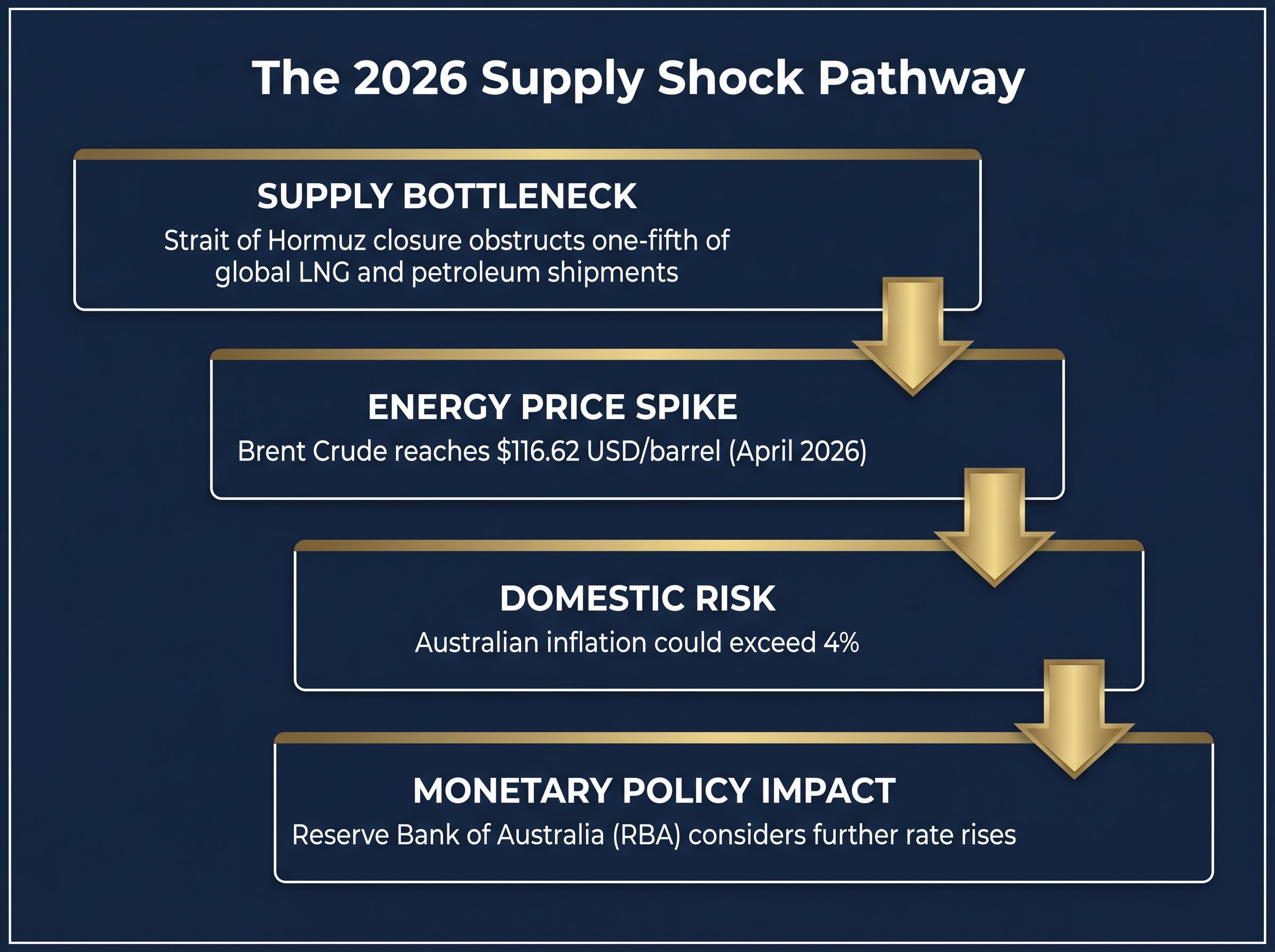

Global energy markets face their most acute bottleneck of the decade following the operational closure of the Strait of Hormuz. Brent Crude oil surged past $116 USD per barrel in late April 2026, fundamentally altering how capital allocators view traditional safe haven investments.

Previous geopolitical shocks typically coincided with collapsing economic growth, prompting central banks to reduce interest rates and flood markets with liquidity. The current macroeconomic environment presents a markedly different reality.

This specific crisis represents a severe supply shock that is sustaining high inflation and actively preventing central banks from executing their planned rate reductions. Understanding the mechanics of protective assets under structurally higher interest rates is now vital for capital preservation.

This analysis unpacks how established defensive strategies are reacting to these unique crosscurrents. The framework provided will offer Australian investors a clear path for defensive portfolio positioning amidst ongoing regional volatility.

Historical assumptions dictate that a geopolitical crisis automatically triggers central bank rate cuts and surging bond valuations. The market mechanics of April 2026 directly contradict this historical assumption.

According to industry data, the operational closure of the Strait of Hormuz is currently obstructing one-fifth of global liquefied natural gas and petroleum shipments. This is a severe resource supply disruption in the Middle East, sharply contrasting with the demand-driven crises of previous decades.

Central banks find themselves hesitating to lower benchmark lending rates despite widespread economic anxiety. The inflationary pressure generated by $116.62 USD per barrel crude oil makes any monetary easing fundamentally dangerous.

This institutional reluctance reflects broader BIS research on supply headwinds, which demonstrates that structurally embedded energy inflation requires prolonged restrictive monetary policy even as underlying growth metrics deteriorate.

This dynamic presents a specific domestic risk for Australia. Australian economists warn that domestic inflation could exceed 4% if the closure persists.

This elevated inflation metric would potentially force the Reserve Bank of Australia (RBA) to consider further rate rises rather than cuts.

The Inflationary Shock Paradigm “Investors must recognise the conceptual shift from a demand-collapse crisis to a supply-disruption shock, as the latter actively prevents central banks from deploying traditional interest rate relief.”

Recognising the root cause of the current market volatility prevents investors from applying outdated crisis playbooks to a structurally different economic environment. Capital allocators anticipating a swift return to low interest rates are misreading the inflationary consequences of the energy bottleneck.

Managing this environment requires understanding what actually constitutes a protective asset during an inflationary supply shock compared to a standard recession. During a traditional growth collapse, fixed-income capital values surge as interest rates fall.

In 2026, sustained high interest rates create a significant opportunity cost for holding assets that do not pay regular dividends or coupons. Capital deployed into zero-yield instruments effectively loses purchasing power while inflation remains elevated.

This dynamic echoes the supply shocks of the 1970s and the recent inflationary spike of 2022. Currency strength acts as a secondary filter that modifies the actual return profile of global assets for local investors.

A comprehensive inflation investing strategy must also balance these immediate energy spikes against hidden disinflationary megatrends, such as rapid artificial intelligence integration, which are actively suppressing long-term operational costs.

A nominally stable international asset can still generate negative real returns for an Australian investor if the domestic currency depreciates against the asset’s underlying denomination. This foundational knowledge empowers readers to evaluate financial instruments based on their underlying mechanics rather than relying on historical reputations.

Historical comparisons to the 2022 inflation environment prove instructive here. Investors who prioritised yield and liquidity during that period successfully insulated their portfolios from the worst capital drawdowns.

Evaluating current opportunities requires applying these exact filters to every potential defensive position. Asset resilience in the current market relies on three specific factors:

Yield Generation: The ability to produce reliable income that outpaces baseline inflation metrics. Energy Independence: Insulation from the direct input costs of soaring petroleum and natural gas prices. * Capital Liquidity: The structural capacity to exit positions swiftly without incurring steep discounts.

Domestic oil production currently dictates international purchasing power, fundamentally reshaping the foreign exchange environment. This dynamic is most visible in the sharp divergence between the United States dollar and the Japanese yen.

The United States operates as a primary energy producer, while Japan remains heavily dependent on energy imports. This structural reality has eroded the yen’s historical reputation as a reliable crisis refuge.

Safe-haven flows now heavily favour the US dollar over traditional currency alternatives. The USD/JPY exchange rate is fluctuating near the 160 threshold, trading at approximately 159.17 to mark significant 20-month highs.

Meanwhile, the Australian dollar operates with distinct sensitivities as a commodity exporter currency amidst the Middle East conflict. The AUD/USD is currently trading at approximately 0.7188, experiencing downward pressure from broader geopolitical anxiety and dominant US dollar strength.

Conversely, the AUD/JPY exchange rate trades strongly at 114.56, reflecting Australia’s relative commodity advantage over an energy-dependent Japan. Foreign exchange movements directly impact the valuation of international equities in an Australian portfolio.

Currency dynamics therefore remain a vital component of total return calculations for domestic investors seeking offshore stability.

| Currency | Net Energy Status | Current Market Positioning |

|---|---|---|

| **US Dollar (USD)** | Major Producer | Primary safe haven, trading at multi-month highs |

| **Japanese Yen (JPY)** | Heavy Importer | Weakened historical crisis refuge status |

| **Australian Dollar (AUD)** | Commodity Exporter | Pressured against USD, strengthened against JPY |

Investors face a complex choice between preserving capital through physical commodities and capturing historically high guaranteed yields. Physical bullion faces notable headwinds despite its traditional status as a geopolitical hedge.

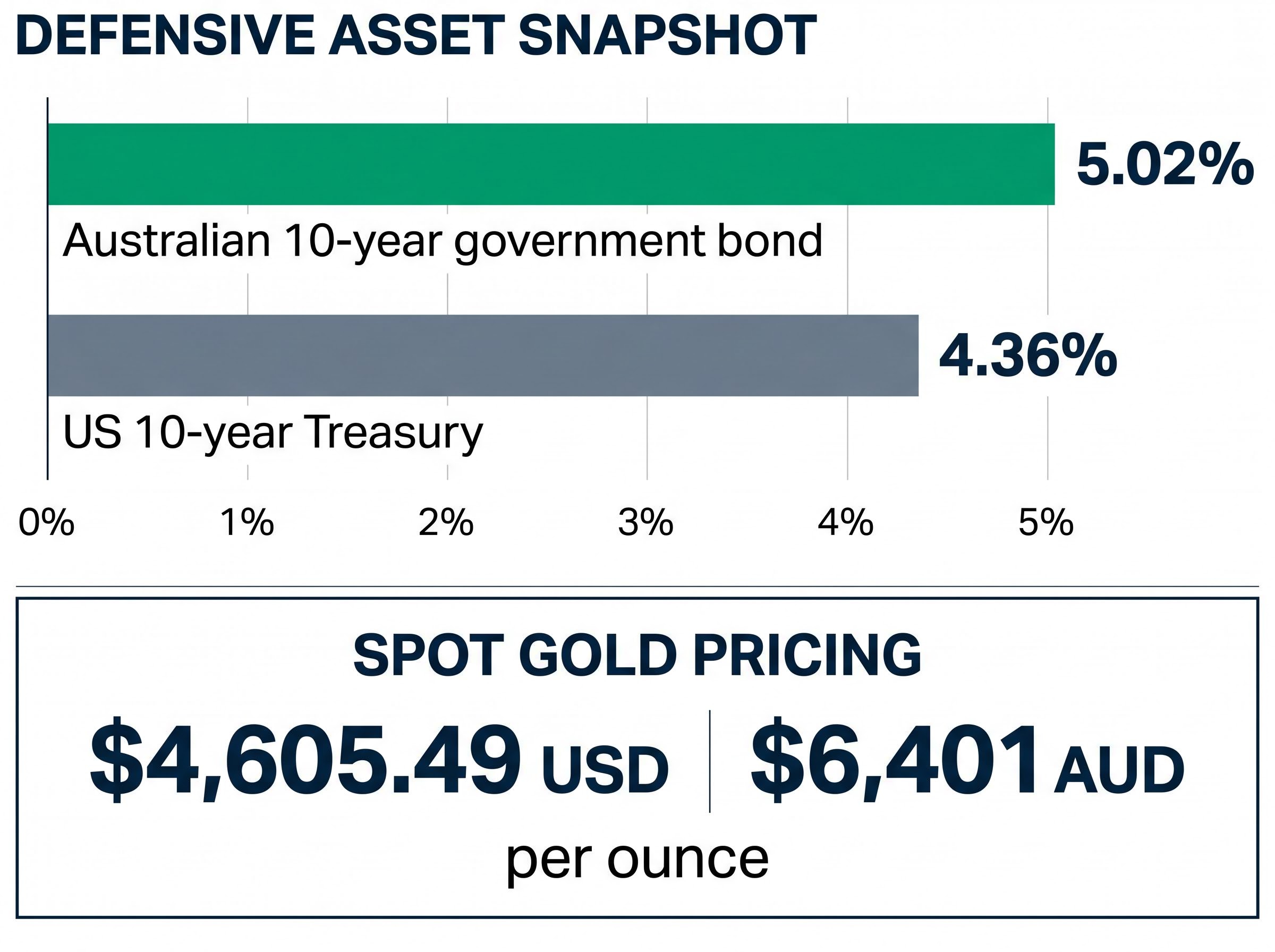

Spot gold pricing reached $4,605.49 USD and $6,401 AUD per ounce. However, strong American currency valuations make the metal increasingly expensive for foreign buyers, creating a natural drag on further upside momentum.

Simultaneously, traders anticipating prolonged inflation control are driving down the capital values of short-duration and long-duration sovereign debt.

This dynamic requires a pivot toward the stabilising power of high coupon payments acting as an anchor for total portfolio returns. Fixed-income assets offset capital value drops by delivering consistent, guaranteed cash flows regardless of daily price fluctuations.

The Australian 10-year government bond yield currently sits at 5.02%, presenting a highly compelling domestic opportunity for capital allocators. This compares favourably to the US 10-year Treasury yield at 4.36%, especially when factoring in the currency risk associated with holding foreign government debt.

By focusing on yield generation rather than capital preservation alone, investors can secure reliable income streams even as underlying asset prices fluctuate. Shifting attention from daily capital pricing to structural income generation is the most pragmatic response to structurally higher borrowing costs.

This yield-centric approach fundamentally changes how portfolios weather macroeconomic storms. The mathematical certainty of a 5.02% sovereign yield provides a measurable buffer against simultaneous equity market volatility.

Defensive positioning in 2026 is less about avoiding all volatility and more about ensuring the portfolio generates enough internal cash flow to ride it out.

For readers wanting to apply these yield-focused concepts to local equities, our comprehensive walkthrough of ASX portfolio defence covers how to identify domestic companies with strong pricing power and optimal debt-to-equity ratios.

Moving from passive market observation to an active posture provides a necessary foundation for navigating ongoing volatility. The first priority for Australian investors is maintaining sufficient liquid capital to manage immediate expenses and execute opportunistic purchases.

According to industry data, Australian portfolio managers are currently emphasising strategic adjustments that favour neutral fixed-income positioning. Wealth platform guidance advocates for maintaining broad exposure and diversified asset allocations across the APAC region.

Effective wealth preservation strategies increasingly rely on rebalancing away from consumer-facing industries and pivoting towards more resilient local sectors like energy, utilities, and financials.

These regional allocations provide geographic insulation from the immediate impacts of the Middle East conflict. Implementing this defensive posture requires clear, methodical steps rather than reactive trading.

Translating complex macroeconomic analysis into actionable steps allows an Australian investor to protect and grow their wealth systematically. Establishing these defensive structures ensures the portfolio remains resilient regardless of how long the Strait of Hormuz bottleneck persists.

Managers stress that abandoning core investment strategies during a crisis often destroys more capital than the crisis itself. By deploying capital systematically, investors remove emotional decision-making from the equation.

This disciplined framework transforms market anxiety into a calculated process of accumulation and yield generation.

Balancing liquid capital with yield-generating fixed-income securities remains the most prudent strategy while global markets await resolution. Macroeconomic authorities are actively attempting to stabilise the core inflation driver behind this crisis.

The International Energy Agency (IEA) recently released 400 million barrels of oil, and the United States has lifted specific sanctions on Russian oil to ease supply constraints. Historical data indicates that financial instruments generally experience price recoveries once a clear trajectory toward resolution emerges.

Maintaining a disciplined asset allocation strategy during this waiting period allows investors to systematically capture discounted international equities before the broader market prices in a full recovery.

This recovery phase frequently begins long before absolute peace is finalised in the affected region. Patience and discipline will serve investors far better than reactive selling at the height of the crisis.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections remain subject to market conditions and various risk factors.

During an inflationary supply shock, safe haven investments are defined by their ability to generate reliable income, their insulation from soaring energy costs, and their capacity for swift liquidation without deep discounts. This differs from traditional safe havens which benefit from falling interest rates.

Australian investors can defend their portfolios by maintaining high liquidity, allocating capital to domestic sovereign bonds with strong yields, and systematically purchasing diversified index funds. Rebalancing towards resilient local sectors like energy, utilities, and financials is also recommended.

Central banks are reluctant to cut rates because the 2026 energy crisis is a severe supply shock that sustains high inflation. Monetary easing in such an environment would be dangerous, reflecting the need for prolonged restrictive policy even as economic growth deteriorates.

The current energy crisis is a supply shock that sustains high inflation, which actively prevents central banks from reducing interest rates. Past geopolitical shocks often coincided with collapsing economic growth, leading to central bank rate cuts and market liquidity.