Lululemon Fundamental Analysis: the Price of Brand Dilution

2 hrs ago

Tomorrow morning, Insperity will release its first-quarter financial report for 2026. The upcoming Insperity earnings disclosure presents high stakes for investors, contrasting a severe fourth-quarter deficit against aggressive recovery projections now circulating on Wall Street.

The company approaches a major test as shareholders seek validation of management’s turnaround strategy following a year of elevated benefit expenses and customer attrition. The release, scheduled for April 30, 2026, represents a definitive moment for the human resources provider. Market participants are watching closely to determine if the business has successfully absorbed the operational shocks of the previous fiscal year.

This analysis evaluates the underlying metrics driving the recovery narrative. It provides a comprehensive pre-market briefing that synthesises conflicting analyst estimates, examines strategic technology partnerships, and breaks down the significance of recent insider buying.

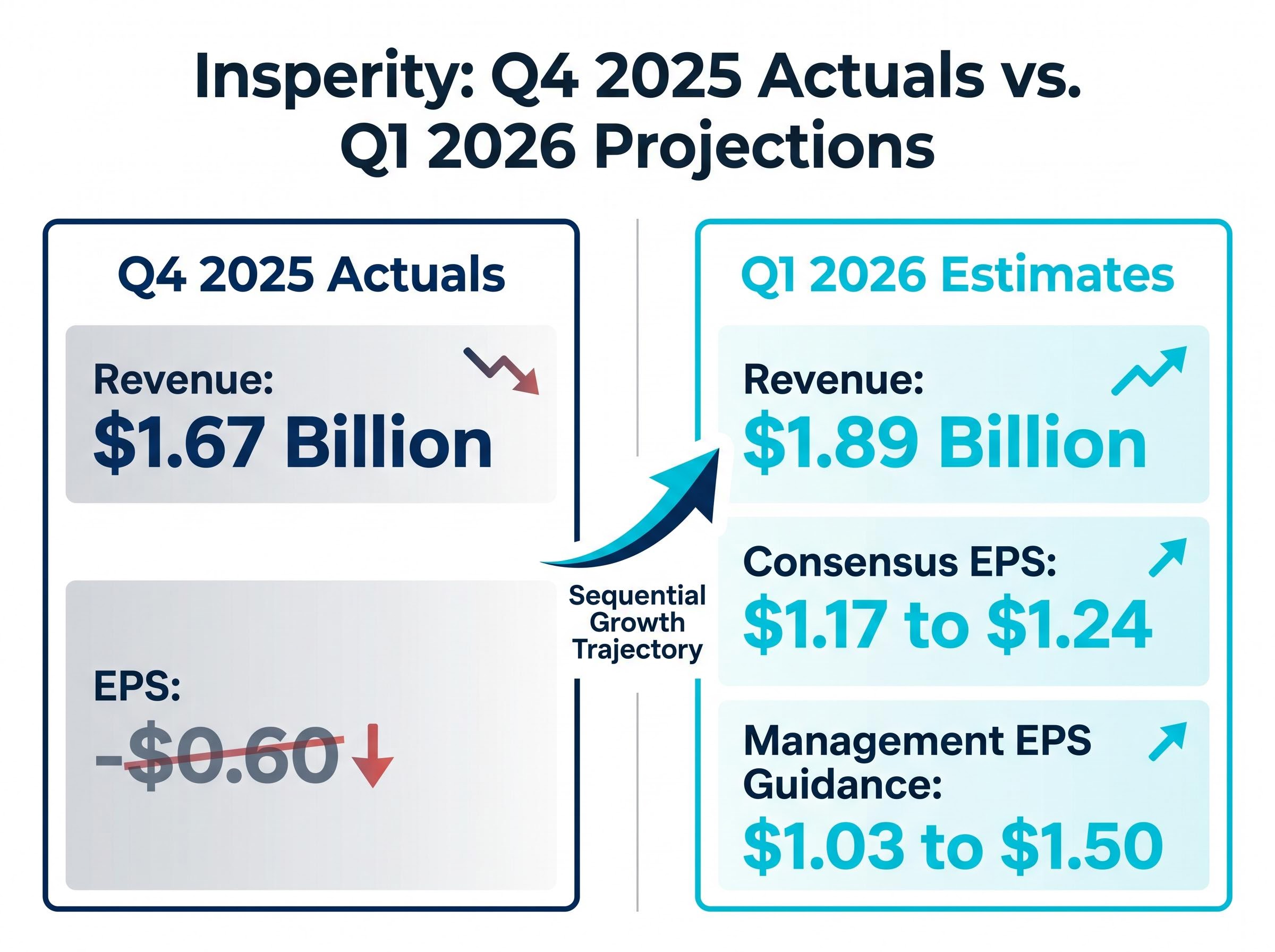

The financial community anticipates a sharp sequential improvement when the reporting period ending March 31, 2026, concludes. Analysts project revenue of $1.89 billion. This presents a stark contrast to the prior quarter actuals, which featured a $0.60 per-share deficit and $1.67 billion in revenue.

Wall Street maintains a wide variance in its expectations for the bottom line. The consensus baseline for earnings per share sits between $1.17 and $1.24, while company management has guided for a broader range of $1.03 to $1.50.

Management established this target range within Insperity’s official quarterly results, setting a clear performance benchmark that Wall Street analysts are currently evaluating ahead of the upcoming call.

Investors need absolute clarity on the consensus baseline to accurately gauge whether the reported figures constitute a beat or a miss when the market opens.

Management has also rescheduled the customary conference call to 5:00 PM ET, shifting away from the traditional morning slot. This logistical change often signals the potential for strategic announcements alongside the standard financial review.

| Metric | Q4 2025 Actuals | Q1 2026 Consensus Estimate |

|---|---|---|

| Revenue | $1.67 billion | $1.89 billion |

| Earnings Per Share (EPS) | -$0.60 | $1.17 to $1.24 |

| Sequential Growth Trajectory | Negative | Moderate Recovery |

Forecasters maintain differing outlooks on the pace of the profitability recovery due to varying assumptions about healthcare cost absorption. Some models assume immediate margin improvement, while others project a delayed realisation of pricing power. Management’s full-year 2026 earnings target of $1.69 to $2.72 remains the ultimate benchmark for success.

Analysts will use the first-quarter results to determine if this annual guidance remains mathematically viable.

A Professional Employer Organisation operates as a co-employer for small and medium-sized businesses. The provider assumes responsibility for payroll, benefits administration, and human resources compliance. This structure allows smaller companies to access large-scale corporate benefits while transferring regulatory liabilities to the provider.

Rising macroeconomic pressures currently act as a fundamental catalyst for business outsourcing in this sector. Employers face a projected 10% median increase in healthcare costs for 2026. This sharp inflationary pressure drives smaller enterprises toward the shared model to secure better premium rates through pooled risk groups.

This estimate aligns with recent industry analyses of projected employer health plan costs, which highlight how inflationary pressures on medical benefits are fundamentally reshaping corporate budgets.

These industry-wide dynamics directly influence the company’s ability to defend its pricing power and gross margins. The business currently reports a trailing twelve-month gross profit margin, while the broader sector continues at a modest low-single-digit expansion pace. Understanding these macroeconomic tailwinds allows investors to separate systemic industry challenges from company-specific execution failures.

Three primary ways inflation and regulatory complexity drive small businesses toward adoption include:

Securing access to pooled healthcare purchasing power to offset double-digit premium increases. Transferring the administrative burden of complex employment laws to specialised providers. * Consolidating fragmented payroll and benefits software systems into a single managed service.

The current equity valuation reflects a clear tension between historical performance constraints and forward-looking optimism. The stock price sits at $35.25, languishing near the lower boundary of its 52-week range. This depressed valuation follows a challenging fiscal year that resulted in a negative trailing price-to-earnings ratio.

However, forward multiples suggest the market has begun to price in an anticipated operational turnaround. The stock trades at a forward price-to-earnings multiple of approximately 15.67. This represents a more normalised valuation framework, assuming management can deliver on its recovery targets.

Market watchers maintain mixed ratings, but recent upgrades suggest a potential stabilisation in sentiment. In April 2026, Zacks upgraded the stock to a hold rating, indicating that the heaviest selling pressure may have concluded. The average analyst price target is $47.50, representing an implied double-digit upside from current trading levels.

This forecasting divergence stems from differing views on the professional employer organisation sector, where specialised Wall Street consensus models attempt to price in both company execution and macroeconomic volatility.

This valuation context helps determine if the stock offers a sufficient margin of safety for new capital allocation. Institutional firms maintain varying degrees of conviction regarding the upside potential.

The highest individual price targets currently maintained by institutional firms include:

Abstract financial models gain credibility when supported by concrete executive action. Between March 17 and March 19, 2026, Chief Executive Officer Paul Sarvadi purchased 201,987 shares of company stock. This massive open-market acquisition serves as tangible evidence that management believes a valuation floor has been established.

The chief executive executed this $4.6 million total investment at price points ranging from $22.53 to $23.93. This transaction resulted in a 16% increase in his personal executive holdings. Executive capital deployment often serves as the most reliable leading indicator of fundamental business improvement, offering readers confidence beyond spreadsheet projections.

Executive Conviction Signal

The aggressive $4.6 million open-market purchase by the chief executive officer represents a substantial commitment of personal capital, acting as a clear indicator of internal confidence in the company’s 2026 recovery trajectory.

Alongside insider buying, the company launched the HRScale platform in February 2026 through a strategic partnership with Workday. This collaboration targets small and medium-sized businesses with integrated technology and human resources services. These two developments serve as the primary qualitative pillars supporting the bullish recovery thesis for the current fiscal year.

Investors exploring the strategic value of this technology integration will find our full explainer on the HRScale partnership, which examines how the Workday collaboration is specifically designed to improve client retention and offset recent attrition metrics.

The balance of risks and opportunities remains delicate ahead of the impending earnings release. Investors must monitor the reported gross profit margins and any commentary on healthcare cost containment when the figures are published. These specific metrics will indicate whether the strategic adjustments implemented late last year have successfully stabilised the underlying business model.

Similar to other major corporate turnaround initiatives across the consumer and service sectors, the market requires consistent execution on operational efficiency targets before rewarding the equity with multiple expansion.

At current valuation levels, the stock presents a commercial viability that relies heavily on management’s ability to execute its margin recovery plan. The rescheduled 5:00 PM ET conference call will demand close attention, as forward-looking commentary will likely dictate the immediate market reaction.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

Insperity is scheduled to release its first-quarter 2026 financial report on April 30, 2026, with the customary conference call rescheduled to 5:00 PM ET.

A PEO like Insperity co-employs small and medium-sized businesses, managing payroll, benefits, and HR compliance. This model helps smaller companies access large-scale benefits and mitigate regulatory liabilities, especially amid rising healthcare costs.

Investors should closely monitor reported gross profit margins and any commentary on healthcare cost containment, as these metrics will indicate the success of recent strategic adjustments. The company's ability to meet its full-year 2026 EPS guidance will also be critical.

CEO Paul Sarvadi's recent $4.6 million open-market purchase of Insperity shares, increasing his personal holdings by 16%, serves as a strong signal of management's conviction in the company's 2026 recovery trajectory and established valuation floor.