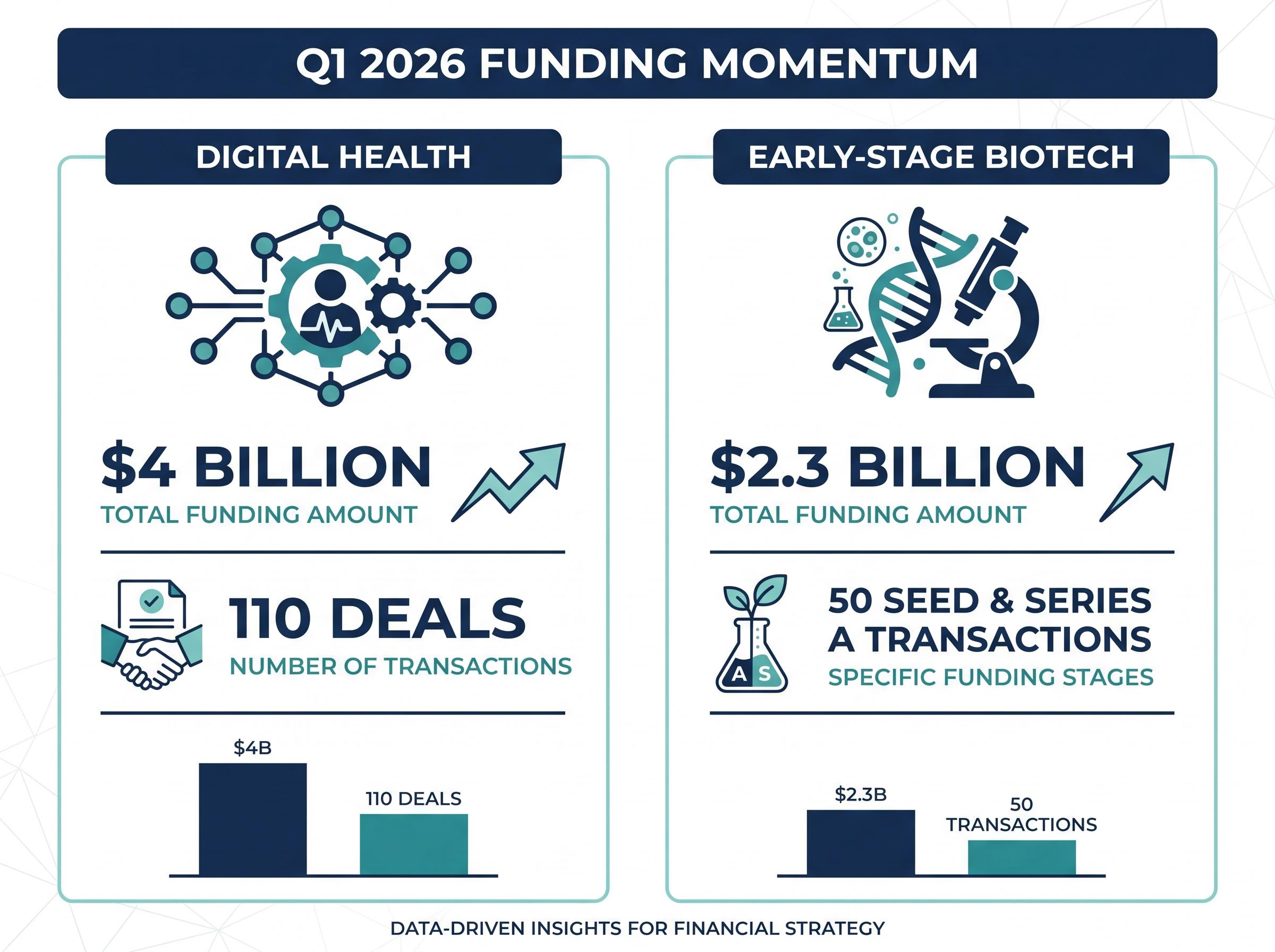

The first quarter of 2026 delivered a decisive shift in medical funding, with digital health startups raising $4 billion across 110 deals. This momentum highlights how health tech investments are pivoting sharply from academic theory into applied clinical practice. Artificial intelligence is no longer an abstract concept but a primary filter directing early-stage healthcare capital within the United States market today.

Finance professionals and venture allocators are actively re-evaluating their portfolios as these technologies target specific diagnostic and therapeutic bottlenecks. The rapid transition of machine learning from research laboratories to patient-facing applications demands a structured approach to sub-sector intelligence.

This analysis profiles four distinct sub-sectors currently capturing early-stage capital. By examining the mechanics of specialised accelerators and the startups they support, this overview provides a clear trend-spotting guide for upcoming medical technology breakthroughs.

The valuation shift in early-stage medical ventures

Evaluating modern medical technology startups requires understanding how clinical validation fundamentally alters early-stage valuation models. There is a distinct financial boundary between funding minor software improvements and backing fundamental biological research. Pure software updates present lower capital requirements, whereas deep-tech biological interventions necessitate rigorous, capital-intensive clinical trials.

The integration of clinical validation and direct provider access has now become the primary value proposition for top-tier medical accelerators. The intersection of artificial intelligence and digital health acts as the core growth driver for seed and Series A rounds. Investors are demanding tangible proof that early-stage platforms can interface seamlessly with established medical networks.

This dynamic forces startups to demonstrate clinical utility much earlier in their lifecycle to justify their initial valuations.

The Rock Health market analysis of Q1 2026 digital health funding confirms this rigorous new baseline, showing that venture capital is increasingly concentrated in enterprises possessing concrete pathways to provider integration rather than pure theoretical research.

Q1 2026 Funding Momentum Market data indicates digital health startups raised $4 billion across 110 deals in the first quarter, while early-stage biotech secured $2.3 billion across 50 seed and Series A transactions.

Standard accelerator equity metrics reflect this stringent new baseline. Institutions such as Cedars-Sinai are currently offering early-stage startups $100,000 for 5% equity. These terms establish a clear standard for healthcare capital allocation, providing investors with a structural framework to assess entry points into clinical artificial intelligence and digital health enterprises.

When big ASX news breaks, our subscribers know first

Bridging academia and commerce via specialised accelerator models

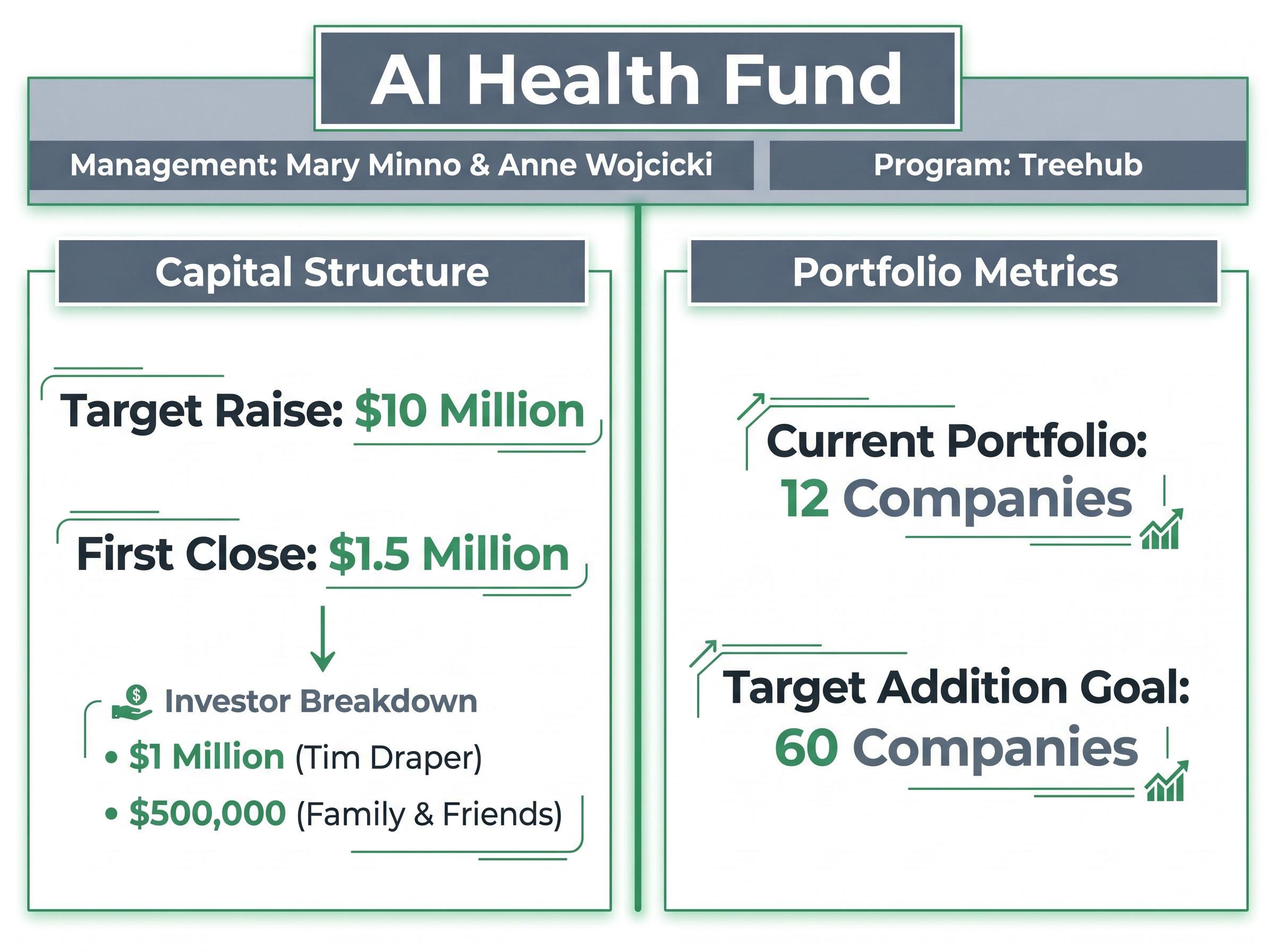

Translating abstract clinical data into viable commercial enterprises requires investment engines designed specifically for medical commercialisation. The AI Health Fund provides a leading example of this operational framework. Positioned strategically alongside Stanford University biomedical data science programmes, the fund bridges the gap between academic research and de-risked institutional capital.

The fund targets a $10 million raise, having held a $1.5 million first close last year. This initial capital pool included a $1 million check from prominent investor Tim Draper, supplemented by $500,000 from family and friends. Management figures such as Mary Minno and Anne Wojcicki are actively championing the commercial viability of these startups, ensuring that scientific discovery maps directly to market demand.

Founders entering the fund’s Treehub programme undergo a rigorous operational cycle. The accelerator provides an introductory capital injection and transitions founders from laboratory isolation to medical network integration. The fund currently backs 12 companies, with an aggressive long-term goal of reaching 60 portfolio additions.

| Startup Name | Target Sub-Sector | Core Technology | Market Driver |

|---|---|---|---|

| Clair Health | Women’s Health | AI Wrist Wearable | $5.28B Endocrine Market |

| Diggy | Pediatric Behavioural Tech | AI Mitigation Platform | 20% Sector Growth |

| Nestwell | Environmental Analytics | Home Testing Systems | Medicaid Budget Integration |

| Korda | Predictive Modelling | Illness Mapping Systems | 22.75% CAGR Projection |

Continuous endocrine tracking and the consumer wearables market

Grounding abstract artificial intelligence concepts into tangible hardware accelerates both consumer adoption and regulatory clarity. Clair Health demonstrates this principle through its rapid entry into the broader femtech ecosystem. Founded in October 2025, the startup transitioned swiftly from stealth mode to active beta testing in early 2026.

This rapid execution speed serves as a primary indicator of market readiness. Industry analysis indicates the continuous endocrine tracking market is expanding aggressively, projected to reach $5.28 billion in 2026, up from $4.36 billion in 2025. Capturing this growth requires hardware that balances clinical accuracy with consumer-friendly pricing.

The company is actively executing the following commercialisation steps:

Beta testing a $299 wrist-worn continuous hormone monitoring device. Integrating artificial intelligence to process real-time endocrine fluctuations. Preparing documentation for formal Food and Drug Administration (FDA) review. Planning a full commercial scale launch targeted for late 2026.

Navigating the regulatory pathway toward FDA approval is necessary for securing institutional healthcare budgets. Connecting hardware innovation directly to concrete pricing models provides investors with transparent timelines for funding milestones. If successful, this wearable technology will transition hormone tracking from periodic clinical blood draws to continuous, non-invasive residential monitoring.

Investors exploring the regulatory hurdles associated with transitioning novel diagnostics and therapeutics to market will find value in our comprehensive walkthrough of FDA pivotal trial requirements, which outlines how single-trial BLA pathways can dramatically reduce commercialisation timelines.

Monetising behavioural platforms and environmental analytics

Scalable software platforms are increasingly capturing healthcare value outside of traditional clinical settings. Technologies addressing pediatric development and home environments are tapping into massive, previously underserved markets by delivering targeted interventions directly to residential addresses. Multidisciplinary care approaches are fueling rapid growth in these behavioural tech platforms.

These out-of-clinic care models reduce systemic healthcare costs while providing founders with highly scalable business trajectories. Connecting residential wellness analytics to established public healthcare funding mechanisms proves the commercial viability of the model.

Pediatric autism platforms and behavioural mitigation

The autism therapy market experienced nearly 20% growth in 2025, driven heavily by demand for accessible interventions. Diggy, spearheaded by Stanford researcher Dennis Walls, is actively building pediatric autism behavioural tech platforms.

The company integrates artificial intelligence to support behavioural mitigation and therapy under specialised medical leadership. This approach allows families to access structured developmental support without waiting for limited clinical appointments.

Companies are increasingly advancing AI infrastructure for autism diagnosis toward formal FDA clearance, aiming to capture the broader pediatric market by leveraging smartphone-based assessment models.

Residential wellness analytics and public health integration

Environmental analytics represent another major expansion of the home health platform model. Nestwell launched in 2026 to provide comprehensive environmental testing and residential wellness analytics.

- Deploying diagnostic testing hardware into the residential environment.

- Analysing local environmental data for public health risks.

- Integrating findings directly with public health networks.

The commercial validation for this sub-sector is already established in parallel markets. An affiliated entity, Nest Health, successfully raised a $22.5 million Series A in November 2025. This capital injection specifically funded in-home care expansion tailored to addressing environmental factors for Medicaid-eligible families.

Predictive disease modelling as a long-term capital play

Predictive medical modelling represents the ultimate convergence of massive data sets and long-term clinical forecasting. While consumer wearables and home testing offer immediate commercial feedback, predictive analytics require longer gestation periods to map complex medical progressions. This sub-sector engineers systems that identify illness vulnerabilities years before symptoms present.

Foundational academic research, such as the NIH systematic review on predictive healthcare, provides the clinical validation necessary to justify the extended gestation periods of these deep-tech medical algorithms.

Market Growth Projection Research data indicates the predictive disease analytics sector is projected to soar from $3.83 billion in 2025 to an estimated $24.23 billion by 2034, reflecting a massive Compound Annual Growth Rate (CAGR) of 22.75%.

Despite these immense market growth projections, near-term funding updates for deep-tech medical modelling often remain opaque. Startups in this space operate with extended development cycles, prioritising data acquisition and algorithmic refinement over immediate hardware sales.

Korda serves as a representative entity within this specialised field. The company focuses on engineering advanced systems to map long-term medical trajectories. While it has not released public funding or trial updates in 2026, its foundational technology addresses the high-reward, longer-horizon sub-sector required for diversified medical portfolios. Balancing rapid-commercialisation hardware with deep-tech predictive modelling allows venture capital to capture both immediate market share and structural long-term upside. Investors willing to absorb these longer development cycles stand to benefit from platforms that alter how global healthcare networks anticipate and allocate resources for chronic illnesses.

Assessing the next wave of healthcare capital allocation

Continuous tracking, environmental analytics, and predictive modelling form the core pillars of future medical technology investments. The momentum observed in early 2026 confirms that artificial intelligence validation is permanently altering the criteria for early-stage healthcare funding. Startups must now demonstrate clear clinical utility and provider integration from their inception.

Achieving multi-site institutional adoption across tier-one hospital networks remains the ultimate proof of concept, transitioning emerging technologies from pilot phases into standardized clinical guidelines.

Specialised accelerators play a central role in transitioning these academic concepts into viable, de-risked commercial enterprises. By providing early capital, structured mentorship, and direct access to medical networks, these programmes minimise the traditional friction of medical commercialisation. For finance professionals assessing the sector, monitoring these structured accelerator cohorts offers the clearest visibility into the next generation of healthcare breakthroughs.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.