Goldman Sachs Cuts 2026 Smartphone Shipment Forecast 10% on AI Crunch

19 hrs ago

As Wall Street evaluates the current cycle of Big Tech earnings, the defining analytical narrative has shifted from software development to the physical supply chain required to run artificial intelligence. The reporting period in late April 2026 exposes a fundamental market reality regarding the sheer scale of the technology capital expenditure supercycle. Financial disclosures from major hyperscalers are now serving as a critical barometer for downstream infrastructure health rather than mere indicators of digital advertising or cloud software demand.

This pivot requires investors to re-evaluate traditional tech valuations, as capital actively rotates away from digital-only models toward tangible hardware and energy assets.

The true commercial opportunities in this technology cycle require looking past the hyperscalers themselves. Analysts expect capital to flow rapidly toward the utility and alternative energy providers that are actively solving the power bottlenecks threatening artificial intelligence deployment. Identifying these beneficiaries involves tracking how massive infrastructure budgets are converting into physical grid adaptations. Investors must look at the companies providing the physical foundation for this digital expansion to understand where the next phase of market rotation is heading.

Combined artificial intelligence infrastructure capital expenditures for Amazon, Alphabet, Meta, and Microsoft are projected to reach between $600 billion and $720 billion in 2026. This historic investment volume signals that artificial intelligence is no longer merely a software pursuit. It has rapidly evolved into a highly capital-intensive physical asset class requiring massive downstream supply chains.

Aggregated financial projections from Bloomberg’s 2026 infrastructure expenditure analysis confirm that the bulk of this corporate spending will target custom cooling systems and dedicated utility construction rather than standard computing hardware.

The upcoming financial disclosures will test whether cloud and search revenue growth can justify these historic spending levels. Market forecasts suggest strong underlying performance, with Alphabet expecting 30 percent revenue growth to roughly $55 billion. The company also projects profit margins to remain above 17 percent, providing the necessary capital to fund continued infrastructure expansion.

| Technology Giant | Projected 2026 Infrastructure CapEx |

|---|---|

| Amazon | ~$200 billion |

| Alphabet | ~$180 billion |

| Meta | ~$125 billion |

| Microsoft | ~$105 billion |

According to market estimates, the four reporting technology giants currently account for approximately 18.3 percent of the total S&P 500 index valuation. This concentration means their collective capital allocation decisions dictate broader market trends. The multi-billion dollar expenditures detailed above represent a direct transfer of wealth from technology balance sheets to the companies responsible for building physical data centres, cooling systems, and power generation facilities.

Readers analysing these earnings reports must look beyond the top-line software revenue. The sheer volume of projected spending establishes a massive pool of capital that is actively flowing downstream to physical infrastructure providers.

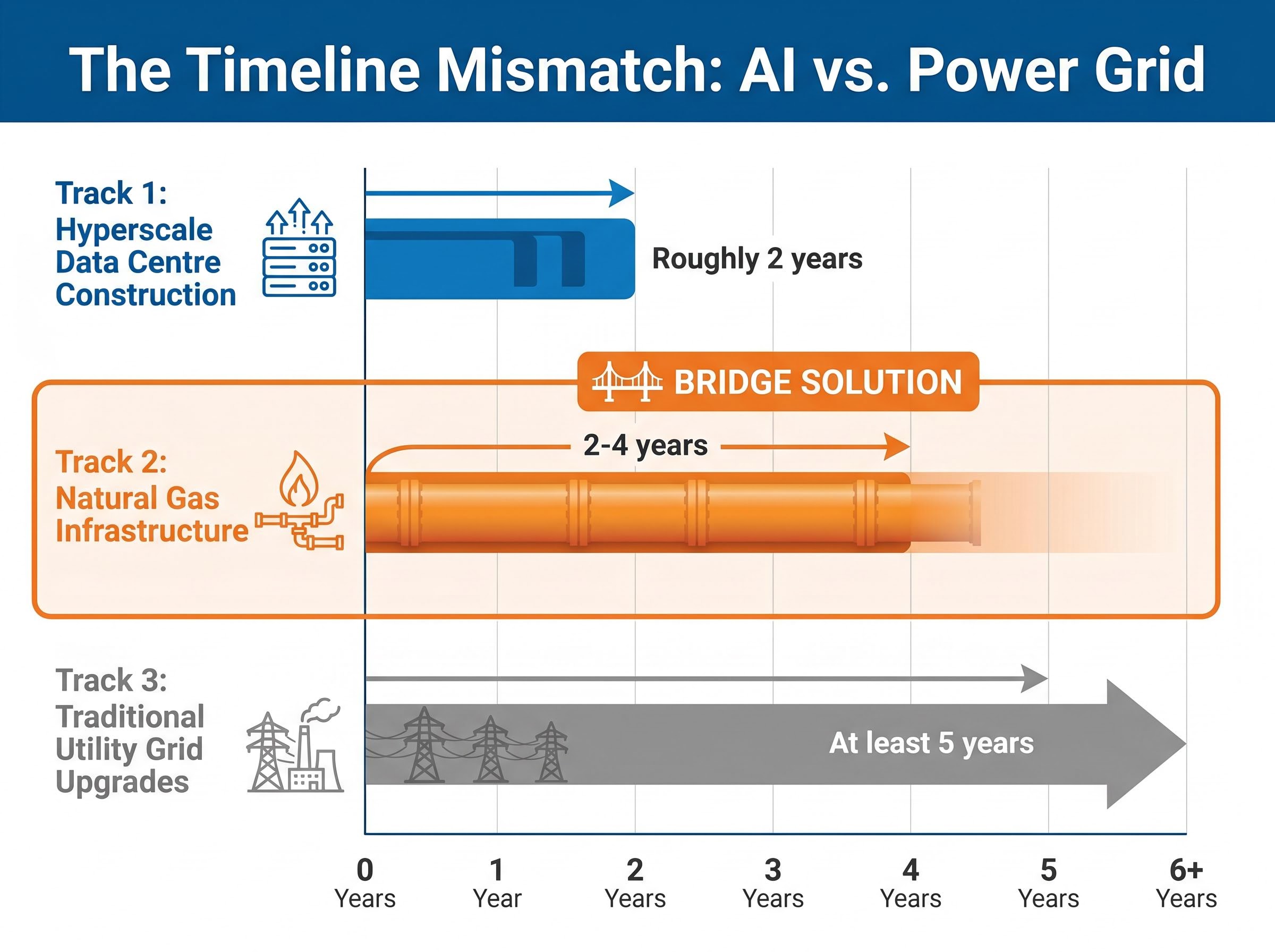

The scale of projected data centre construction places a severe burden on existing power grids. Traditional grid infrastructure is entirely insufficient to support the rapid deployment rate of modern hyperscale computing facilities. Data centre operations require continuous, uninterrupted base-load power to function, and the current electrical grid lacks the capacity to meet this sudden surge in concentrated demand.

An official Department of Energy analysis identifies these concentrated computing workloads as the primary catalyst for domestic capacity shortfalls, prompting federal utility regulators to accelerate national transmission planning.

“United States data centre power demand is projected to reach 106 GW by 2035, representing a 36 percent increase from prior industry estimates.”

Overall domestic energy demand is expected to triple in this same timeframe. The core issue driving infrastructure investment is a profound timeline mismatch between digital ambition and physical reality. Technology companies can construct a new hyperscale data centre in roughly two years, but traditional utility grid upgrades and transmission line installations typically require at least five years to complete.

This structural delay has positioned natural gas as the critical bridge fuel for the artificial intelligence supply chain. Natural gas infrastructure is deployable within 2-4 years, offering a much faster alternative to waiting for standard grid overhauls. Technology companies simply cannot wait for long-term transmission upgrades if they intend to maintain their current artificial intelligence development schedules.

Consequently, utility planning documents show that proposals for new gas-fired power generation have tripled in the United States to 252 GW. Forward projections indicate that while renewable sources will meet approximately 40 percent of new data centre demand, natural gas will fulfill the majority of the remaining deficit. By understanding this timeline delay, investors can grasp why alternative behind-the-meter generation has suddenly become a premium commercial asset.

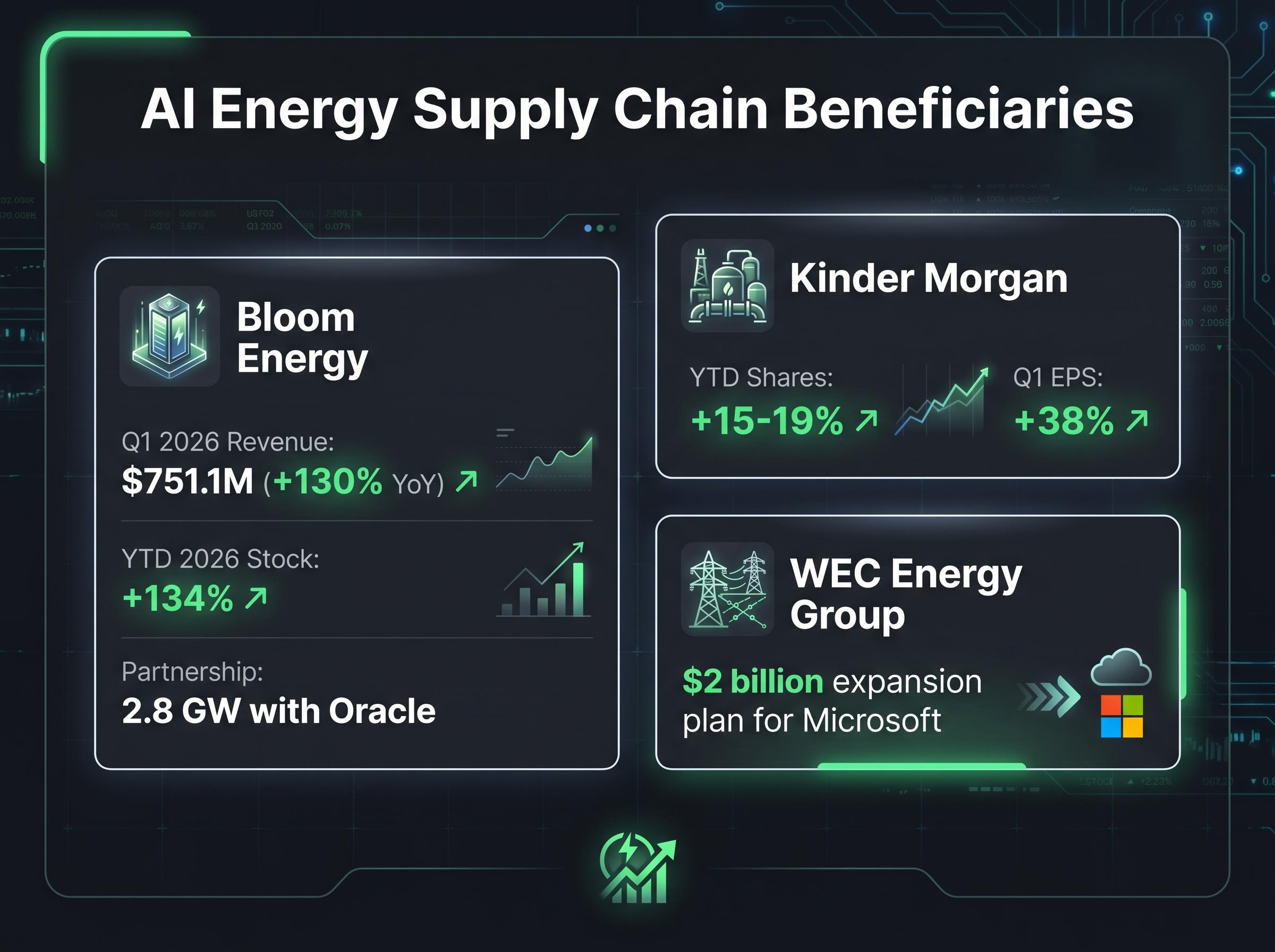

Alternative energy companies are capitalising on these supply chain bottlenecks by providing independent power generation solutions directly to technology firms. Bloom Energy serves as the primary case study for how behind-the-meter technology demands translate into commercial success. The company reported record Q1 2026 revenue of $751.1 million, representing a 130 percent year-over-year increase.

This financial performance is driven directly by the artificial intelligence sector securing independent power sources. Bloom Energy recently announced a major partnership with Oracle to deploy up to 2.8 GW of fuel cell systems for new data centre infrastructure. As a result of this technology sector integration, Bloom Energy stock has surged 134 percent year-to-date in 2026.

The shift toward long-term power contracts and geographic flexibility allows technology companies to bypass grid constraints entirely. This dynamic creates distinct commercial opportunities for energy providers willing to enter into direct partnerships with hyperscale developers.

Regional utilities and traditional natural gas producers are executing massive custom projects to meet these specific hyperscaler demands. Companies like Entergy and Williams Companies are developing tailored infrastructure solutions, including dedicated power plants built explicitly for individual technology clients. These dedicated facilities bypass the broader grid to deliver reliable power directly to targeted computing locations.

Industry data highlights the immediate financial impact of these custom infrastructure agreements across the sector:

Kinder Morgan shares have gained 15-19 percent year-to-date, supported by a 38 percent increase in Q1 earnings per share directly tied to data centre natural gas demand. WEC Energy Group is dedicating a new $2 billion natural gas expansion plan specifically to power Microsoft computing facilities. * EQT Corporation and other natural gas producers are experiencing sustained volume growth as they supply the fuel necessary for these independent generation projects.

These metrics demonstrate how massive technology budgets are translating into record earnings for specific energy equities. The power sector has effectively transformed into the physical supply chain for the artificial intelligence industry.

Readers interested in the specific mechanics of these independent power agreements will find value in our comprehensive walkthrough of hyperscaler grid bypass strategies, which analyses how alternative energy stocks are securing lucrative off-grid contracts.

The multi-trillion dollar infrastructure frenzy requires a predictable macroeconomic environment to remain viable. Current central bank policy is acting as the necessary catalyst for these massive, multi-year construction projects. The capital expenditure requirements detailed in major technology earnings reports rely heavily on stable borrowing costs across the supply chain.

As of late April 2026, the Federal Reserve target federal funds rate remains confirmed at 3.50-3.75 percent. The effective rate sits at 3.64 percent following the central bank’s third consecutive meeting without policy changes. This steady hold creates a highly predictable financing environment for long-term utility and infrastructure developments.

According to some forecasts, market analysts note that traders do not anticipate monetary easing actions until late 2027. This makes the current stable interest rate environment a long-term feature of the market rather than a temporary pause. For highly leveraged infrastructure providers, this predictability ensures that massive capital projects can proceed without the threat of sudden debt servicing spikes.

Maintaining these steady borrowing costs is also critical for sustaining hardware supplier profitability expectations, as any tightening in credit markets could force technology giants to aggressively scale back their future procurement budgets.

Investors assessing the macroeconomic risk profile must factor in these stable borrowing costs. Lower volatility in debt markets provides the financial foundation required to sustain the current pace of physical artificial intelligence development.

The journey from abstract technology earnings to physical energy constraints reveals distinct islands of wealth forming across the market. The next phase of the artificial intelligence boom will not be built solely on software algorithms. It will be built on natural gas pipelines, alternative fuel cells, and extensive physical grid adaptations.

A precise stock selection strategy is required to navigate this shift. Investors should look beyond broad technology market exposure and focus on the direct infrastructure beneficiaries securing long-term hyperscaler contracts. The utility providers and energy firms actively solving the grid bottleneck represent the practical commercial application of the 2026 technology capital expenditure supercycle.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections and forward-looking statements are subject to market conditions and various risk factors.

Recent Big Tech earnings reports indicate a significant pivot from software development to massive physical infrastructure investments for AI, with projected capital expenditures of $600 billion to $720 billion in 2026.

The primary beneficiaries include utility companies, alternative energy providers, and natural gas producers that are building dedicated power plants, cooling systems, and grid adaptations for hyperscale data centers.

Natural gas infrastructure can be deployed in 2-4 years, offering a much faster solution than the 5+ years typically required for traditional utility grid upgrades and transmission line installations to meet surging data center power demands.

Stable interest rates, with the Federal Reserve maintaining its target at 3.50-3.75 percent, provide a predictable financing environment essential for the massive, multi-year construction projects required for AI infrastructure.