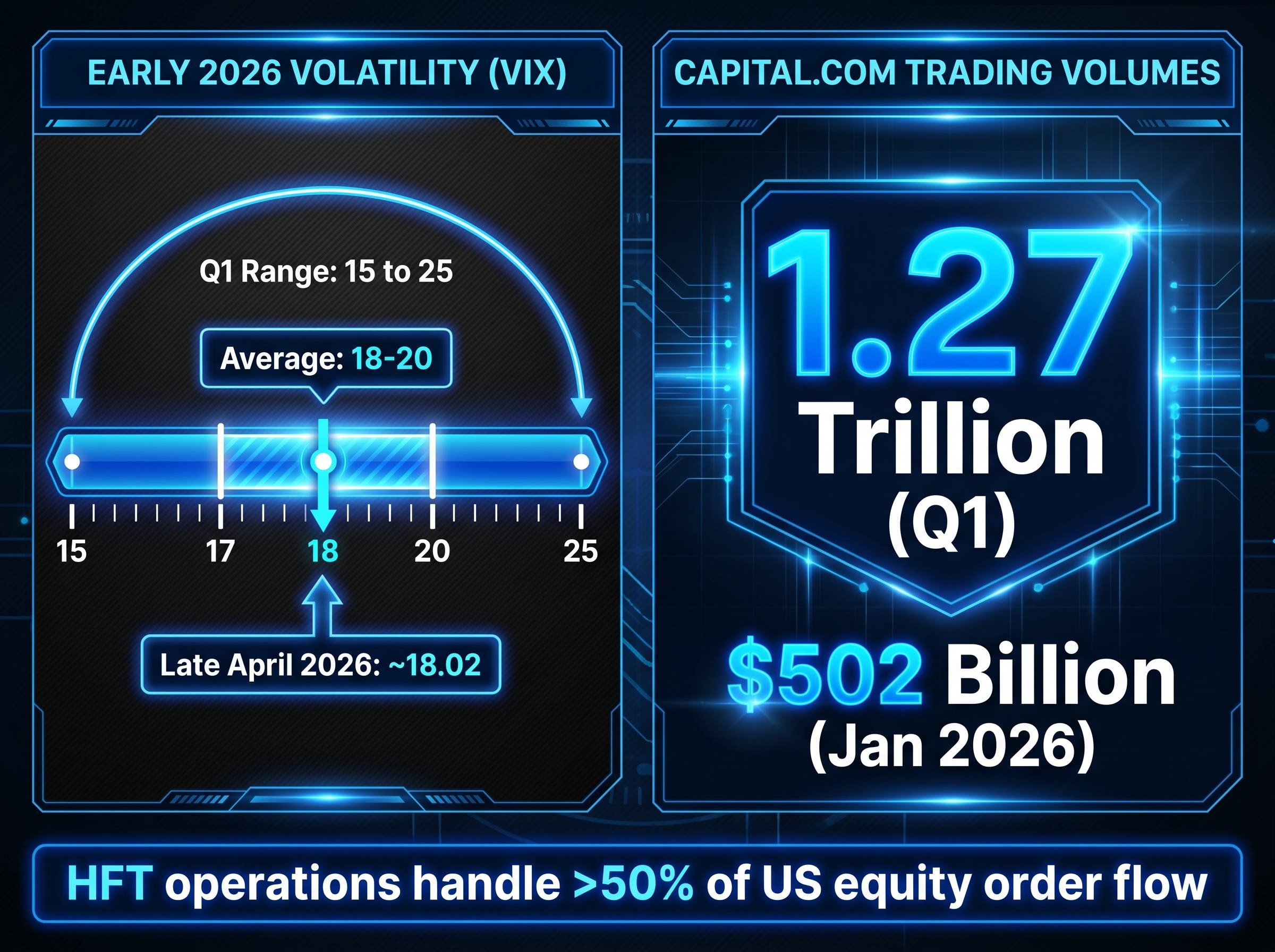

Global trading platforms absorbed elevated volumes in early 2026, with Capital.com reporting $1.27 trillion in client trading volumes for the first quarter alone. The United States market environment faces elevated but contained volatility, driven by the sharp repricing of geopolitical risks in European equities and central bank gold purchasing reaching a 25-year high. Firms like Jane Street and Citadel Securities generated tens of billions of dollars in revenue by capitalising on this precise market environment.

This article unpacks the hidden machinery behind the record profits generated by top algorithmic operations. It explains the core mechanisms of a high frequency trading strategy, revealing how leading firms combine immense capital injections, elite quantitative talent, and strict coding disciplines to maintain dominance. By examining these overlapping forces, investors gain a clearer view of how automated platforms convert tiny market fluctuations into billions of dollars in net revenue. Understanding this operational reality provides vital context for anyone observing modern financial markets.

The Mechanics of Market Making in High Volatility Environments

Algorithmic market making involves deploying automated software to continuously quote buy and sell prices across multiple exchanges simultaneously. These operations capture tiny price discrepancies, known as the spread, across millions of individual transactions executed in fractions of a second. The strategy thrives during periods of elevated but non-extreme market movement, where price fluctuations create constant trading opportunities without triggering structural panics.

High-frequency operations currently handle over 50% of United States equity order flow. The market conditions of early 2026 provided an ideal environment for these automated desks. The CBOE Volatility Index (VIX) fluctuated between 15 and 25 throughout the first quarter, averaging between 18 and 20.

Recent academic research on market efficiency confirms this dominant market share, demonstrating how automated liquidity provision stabilizes bid-ask spreads even during heightened institutional trading activity.

As of late April 2026, the VIX sits at approximately 18.02, a level that provides enough movement for algorithms to profit while remaining predictable enough for risk models to manage. Broader market activity amplified these opportunities, with surging spot trading pushing platform volumes higher. January 2026 alone accounted for $502 billion of Capital.com’s volume, driven by gold trading and a fivefold increase in silver spot trading.

This foundation of elevated volatility acts as the primary catalyst for automated trading profits. This foundational knowledge clarifies a concept often obscured by Wall Street jargon, showing that these firms primarily provide liquidity in exchange for capturing the spread.

Core Infrastructure and Execution Speed

Software algorithms hold no value without the physical hardware required to execute trades faster than competing firms. The physical reality of low-latency trading requires highly specialised, purpose-built equipment that operates continuously.

Firms rely on three primary infrastructure components to achieve this level of market making:

- High-performance computing networks designed to process vast datasets in real time.

- Co-located servers positioned physically adjacent to exchange matching engines to achieve microsecond latency.

- Custom execution platforms capable of processing millions of daily trades without system degradation.

These physical assets form the necessary foundation before a single line of algorithmic code can be deployed.

When big ASX news breaks, our subscribers know first

Fueling the Algorithms with Massive Capital Injections

While sophisticated code identifies trading opportunities, raw financial power dictates the scale of the resulting profits. Algorithms require immense base funds to operate effectively, meaning success in automated execution is ultimately a game of capital scale. Deploying massive amounts of capital acts as pure fuel for these highly tuned execution engines, allowing them to absorb positions and manage risk across global exchanges.

Recent financial results demonstrate the phenomenal return on capital these firms achieve during favourable market conditions. Jane Street generated approximately $40 billion in net trading revenue in 2025, nearly doubling its previous year’s net trading revenue of $20.5 billion. Hudson River Trading reached approximately $12.3 billion in revenue, closely followed by Citadel Securities at roughly $12.2 billion.

Strategic capital deployment directly correlates with outsized quarterly returns for these dominant players. According to reports, Virtu Financial recently injected $500 million into its active trading funds to capture emerging market opportunities. According to reports, as of March 2026, the publicly traded firm held $2.6 billion in total deployed capital.

This expanded capacity is essential for converting market volatility into profitability, allowing algorithmic systems to capture wider bid-ask spreads during periods of elevated trading volumes.

According to reports, this massive financial scale allows Virtu’s market-making sector to generate $10.4 million in daily net trading proceeds. According to reports, over the trailing twelve months, the firm achieved a 107% average yield on its deployed capital, highlighting the sheer efficiency of well-funded algorithmic operations.

| Trading Firm | 2025 Revenue Estimate | Reported Scale Metrics |

|---|---|---|

| Jane Street | $40.0B | Nearly doubled year-on-year net trading revenue |

| Hudson River Trading | $12.3B | Sustained high-performance computing investments |

| Citadel Securities | $12.2B | Paid 75-100% premium for elite quantitative talent |

| Virtu Financial | N/A (Publicly listed) | According to reports, $2.6B deployed capital (March 2026) |

These figures confirm that the barrier to entry in modern quantitative finance is largely defined by the ability to secure and deploy multibillion-dollar funding lines. By examining these exact revenue figures, observers can see that mathematical brilliance requires billions in base funding to generate material returns.

The Talent War Squeezing Industry Profit Margins

The competitive battleground extends far beyond server speeds and capital reserves to the human intelligence required to build the machines. Top United States trading operations face intense pressure to secure premium industry talent from a highly restricted global pool. Firms do not view these elevated personnel costs as negative expenses, but rather as deliberate strategic necessities required to support ongoing market dominance.

Securing the specific expertise needed to process real-time market data requires aggressive recruitment across major financial hubs. Firms like Tower Research and Jump Trading are currently focused on hiring for the following highly sought-after roles:

Machine learning talent capable of designing statistical arbitrage models. Artificial intelligence specialists focused on quantitative market analytics. C++ engineers tasked with writing low-latency execution code. Hardware experts and real-time data analysts.

Compensation Structures and Retention Strategies

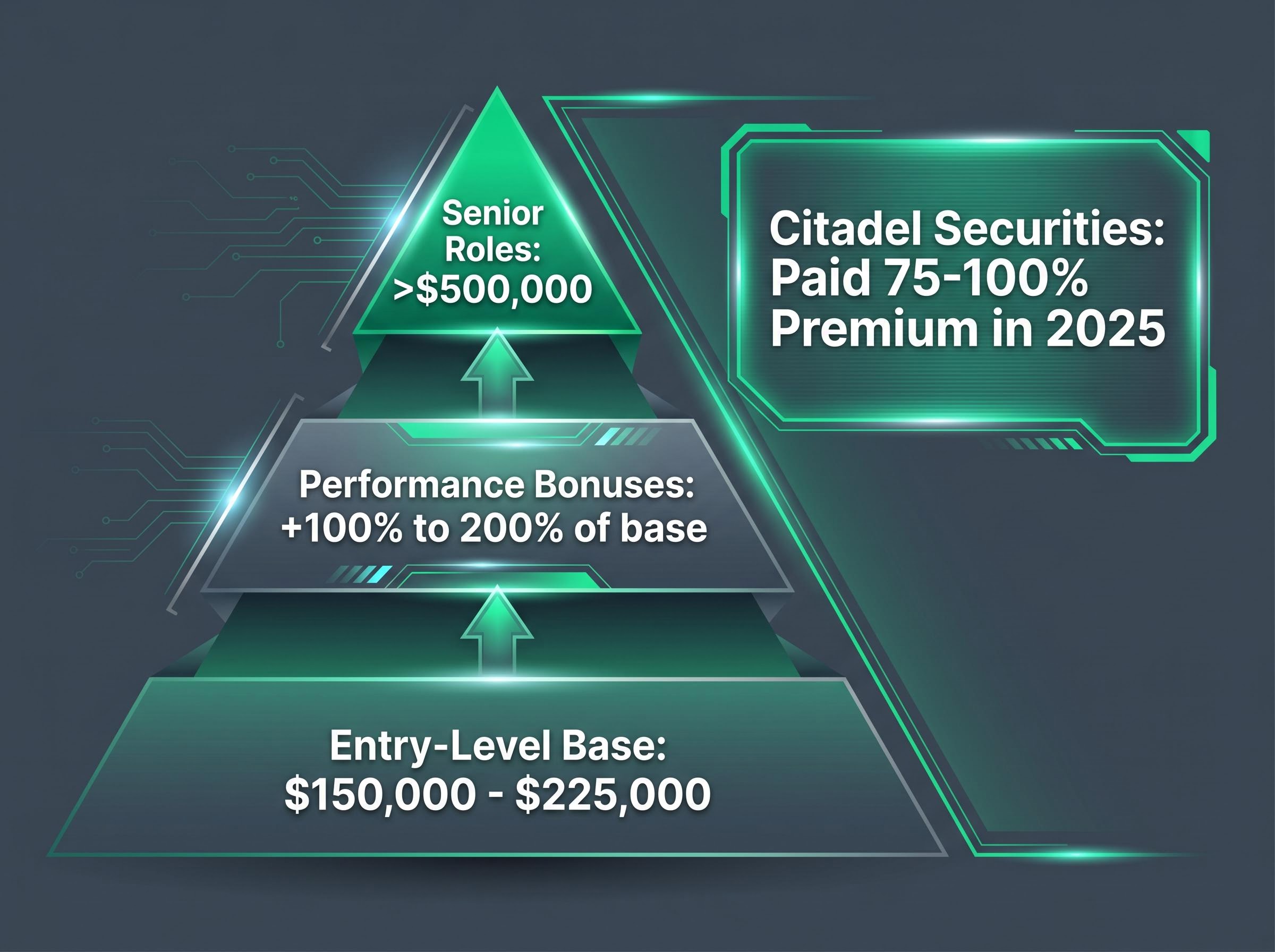

Outsized profitability directly translates into talent retention in this fiercely competitive environment. Entry-level quantitative analysts command base salaries ranging from $150,000 to $225,000. These base figures represent only a fraction of total remuneration, with performance bonuses frequently reaching 100% to 200% of base pay depending on fund performance.

Senior role compensation packages routinely exceed $500,000, with top-performing portfolio managers and developers securing total earnings well into the millions. Citadel Securities aggressively led the market in 2025, paying a 75% to 100% premium over peer firms to secure elite quantitative talent. This aggressive strategy forces competing operations to continually adjust their own remuneration models upwards to prevent staff attrition.

According to reports, Virtu Financial allocates 22% of its revenues to employee remuneration, viewing this expenditure as a core operational requirement. According to reports, the firm projects a total headcount of approximately 1,100 individuals for 2026, underscoring the massive personnel requirements of automated trading. This compensation structure reveals the exact kind of human capital required to run automated financial systems, providing a rare look into Wall Street’s most secretive sector.

For investors analyzing how human capital drives algorithmic outperformance, our deep-dive into Virtu Financial’s strategic resilience explores how precise personnel investments and controlled technology frameworks created a structural moat that generated massive quarterly beats.

The Generative AI Wall in Core Execution Code

While the algorithmic trading sector relies heavily on traditional machine learning for statistical arbitrage, it deliberately rejects Generative AI for core trading infrastructure. This creates a clear technological boundary within the smartest firms on Wall Street. Generative models, which predict sequential outputs based on vast training data, are entirely unsuitable for the strict, deterministic requirements of algorithmic execution.

A deep technical analysis of latency mismatch highlights how artificial intelligence inference times remain measured in milliseconds, making them fatally slow for execution frameworks that operate within sub-microsecond constraints.

The risks associated with hallucinations or unverified code are catastrophic in low-latency, high-stakes financial environments where millions of dollars can be lost in milliseconds. Firms utilise traditional artificial intelligence for market analysis, quantitative strategy development, and historical pattern recognition. However, the latency-critical C++ execution algorithms remain strictly traditionally engineered by human developers.

According to industry analysis, there is currently zero verifiable public data indicating that leading market makers have adopted Generative AI for deploying core trading code. Generative tools may assist with routine developmental tasks or back-office coding processes, but they do not touch the execution mechanisms that route live orders to exchange servers.

Industry Leadership Stance on Core Systems Market making executives explicitly cite software reliability and hallucination risks as the primary barriers to core implementation. Institutional leadership maintains a strict separation between Generative AI experimentation and latency-critical execution code, ensuring that all live trading systems remain entirely predictable and deterministically programmed.

This deliberate rejection helps investors differentiate between general technology trends and the rigorous reality of institutional algorithmic operations. The speed and accuracy demanded by high frequency systems simply cannot tolerate the unpredictable processing pathways inherent in large language models.

The Future Equation for Algorithmic Dominance

The modern automated trading sector relies on a precise equation of massive capital scale, elite human talent, and strictly disciplined technological infrastructure. Firms that successfully integrate these three pillars generate outsized returns during periods of elevated market movement. However, the sector faces identified forward-looking risks that require constant navigation.

Regulatory shifts, escalating personnel expenditures, and fluctuating economic environments all threaten to compress profit margins over time. Past performance during the volatility of early 2026 does not guarantee future results, as financial projections remain subject to rapidly changing market conditions.

Despite massive advances in automated execution and statistical modelling, the ultimate differentiator in modern market making remains the quality of human strategic oversight. The algorithms simply execute the vision programmed by quantitative talent and funded by strategic capital allocation.

While autonomous AI agents are rapidly disrupting traditional SaaS models across the broader technology sector, high frequency trading operations deliberately maintain human oversight to prevent catastrophic execution errors.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.