The latest Virtu Financial earnings data reveals a fundamental detachment between market expectations and high-frequency trading realities. As broader United States equities navigated persistent inflation concerns throughout the first quarter of 2026, this execution specialist converted macroeconomic friction into record commercial output.

This analysis evaluates whether the firm’s unprecedented revenue beat signals a permanent structural advantage or a temporary volatility premium. Investors must understand how these massive operational metrics translate into forward-looking equity valuation. Understanding these mechanics provides a critical edge for portfolio positioning.

Quantifying the First Quarter Revenue Shock

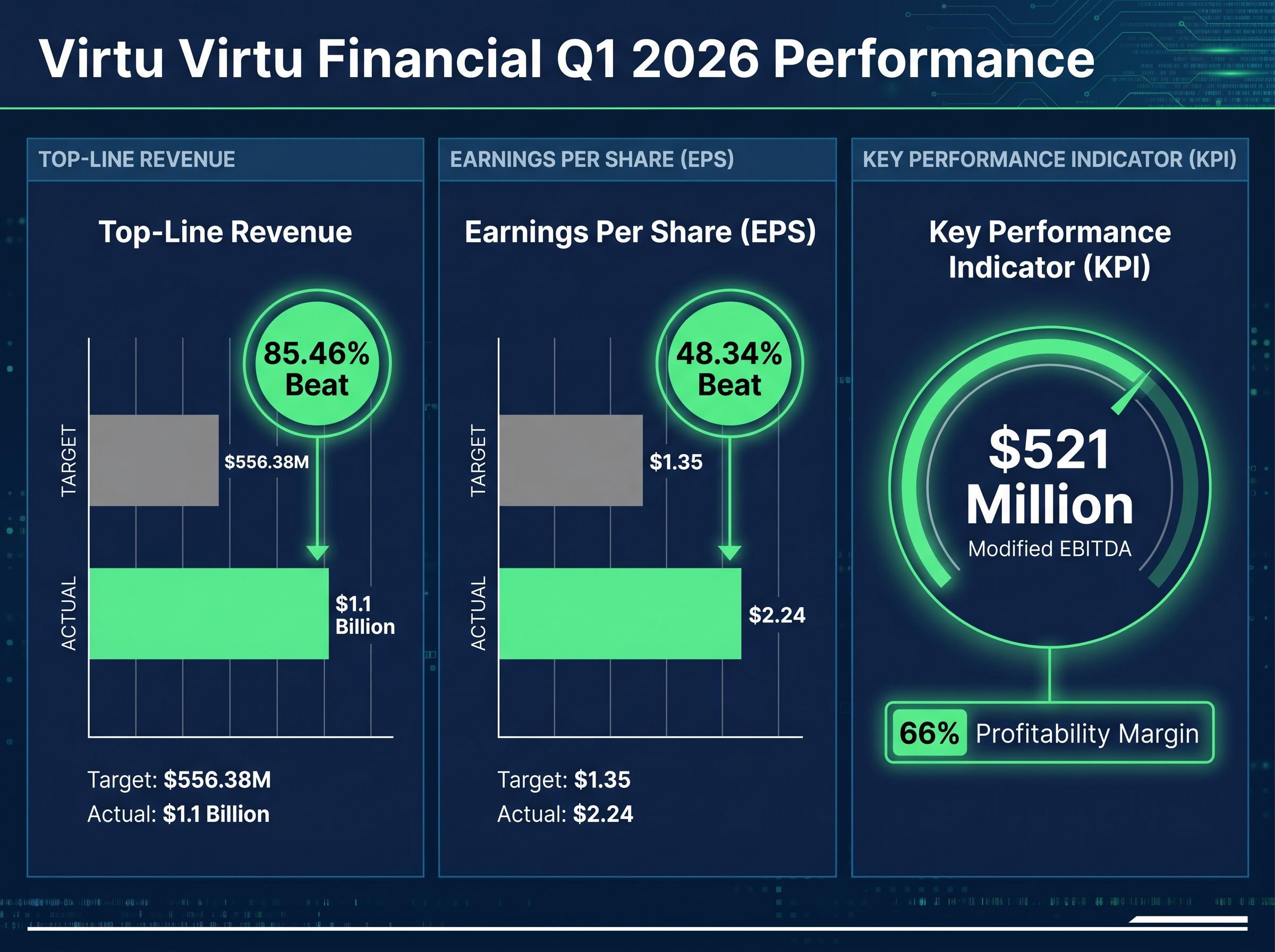

Wall Street forecast a highly profitable quarter, but the actual figures dismantled baseline projections entirely. The firm generated top-line revenue totalling $1.1 billion, eclipsing the pre-release consensus of $556.38M by a staggering 85.46%. This massive top-line expansion immediately cascaded through the company’s operating leverage.

Revenue Outperformance “The 85% top-line beat represents a historic operational milestone, demonstrating the immense scalability of the firm’s execution infrastructure during periods of market stress,” reported leading sector analysts reviewing the preliminary data.

Per-share earnings reached $2.24, representing a 48.34% positive variance against the anticipated $1.35 target. The profitability metrics proved equally striking when compared to historical performance. According to company data, modified EBITDA settled at $521 million, yielding a 66% profitability margin that few traditional financial institutions can replicate.

The official first quarter financial results confirm this massive operational scaling, demonstrating how peak transaction volumes convert directly into sustained free cash flow.

This corporate success stems directly from sustained operational momentum within the execution services division over the trailing twelve months. Across the three-month period, according to company data, modified daily net commercial income equated to $12.9 million. These figures provide investors with a concrete baseline to anchor expectations for the firm’s forward-looking operational scale.

| Financial Metric | Pre-Release Consensus | Q1 2026 Actuals |

|---|---|---|

| Top-Line Revenue | $593.11 million | $1.1 billion |

| Earnings Per Share (EPS) | $1.51 | $2.24 |

| Profitability Margin (EBITDA) | N/A | 66% |

The magnitude of this positive variance highlights the substantial operating leverage inherent in the firm’s commercial framework. When trading volumes spike, top-line generation translates almost directly into massive profitability margins without requiring proportional cost increases. The market reaction confirmed the absolute scale of this financial surprise. Institutional investors immediately began recalculating the firm’s earning power based on this newly established operational floor.

When big ASX news breaks, our subscribers know first

The Mechanics of Market-Making Profitability

Understanding this financial outperformance requires examining how liquidity providers actually operate in modern financial markets. Unlike traditional asset managers who require equity prices to rise, market makers generate income from the friction of trading activity itself. When United States macroeconomic conditions shift rapidly, trading volumes naturally expand.

This environment allows execution services to capture the bid-ask spread, which is the tiny price difference between a buyer’s offer and a seller’s asking price. As broader market volatility increases, these spreads widen significantly. This mechanism multiplies the profit opportunity on every individual transaction processed through the firm’s algorithms.

Volume Expansion: Increased market uncertainty drives higher transaction counts across all asset classes. Spread Widening: Volatility increases the risk of holding assets, forcing market makers to demand wider spreads for providing immediate liquidity. * Algorithmic Capture: High-frequency systems execute millions of these widened spread transactions daily to compound fractional gains into massive revenue.

The specific market environments of early 2026 directly fuelled this mechanism, rewarding the firm’s structural framework. The execution segment registered its eighth sequential three-month span of expanding net commercial income. Daily execution services generated roughly $2.5 million throughout the quarter, a marked increase from the $2.1 million daily average recorded across the previous year.

Retail investors often view market turbulence as a portfolio threat. However, for specialized execution firms, these volatile periods act as the primary catalyst for rapid revenue generation. Macroeconomic volatility serves as a distinct structural advantage rather than an operational headwind.

The rise of extreme index concentration has only amplified this perceived threat, as heavy weightings in a few mega-cap stocks can cause significant swings in passive retirement accounts.

Capital Allocation and the Engineering Arms Race

Management is aggressively reinvesting these windfall profits to secure long-term operational superiority across the financial sector. The firm is not simply harvesting temporary volatility spikes to pad immediate earnings. Leadership is actively expanding the foundational trading capacity and engineering talent pool required to maintain market dominance.

- Active Trading Funds: Deploying excess capital directly into market-making strategies to increase total daily transaction volume capacity.

- Talent Acquisition: Offering top-tier remuneration to secure elite quantitative developers and engineering specialists.

- Shareholder Payouts: Sustaining a recurring dividend to reward investors while funding operational expansion.

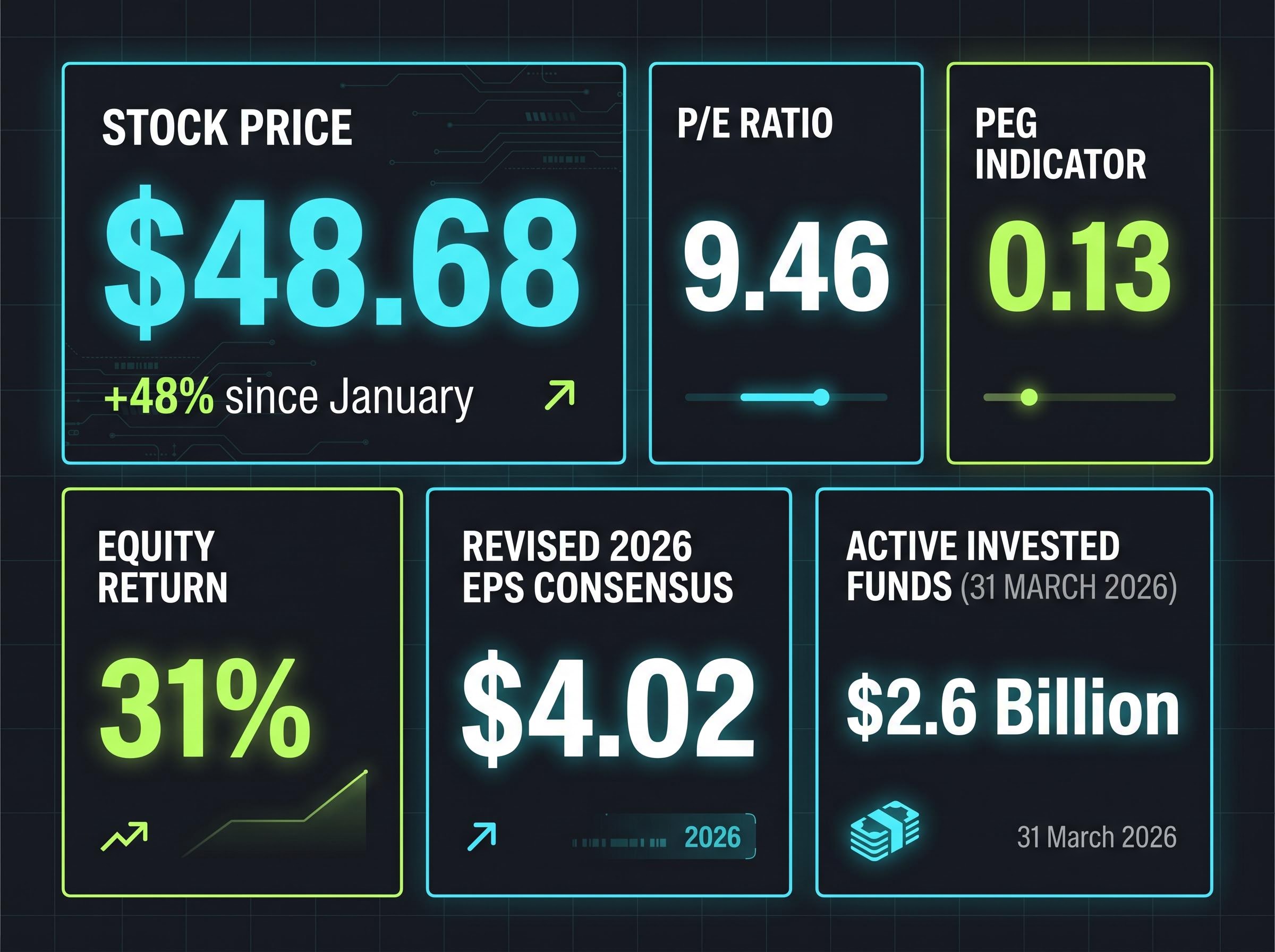

As of 31 March 2026, according to company data, active invested funds amounted to $2.6 billion. This massive capital base generated an average 107% return throughout the preceding twelve months. To compound this mathematical advantage, management augmented the active trading base by more than $500 million over the previous seven-month span.

The enterprise also sustained its recurring $0.24 per-share shareholder payout. This strategic decision balances aggressive reinvestment needs with immediate capital returns for existing investors.

Navigating AI Integration in Core Trading

The expansion of trading capacity requires premier engineering talent. Leadership intends to expand the workforce toward roughly 1,100 personnel over the 2026 calendar year. The firm accepts elevated remuneration ratios to recruit elite developers from a highly competitive technology sector.

Interestingly, executives maintain a strict boundary regarding artificial intelligence deployment within their core systems. While the enterprise embraces machine learning for routine coding and back-office software efficiency, leadership explicitly rejects automated generation for complex live trading algorithms. This calculated restraint prevents systemic vulnerabilities and keeps core execution strategy firmly human-directed.

For investors comparing this disciplined technological approach against the broader market frenzy, our detailed coverage of AI infrastructure risks examines how massive, unprofitable hardware spending threatens valuations elsewhere in the tech sector.

Translating Earnings Windfalls into Equity Valuation

The sheer scale of the first-quarter performance has fundamentally altered the underlying stock’s valuation framework. Shares logged a 48% appreciation since January began, hitting $48.68 during preliminary trading sessions following the earnings release. Investors must now carefully evaluate whether this rapid surge leaves any room for new capital deployment.

Despite the dramatic year-to-date rally, current valuation multiples suggest the equity remains attractively priced against its revised earnings baseline. The stock trades at a 9.46 price-to-earnings ratio, paired with a remarkably low 0.13 PEG indicator. Equity return metrics currently measure at an exceptional 31%.

These baseline fundamentals prompted immediate reaction from institutional market observers. Half a dozen financial analysts aggressively raised their future profit expectations in response to the operational data. The consensus revision highlights a broader institutional recognition of the firm’s market-making dominance. Analysts now view the early-year performance as a sustainable operational baseline rather than an isolated anomaly.

Consensus Revision “The magnitude of the first-quarter outperformance has forced a complete recalibration of forward models, establishing a revised $4.02 per-share consensus for the full 2026 timeline,” reported institutional trading analysts.

This rigorous commercial framework indicates the underlying equities may not be overbought despite recent price action. The revised baseline presents a highly favourable risk-to-reward profile for investors seeking exposure to execution services. Capital deployment at these levels still offers a logical entry point relative to projected future cash flows.

Evaluating Headwinds That Threaten Margin Sustainability

Peak margins inevitably attract operational friction, and investors must systematically assess the specific vulnerabilities that could erode these historic returns. The bullish narrative faces clear structural and regulatory challenges that demand careful consideration. Committing capital at a peak valuation requires acknowledging these distinct operational risks.

External Market and Regulatory Vulnerabilities

The fluctuating United States macroeconomic environment presents the most immediate threat to daily volume generation. Prolonged periods of low volatility could severely compress execution margins and restrict revenue opportunities. If inflation concerns suddenly abate and interest rate stability returns, the trading friction that funds this operational model will naturally diminish.

Furthermore, execution services operate under continuous regulatory scrutiny that could impact operational profitability.

Algorithmic Oversight: Potential regulatory shifts targeting the speed and frequency of automated trade execution. Market Structure Reforms: Proposals that could alter how bid-ask spreads are quoted across major exchanges. * Reporting Requirements: Increased compliance costs associated with heightened transaction monitoring and data retention mandates.

The persistent threat of Securities and Exchange Commission oversight shifts could force costly adaptations to existing algorithmic trading frameworks. Such changes frequently require massive internal development resources to maintain compliance.

Internal Cost Drivers and Talent Retention

Internal expenditure presents an equally pressing challenge to long-term margin sustainability. According to company data, direct monetary remuneration accounted for 22% of total expenses during the three-month period. This heavy cost burden reflects the escalating obligations required to maintain top-tier operational talent.

The enterprise is fighting a constant talent war against primary competitors like Citadel Securities and Jane Street. To manage these pressures, leadership made an explicit decision to avoid establishing an internal hedge fund vehicle due to capacity limitations. This keeps the firm entirely reliant on its core market-making operations rather than diversifying revenue streams.

Recent compensation data for quantitative developers highlights how this specialized talent pool commands increasingly aggressive remuneration packages across the broader proprietary trading sector.

Weighing the Strategic Position in the 2026 Financial Sector

The massive first-quarter revenue outperformance validates management’s strategy of pairing aggressive active capital deployment with strict algorithmic oversight. While shifting regulatory frameworks and high remuneration costs present real ongoing risks, the firm’s competitive positioning appears highly fortified. The execution services division continues to convert macroeconomic uncertainty into reliable daily net commercial income.

This dynamic becomes particularly lucrative when underlying structural fragility in the US economy forces rapid capital reallocation across institutional portfolios.

The underlying operational expansion thoroughly justifies the newly elevated 9.46 price-to-earnings ratio. Management has demonstrated a clear ability to expand workforce capacity without sacrificing core profitability margins. For investors seeking structural exposure to broader market volatility, this enterprise offers a unique combination of operating leverage and technological discipline for the remainder of 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.