Sovereign acquisition patterns experienced a severe plunge in early 2026, yet central bankers emerged projecting overwhelmingly positive sentiment. Formulating an accurate gold price prediction model requires reconciling this apparent contradiction.

The market currently reflects this tension, with spot valuations stabilising in the mid-$4,500 range during late April. This pricing follows extreme first-quarter volatility driven by sudden geopolitical conflicts and abrupt shifts in monetary policy expectations.

This analysis examines the structural drivers behind sovereign purchasing patterns and the logistical shift toward domestic storage. Investors require a clear framework to contextualise the geopolitical hazards shaping institutional valuation targets for the remainder of the year. By tracking how central banks manage their physical reserves, market participants can better understand the baseline demand supporting current valuations.

Institutional Forecasts Point to a Sustained Rally

The precious metals market has absorbed the early-year shocks to establish a new pricing floor. As of 29 April 2026, spot valuations are trading in a narrow band between $4,570 and $4,575 per ounce. This late-April stabilisation represents a marked recovery from the mid-March lows that followed shifting interest rate expectations.

Major financial institutions have looked past this temporary first-quarter volatility to model aggressive long-term targets. J.P. Morgan projects valuations reaching $6,300 by the end of 2026, citing strong demand from both investors and sovereign entities. Goldman Sachs maintains a baseline target of $5,400, with their models accommodating an upside scenario of $6,350.

Recent Reuters reporting on revised targets underscores how tier-one investment banks are actively adjusting their long-term commodity models to account for this relentless physical accumulation.

These projections highlight the significant upside built into tier-one baseline models. State Street offers a more conservative base case between $4,000 and $4,500, but their bull scenario still pushes past the $5,000 threshold. For investors tracking these movements, the consensus indicates that temporary price pullbacks are occurring within a broader structural rally.

| Institution | Base Target 2026 | Bull Target 2026 | Key Driver |

|---|---|---|---|

| J.P. Morgan | $6,300 | Not specified | Strong structural demand |

| Goldman Sachs | $5,400 | $6,350 | Geopolitical hedging |

| State Street | $4,000 – $4,500 | $5,000+ | Monetary policy shifts |

When big ASX news breaks, our subscribers know first

Inside the Sovereign Buying Paradox

Sovereign acquisition patterns presented a confusing signal early in the year. Purchasing volumes rebounded to 27 tonnes in February 2026, leading some analysts to question whether the accumulation cycle had concluded. However, data directly contradicted the theory of a structural pullback.

Market models interpret the massive February drop as a temporary liquidity reaction rather than a trend reversal. When faced with sudden geopolitical volatility, several central banks paused acquisitions to assess immediate cash requirements. The underlying sentiment remains aggressively positive, as revealed by the conference polling data.

Reserve institutions anticipate expanding their holdings this year. Predict prices will remain above $5,000 per troy ounce over the next 12 months. Projections anticipate sovereign banks acquiring. The World Gold Council forecasts total central bank demand reaching 850 tonnes for the full year 2026.

The Mechanics of Sovereign Vaulting and the Repatriation Shift

Understanding market valuations requires examining how central banks physically manage their acquired assets. Historically, national reserve institutions preferred to store their bullion in international hubs like the Bank of England or the Federal Reserve Bank of New York. These offshore facilities offered high security and immediate liquidity, allowing nations to execute trades or secure loans without physically moving heavy metal.

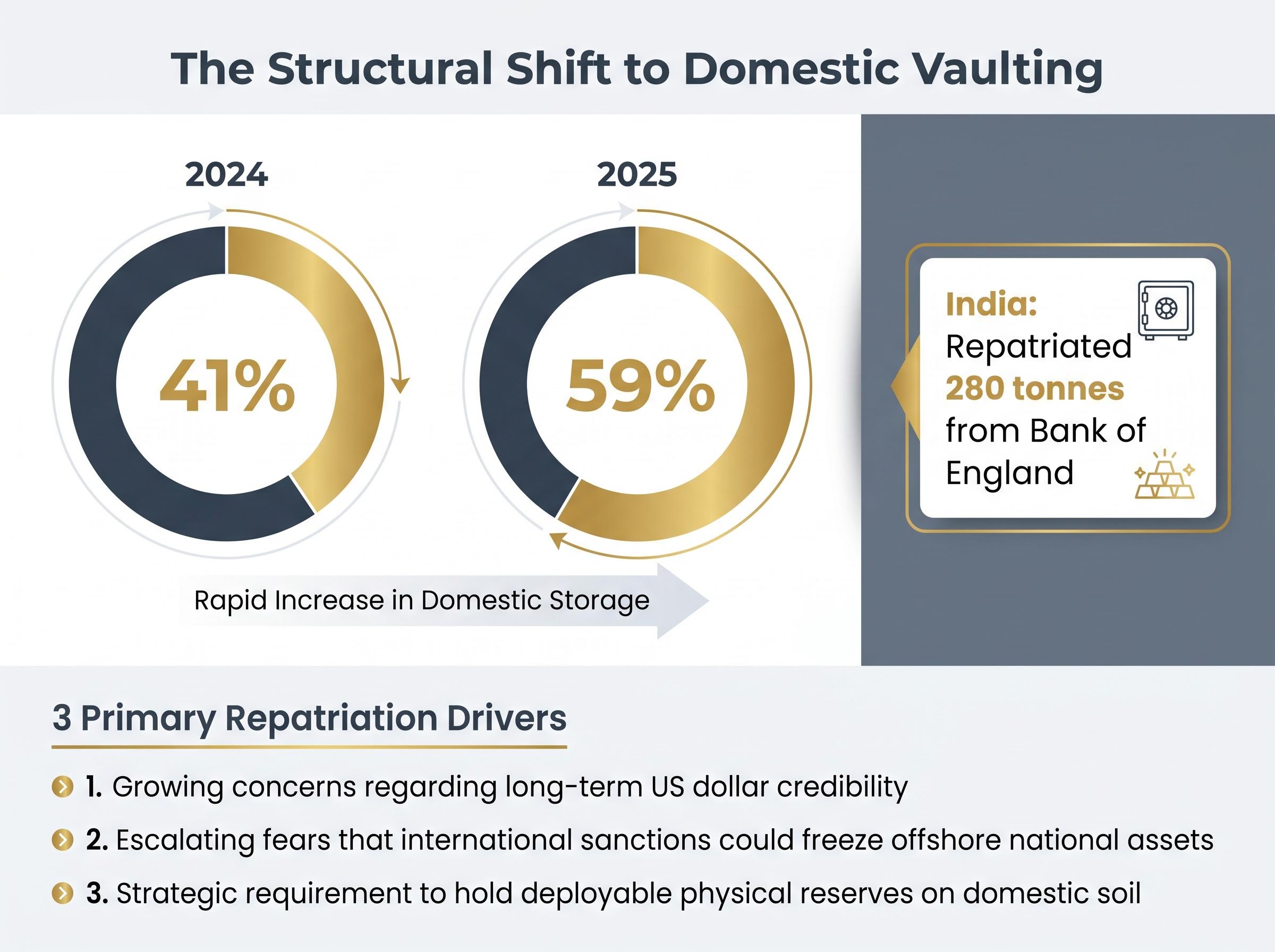

This established system is currently undergoing a massive structural shift toward domestic storage. As of 2025, data indicates that 59% of central banks now store their bullion domestically. This represents a significant and rapid increase from just 41% in 2024.

The latest World Gold Council survey data confirms this rapid accumulation of sovereign reserves within domestic borders, reflecting a broader institutional strategy to mitigate geopolitical risk by maintaining absolute physical control over national wealth.

This logistical reversal acts as a leading indicator for systemic risk assessment, signalling a fundamental decrease in trust toward Western financial infrastructure.

The recent actions of India provide a prime example of this geopolitical asset securing strategy. The nation recently executed the repatriation of 280 tonnes from the Bank of England to secure facilities within its own borders. Analysts suggest three primary drivers are accelerating this ongoing repatriation trend:

- Growing concerns regarding long-term US dollar credibility.

- Escalating fears that international sanctions could freeze offshore national assets.

- The strategic requirement for sovereign nations to hold deployable physical reserves on domestic soil.

By relocating physical bullion, nations are telegraphing their expectations for future global instability. For investors, these physical movements confirm that the current demand represents long-term strategic hedging rather than speculative trading.

Geopolitical Shocks Escalate Safe Haven Demand

Abstract market projections are currently being tested against a series of severe international crises. Early 2026 delivered multiple concurrent conflicts that forced institutional capital into alternative assets. These rapid geopolitical escalations have created a high pricing floor during turbulent trading weeks.

Regional Conflict and Energy Market Threats

The capture of Venezuelan President Nicolás Maduro on 3 January 2026 introduced immediate uncertainty into global energy markets. This specific event triggered a sudden flight to safety, driving a 3.4% valuation spike as capital sought shelter from anticipated supply chain disruptions.

This volatility compounded when the Iran conflict initiated on 28 February 2026. The resulting instability pinned trading within a wide and volatile band between $4,300 and $5,600. According to Goldman Sachs, escalating military tensions near the Strait of Hormuz continue to place a high premium on safe-haven positions.

Capital allocators are using physical precious metals as a direct proxy to hedge against these combined Middle Eastern and South American supply threats.

For investors wanting to understand the broader macroeconomic implications of these supply bottlenecks, our full explainer on how oil shocks transmit into recession risk details the four primary channels through which energy costs degrade consumer spending and corporate margins.

Unconventional Sovereign Risks

Beyond traditional military conflicts, markets are pricing in unconventional diplomatic friction. Recent territorial tensions regarding Greenland, coupled with associated tariff threats, have introduced an entirely new category of sovereign risk.

This diplomatic friction has disrupted traditional trade assumptions, forcing further capital into tangible assets. These overlapping crises translate directly into market impact, providing a measurable link between global headlines and institutional valuation spikes.

Managing the Federal Reserve Headwind

While international instability supports bullish sentiment, strict monetary policy provides a powerful analytical counterweight. The Federal Reserve continues to maintain a highly restrictive stance, creating macroeconomic friction that caps short-term upside potential.

Following the mid-March Federal Open Market Committee (FOMC) decision to hold rates steady, the market experienced a sharp valuation drop from over $5,000 down to the $4,100 range. As of late April, forward pricing models anticipate zero rate cuts for the remainder of 2026. Current derivatives markets indicate an approximate 30% probability of further rate hikes, with the central bank expected to hold the target range at 3.5% to 3.75%.

The conventional expectation for a rate-cut cycle has been heavily compromised by energy-driven inflation stemming from global shipping disruptions.

Downside Risk Warning “Past performance does not guarantee future results. Financial projections are subject to market conditions, and sustained high interest rates present a specific liquidation hazard if stock and bond sectors experience simultaneous downturns.”

This hawkish monetary environment maintains strong US dollar dynamics and high real yields. When yields on government debt remain elevated, non-yielding physical assets face natural resistance.

Analysts caution that if broader equity markets experience a severe correction, institutional investors may be forced to execute sudden portfolio liquidations to cover margin requirements. This dynamic protects investors from one-sided bullishness by highlighting the very real macroeconomic headwinds capable of triggering short-term value declines.

The Unprecedented Floor Under Alternative Assets

The current market environment is defined by the clash between restrictive central bank policy and relentless sovereign accumulation. The Federal Reserve’s hawkish stance successfully caps short-term pricing explosions by maintaining competitive yields on government debt. However, the purchasing data demonstrates that national reserve buyers are ignoring short-term yield dynamics in favour of long-term security.

This combination of determined central bank demand and ongoing geopolitical fracturing has established a historically high valuation floor. For valuations to break permanently through the $5,000 and $6,000 thresholds, a specific catalyst must emerge. Markets are waiting to see whether a formal shift in US monetary policy or a major escalation in the Strait of Hormuz will provide the necessary momentum to validate the highest institutional targets.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding market forecasts are speculative and subject to change based on macroeconomic developments.