Endeavour Group’s Dividend Reset: Income Stock or Reinvestment Bet?

6 hrs ago

The headline figures from the latest Parsons Corporation earnings report present a striking contradiction for the first quarter of 2026. A superficial reading shows a contraction in top-line revenue, but the underlying financials reveal unprecedented margin expansion and a historic contract backlog. The 29 April 2026 release arrives at a critical moment for United States federal defence and infrastructure spending.

Investors are currently weighing temporary accounting distortions against the core operational health of major government contractors. A comprehensive analysis of the underlying organic growth metrics is necessary to separate these isolated project fluctuations from the firm’s true trajectory. Government budgets remain under tight scrutiny, making efficiency metrics just as critical as top-line revenue intake.

By stripping away the temporary distortions caused by classified projects, a much clearer picture of baseline expansion emerges. The focus must shift from surface-level misses to the structural profitability that defines the company’s current market position.

Total capital intake dropped, but the firm’s profitability metrics surged. The divergence between the top-line revenue miss and the significant bottom-line earnings beat defines the quarter. Parsons reported total revenue of $1.491 billion, falling short of the $1.529 billion Wall Street consensus and representing a 3-4% year-on-year decline.

Despite this contraction, the company delivered an adjusted earnings per share of $0.79, comfortably beating the consensus estimate of $0.69 to $0.70. Record margin expansion drove this positive earnings surprise. According to company data, the firm achieved first-quarter margins of 10.1%, representing a 50-basis-point expansion from the previous year.

This earnings beat highlights a shift toward rigorous operational cash management, allowing the firm to translate a smaller revenue pool into a substantially higher earnings yield per share.

Adjusted EBITDA reached $151 million, marking a 1% increase despite the reduced revenue base. This efficiency demonstrates why a drop in total capital intake did not compromise the underlying operational profitability. According to company data, net income did settle lower at $53 million, marking a 20% drop, but this figure requires context within the broader financial picture and margin improvements.

The market often penalises headline revenue misses, yet these figures indicate an organisation operating with enhanced efficiency. The ability to extract higher earnings from a smaller revenue base signals strong internal cost management.

| Q1 Metric | Wall Street Estimate | Reported Actual |

|---|---|---|

| Adjusted EPS | $0.69 to $0.70 | $0.79 |

| Total Revenue | $1.529 billion | $1.491 billion |

| Adjusted EBITDA | N/A | $151 million |

Federal contract accounting often obscures a firm’s broader organic growth trajectory. The mechanics of classified and confidential contracts in the defence sector mean that sudden conclusions or adjustments can artificially skew overall performance metrics. When a highly classified project shifts in scope, the reported revenue can drop sharply, even if the rest of the business is expanding.

Federal accounting standards grant agencies specific flexibility regarding financial reporting rules for classified programs, allowing them to modify disclosure statements to protect national security interests at the expense of top-line transparency.

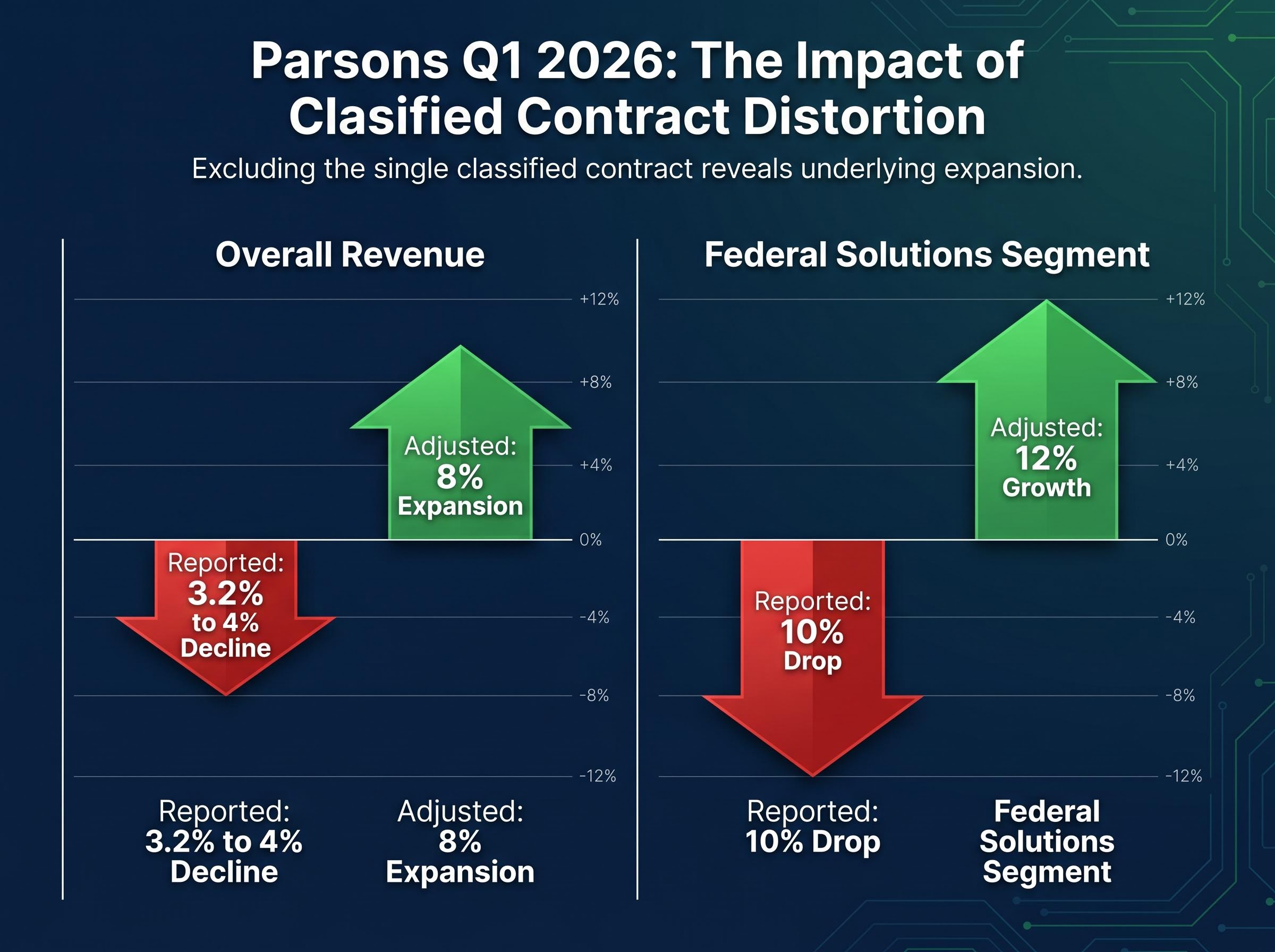

This exact dynamic explains the 3.2-4% overall revenue decline reported by the company. The contraction was strictly tied to a specific confidential contract.

Excluding this isolated project, the baseline operational metrics tell a completely different story.

Overall sales actually expanded by 8% annually when removing the classified distortion, delivering a 3% organic growth rate. The Federal Solutions segment, which houses the Space and Missile Defence portfolio, provides the clearest example of this accounting anomaly.

While the segment officially recorded a steep contraction, the underlying portfolio demonstrated significant expansion. Stripping away these classified distortions gives investors a much more accurate framework for valuing the stock’s actual performance.

Reported Figures: Overall revenue declined by 3.2-4%, with the Federal Solutions segment officially reporting a 10% drop. Adjusted Figures: Excluding the single classified contract, overall sales expanded by 8%, while the Federal Solutions segment grew by 12%.

Headline revenue dips often raise questions about cash burn, but the firm’s operational efficiency highlights an emphasis on capital preservation. The company demonstrated marked improvements in operating cash flow utilisation compared to the previous year. According to company data, operating cash flow utilisation fell to just $4 million, a massive improvement from the $12 million utilised during the equivalent timeframe last year.

This reduced cash burn connects directly to the organisational efficiencies that produced the 10.1% record margins. The firm is maximising its capital and operating leaner, offsetting the temporary top-line pressure. Investors seeking proof of strong internal management can look to this improved cash retention.

The current debt load remains a critical factor in evaluating the firm’s operational durability. Total debt stood at $1.513 billion as of 31 March 2026.

When paired with the reduced cash burn and expanding margins, this debt level appears manageable within the current capital structure. The improved cash flow mechanics ensure the company does not need to burn through reserves to survive a temporary revenue adjustment.

For readers wanting to compare these capital preservation strategies across the sector, our detailed coverage of mid-tier defence contractor financial health evaluates how firms manage project pipeline visibility against their debt obligations.

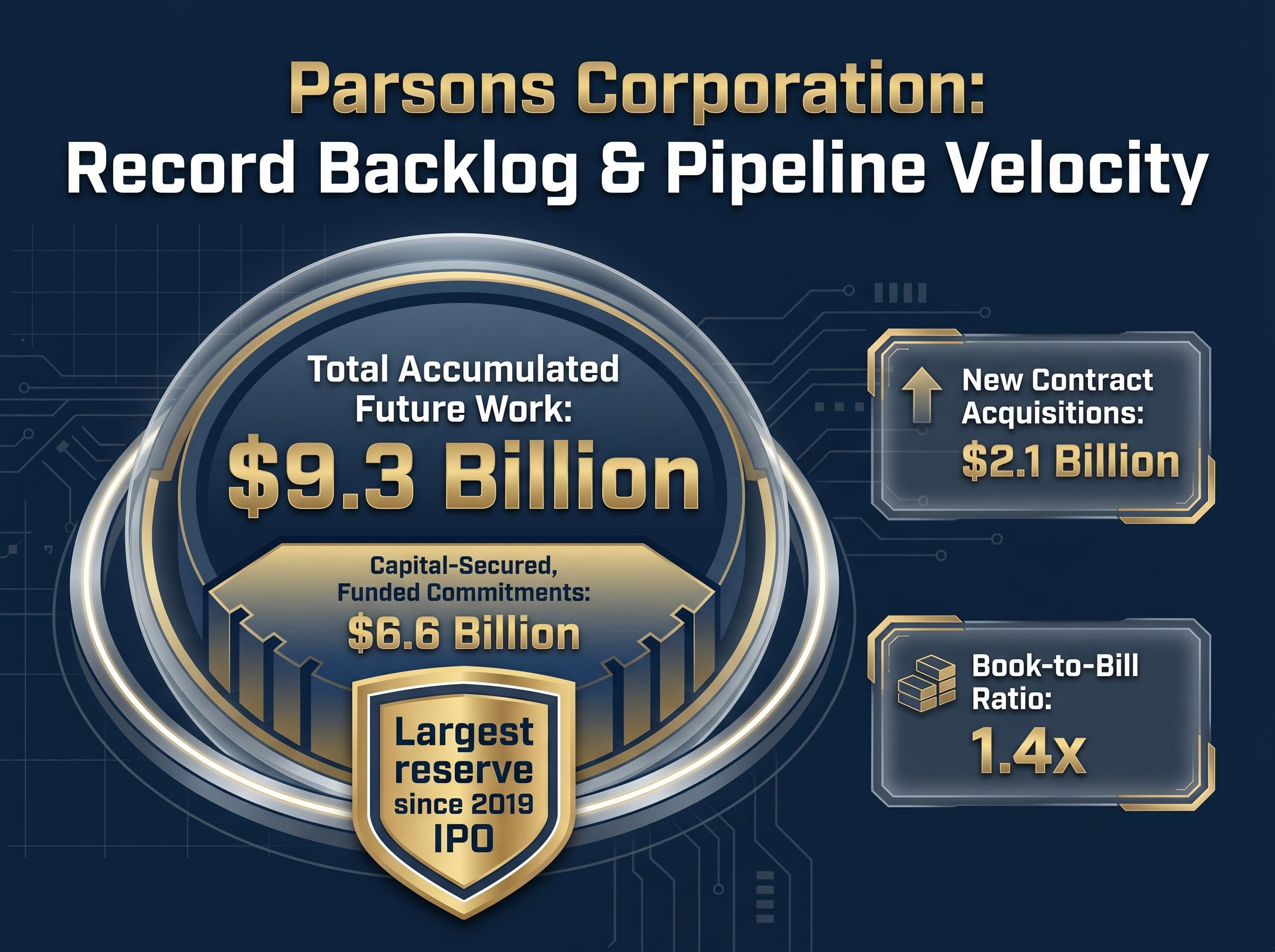

The complexities of the current quarter’s results ultimately give way to the undeniable strength of future revenue visibility. The record backlog stands as the most critical forward-looking indicator in the entire earnings report. A high backlog guarantees future cash flow, allowing investors to assess the long-term stability of the stock value.

According to company data, overall accumulated future work reached an unprecedented $9.3 billion during the quarter. According to company data, within this total, capital-secured, funded project commitments hit $6.6 billion, representing the largest reserve since the firm’s 2019 initial public offering.

Analysts closely monitor these funded obligation metrics because they provide a concrete timeline for when contracted work will convert into actual billing and verifiable cash flow.

This massive reserve of funded projects secures the forward trajectory.

According to company data, the company recorded a 1.4x book-to-bill ratio across its operational segments. This metric means the firm is acquiring new future revenue at 1.4 times the rate it is billing current work, indicating a highly positive revenue replacement rate. According to company data, new contract acquisitions amounted to $2.1 billion over the three-month period.

Recent contract acquisitions further validate the momentum in the classified and federal space. The momentum continued immediately following the quarter’s close, adding substantial future value.

The reaffirmed full-year financial projections provide a final verdict on the firm’s forward positioning. Leadership maintained their Fiscal 2026 guidance, projecting $6.5 billion to $6.8 billion in total revenue. The $6.65 billion guidance midpoint sits slightly beneath the Wall Street consensus, yet the market response remained positive.

Shares experienced a pre-market bump, eventually settling at $51.69, up 0.37%, by mid-afternoon on 29 April 2026. Analyst consensus currently points to a Buy rating, with an average price target of $78.67 and a median target of $72.00.

CEO Commentary “Looking forward, we are very optimistic about our future. There is increasing global demand for both defence and infrastructure. Our ability to deliver operationally relevant solutions with speed, digitally transform our offerings, and leverage non-traditional commercial business models enables us to uniquely meet our customers’ critical needs,” said Carey Smith, Chief Executive Officer.

These projections indicate that leadership expects defence and infrastructure demand to persist. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

The baseline federal budget projections for defence spending suggest a stable long-term funding environment, providing a macroeconomic foundation that supports this anticipated growth trajectory.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Parsons Corporation reported total revenue of $1.491 billion, missing analyst estimates, but achieved an adjusted earnings per share of $0.79, exceeding expectations due to record 10.1% margins.

A specific confidential contract led to a reported 3.2-4% overall revenue decline; however, excluding this distortion, overall sales actually expanded by 8% annually.

The unprecedented $9.3 billion backlog, including $6.6 billion in funded project commitments, signals strong future revenue visibility and long-term stability for the company's stock value.

Parsons demonstrated improved operational efficiency, reducing operating cash flow utilization to just $4 million in Q1 2026, significantly better than the $12 million utilized in the prior year.

Shares experienced a positive reaction to the earnings, and analysts generally maintain a Buy rating with an average price target of $78.67, anticipating continued demand in defence and infrastructure.