Lululemon Fundamental Analysis: the Price of Brand Dilution

3 hrs ago

Understanding the core principles of defence contractor investing requires looking beyond surface-level revenue figures to evaluate long-term pipeline visibility. Parsons Corporation reported its Q1 2026 earnings on 29 April 2026, delivering a compelling contrast between a record contract pipeline and immediate top-line revenue scrutiny. The market reaction to this specific release highlights the complex financial mechanics unique to the sector.

This analysis uses the latest earnings print as a detailed case study for evaluating underlying contract health, funded obligations, and future visibility. Readers will learn how to parse forward-looking indicators when immediate revenue misses short-term expectations. Developing this analytical skill is particularly relevant today. The United States Department of Defense faces a shifting budgetary environment, requiring investors to accurately separate guaranteed revenue from vulnerable government appropriations.

The market response to the latest earnings print from Parsons demonstrates exactly how investors weigh historical profitability against top-line contraction. Heading into late April 2026, the company had experienced a year-to-date share underperformance of approximately 16.17 percent. This downward pressure was driven by an overall unfavourable estimate trend and consensus “Sell” ratings from certain quantitative analysts.

The actual release triggered a mixed reaction across trading desks, as the company reported a slight revenue miss. Total sales came in at $1.5 billion, falling 0.47 percent short of the $1.507 billion expectation. This figure represents a 4 percent annual drop compared to the previous year.

According to market data, despite this top-line decline, shares climbed 3.2 percent in pre-market trading immediately following the print. This upward movement stems from a substantial accumulation of fresh agreements and strong bottom-line outperformance. Adjusted earnings per share reached $0.79, comfortably beating the $0.70 Wall Street consensus estimate.

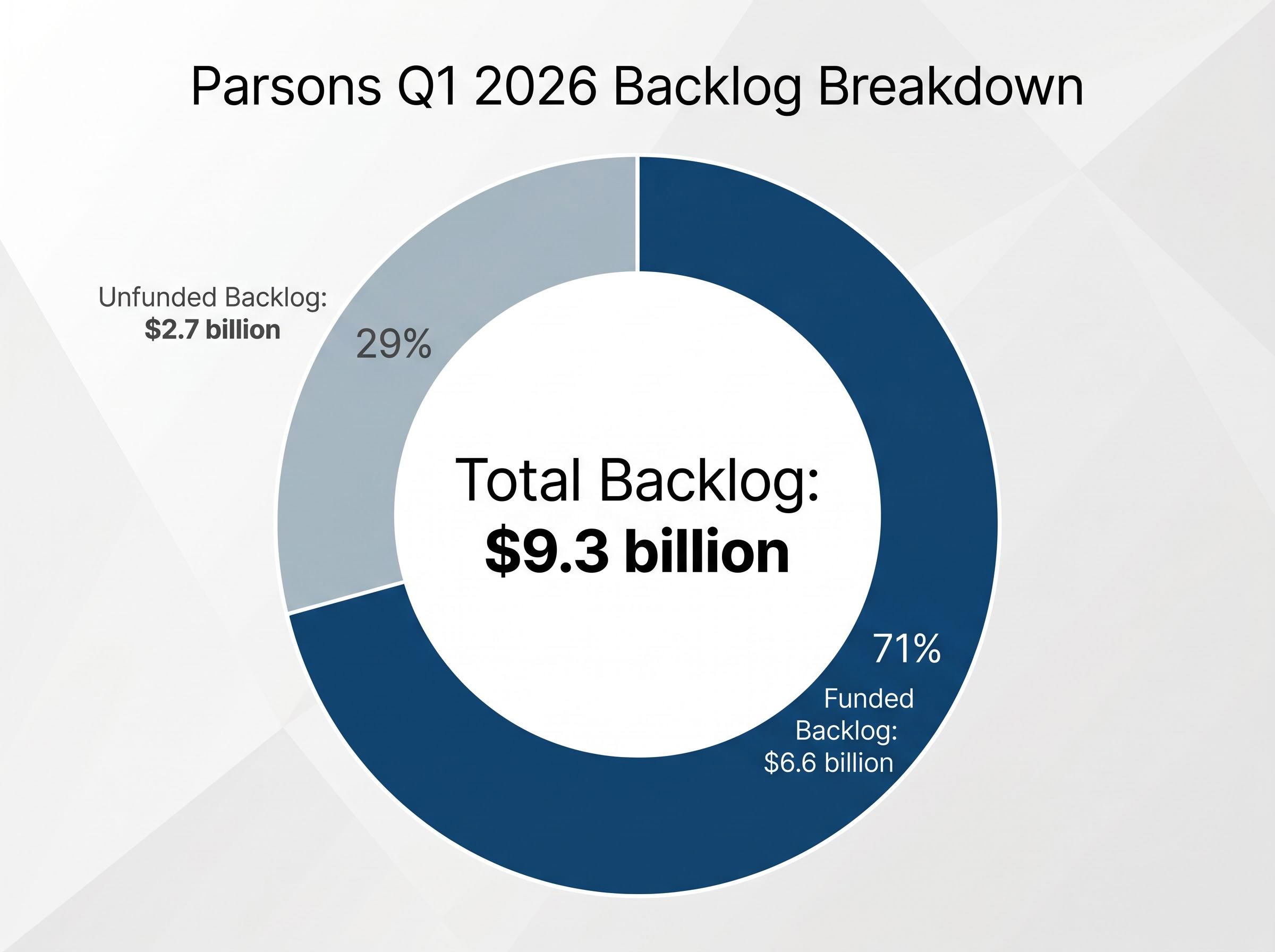

Furthermore, the company secured $2.1 billion in new agreements during the quarter alone. These new contract wins pushed the total future work inventory to a record high of $9.3 billion. According to company data, margin expansion continued despite lower overall net income, with profitability ratios hitting an unprecedented 10.1 percent. According to company data, adjusted EBITDA for the quarter stood firm at $151 million, signalling that the underlying business remains highly efficient.

| Financial Metric | Wall Street Consensus Estimate | Parsons Q1 2026 Actual Result |

|---|---|---|

| Quarterly Revenue | $1.507 billion | $1.5 billion |

| Adjusted Earnings Per Share | $0.70 | $0.79 |

| Total Backlog | Not Specified | $9.3 billion |

According to company data, beneath the headline figures, the company achieved a favourable historical benchmark by minimising operational capital outflows to just $4 million. This capital efficiency serves as a highly positive signal for organisational health. It demonstrates management’s ability to control operational costs and protect margins even when experiencing a temporary top-line contraction.

This efficiency metric is critical when evaluating defence stocks during periods of budgetary uncertainty. A company that can generate high adjusted EBITDA while keeping capital expenditure low demonstrates a highly flexible operating model. This flexibility allows management to redirect cash flows toward strategic acquisitions or share repurchases, returning value to shareholders even when top-line growth stalls.

For investors wanting to explore how this operational efficiency directly impacts valuation, our detailed coverage of Parsons stock profitability metrics unpacks the record adjusted EBITDA performance and margin expansion strategies that offset the recent top-line contraction.

Evaluating sector risks requires a clear understanding of what a future work pipeline actually represents mechanically. The headline total backlog is frequently misunderstood by retail investors, leading to inaccurate assessments of a company’s downside protection. Investors must differentiate between appropriated government funds and anticipated administrative awards.

For Parsons, the record $9.3 billion total backlog splits into two distinct categories that carry vastly different risk profiles. The company successfully secured a post-IPO high of $6.6 billion in financially backed future work during the quarter. The remaining $2.7 billion consists of unfunded obligations that remain strictly contingent on future government allocations.

The primary metrics for evaluating these defence sector pipelines are defined as follows:

Total Backlog: The absolute value of all future work under contract, regardless of whether the relevant government agency has appropriated the specific funds to pay for the operations. Funded Backlog: The secure portion of the total backlog where funding has been officially authorised, allocated, and legally committed by the client for immediate use. Unfunded Backlog: Contracted work that currently lacks budgetary appropriation, carrying a much higher risk of cancellation, scaling back, or delay if government priorities shift. Book-to-Bill Ratio: The ratio of new orders received to existing units billed for a specific financial period, where a score above 1.0 indicates more demand is entering the pipeline than the company is fulfilling.

Parsons reported an impressive 1.4x book-to-bill ratio for the first quarter of 2026. Financial analysts use this specific multiplier to project future cash flows, as it confirms the company is winning new work significantly faster than it is depleting its current active contracts.

A high funded backlog acts as a structural buffer against broader market volatility and political gridlock. Because the $6.6 billion is already backed by appropriated funds, the company possesses guaranteed revenue streams that remain insulated from near-term legislative delays in Washington.

While commercial sectors often experience significant volatility during fragile macroeconomic conditions and periods of declining consumer savings, defence contractors rely on structurally protected government allocations that provide unique defensive characteristics.

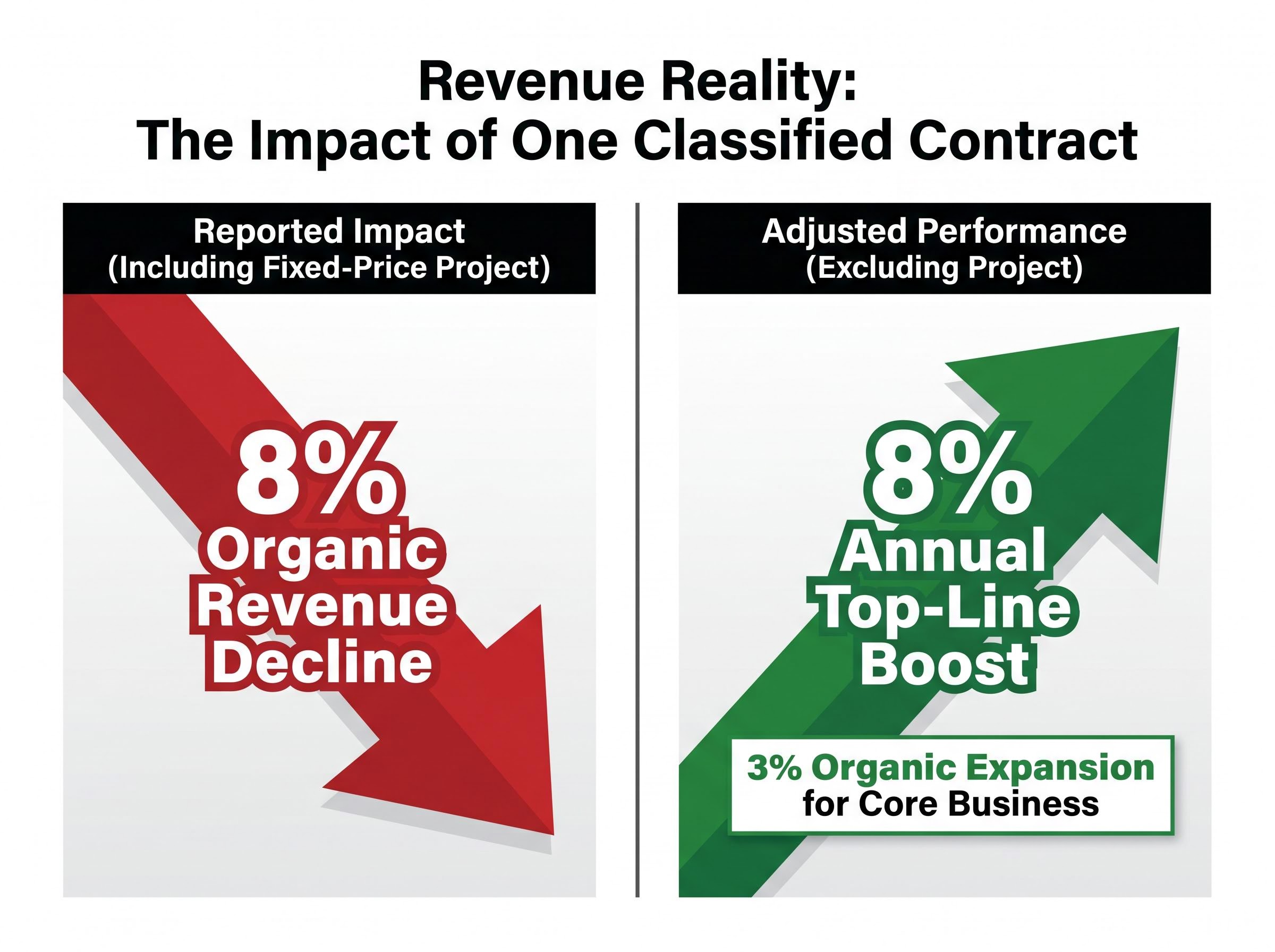

While pipeline optimism supports the long-term outlook, opaque contract variables can create immediate financial headwinds. The 4 percent revenue decline reported in Q1 2026 highlights the double-edged nature of classified, fixed-price defence contracts. These agreements lock in revenue schedules but shift the risk of cost overruns and execution delays entirely onto the corporate contractor.

Government agencies heavily favour these fixed-price structures during tight budgetary periods because they transfer inflation and supply chain risks away from the public sector. Financial analysts continuously scrutinise these specific contract types because a single poorly negotiated fixed-price agreement can compress margins across an entire corporate portfolio.

A formal GAO analysis of fixed-price contracts confirms that while these structures protect public funds from cost overruns, they force corporate entities to absorb the full financial impact of sudden materials inflation or execution delays.

Parsons attributed its 8 percent organic revenue decline primarily to lower volume on one specific fixed-price confidential project. Stripping out this isolated contract anomaly provides a completely different view of the company’s underlying operational health. Without the undisclosed project dragging down the averages, adjusted revenue would have shown an 8 percent annual top-line boost.

This translates to a healthy 3 percent organic expansion for the core business. The classified project also drove a 12 percent fall in operating income during the quarter, which was further compounded by recent acquisition costs. Separating systemic business failure from isolated, project-specific headwinds is a necessary analytical skill when reviewing earnings reports.

Analyst Perspective Fixed-price classified contracts remain a critical investor watch point, as limited public visibility makes it exceptionally difficult to forecast their ongoing impact on revenue growth, profit margins, and cash flow predictability.

Individual company performance metrics carry limited analytical weight without the context of the broader macroeconomic environment. Early 2026 performance across the sector shows consistent demand generation despite tightening fiscal conditions. Comparing pipeline metrics against primary competitors provides a framework for measuring relative valuation and market share.

Booz Allen Hamilton recently reported a book-to-bill ratio of 1.42x alongside a massive $38 billion total backlog. Meanwhile, SAIC reported a 1.3x book-to-bill ratio with an approximate $22.3 billion backlog. Parsons aligns closely with the larger peers in demand generation despite operating with a smaller total backlog size. Further clarity on sector momentum will emerge when Leidos reports its earnings scheduled for 5 May 2026.

| Defence Contractor | Total Pipeline Backlog | Book-to-Bill Ratio | Relative Market Scale |

|---|---|---|---|

| Booz Allen Hamilton | $38.0 billion | 1.42x | Large-cap sector leader |

| SAIC | $22.3 billion | 1.30x | Mid-to-large-cap peer |

| Parsons | $9.3 billion | 1.40x | Mid-cap growth competitor |

Securing these high funded backlogs is particularly urgent given the top-down risk factors currently facing the sector. The Pentagon submitted an $848.3 billion budget request for FY2026. When adjusted for inflation, this figure represents a functional budget cut compared to previous fiscal years.

Total United States national defence spending was projected at approximately $919.2 billion for FY2025. The FY2026 budget cycle focuses heavily on reconciliation funding and an overarching strategic emphasis on countering global threats, particularly in Asia. Broader projections suggest total national security spending could reach up to $1.05 trillion when including atomic energy programmes.

The official Department of Defense FY2026 budget request details how these allocation priorities support specific theatre commands, confirming that future government appropriations will heavily favour contractors positioned to deliver modernised deterrence technologies.

The strategic emphasis on countering these threats requires contractors to continuously invest in advanced technology and modernised engineering capabilities. Companies that successfully align their project pipelines with these specific strategic priorities are more likely to see their unfunded obligations convert into funded backlogs. These constraints increase the threat of appropriations delays, ensuring companies with outsized funded obligations are best positioned to maintain operations while competitors wait for new government allocations.

The Q1 2026 earnings release from Parsons demonstrates that top-line misses can serve as temporary noise if funded backlogs demonstrate structural demand. Strong book-to-bill ratios indicate that future revenue streams are actively expanding despite isolated project headwinds.

Analysts evaluating the broader sector regularly look beyond statutory net income declines, recognising that adjusted per-share metrics often provide a more accurate reflection of underlying cash generation and operational success.

When evaluating the next sector earnings print, investors should look for three specific confirmation signals. First, assess the ratio of funded obligations versus unfunded backlog to measure actual revenue security. Second, verify that the book-to-bill ratio remains consistently above the 1.0 threshold across multiple consecutive quarters.

Finally, calculate the organic revenue growth rate by stripping out the impact of isolated fixed-price contracts. This adjusted figure reveals whether the core business is actually contracting or simply absorbing a single unprofitable project. The final proof point of pipeline strength translating to future performance is the company’s reaffirmed full-year outlook.

Parsons maintained its FY2026 guidance, projecting $6.5 to $6.8 billion in total revenue. The company also projects $615 to $675 million in adjusted EBITDA for the year. These statements are speculative and subject to change based on market developments and company performance.

Past performance does not guarantee future results, as financial projections are subject to market conditions and various risk factors.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

A funded backlog represents future work where funding has been officially authorized and committed by the client, providing guaranteed revenue streams. An unfunded backlog consists of contracted work that lacks budgetary appropriation, carrying a higher risk of cancellation or delay if government priorities shift.

Parsons reported Q1 2026 revenue of $1.5 billion, a slight miss, but achieved adjusted earnings per share of $0.79, comfortably beating estimates. The company secured a record $9.3 billion total backlog and maintained a 10.1 percent profitability ratio.

A book-to-bill ratio above 1.0, such as Parsons' 1.4x in Q1 2026, signifies that the company is winning new work significantly faster than it is completing its current active contracts. This indicates expanding future revenue streams and strong demand generation.

Fixed-price classified contracts transfer the risk of cost overruns and execution delays to the contractor, potentially compressing margins if inflation or supply chain issues arise. Limited public visibility also makes forecasting their ongoing impact on revenue and profit margins challenging.

Investors should assess the ratio of funded versus unfunded backlog for revenue security, verify consistent book-to-bill ratios above 1.0, and calculate organic revenue growth by isolating impacts from specific fixed-price contracts to understand core business health.