The $30 Oil Gap That Holds the Inflation Outlook Hostage

3 hrs ago

Regeneron Pharmaceuticals reported a strong double-digit beat on both its top and bottom lines for the first quarter of 2026, sending its stock higher in pre-market trading on 29 April 2026. The latest Regeneron earnings results delivered total revenues of $3.6 billion, comfortably exceeding Wall Street expectations. This performance was anchored by massive growth in its blockbuster immunology franchise and calculated transitions within its ophthalmology portfolio.

Investors reacting to the morning release are closely examining how the company navigated operational challenges to post a 19 percent year-over-year revenue increase. The financial report demonstrates how strategic drug lifecycle management and lucrative collaboration agreements continue to drive corporate profitability. Readers will learn how these specific immunology sales, combined with aggressive capital allocation decisions, shape the company’s financial trajectory for the remainder of the year.

The company’s financial performance established a baseline of immediate corporate strength, outpacing market consensus across critical metrics. Total revenues for the first quarter of 2026 reached $3.6 billion, marking a 19 percent increase from the $3.029 billion recorded in the same period last year. This result easily cleared analyst forecasts of $3.4479 billion.

Non-GAAP earnings per share came in at $9.47, representing a 15 percent year-over-year expansion and beating Wall Street expectations of $9.10. The bottom-line outperformance occurred despite a significant accounting headwind. The company absorbed a $102 million pre-tax In-Process Research and Development charge, which stemmed from equity premiums and collaboration payments.

This research charge created a $0.80 negative impact on the non-GAAP earnings per share. GAAP earnings per share stood at $6.75, experiencing a slight contraction compared to the previous year due to these same operational costs.

Managing operational costs remains a priority across the healthcare sector, prompting some drug developers to launch direct-to-patient pharmacy platforms that bypass traditional middlemen and capture higher distribution margins.

| Metric | Q1 2026 Actuals | Analyst Estimates | Q1 2025 Actuals |

|---|---|---|---|

| Total Revenue | $3.6 billion | $3.4479 billion | $3.029 billion |

| Non-GAAP EPS | $9.47 | $9.10 | $8.23 |

The sheer scale of the immunology growth engine provided the primary catalyst for the revenue outperformance. Global net sales for Dupixent surged to $4.9 billion, representing a 33 percent increase compared to the previous year. This commercial momentum translated directly into lucrative returns from the company’s partnership with Sanofi, generating collaboration revenue that increased 36 percent to $1.605 billion.

The oncology franchise demonstrated parallel domestic and international expansion. Global net sales for Libtayo achieved $438 million, an impressive 54 percent year-over-year jump. The domestic market anchored this performance, with US net sales accounting for $286 million, or a 49 percent increase. These figures prove the core commercial assets remain highly resilient and are actively capturing wider market share.

CEO Commentary “Achieved strong double-digit growth on top and bottom lines while investing in nearly 50 product candidates; entered U.S. government agreement for Most-Favored-Nation Pricing on certain products and future medicines, promoting balanced pricing with other developed nations,” said Leonard Schleifer, Chief Executive Officer.

The administration’s recent White House pricing fact sheet details how this Most-Favored-Nation framework will reduce Medicaid costs for specific cardiovascular treatments like Praluent, signaling a broader shift in government contracting for biopharmaceuticals.

Pharmaceutical companies face significant revenue risks when highly profitable medications approach the end of their patent protection. To manage this impending biosimilar competition, drug developers often introduce next-generation formulations designed to transition patients before generic alternatives enter the market. This process creates a period of deliberate self-cannibalisation, where a company intentionally sacrifices sales of its older drug to build market share for its new, patent-protected replacement.

Beyond managing biosimilar competition for established products, the biotechnology sector is actively pursuing novel vision preservation treatments, with companies securing regulatory alignment for therapies targeting rare genetic blinding diseases that currently have no approved options.

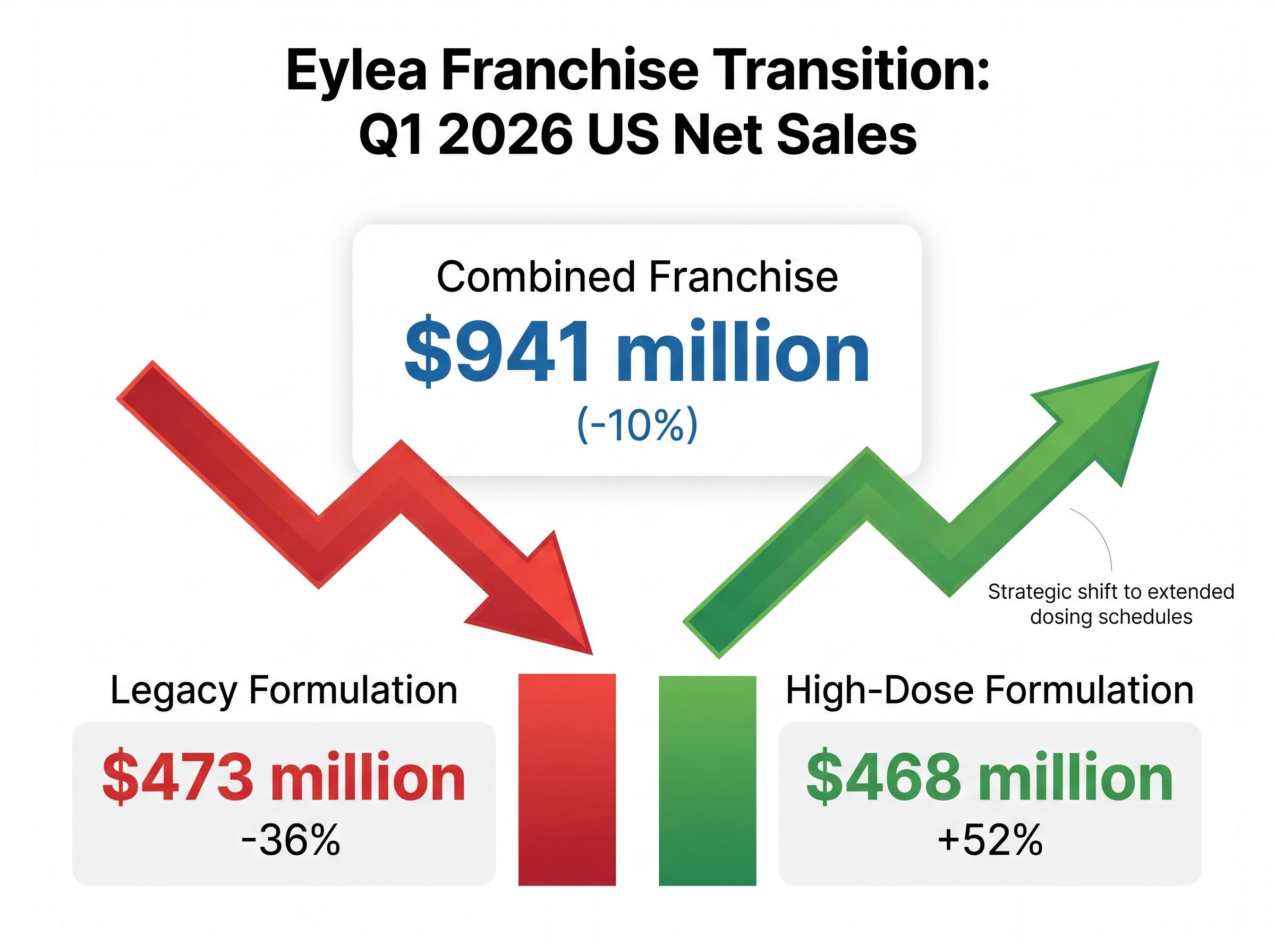

The Eylea franchise is currently navigating this exact lifecycle transition. Total US net sales for the combined vision treatment portfolio dropped 10 percent to $941 million during the first quarter. However, this headline decline masks a highly successful transition strategy occurring beneath the surface. Legacy US sales deliberately dropped 36 percent to $473 million, while the new high-dose formulation surged 52 percent to reach $468 million.

Recent regulatory wins have accelerated this patient migration strategy. The Food and Drug Administration (FDA) recently approved extended dosing schedules for the high-dose formulation based on positive data from the PULSAR and PHOTON clinical trials. This approval provides a competitive advantage over legacy treatments by reducing the frequency of patient injections, supporting the strategic replacement of the older asset.

| Product Category | Q1 2026 US Net Sales | Year-Over-Year Change |

|---|---|---|

| Combined Franchise | $941 million | -10% |

| High-Dose Formulation | $468 million | +52% |

| Legacy Formulation | $473 million | -36% |

Operational realities within global supply chains occasionally interrupt broader corporate momentum. During the first quarter, the company experienced a temporary interruption of bulk manufacturing at its facility in Limerick, Ireland, due to unanticipated repair requirements. Management confirmed that this production halt did not impact commercial product availability, and operations resumed normally in the second quarter.

However, the interruption carried tangible accounting consequences. The combination of discarded inventory and unabsorbed overhead costs negatively affected GAAP gross margins. This physical supply chain disruption directly forced a revision in forward-looking profitability metrics, specifically on a GAAP basis.

The updated full-year margin guidance reflects this specific manufacturing hurdle:

GAAP Gross Margin Guidance: Lowered to 77 to 78 percent for the full year of 2026, down from prior estimates of 79 to 80 percent. Non-GAAP Gross Margin Guidance: Remains entirely unchanged at 83 to 84 percent, indicating the underlying business model remains intact despite the physical production delay.

For investors wanting to understand how these manufacturing hurdles and associated costs influence broader financial models, our detailed coverage of Regeneron’s margin pressures examines the strategic implications of the GAAP profitability revision and its impact on full-year valuation metrics.

Management signalled intense conviction in the company’s valuation through an aggressive stock buyback strategy executed throughout the first quarter. The company repurchased $803 million in common stock, effectively shrinking the outstanding share count to consolidate shareholder value. Building on this momentum, the board authorised a massive new $3.0 billion share repurchase programme in April 2026.

Executing capital returns of this magnitude requires strict compliance with SEC safe harbor provisions, which dictate specific daily timing and volume limits to ensure market stability during the ongoing purchase period.

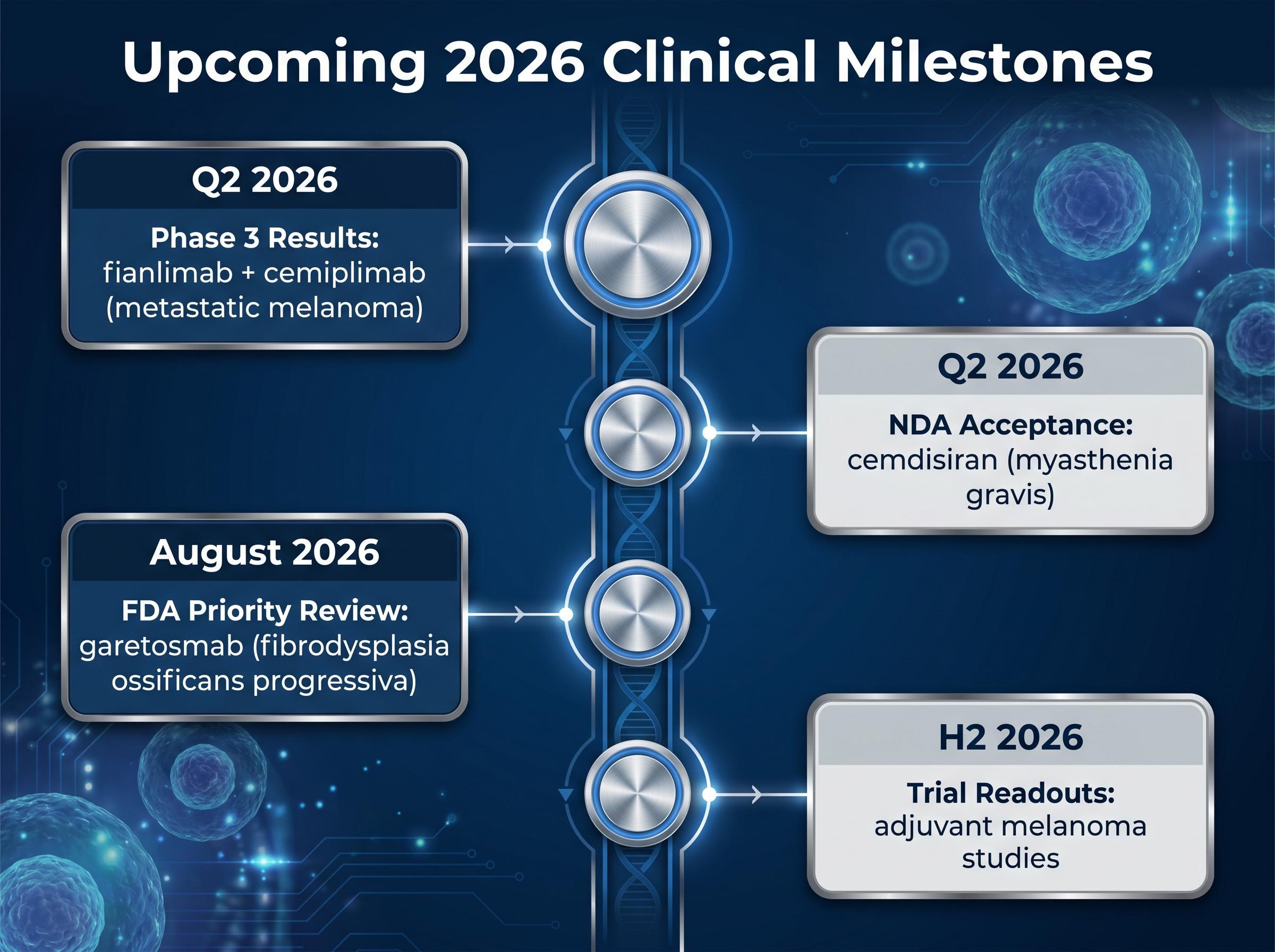

These substantial capital return manoeuvres are directly supported by an advancing clinical portfolio. The aggressive share reduction suggests internal confidence that the upcoming trial data readouts will structurally increase corporate value over the remainder of the year.

The remaining months of 2026 hold several specific regulatory and trial catalysts expected to drive market sentiment:

The 19 percent top-line growth achieved in the first quarter demonstrates that the company can successfully expand its blockbuster immunology portfolio while managing complex ophthalmology product transitions. Generating $3.6 billion in revenue provides the financial flexibility required to absorb temporary manufacturing interruptions without altering long-term commercial trajectories.

The newly authorised $3.0 billion share buyback serves as a clear signal of internal stability and management confidence. As the year progresses, Wall Street sentiment will likely shift focus toward the upcoming clinical data releases and regulatory decisions. The combination of strong baseline cash flow and an advancing pipeline positions the company to maintain its competitive advantage across multiple therapeutic categories.

This internal stability is further reinforced when pharmaceutical developers successfully navigate postmarketing compliance obligations, as the removal of burdensome regulatory study requirements can substantially reduce future operational costs and validate a drug’s long-term safety profile.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Regeneron reported total revenues of $3.6 billion, marking a 19 percent year-over-year increase, and non-GAAP earnings per share of $9.47, a 15 percent expansion from the prior year.

Dupixent's global net sales surged 33 percent to $4.9 billion, and Libtayo's global net sales jumped 54 percent to $438 million, collectively fueling Regeneron's top-line performance.

Regeneron is executing a lifecycle transition by deliberately shifting patients from the legacy Eylea formulation to a new high-dose version, which saw a 52 percent sales increase, to manage impending biosimilar competition.

Regeneron lowered its GAAP gross margin guidance to 77-78 percent due to a temporary manufacturing interruption at its Limerick facility, which caused discarded inventory and unabsorbed overhead costs.

Regeneron repurchased $803 million in common stock during Q1 and authorized a new $3.0 billion share repurchase program in April 2026, signaling strong management confidence in the company's valuation.