Intel Stock Surges 10% to Record High on Apple Chip Deal

25 mins ago

The year 2026 has shifted electric aviation from a theoretical concept into an immediate operational reality. Active commercial flights and multi-billion-dollar market capitalisations now define the sector. Investors evaluating the current market for electric vertical takeoff and landing equities, commonly referred to as eVTOL stocks, must navigate a highly complex transition phase.

Companies like Joby Aviation, Archer Aviation, and Vertical Aerospace are rapidly advancing toward regulatory approval and passenger launches across global jurisdictions. These organisations face intense capital pressures alongside divergent strategic paths to reach commercialisation. What follows is a comprehensive analytical framework to assess these aerospace entities based on cash burn, business integration, and commercial launch viability.

The financial dichotomy of 2026 highlights a clear transition from early market enthusiasm to strict operational execution. Downward pressure on equity valuations has heavily impacted early entrants throughout the current calendar year. This reality contrasts sharply with the positive momentum of newly funded or freshly public competitors navigating similar aerospace certification pathways.

Ongoing capital injections remain the primary survival metric for companies executing complex manufacturing blueprints. Investors face an environment of high capital expenditure where a company’s available liquidity directly indicates its ability to survive the certification process. Market capitalisation disparities recorded in late April 2026 reflect which operators possess the financial runway to sustain manufacturing scale-up.

| Company | Market Capitalisation | Year-to-date Performance | Recent Capital Action | Core Focus |

|---|---|---|---|---|

| Joby Aviation | $8.9 Billion | -20.0% | Q4 2025 Earnings Finalised | Integrated Passenger Network |

| Archer Aviation | $4.4 Billion | -22.3% | Strategic Municipal Funding | Piloted Passenger Aircraft |

| Beta Technologies | $3.5 Billion | +44.8% | Initial Public Offering | Cargo and Medical Logistics |

| Vertical Aerospace | $299 Million | +55.9% | $850 Million Financing Package | Specialised Fabrication |

Analyst Perspective on Capital Requirements “The transition from prototype to commercial operation requires unprecedented liquidity. The current market heavily penalises manufacturers that fail to secure long-term funding before entering the final, most expensive stages of passenger certification.”

The substantial market disparities provide clear signals regarding investor confidence. The $850 million financing secured by Vertical Aerospace on 20 April 2026 demonstrates how targeted capital raises can trigger immediate stock momentum. Conversely, companies trading at lower valuations without recent capital injections face higher structural risk profiles.

Detailed analysis of the Vertical Aerospace funding package reveals that these substantial capital injections are strategically structured to bridge the liquidity gap between late-stage prototype testing and final passenger-rated certification.

Evaluating electric flight requires distinguishing clearly between aircraft manufacturing and network operation. Operating as an original equipment manufacturer requires massive upfront costs associated with aerospace certification and proprietary facility construction. Running a fully integrated passenger transportation network adds an entirely different layer of ongoing operational expenditure.

General industry projections indicate that reaching financial self-sustainability remains a long-term goal, frequently targeting the 2030 horizon. The capital requirements for passenger-rated certification are significantly higher than those needed for alternative use cases. By grasping these underlying cost structures, observers can better evaluate why certain companies burn cash faster than others.

Optimising power consumption remains a major technical hurdle during this phase, and innovations in commercial drone battery endurance technologies demonstrate how edge-AI processing can significantly extend aircraft mission durations without adding expensive, heavy battery payloads.

Specific cost burdens vary significantly across the two primary operational phases:

Manufacturing Phase Costs: Proprietary engineering research, battery system validation, aerospace certification testing, and physical fabrication facility construction. Network Operation Phase Costs: Vertiport infrastructure development, ongoing pilot compensation, local traffic coordination software, and fleet maintenance.

This economic reality dictates that business models offering the clearest path to profitability are those that carefully stage these expenditures. Companies attempting to fund both phases simultaneously face the highest capital burn rates in the sector.

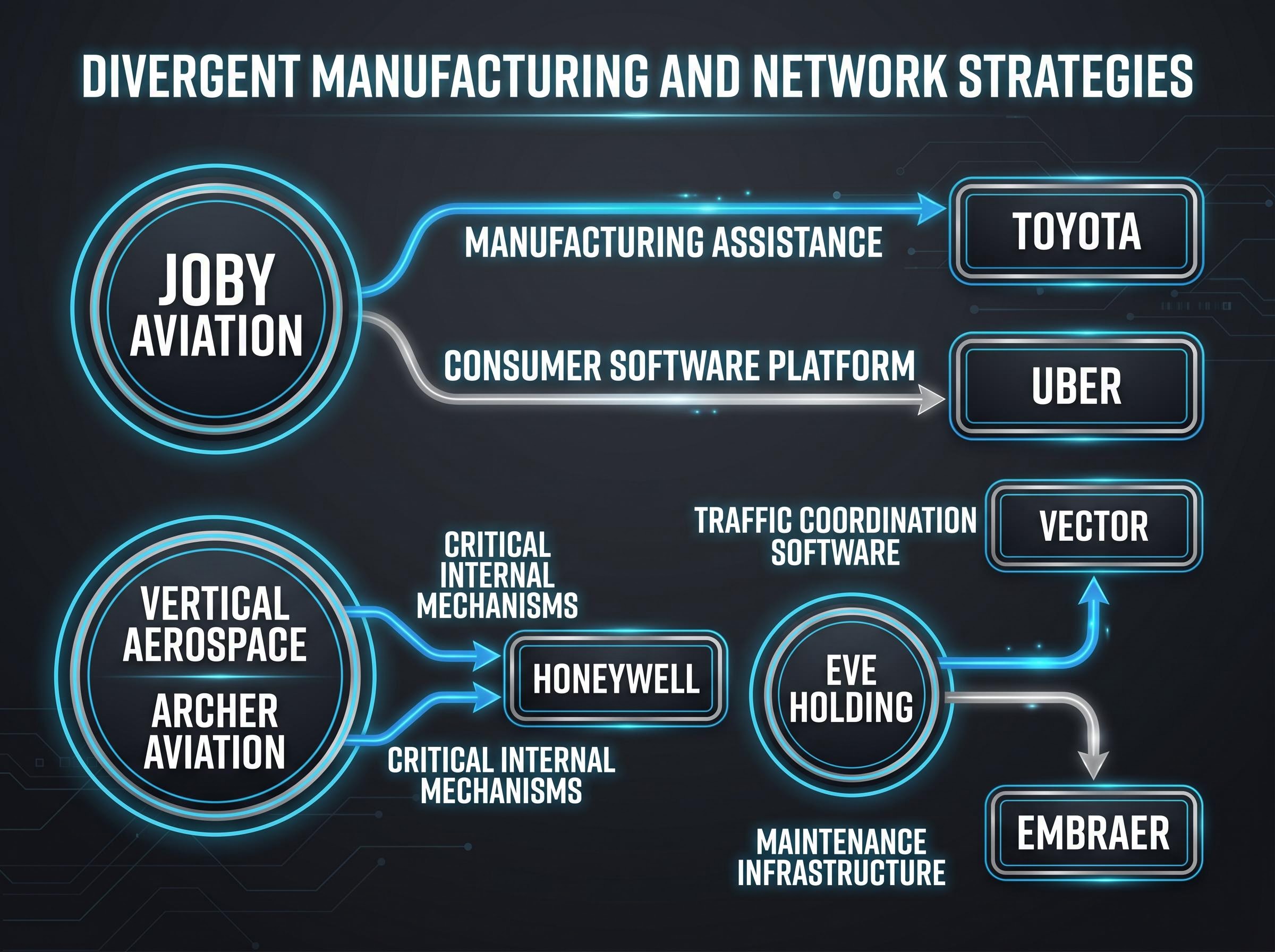

Corporate strategy directly impacts cash runway and certification risk across the sector. Highly integrated business models require immense short-term capital but provide long-term operational control over the final network. Strategies relying on established aerospace supply chains attempt to reduce early financial burn by purchasing critical internal mechanisms from experienced partners.

Joby Aviation pursues a highly comprehensive approach, utilising manufacturing assistance from Toyota and building a consumer software platform alongside Uber. Vertical Aerospace and Archer Aviation focus instead on purchasing critical internal mechanisms from established suppliers like Honeywell. Eve Holding combines physical manufacturing with its Vector traffic coordination software while relying heavily on maintenance infrastructure from Embraer.

These divergent strategies allow investors to align their portfolios with either high-risk integration models or specialised, partnership-reliant frameworks.

Removing the pilot from the cockpit entirely represents a structural shift in aviation economics. Wisk Aero focuses exclusively on engineering self-navigating aircraft to remove ongoing crew salaries from the long-term operational equation. Their Generation 6 aircraft continues active testing throughout 2026.

This approach shifts the financial burden from ongoing pilot compensation to upfront software development and regulatory friction. The autonomous strategy requires navigating a highly complex certification process. This extends the timeline before commercial passenger revenue can materialise, requiring deep capital reserves to sustain the operation.

The shift toward pilotless flight extends beyond passenger transport into logistics and industrial applications, where advancements in autonomous drone navigation are already unlocking complex commercial use cases without relying on traditional GPS infrastructure.

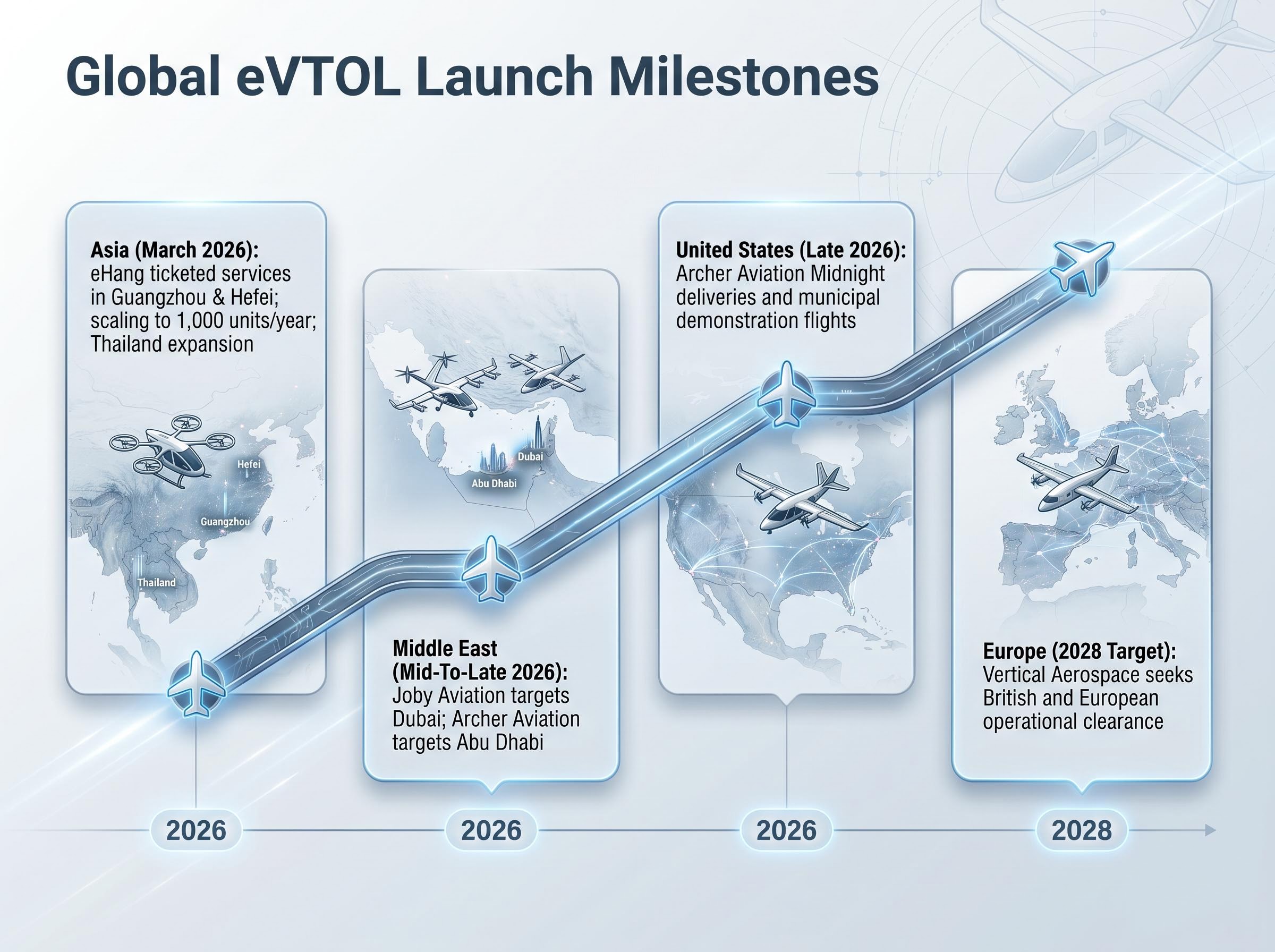

Initial launch markets have shifted distinctly toward the Middle East and Asia, driven by supportive regulatory environments and proactive infrastructure investments. Monitoring these specific geographic launches provides tangible proof of concept for unproven technologies. These milestones serve as the most significant catalysts for future stock price movements.

Domestic Chinese operations have already crossed the threshold into routine commercial service. This contrasts sharply with the longer timelines expected for European and American regulatory approvals. These statements are speculative and subject to change based on market developments and company performance.

The major global launch milestones sequence chronologically across key regions:

Meeting these regional milestones requires strict compliance with the EASA advanced air mobility regulations, which establish the foundational certification criteria for piloted electric aircraft operating within European airspace.

The success of these operational launches will heavily influence investor confidence globally. Delays in any specific region could severely impact the valuation of the associated manufacturer.

Non-passenger revenue streams provide a vital structural hedge against stringent passenger certification delays. A strategic pivot toward freight logistics generates early revenue while core passenger technologies mature. Producing conventional electric aircraft alongside vertical takeoff models broadens the addressable market and accelerates commercial deployment.

Beta Technologies leads this diversification by engineering conventional and vertical aircraft for cargo operators like Air New Zealand, United Therapeutics, and UPS. According to company data, financial forecasts for the company predict $971 million in available liquid assets by the end of 2026. Their strong post-IPO momentum validates the market preference for alternative revenue pathways.

Component distribution and charging network operations offer stable, recurring revenue channels. Beta Technologies operates universally compatible charging networks and actively distributes internal propulsion mechanisms to competitor Eve Holding. Companies with diversified revenue streams present a structurally lower risk profile, as they avoid total dependence on high-stakes passenger certification outcomes.

For investors exploring how aerospace manufacturers secure early cash flow through defence sector diversification, our detailed coverage of military drone propulsion contracts examines how tactical UAV engine agreements can provide stable recurring revenue while passenger technologies mature.

The relationship between current capital reserves and international certification timelines dictates sector survival. The window for unproven concepts has officially closed, with the market now strictly rewarding tangible operational milestones and sustainable liquidity. Observing cash burn rates alongside upcoming regulatory decisions remains a required practice over the next 12 to 24 months.

Companies possessing diversified revenue streams and confirmed launch dates are structurally positioned to outlast highly speculative competitors. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The eVTOL market in 2026 is defined by a transition from theoretical concepts to immediate operational reality, featuring active commercial flights and multi-billion-dollar market capitalizations, which requires strict operational execution.

High capital expenditure means a company's available liquidity directly indicates its ability to survive the certification process, with the market heavily penalizing manufacturers that fail to secure long-term funding for expensive final stages.

Beta Technologies leads diversification by engineering conventional and vertical aircraft for cargo operators like Air New Zealand and UPS, while other companies secure early cash flow through defence sector diversification and charging network operations.

Initial commercial launches in 2026 are targeting Asia, with eHang initiating services in China, and the Middle East, with Joby Aviation and Archer Aviation planning operations in Dubai and Abu Dhabi within the calendar year.