Starbucks Builds AI Tools to Drop Microsoft, IBM and Oracle Apps

2 hrs ago

A stark divergence defined the latest Regeneron earnings report released on 29 April 2026. The biotechnology firm delivered a robust $3.6 billion first-quarter revenue beat, yet financial markets immediately focused on an unexpected drop in gross product margins. This gap between top-line commercial success and underlying profitability pressures reveals how the company is managing current industry dynamics.

The ophthalmology sector is facing intense competitive pressures, and global supply chains remain sensitive to the slightest manufacturing disruptions. The market’s reaction hinges on how effectively the company can balance these domestic headwinds with international joint venture strength.

Investors require a clear understanding of how management intends to deploy its massive capital reserves to offset margin compression. By leveraging aggressive stock repurchases alongside the explosive growth of its immunology portfolio, the firm aims to bridge the gap between temporary operational friction and long-term pipeline development.

The core financial narrative of the first quarter is one of top-line acceleration outperforming consensus models. Total corporate revenue climbed, representing a 19% year-over-year increase. This robust performance comfortably bypassed the $3.45 billion projected by Wall Street analysts prior to the release.

Adjusted per-share profits followed this upward trajectory, eclipsing consensus forecasts by fifty cents. However, the underlying cost of delivering this revenue has steepened considerably. The company reported a sharp decline in GAAP gross product margins, which dropped from 81% in the prior year period.

The official SEC quarterly filing disclosures provide the granular breakdown of these manufacturing costs, allowing investors to track how specific facility disruptions flow directly into the consolidated financial statements.

| Financial Category | Q1 2026 Actuals | Q1 2025 Actuals | Q1 2026 Consensus |

|---|---|---|---|

| Total Revenue | $3.6 billion | $3.02 billion | $3.48 billion |

| Adjusted EPS | $9.47 | Not Disclosed | $8.97 |

| GAAP Gross Margin | 76% | 81% | Not Disclosed |

The initial stock market reaction reflected a calculated absorption of these mixed financial signals. The stock valuation climbed 1.4% immediately following the announcement, as institutional investors priced in the revenue beat alongside the operational hiccups.

Management adjusted their full-year profitability projections downward to reflect ongoing operational and supply chain realities. The modified full-year GAAP gross margin projection now sits at 77% to 78%, representing a noticeable step down from the previous guidance of 79% to 80%.

Wall Street analysts are actively recalibrating their forward models to account for this revised profitability guidance. The fundamental question for portfolio managers is whether these margin pressures are a structural flaw in the manufacturing base or a purely transitional phase.

Gross margins in biotechnology measure the direct profitability of a therapeutic product before broader research and administrative costs are deducted. When physical manufacturing encounters friction, these margins compress rapidly.

Recent supply chain dynamics illustrate this mechanical relationship clearly. While unified industry research confirms the company’s Limerick, Ireland facility is fully operational without halts in 2026, there are no gross margin impacts.

A temporary halt in manufacturing triggers a specific, unavoidable cascade of financial consequences:

Elevated Inventory Write-offs: Batches of complex biologic therapeutics that fail to complete the manufacturing cycle during a shutdown must be discarded. These discarded batches are written off as total financial losses. Unabsorbed Operational Expenses: Fixed facility costs, such as specialised labour and clean-room maintenance, continue accruing even when output volumes drop. This increases the per-unit cost of the remaining usable inventory. * Margin Dilution: The combination of lost inventory and steady fixed costs mechanically lowers the gross product margin for the quarter in which the products are eventually sold.

Management expectations suggest these profitability constraints will persist through the near term. Standard output volumes must return fully before the fixed cost base is efficiently absorbed later in the year.

The relationship between facility utilization and profitability remains an industry-wide dynamic; successful API manufacturing growth often translates directly into rapid earnings improvements by efficiently absorbing those steep underlying operating expenses.

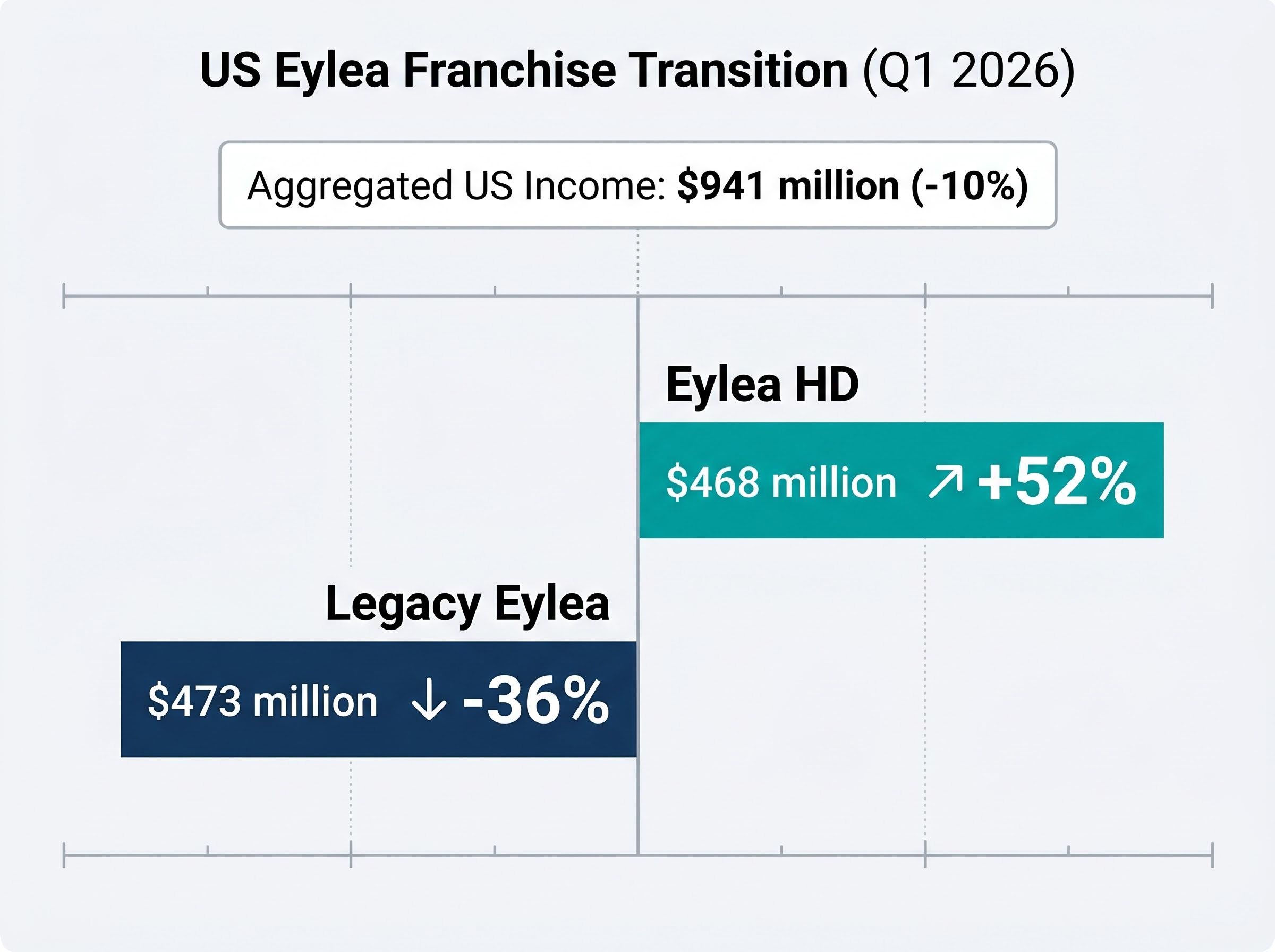

The ophthalmology portfolio remains a critical battleground for domestic market share and long-term cash flow generation. The ongoing transition from the legacy treatment to the newer high-dose formulation is accelerating, creating a complex commercial cannibalisation curve.

Aggregated domestic income for both Eylea variants dropped 10% to $941 million during the first quarter. This contraction masks a rapid rotation beneath the surface, where the newer formulation is actively racing against the structural decline of the legacy product. Legacy Eylea medication revenues dropped 36% to $473 million, reflecting intense biosimilar competition and broader market saturation.

Conversely, the Eylea HD formulation experienced a massive 52% revenue jump, demonstrating strong physician adoption.

| Product Formulation | Q1 2026 US Sales | Year-over-Year Growth Rate |

|---|---|---|

| Eylea HD | $468 million | +52% |

| Legacy Eylea | $473 million | -36% |

The company secured a crucial defensive moat in April 2026 when the Food and Drug Administration (FDA) approved extended dosing parameters. The regulatory agency approved Eylea HD for up to 20-week dosing intervals based on efficacy data from the PULSAR and PHOTON clinical trials. This extended schedule provides a distinct clinical advantage over standard biosimilar dosing routines, serving as a critical tool for retaining market share amid intensifying competitive pressures.

Investors exploring emerging clinical developments in the broader ophthalmology sector will find our detailed coverage of the PYC Therapeutics ADOA program highly relevant, as it examines early Phase 1A efficacy data for a disease-modifying candidate targeting blinding conditions with no currently approved treatments.

While the domestic ophthalmology transition presents distinct commercial headwinds, the company’s immunology joint venture provides unambiguous financial ballast. The Sanofi partnership operates as the fundamental growth engine stabilising the broader commercial portfolio.

Worldwide Dupixent commercialisation jumped 33%, demonstrating exceptional clinical demand across multiple indications. Income derived specifically from the Sanofi collaboration expanded by 36% to $1.6 billion. This massive influx of collaborative revenue effectively offsets the contraction within the Eylea franchise, insulating the balance sheet from singular therapeutic risks.

Strategic Focus “The continued expansion of our collaborative pipeline provides essential cash flow, allowing us to absorb transitional margin pressures while maintaining aggressive reinvestment in our portfolio of fifty distinct therapeutic candidates,” according to corporate strategy statements.

This diversified revenue architecture proves to investors that the firm is not overly reliant on a single therapeutic area for its long-term financial health.

Beyond established commercial joint ventures, the firm continues to secure early-stage assets, recently committing up to $2.1 billion in a Regeneron radiopharmaceutical partnership with Telix Pharmaceuticals to explore biologics-based treatments for solid tumours.

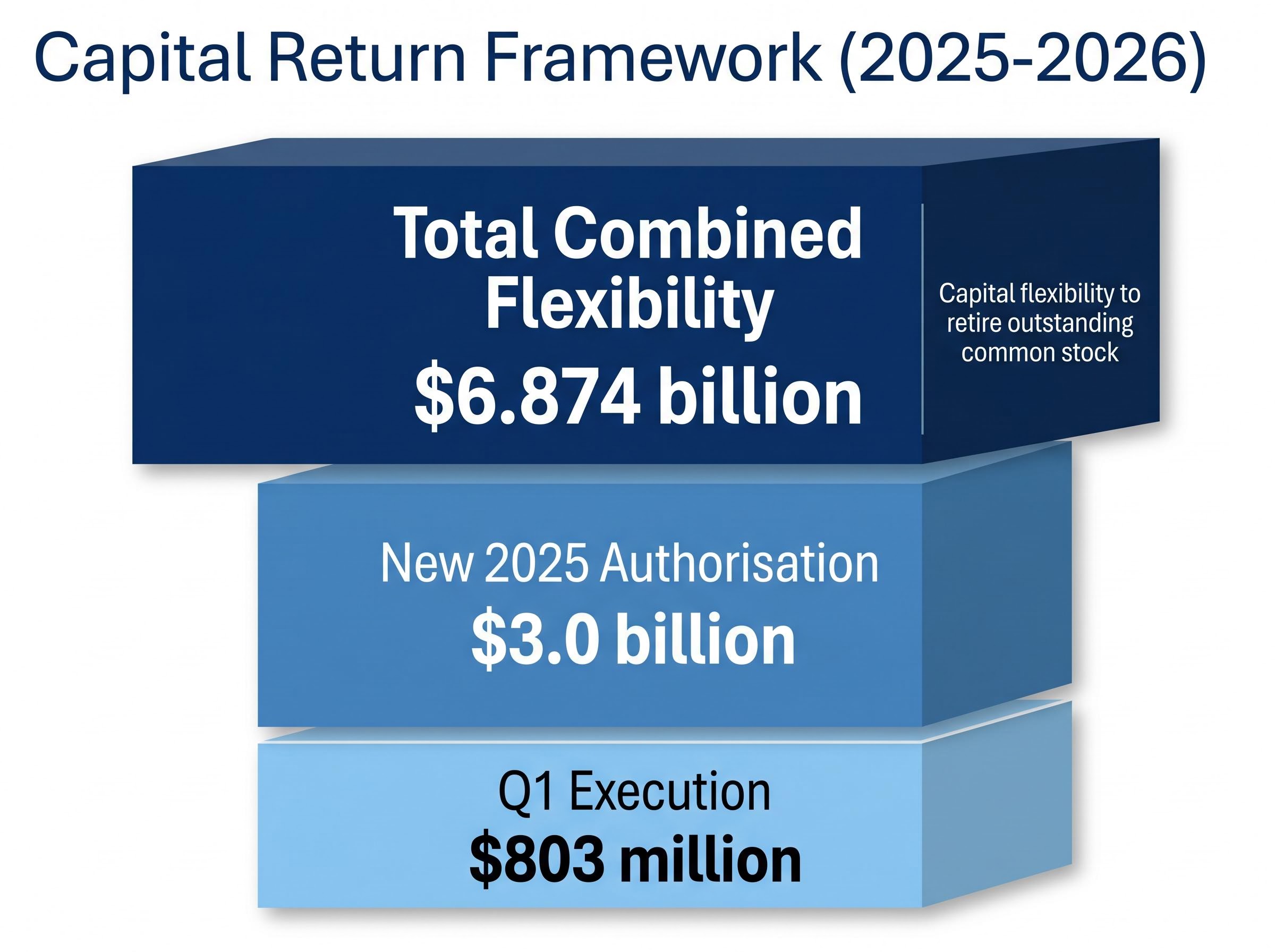

Management is actively leveraging the company’s massive capital reserves to absorb operational shocks and aggressively support equity valuation. Corporate share repurchase initiatives serve as a deliberate buffer against temporary manufacturing headwinds and a core mechanism for returning value.

During the first quarter, the company executed common stock buybacks. Analysts from investment firms such as TD Cowen view this ongoing repurchase activity positively, noting it as a strategic catalyst for per-share earnings growth. Stock buybacks mechanically improve per-share metrics by reducing the total float, signalling management’s firm belief that their equity remains undervalued.

Recent TD Cowen forward price target adjustments highlight how reducing the outstanding share count mathematically amplifies the impact of every dollar generated by the commercial portfolio.

The current capital return framework consists of three primary components:

The first quarter of 2026 presents a clear synthesis of opposing operational forces. Top-line commercial success, driven by the explosive growth of Dupixent and the steady adoption of Eylea HD, provides strong forward momentum. However, trailing manufacturing impacts enforce a temporary but noticeable margin contraction.

Despite the profitability drag stemming from historical Limerick facility setbacks and supply chain friction, fundamental demand for the broader product portfolio remains robust. Institutional sentiment reflects this balanced perspective, supported by a consensus stock price target of $854.13. The extensive share repurchase authorisation provides a durable financial safety net, ensuring that management possesses the capital flexibility required to defend equity valuations while manufacturing efficiency fully normalises into the second half of the year.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Regeneron reported a robust $3.6 billion first-quarter revenue, surpassing analyst expectations, but also noted a decline in GAAP gross product margins from 81% to 76%.

Gross product margins declined due to historical Limerick facility setbacks and ongoing supply chain friction, which led to impacts like elevated inventory write-offs and unabsorbed operational expenses.

Regeneron is managing the transition from legacy Eylea to the high-dose Eylea HD, which saw 52% revenue growth, and secured FDA approval for extended 20-week dosing for Eylea HD, offering a competitive advantage.

The Dupixent joint venture with Sanofi is a critical growth engine, with collaborative revenue expanding 36% to $1.6 billion, effectively diversifying Regeneron's revenue streams and offsetting ophthalmology segment contractions.

Regeneron is actively supporting its equity valuation through aggressive share repurchases, executing $803 million in Q1 buybacks and holding a total repurchase capacity of $6.874 billion.