ECB Warns €425bn in Private Credit Poses Spillover Risk

1 hr ago

Seagate Technology capped an extraordinary annual stock gain with a massive 16% after-hours surge on 28 April 2026, following its fiscal third-quarter earnings release. The dramatic upward movement was triggered by a substantial earnings beat and exceptional forward guidance that forced Wall Street to rapidly revise its financial models.

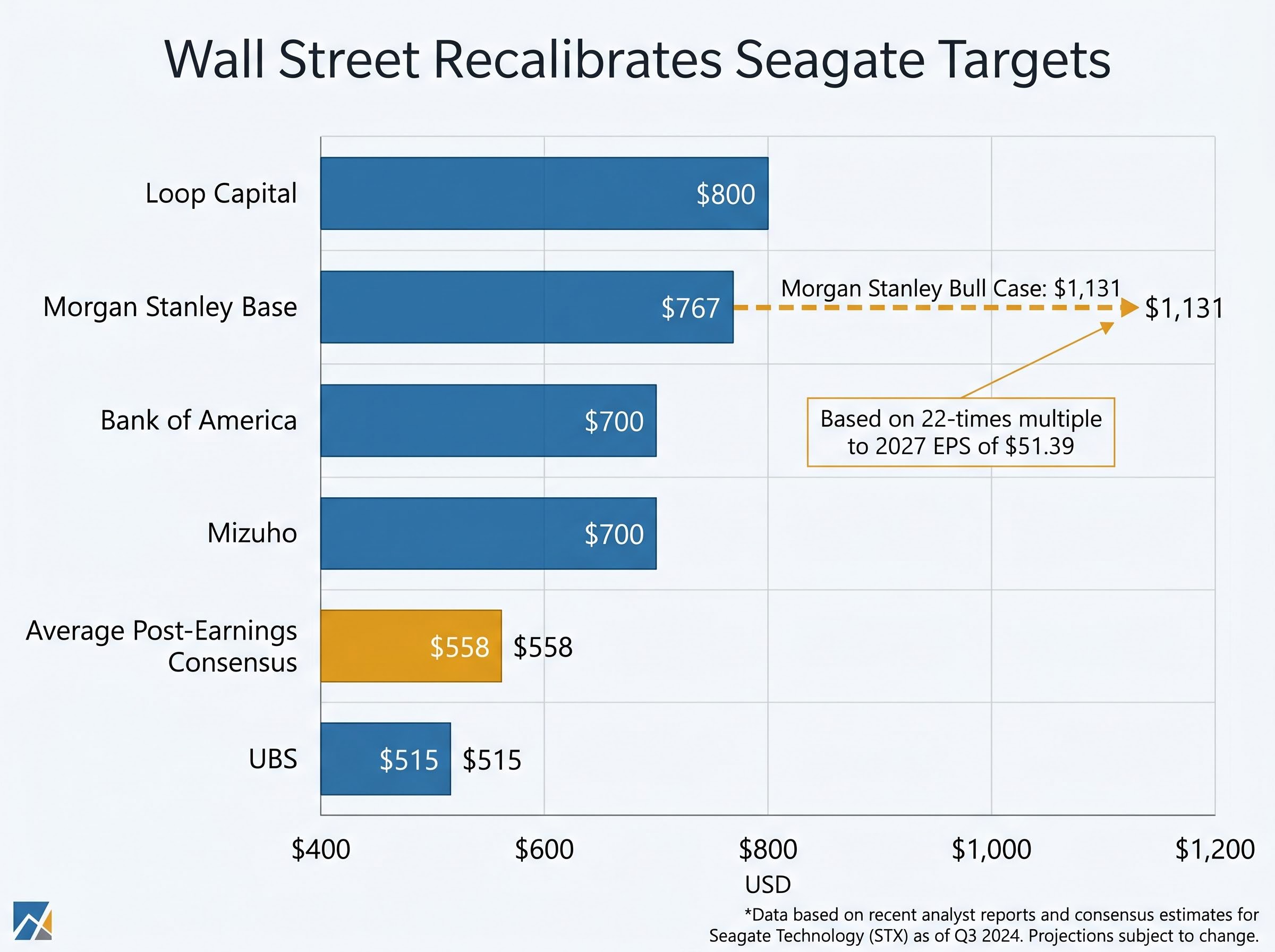

Following the results, sweeping upgrades on 29 April saw analysts significantly raise their Seagate stock price target projections. This rapid recalibration reflects a sudden shift in institutional understanding of artificial intelligence infrastructure spending. The underlying data centre demand is translating directly into hardware profits much faster than previously anticipated.

What follows is a comprehensive breakdown of the specific financial metrics, the physical storage technology driving the surge, and exactly what this baseline reset means for the broader hardware sector.

The flurry of analyst actions that hit trading desks on Wednesday morning was immediate and aggressive. Institutional coverage scrambled to catch up with the company’s forward momentum, resulting in a wave of projection increases across major investment banks. Morgan Stanley established itself as the most aggressive bull in the technology hardware sector.

The underlying mathematics of these new valuations rely heavily on calendar year 2027 profit expectations. Analysts are projecting that current artificial intelligence capital expenditures will result in sustained, multi-year margin expansion for storage providers.

| Firm | New Price Projection | Rating |

|---|---|---|

| Loop Capital | $800 | Buy |

| Morgan Stanley | $767 | Overweight |

| Bank of America | $700 | Buy |

| Mizuho | $700 | Outperform |

| UBS | $515 | Neutral |

Loop Capital raised its projection to $800, while Morgan Stanley increased its base target to $767. According to market reports, the highest tier of Wall Street optimism belongs to Morgan Stanley’s bull-case scenario, which calculates a $1,131 valuation. This specific ceiling is based on assigning a 22-times multiple to a 2027 earnings estimate of $51.39 per share.

The Morgan Stanley price target upgrades rely on expanding profit margins driven by pricing power, reflecting a broader institutional consensus that hardware suppliers will capture an outsized portion of total infrastructure spending.

The average post-earnings consensus now sits around $558. UBS maintained a more conservative stance, holding a $515 projection with a Neutral rating. These institutional upgrades serve as leading indicators for sustained institutional buying, helping investors gauge the absolute ceiling of the current hardware cycle.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The raw financial data from the fiscal third quarter ending 3 April 2026 proves that artificial intelligence infrastructure spending is translating into immediate profits. The contrast between consensus estimates and actual reported figures highlights a level of operational execution that caught the market by surprise.

The official Seagate fiscal third quarter results confirm these sweeping beats across both revenue and earnings per share, demonstrating how aggressively cloud hyperscalers are scaling their physical infrastructure purchases.

March Quarter Revenue: Reported at $3.11 billion, beating the $3.0 billion estimate. March Quarter Non-GAAP EPS: Reported at $4.10, surpassing estimates of $3.48 to $3.50. June Quarter Revenue Guidance: Projected at $3.45 billion, easily clearing the $3.15 billion consensus. June Quarter EPS Guidance: Projected at $5.00, heavily outpacing the $3.97 expectation.

This surprisingly strong June quarter forward guidance forced analysts to rewrite their financial models entirely. Management commentary further cemented the bullish narrative. Dave Mosley, Chair and Chief Executive Officer, reported that the company achieved record margin performance alongside the revenue beat.

Operations generated close to $1 billion in free cash flow during the quarter. This tangible cash generation demonstrates that the hardware providers supplying the artificial intelligence build-out are securing real profits, rather than just distant theoretical gains.

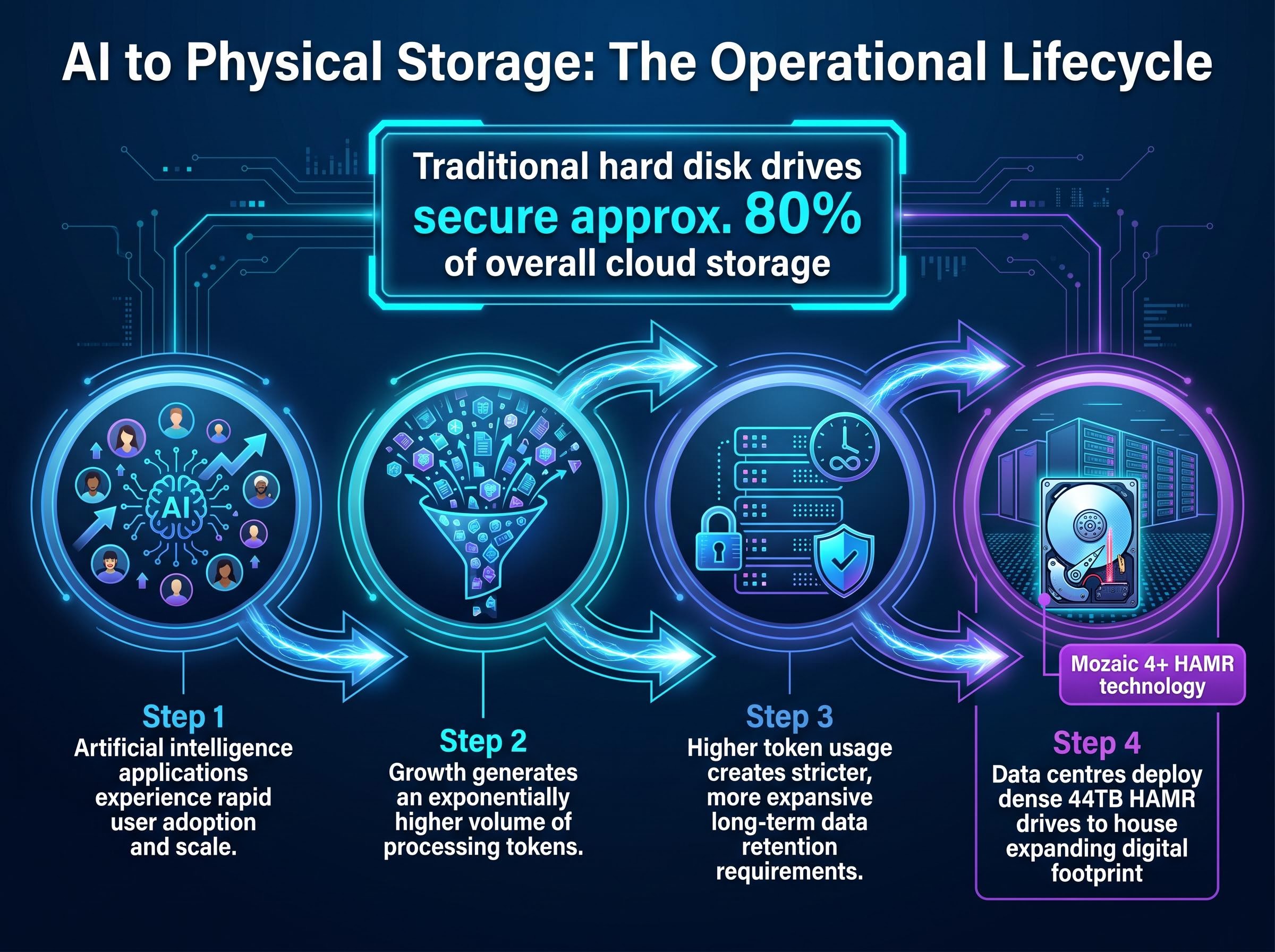

The explosion of artificial intelligence capabilities requires a massive physical storage expansion to function. According to industry estimates, while solid-state drives dominate consumer electronics, traditional hard disk drives still secure approximately 80% of overall cloud storage requirements. Cloud hyperscalers require high-capacity, cost-effective mediums to store the vast datasets that train large language models.

To meet this unprecedented cloud demand, Seagate has introduced its proprietary Mozaic 4+ HAMR technology. This specific architecture delivers up to 44TB per drive and has officially begun revenue shipments to major cloud providers. The structural permanence of this demand becomes clear when tracing the operational lifecycle of machine learning models.

Understanding this physical sequence explains why hard drive manufacturers are capturing such significant capital expenditure. The technology provides a defensible moat against competing storage mediums.

Volume growth provides positive revenue momentum, but pricing power is the true engine of margin expansion. The current profit equation relies just as heavily on constrained supply as it does on artificial intelligence demand. The consolidation of major storage suppliers over the past decade has led to tight production control and strategic inventory shortages across the sector.

This macroeconomic supply and demand imbalance is generating unprecedented pricing leverage for hardware manufacturers.

Critical Pricing Metric According to market reports, the cost of storage capacity per terabyte increased by 5% during the initial three months of the calendar year, significantly outpacing the anticipated 1% expansion rate forecasted by industry analysts.

Morgan Stanley analysts specifically cited these pricing dynamics as the primary catalyst for expanding profit margins. When manufacturers can successfully raise per-terabyte costs against a backdrop of surging volume demand, the result is the type of earnings outperformance witnessed this week.

For investors evaluating whether this hardware supercycle is fully reflected in current share prices, our detailed coverage of Seagate’s HDD valuation examines the underlying total cost of ownership advantages over solid-state alternatives and assesses the potential duration of the current upcycle.

A rising tide lifts all boats within the data infrastructure sector. The immediate ripple effects of the 28 April earnings release sent direct competitors surging in extended trading. This singular corporate success provided broader validation for artificial intelligence data centre infrastructure spending across the entire hardware ecosystem. For investors holding adjacent technology stocks, this massive earnings beat derisks the near-term sector outlook.

Western Digital shares jumped approximately 10% in extended trading directly following the announcement. Upward momentum was also observed in related memory peers like Micron, as the market digested the strength of enterprise demand.

The broader market consensus now anticipates that calendar year 2027 profits will remain highly elevated. As the hardware supercycle continues, suppliers with established pricing power are well-positioned to capture the ongoing capital expenditure boom.

However, these optimistic multi-year hardware projections must still be weighed against broader market recession risks, particularly as sustained energy shocks threaten to disrupt the underlying corporate spending environment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Seagate's stock surged over 16% after-hours due to a substantial fiscal third-quarter earnings beat and exceptional forward guidance, driven by accelerating artificial intelligence infrastructure spending.

Analysts aggressively raised their Seagate stock price target projections after the earnings, with firms like Loop Capital moving to $800 and Morgan Stanley to $767, based on increased 2027 profit expectations.

Mozaic 4+ HAMR is Seagate's proprietary hard drive technology, delivering up to 44TB per drive, designed to meet the high-capacity, cost-effective storage demands of cloud hyperscalers for AI datasets.

AI applications generate exponentially higher data volumes and processing tokens, creating vast long-term data retention requirements that necessitate the deployment of high-density hard drives like Seagate's HAMR technology.