Domino’s Falls 9.6% to 52-Week Low After Q1 Miss on All Metrics

15 hrs ago

Fewer than 1% of Blue Owl Capital Corporation II (OBDC II) shareholders tendered their shares at $3.80 apiece, delivering one of the most lopsided rejections of an unsolicited tender offer in recent non-traded business development company (BDC) history. The offer, launched by Saba Capital Management and Cox Capital Partners in early March 2026, sought up to 6.9% of OBDC II’s outstanding shares at a discount of roughly 33-35% to net asset value (NAV). With the tender window closing on 24 April 2026, the near-total rejection ends a seven-week standoff that tested shareholder conviction against a firm whose business model centres on buying private credit assets cheaply. What follows covers the offer’s precise terms, the board’s layered case for rejection, what the outcome signals about OBDC II’s outlook, how Saba Capital’s broader strategy frames the stakes for retail holders of private credit funds, and where the story goes from here.

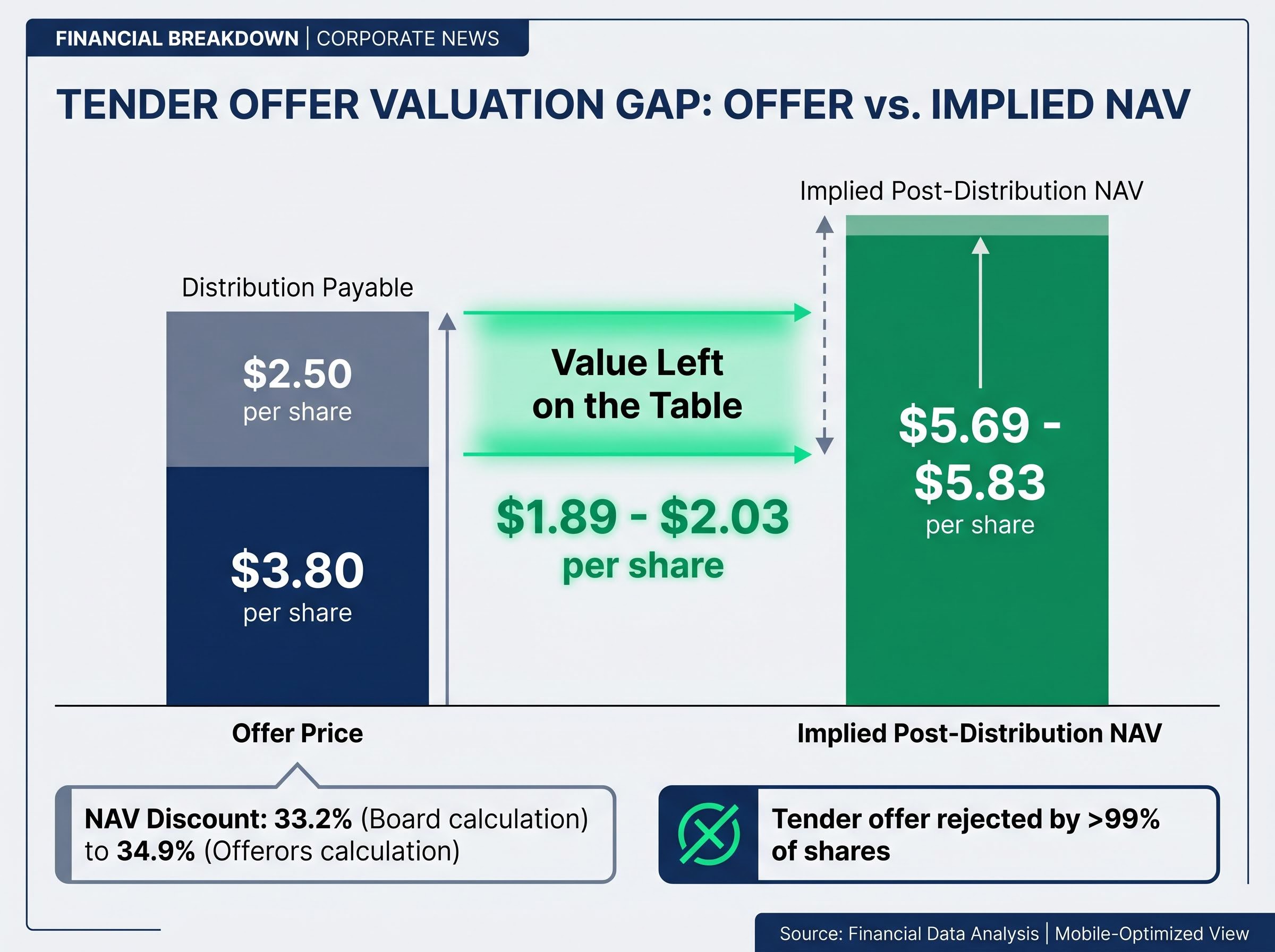

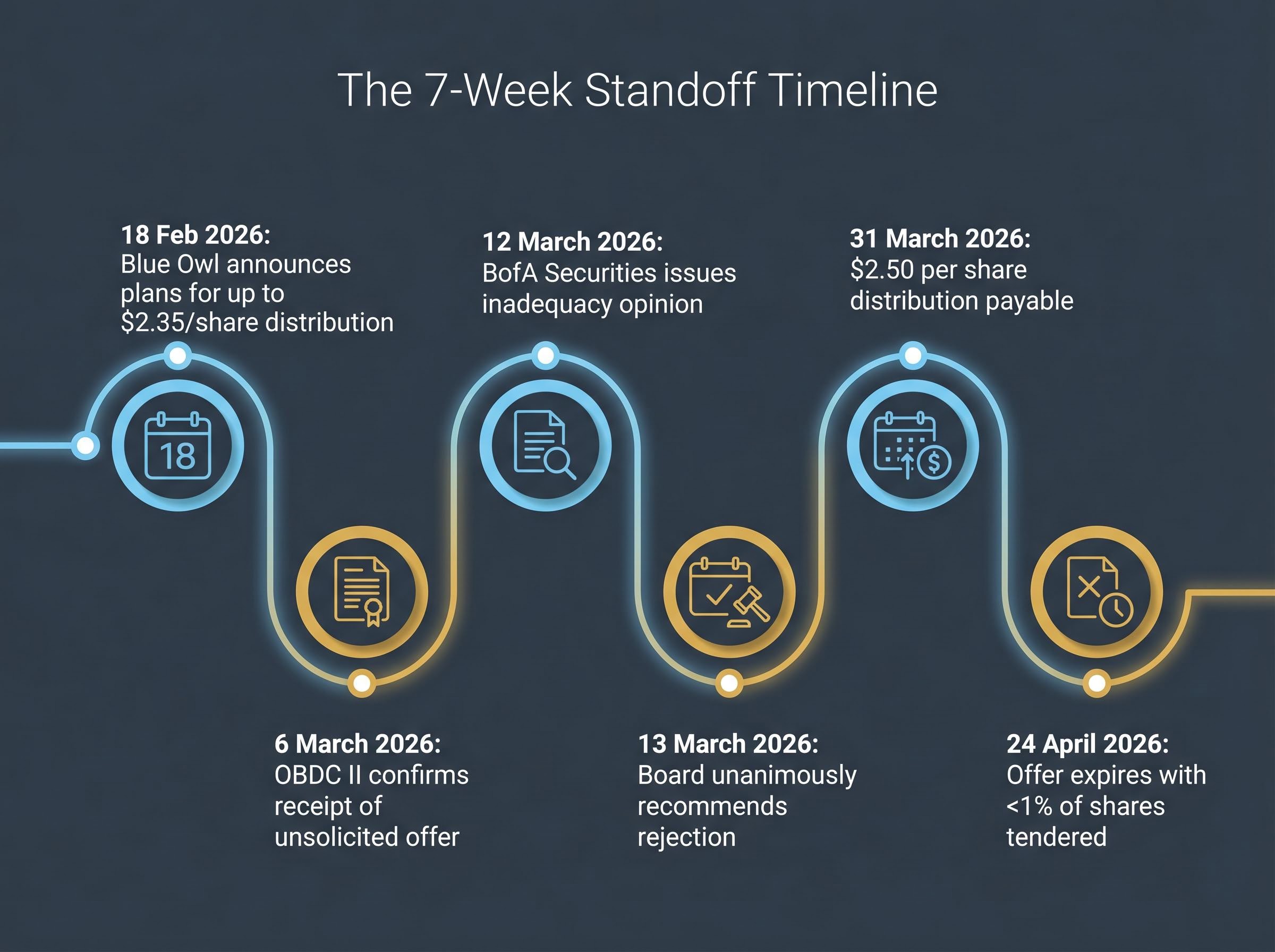

The terms were straightforward. Saba Capital and Cox Capital Partners offered $3.80 per share in cash for up to 8 million shares, a total outlay of approximately $30.4 million representing roughly 6.9% of OBDC II’s outstanding shares. The offer was unsolicited; OBDC II confirmed receipt on 6 March 2026 and promised a formal board recommendation.

The headline figure, however, was the discount. The two sides could not agree on its exact size, because they used different NAV reference dates. The board pegged the discount at approximately 33.2%, calculated against the 24 February 2026 NAV and adjusted for the $2.50 per share return-of-capital distribution payable by 31 March 2026. The offerors cited approximately 34.9%, using the 26 February 2026 dividend reinvestment plan (DRIP) issuance value less the same distribution.

Key offer terms at a glance:

The central number: At either party’s calculation, shareholders were being asked to sell at a discount of roughly 33-35% to the fund’s stated net asset value.

Both figures imply a post-distribution NAV between $5.69 and $5.83 per share, meaning the offer left between $1.89 and $2.03 per share of recognised value on the table. That gap is the single most important number in the story.

The disagreement over reference dates and discount calculations in this case reflects a broader problem across the sector: the private credit NAV valuation gap between reported book values and what secondary market buyers will actually pay has widened to levels not seen in 25 years, with secondary buyers pricing fund stakes at approximately 65 cents on the dollar even as managers continue reporting near-par valuations.

On 13 March 2026, the board issued a unanimous recommendation to reject the offer. The recommendation was not a boilerplate rebuff. It was backed by a formal inadequacy opinion from BofA Securities, dated 12 March 2026, which concluded that the $3.80 offer price was inadequate from a financial point of view. Legal counsel Kirkland & Ellis and Eversheds Sutherland advised the board through the process.

The board’s stated rationale rested on three pillars:

A formal inadequacy opinion from a major bank carries more weight than a standard board rejection. It signals that an independent financial adviser examined the terms and found them deficient, not merely that management preferred shareholders stay.

The timing of the offer compounded its unattractiveness. On 18 February 2026, Blue Owl had announced plans to distribute up to $2.35 per share (approximately 30% of NAV) as a return of capital, backed by approximately $1.4 billion in planned asset sales across its BDC platform. The final declared distribution was $2.50 per share, payable by 31 March 2026 to shareholders of record as of 24 March 2026.

For a shareholder already owed $2.50, tendering at $3.80 meant accepting just $1.30 in net additional value for shares the board valued well above that level. OBDC II’s stated targets for 2026, quarterly returns exceeding 5% and total returns of more than 50% of net assets, further widened the gap between the offer price and the board’s projected shareholder outcome.

Fewer than 1% of OBDC II shareholders tendered their shares, one of the most decisive rejections on record for a non-traded BDC tender offer.

The scale of the rejection removes ambiguity. Shareholders who received the offer, read the board’s recommendation, and weighed the pending $2.50 distribution overwhelmingly concluded that $3.80 was not sufficient.

The parent company’s operating metrics provide context for that conviction. Blue Owl Capital (NYSE: OWL), which manages OBDC II, reported revenue growth of approximately 25% year-over-year and carried a dividend yield of approximately 9.80% as of late April 2026.

| Metric | Value | Context |

|---|---|---|

| Revenue growth (YoY) | ~25.04% | Reflects growth across Blue Owl’s credit platform |

| Dividend yield | ~9.80% | Income-focused investors’ primary return metric |

| Market capitalisation | ~$14.36 billion | Among the larger alternative asset managers |

| Forward P/E ratio | ~10.35 | Below broader market multiples |

| OWL closing price (24 April 2026) | $9.52 | Down ~7.8% from $10.33 on 21 April 2026 |

OWL shares closed at $9.52 on 24 April 2026, down approximately 7.8% from $10.33 on 21 April 2026. No direct causal link between the tender offer outcome and this price movement has been established; broader market conditions may account for the decline.

For income-focused holders of OBDC II and similar Blue Owl vehicles, the near-total rejection, combined with the parent company’s operating trajectory and OBDC II’s 9.1% annualised return since inception, reinforces the board’s framing that the fund’s long-term value materially exceeded the offer.

Saba Capital’s approach to OBDC II follows a documented strategy. The firm targets retail-held, non-traded closed-end funds and private credit vehicles where shares trade at significant discounts to their stated NAV. It positions itself as a secondary market liquidity provider, offering cash to shareholders who lack other exit routes.

The strategy rests on three components:

Saba Capital’s documented target: acquiring positions at 30-40% discounts to NAV in retail-held private credit vehicles.

Background context matters here. Blue Owl had previously pursued a merger of OBDC and OBDC II, which was terminated on 19 November 2025 due to adviser pushback and market volatility. That termination may have influenced the timing of the Saba and Cox tender offer, as it left OBDC II without a near-term structural catalyst and potentially more exposed to unsolicited approaches.

The OBDC II offer did not emerge in isolation; sector-wide redemption gating across Blue Owl, Blackstone, and Ares funds was already a documented pattern by early 2026, with some funds receiving redemption requests equal to 41% of fund assets while quarterly caps permitted only 5% to exit, conditions that create exactly the kind of trapped-investor dynamic that discount tender offerors are designed to exploit.

Retail investors in non-traded BDCs and private credit funds are recurring targets of this type of offer. Recognising the strategy helps shareholders in similar vehicles evaluate future unsolicited approaches on their financial merits rather than responding to the pressure of a limited tender window.

As of 27 April 2026, no public disclosure of final share-count results from Saba Capital or Cox Capital Partners has emerged. The definitive record of how many shares were tendered and accepted will come from post-expiration SEC filings, likely an amended Schedule TO.

Three items define the near-term timeline:

A regulatory development in April 2026 could shape the pace of future unsolicited offers. The SEC issued exemptive relief permitting 10-business-day tender offers for equity securities of certain public and private companies, according to commentary from Eversheds Sutherland and the Free Writings law blog. This halves the standard 20-business-day minimum tender period.

The relief is not specific to BDCs, but its implications for the non-traded fund sector are direct. A shorter tender window compresses the time shareholders have to evaluate board recommendations and seek independent advice, potentially increasing the effectiveness of unsolicited offers targeting retail-held vehicles.

Sidley Austin’s legal analysis of the SEC’s 10-business-day tender offer exemptive relief, published on 22 April 2026, details the conditions under which the halved minimum period applies to cash-only, fixed-price equity tender offers, with the firm noting that the compressed timeline materially changes the practical dynamics of offer evaluation for target shareholders.

OBDC II’s planned distribution programme and its next quarterly filing remain the most concrete data points for shareholders tracking the fund’s trajectory. The rejection of Saba’s offer closes one chapter; the distribution schedule and updated NAV data will open the next.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Forward-looking statements regarding OBDC II’s distribution targets and planned capital returns are subject to change based on market conditions, asset sale outcomes, and fund performance. Past performance does not guarantee future results.

The OBDC II tender offer was an unsolicited cash bid of $3.80 per share for up to 8 million shares (approximately 6.9% of outstanding shares), launched by Saba Capital Management and Cox Capital Partners in early March 2026. The offer represented a discount of roughly 33-35% to OBDC II's net asset value and expired on 24 April 2026.

The board unanimously recommended rejection on three grounds: the $3.80 price was characterised as arbitrary and value-capturing at remaining shareholders' expense, tendering would forfeit a $2.50 per share return-of-capital distribution already in motion, and OBDC II's 9.1% annualised return since inception demonstrated the fund's long-term value materially exceeded the offer price. The recommendation was backed by a formal inadequacy opinion from BofA Securities.

Fewer than 1% of OBDC II shareholders tendered their shares, making it one of the most decisive rejections on record for an unsolicited non-traded BDC tender offer. The definitive share count will be confirmed in post-expiration SEC filings from the offerors.

Saba Capital targets retail-held, non-traded closed-end funds and private credit vehicles where shares trade at significant discounts to stated NAV, typically seeking to acquire positions at 30-40% discounts. The firm positions itself as a secondary market liquidity provider, framing its offers as exit options for investors in otherwise illiquid vehicles.

Shareholders should monitor the offerors' amended Schedule TO filing confirming final tender results, OBDC II's Q1 2026 Form 10-Q on SEC EDGAR for updated NAV data following the $2.50 distribution, and the fund's planned quarterly distributions targeting returns exceeding 5% per quarter and more than 50% of net assets across 2026.