What Domino’s Q1 Results Reveal About the Consumer Spending Slowdown

11 hrs ago

When Saba Capital and Cox Capital Management showed up in February 2026 offering to buy Blue Owl Capital Corporation II shares at a 33% discount to net asset value, they were not doing retail investors a favour. They were doing themselves one.

Non-traded business development companies (BDCs) and interval funds have become the preferred vehicle for bringing private credit to retail portfolios. The quarterly redemption structures underpinning these products, however, are now buckling under simultaneous withdrawal pressure across Blue Owl, Blackstone, and Ares. Saba Capital’s tender offer campaign is the single most visible symptom of a structural problem that has been building for years, and it raises uncomfortable questions about what retail investors actually hold when they own a “semi-liquid” private credit fund.

By the end of this article, the mechanics of Saba’s arbitrage, the structural disadvantage facing retail investors in these products, the live stress data across major non-traded BDCs, and the specific questions any investor should ask before committing capital to a private credit fund will all be clear.

Saba Capital, with approximately $9.7 billion in assets under management as of 2023, built its franchise on a simple observation: non-traded private credit vehicles promise investors quarterly liquidity that the underlying assets cannot deliver. When redemption pressure arrives, the gap between net asset value and available exit price widens. Saba’s business is to stand in that gap.

The activist toolkit has three components:

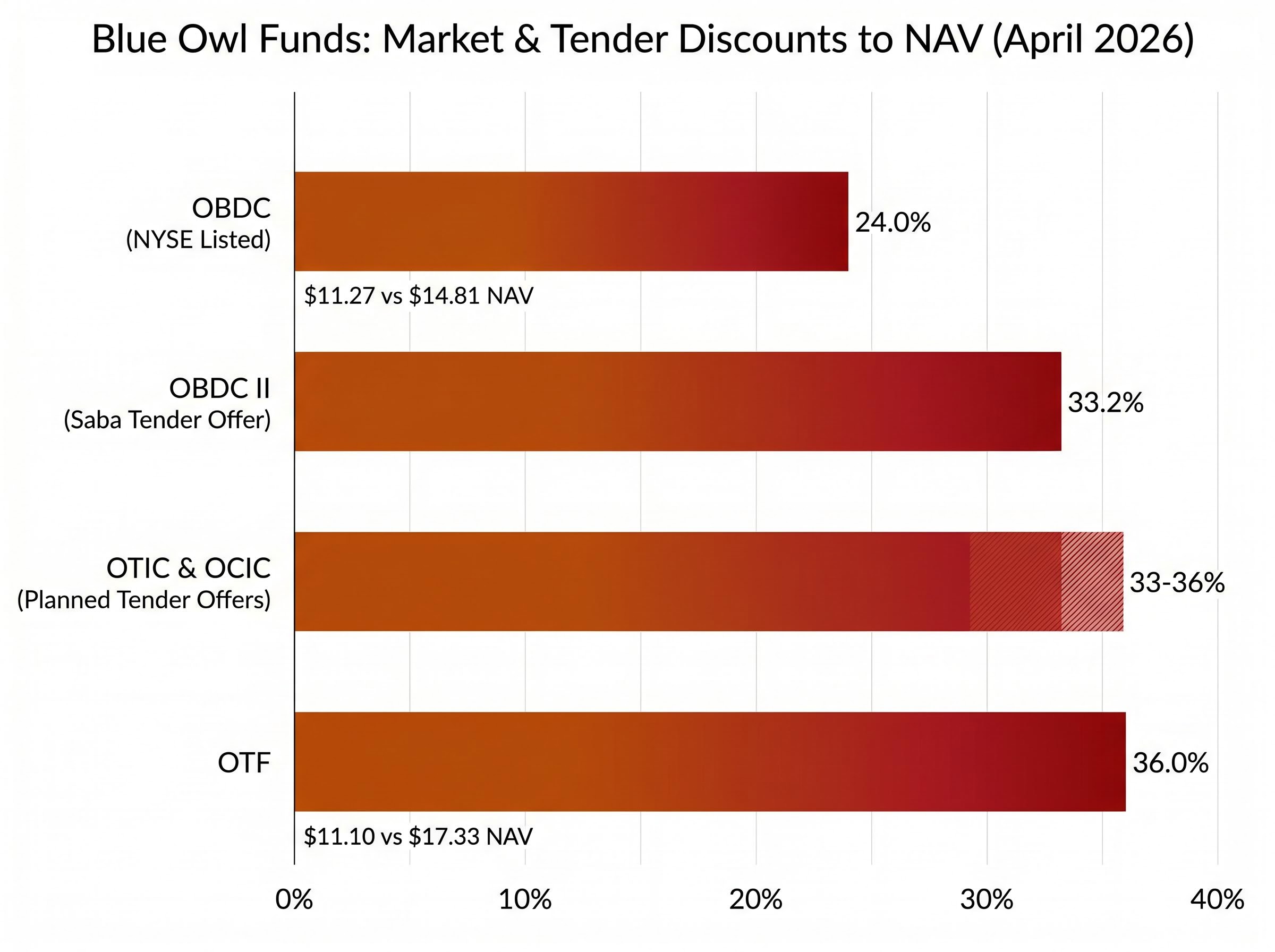

For OBDC II, the tender offer came in at approximately 33.2% below NAV. Planned offers for Blue Owl Technology Income Corp. (OTIC) and Blue Owl Credit Income Corp. (OCIC) targeted a similar 33-36% discount range. The offers commenced on 6 March 2026 and expired on 24 April 2026.

Saba and Cox cited “significant industry-wide” redemption pressures and restricted withdrawals across non-traded BDCs as the rationale for their offers, framing the discounted bids as a necessary liquidity solution for stranded retail investors.

OBDC II’s board unanimously recommended shareholders reject the offer. Participation came in at well under 1% of shares outstanding. Yet the mere existence of the bid tells a story: in the absence of an exchange-based secondary market, a 33% discount from a sophisticated arbitrageur is functionally the only liquid exit price available to retail holders who need their capital back.

The liquidity mismatch in non-traded private credit was not a bug that emerged under stress. It was a design feature that was always going to create this outcome at scale.

The underlying assets in these funds are direct loans to middle-market companies, typically carrying multi-year maturities with no active secondary market. These loans were packaged inside vehicles offering quarterly redemption windows, creating the impression of semi-liquid access. The standard cap allows redemptions of 5% of fund assets per quarter. When investor requests exceed that cap, a gate activates and requests are filled on a pro-rata basis.

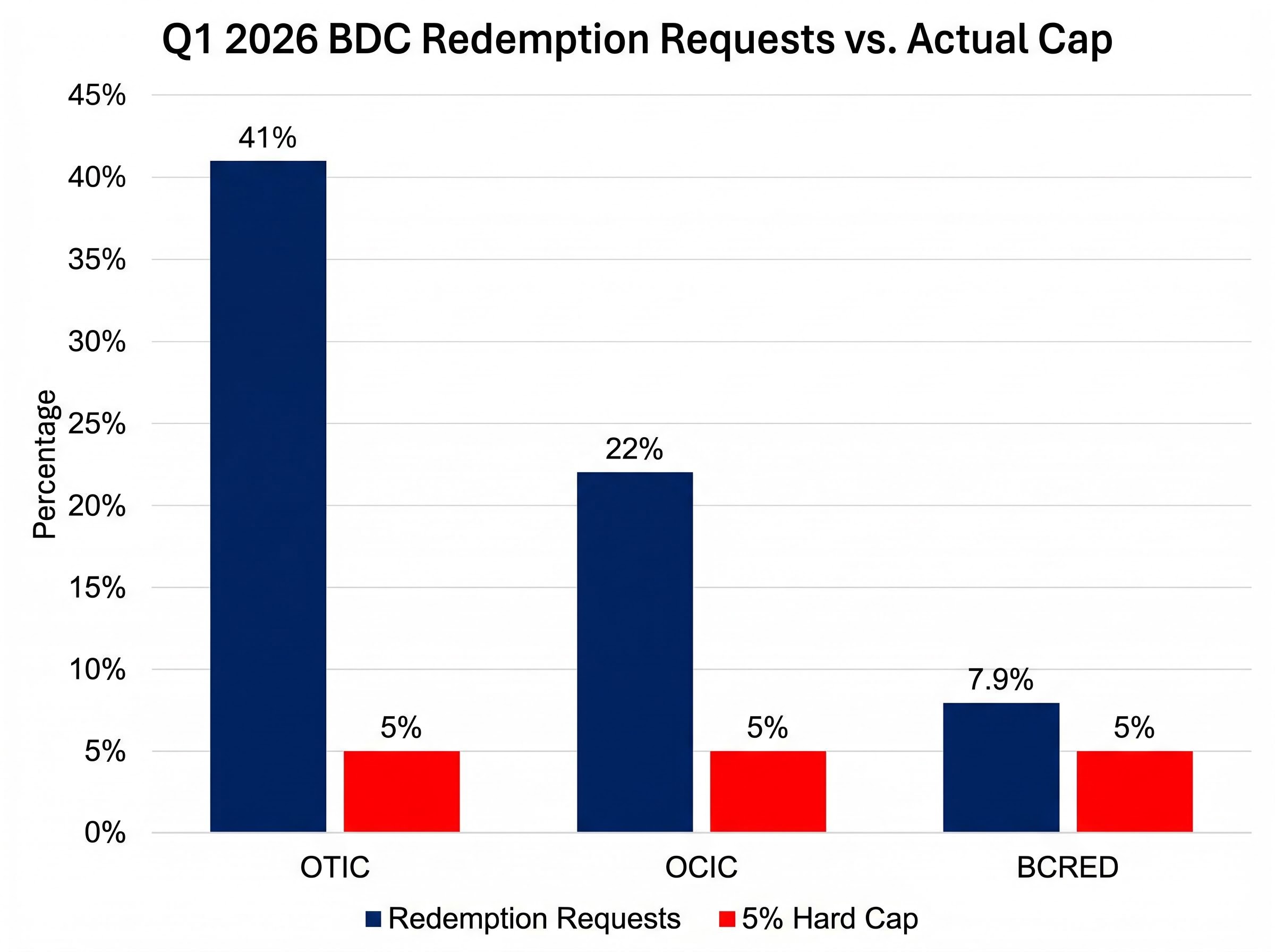

In Q1 2026, the scale of the mismatch became measurable. OTIC received redemption requests equivalent to 41% of fund assets; the gate capped actual redemptions at 5%. OCIC received requests equivalent to 22% of fund assets; the same 5% cap applied. Blackstone’s BCRED faced requests of approximately 7.9% of fund assets in the same quarter.

| Fund | Structure | Q1 2026 Redemption Requests (% of Assets) | Redemption Cap Applied |

|---|---|---|---|

| OTIC | Non-traded BDC | 41% | 5% |

| OCIC | Non-traded BDC | 22% | 5% |

| BCRED | Non-traded BDC | ~7.9% | 5% |

Even the exchange-listed escape valve carries its own discount risk. OBDC, the publicly traded NYSE peer, was trading at approximately a 24% discount to NAV (around $11.27 versus $14.81 NAV) as of approximately April 2026. OTF (Blue Owl Capital Corporation III) traded at approximately a 36% discount (around $11.10 versus $17.33 NAV).

Fergus McCorkell of Troy Asset Management warned in a January 2026 paper of contagion risk: if broader market concerns triggered a rush to sell, investors would liquidate liquid assets first, leaving illiquid private credit positions trapped and unable to fund redemptions.

The gap between promised liquidity and available liquidity is the risk that most product marketing materials obscure. What happened at Blue Owl made it visible.

For investors who want the fuller picture before examining BDC-specific mechanics, our full explainer on the hidden risks in private equity and private credit covers record 9.2% default rates across US private credit, the institutional retreat by Yale and Harvard from illiquid allocations, and the SEC’s 2026 examination priorities targeting private fund valuation practices and conflict-of-interest disclosures.

The OBDC II episode provides the clearest available template for how fund-level stress unfolds in real time. The sequence ran as follows:

The loan sale at 99.7% of par was notable. It meant the portfolio’s mark-to-market was largely intact; the problem was not credit quality but the structural inability to convert performing loans into cash at the pace investors demanded.

Blue Owl (OWL) shares fell approximately 10% over the week ending 20 February 2026, with a 6% decline on 19 February followed by a further 4% drop on 20 February. Public equity markets were pricing the reputational and structural risks into the asset manager itself, not just the funds.

The simultaneous triggering of redemption caps across Blue Owl, Blackstone, and Ares in Q1 2026 removed any possibility that this was an idiosyncratic event. Fitch Ratings characterised non-traded BDCs as experiencing “more widespread negative net flows” as of 13 April 2026.

Total BDC assets under management across all structures stood at approximately $481 billion as of Q2 2025. When parallel redemption pressure hits multiple managers simultaneously, no single fund can quietly resolve its liquidity mismatch in isolation. The gate mechanism prevents disorderly unwinds, but it also ensures that capital remains trapped precisely when investors most want it released.

A business development company is a fund structure that makes direct loans to middle-market companies, typically businesses too small to access public bond markets. These loans generate income through interest payments, which is distributed to fund investors. BDCs come in two forms: traded and non-traded.

The quarterly redemption structure was designed with a logic: the underlying loans are illiquid, so the fund should not promise daily liquidity it cannot deliver. The 5% quarterly cap was intended to balance investor access against portfolio stability. Under normal conditions, where redemption requests remain modest, the structure functions as intended.

Under stress, the structure functions as a gate.

The SEC’s Investor Advisory Committee issued formal recommendations in September 2025 on retail investor access to private market assets, explicitly acknowledging the liquidity mismatch risks for retail participants in these vehicles.

FINRA followed with an update to Rule 5123 (SR-FINRA-2026-002, January 2026), modifying requirements relevant to private credit product distribution to retail investors. Both actions signal that regulators have formally recognised the gap between how these products are sold and how they perform under redemption pressure.

The SR-FINRA-2026-002 filing amending Rule 5123 for private placements modifies the documentation and disclosure requirements that broker-dealers must meet when distributing private credit products to retail investors, representing a formal regulatory acknowledgment that existing standards were inadequate for the current scale of retail participation.

Saba Capital’s stated position is that retail-held private credit is heading for significant near-term stress. That thesis is worth examining on its merits, even while noting that Saba’s business model depends on it being correct.

The target entry range of 30-40% discounts to NAV represents the zone where their arbitrage becomes commercially viable. Their willingness to deploy capital at those levels is a market signal: a sophisticated fund with nearly $10 billion in assets is positioning for the probability that structural stress in non-traded BDCs will persist, not resolve.

Three conditions could accelerate that stress. Broader credit deterioration would increase loan defaults in the underlying portfolios. Continued negative net flows would shrink fund assets and reduce the capital available to honour redemptions. Any macro shock triggering simultaneous redemption pressure across the sector would replicate and amplify the Q1 2026 dynamic.

As of late April 2026, gates remain active at both OTIC and OCIC, with no publicly announced resolution timeline. Fitch’s characterisation of negative net flows as more widespread, rather than stabilising, reinforces that the sector has not turned a corner.

Each question maps directly to a risk dimension this analysis has identified: gate risk, discount risk, asset liquidity, and regulatory standing. The answers, or the inability to get clear answers, should inform any decision about remaining in these products.

Saba Capital’s tender offers are not the cause of the stress in retail private credit. They are the price signal that emerges when a structural mismatch between illiquid assets and semi-liquid promises meets a redemption cycle under pressure.

The Blue Owl episode, the simultaneous gating at Blackstone and Ares, and Fitch’s characterisation of sector-wide negative flows all point to the same conclusion: the retail democratisation of private credit has moved faster than the secondary market infrastructure needed to support it.

Structural lock-in in illiquid private market allocations is not a retail-only problem: Washington State Investment Board, managing $230.5 billion, voted in late 2024 to reduce its private equity target from 28% to 23% and was still approving new commitments in April 2026 because the multi-year capital call cycle makes meaningful reductions impossible on any reasonable timeline.

The 33-36% discounts Saba is offering are not arbitrary. They represent the market-clearing price for immediate liquidity in a structure that was never designed to provide it on demand. For retail investors still holding these products, the relevant question is not whether Saba is acting in their interest but whether their own liquidity needs align with the structural realities of what they own.

Any investor holding a non-traded BDC or interval fund should review the specific redemption terms, current gate status, and underlying loan quality of that position before the next quarterly redemption window, not after it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A non-traded business development company (BDC) is a fund that makes direct loans to middle-market companies but is not listed on any stock exchange, meaning investors can only access liquidity through quarterly redemption windows capped at 5% of fund assets. A traded BDC is listed on an exchange like the NYSE, allowing daily buying and selling at market prices, though those prices may still trade well below the fund's stated net asset value.

In Q1 2026, redemption requests far exceeded the 5% quarterly cap at multiple major non-traded BDCs, including Blue Owl's OTIC (41% of assets requested) and OCIC (22% of assets requested), triggering gates that restricted withdrawals because the underlying loans cannot be converted to cash fast enough to meet investor demand.

Saba Capital acquires shares in non-traded private credit funds at steep discounts to net asset value, typically 33-36%, exploiting the gap between promised liquidity and actual exit prices available to retail investors who need immediate cash. For retail holders, Saba's discounted bids often represent the only functional liquid exit in the absence of an exchange-based secondary market.

Investors should ask about the fund's current redemption cap utilisation, how many consecutive quarters gates have been triggered, the discount between stated NAV and secondary market transaction prices, the liquidity of the underlying loan portfolio, and whether the manager has faced any regulatory inquiries related to liquidity management.

The SEC's Investor Advisory Committee issued formal recommendations in September 2025 acknowledging liquidity mismatch risks for retail investors in these vehicles, and FINRA updated Rule 5123 in January 2026 to modify disclosure requirements for broker-dealers distributing private credit products to retail investors.