How Hormuz Closure at $104 Oil Is Reshaping Every Asset Class

6 hrs ago

On 27 April 2026, Paramount‘s chief legal officer Makan Delrahim signed and submitted a petition to the Federal Communications Commission (FCC) arguing that three Gulf sovereign wealth funds holding a combined 38.5% equity stake in the company is not merely permissible under federal communications law, but actively serves the public interest of American broadcast television. The filing is the latest regulatory milestone in Paramount‘s proposed $111 billion acquisition of Warner Bros. Discovery (WBD), a deal that requires FCC sign-off on foreign ownership levels that significantly exceed the statutory 25% threshold under Section 310(b)(4). With WBD shareholders having already approved the transaction, the FCC process is now the critical path.

What follows is an analysis of what Paramount actually argued in the petition, why those arguments are structured the way they are, how the regulatory machinery processes them, and what the deal’s foreign ownership profile signals about the broader pressures reshaping American broadcast media.

The petition, directed to an FCC currently led by Chair Brendan Carr, addresses only the foreign financing component of the transaction, not the acquisition itself. Paramount‘s own characterisation of the filing reinforces that distinction.

Paramount spokesperson statement: The filing represents “standard practice for investments of this nature.”

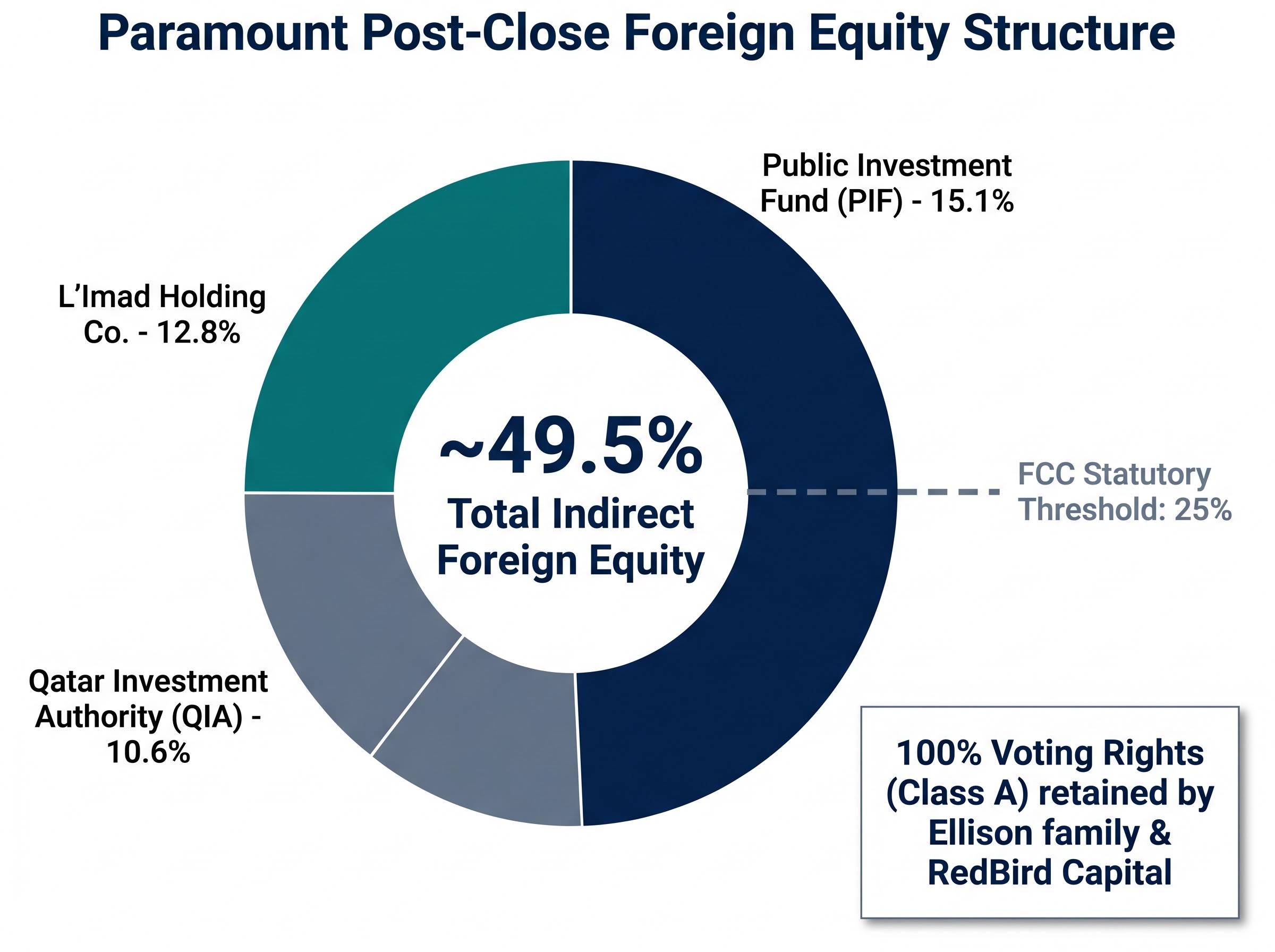

Standard practice or not, the numbers under review are substantial. Post-close, total indirect foreign equity in the combined entity would reach approximately 49.5%, nearly double the statutory threshold. The three sovereign wealth funds contributing that capital break down as follows:

Between them, those three funds account for a combined 38.5% non-voting stake in Paramount equity, and it is that figure on which the FCC’s public interest determination will turn. The petition is not a formality. It is the legal document on which a $111 billion deal now pivots.

Section 310(b)(4) of the Communications Act caps foreign equity or voting interest in entities holding FCC broadcast licences at 25%. Exceeding that threshold is not automatically prohibited, but it does require a formal petition demonstrating the arrangement serves the “public interest.” The provision reflects a deliberate congressional choice: foreign participation in American airwaves is permitted, but only under regulatory oversight.

The petition process follows a defined sequence:

Paramount is simultaneously providing responses to Team Telecom as part of a parallel review process, meaning two regulatory tracks are running concurrently.

On 29 January 2026, the FCC adopted reforms that codified the foreign ownership petition process and introduced a formal definition of “controlling U.S. parent,” a term designed to provide regulatory certainty about which domestic entity bears compliance obligations. The reforms also enhanced national security reporting requirements for foreign-backed media entities.

The FCC Report and Order updating Section 310(b)(4) foreign ownership rules, published in the Federal Register on 9 April 2026, codified the ‘controlling U.S. parent’ definition and streamlined the declaratory ruling petition process, creating the precise legal pathway Paramount is now navigating.

These changes are directly relevant. The codified definition of “controlling U.S. parent” creates the specific legal pathway Paramount is now navigating, while the emphasis on national security sets up the tension the petition must address: demonstrating that sovereign wealth fund capital flowing into an FCC-licensed entity poses no threat to the interests those reforms were designed to protect.

Delrahim‘s petition constructs three affirmative arguments, each designed to satisfy a different dimension of the FCC’s public interest standard.

Delrahim’s framing of the public interest case: The petition argues that the arrangement “increases competitiveness in the broader video marketplace” and positions the combined entity to invest in broadcast programming at a scale that the current capital structure cannot sustain.

The petition also includes a request for authorisation for up to 100% foreign equity or voting shares. This is standard legal practice in declaratory ruling petitions, designed to provide flexibility for future ownership changes without requiring a new filing. It does not reflect an operational intention to transfer full ownership to foreign entities.

Each argument is calibrated to address a specific FCC concern. The broadcast investment argument speaks to the Commission’s mandate to support local and national programming. The programming diversity argument provides tangible evidence. The competitiveness argument frames the deal as strengthening, not weakening, the American media sector. Together, they form the legal record on which the FCC will render its determination.

Democratic senators including Elizabeth Warren and Richard Blumenthal have publicly challenged the premise that non-voting equity removes foreign influence. Their criticism frames the arrangement as raising “serious national security concerns” and calls on FCC Chair Carr to conduct a rigorous Section 310(b)(4) review rather than treating the petition as procedural.

Separately, Knowledge Ecology International (KEI) filed a petition with the Committee on Foreign Investment in the United States (CFIUS) on approximately 22 April 2026, directly disputing the assumption that non-voting structures place transactions beyond CFIUS jurisdiction. KEI argued that minority investments can still afford access to decision-makers and influence over strategic direction.

| Actor | Position | Key Argument | Regulatory Body Addressed |

|---|---|---|---|

| FCC Chair Brendan Carr | Favourable disposition | Deal is “a lot cleaner” than a prior Netflix offer | FCC |

| Senate critics (Warren, Blumenthal) | Opposed / seeking rigorous review | Arrangement raises “serious national security concerns” | FCC, CFIUS |

| Knowledge Ecology International | Opposed / challenging non-voting premise | Non-voting equity does not remove CFIUS jurisdiction; minority stakes can still confer access | CFIUS |

Under Foreign Ownership, Control, or Influence (FOCI) guidelines, non-voting equity structures can mitigate foreign influence concerns when they do not confer control. Board resolutions limiting foreign voting stock are one example of such mitigation. However, regulatory experts note that these structures do not automatically remove transactions from CFIUS or FCC jurisdiction.

The residual ambiguity is where the debate lives. Non-voting equity can limit formal governance power while still affording access to management, strategic discussions, and operational intelligence. KEI’s petition to CFIUS targets precisely this gap, arguing that influence can persist below the formal voting threshold. The Ellison family and RedBird Capital retain 100% of Class A Common Stock, meaning all voting rights remain with domestic holders. Whether that structural separation is a genuine safeguard or legal architecture designed to satisfy a regulatory threshold is the question the FCC must now answer.

Treasury’s official guidance on CFIUS jurisdiction over non-controlling minority foreign investments clarifies that FIRRMA expanded the committee’s remit to cover certain passive stakes where the foreign investor gains access to material non-public technical information or board observer rights, the precise channels KEI’s petition identified as potential influence vectors.

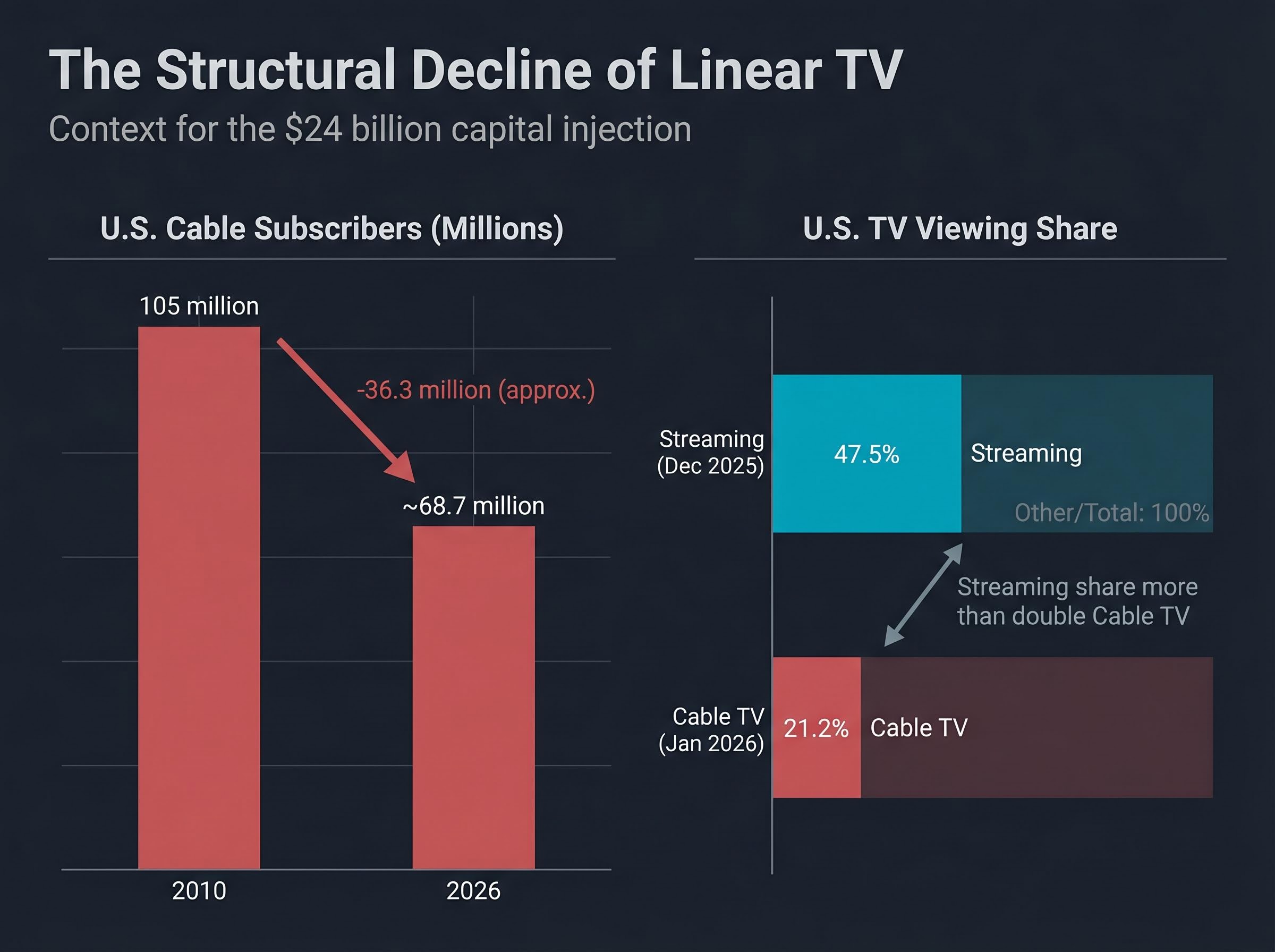

The $24 billion in sovereign wealth fund capital is not incidental to the deal structure. It is the deal structure. The economic backdrop that makes it necessary is the accelerating collapse of traditional television revenue.

Streaming reached 47.5% of U.S. TV viewing in December 2025. Cable TV fell to 21.2% of viewing share as of January 2026.

Nielsen’s The Gauge measurement of streaming’s 47.5% U.S. TV viewing share in December 2025 marked the category’s highest recorded monthly figure, underscoring that the structural erosion of linear television is not cyclical but a durable redistribution of audience attention toward on-demand platforms.

The decline has been steep and sustained:

The merger’s logic, combining Paramount+ and Max, pooling content libraries, and achieving scale against Netflix, Disney+, and Amazon Prime Video, only works with a capital infusion that organic operations cannot provide. Paramount certified substantial compliance with the DOJ’s second request for information on 9 February 2026, clearing the antitrust track, but the FCC petition is where the financial reality meets the regulatory question.

The argument in Paramount‘s petition that foreign capital enables broadcast investment is inseparable from the argument that without it, broadcast investment will contract. That is not a legal manoeuvre. It is a reflection of an industry where the traditional revenue base that once funded broadcast television no longer exists at scale.

Paramount‘s legal team has constructed a public interest argument that ties foreign sovereign capital directly to the survival of broadcast television. The FCC must now decide whether that argument is compelling, or whether national security concerns override it.

The ruling will carry consequences beyond the transaction itself. A favourable determination would set a precedent for how much foreign sovereign wealth fund capital can flow into U.S. media at a moment when linear TV’s economics make that capital increasingly attractive to broadcasters. A protracted review, or one that imposes onerous conditions, would signal that the 25% threshold retains real force even when non-voting structures are in place.

The next milestones are the FCC’s public interest determination and the parallel Team Telecom review. Investors and media observers tracking the transaction should monitor FCC Electronic Comment Filing System (ECFS) filings for the declaratory ruling proceeding as the authoritative source for developments.

Team Telecom’s review window of up to 120 days, with a possible 30-day extension, means the Q3 2026 close target for the WBD merger is directly exposed to the pace of national security deliberations, with the FCC’s own declaratory ruling running on a separate track that must also resolve before the transaction can complete.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding regulatory outcomes and deal timelines are subject to change based on regulatory proceedings, market developments, and evolving policy considerations.

The Paramount FCC petition is a declaratory ruling request filed on 27 April 2026 asking the FCC to approve foreign equity levels in the proposed Paramount-Warner Bros. Discovery merger that exceed the statutory 25% threshold under Section 310(b)(4) of the Communications Act. Paramount's chief legal officer Makan Delrahim filed the petition to demonstrate that three Gulf sovereign wealth funds holding a combined 38.5% non-voting equity stake serves the public interest of American broadcast television.

Three Gulf sovereign wealth funds hold non-voting equity stakes in Paramount: the Public Investment Fund (PIF) of Saudi Arabia at 15.1%, L'Imad Holding Co. of the UAE at 12.8%, and the Qatar Investment Authority (QIA) at 10.6%, combining for a total of 38.5% indirect foreign equity in the company.

Paramount argues that the Gulf sovereign capital will fund expanded broadcast television investment, enable content acquisitions such as UFC broadcast rights that would otherwise be unaffordable, and improve the merged entity's competitive positioning against streaming-native rivals like Netflix and Amazon Prime Video.

Democratic senators including Elizabeth Warren and Richard Blumenthal argue that non-voting equity does not eliminate foreign influence and raises serious national security concerns, while Knowledge Ecology International filed a separate CFIUS petition arguing that minority stakes can still grant access to management and strategic direction even without formal voting rights.

The applicant files a declaratory ruling petition with the FCC disclosing the foreign ownership structure, the FCC then refers the matter to Team Telecom for a national security review that can take up to 120 days with a possible 30-day extension, and the FCC subsequently issues a public interest determination approving, conditioning, or denying the petition.