Record Highs Are Not the Risk Most Investors Think They Are

6 hrs ago

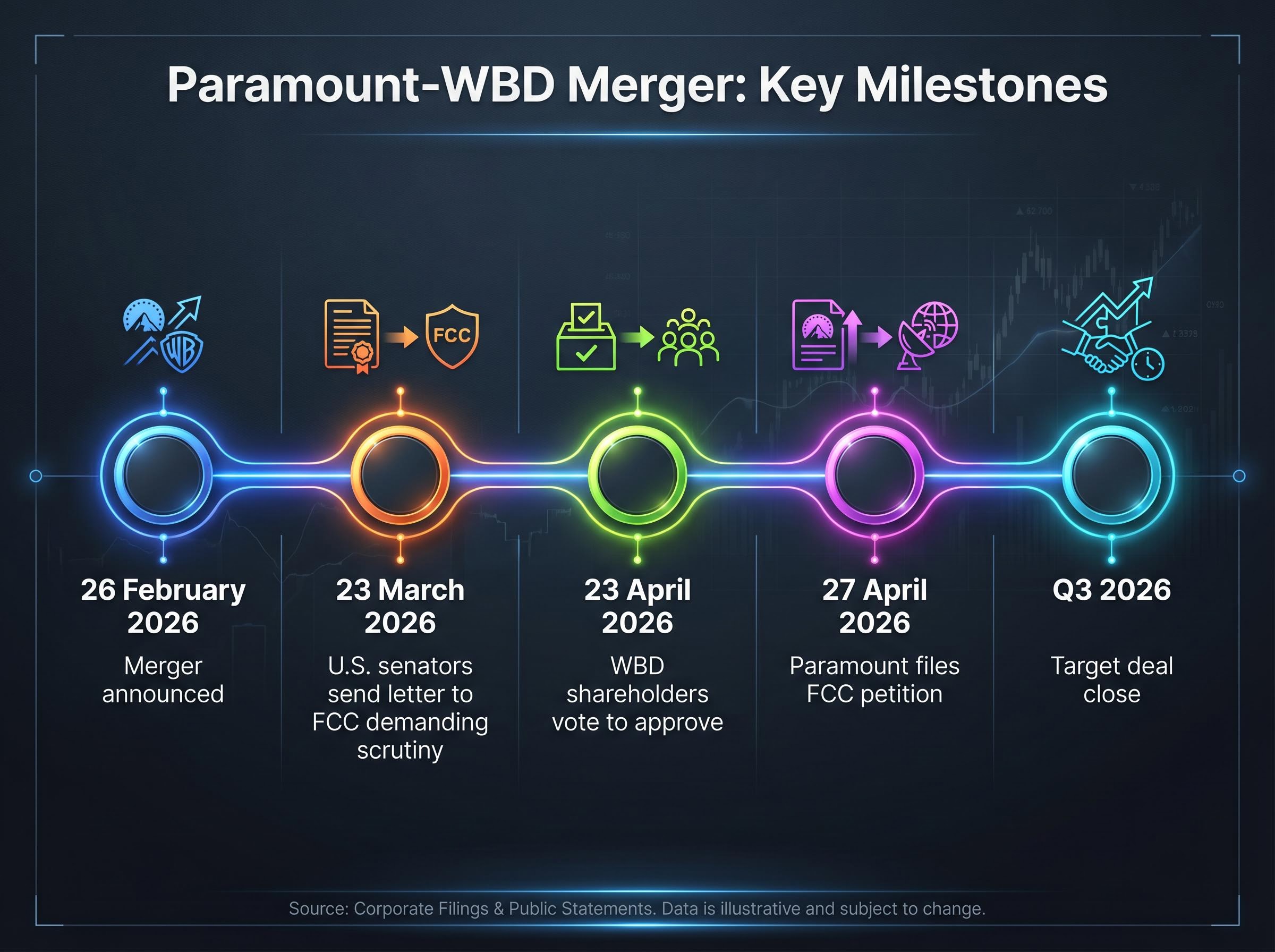

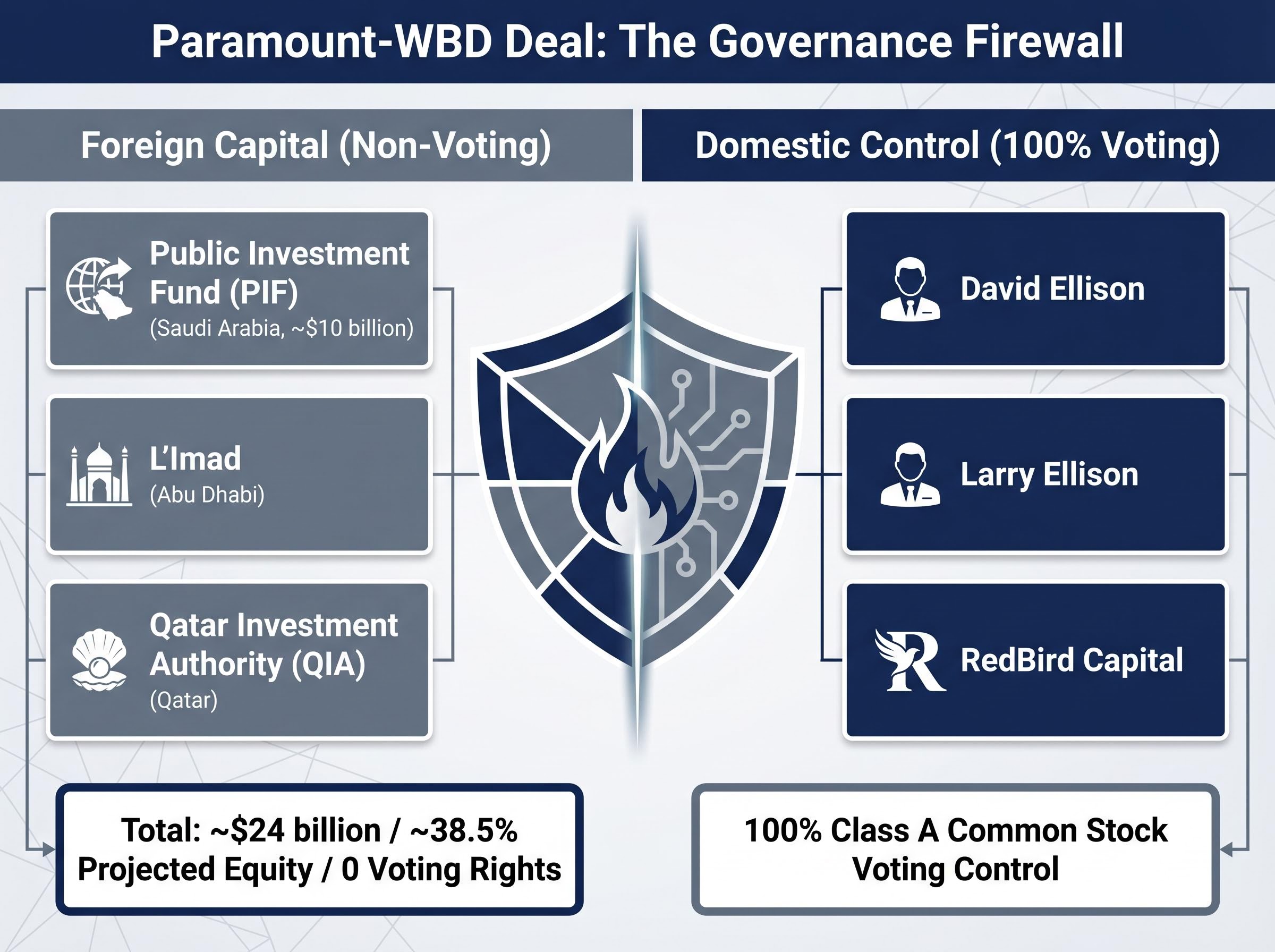

“`json { “fact_checked_full_article”: “Paramount Global filed a petition with the Federal Communications Commission (FCC) on 27 April 2026, requesting authorisation for three Middle Eastern sovereign wealth funds to collectively invest $24 billion in the company’s $111 billion acquisition of Warner Bros. Discovery. The filing, signed by Paramount Chief Legal Officer Makan Delrahim, arrives four days after WBD shareholders voted to approve what would become the largest media merger in history. The FCC petition covers only the foreign financing component of the deal, not the broader transaction, but it marks a significant procedural milestone in a process that has drawn scrutiny from U.S. senators, Hollywood creatives, and national security reviewers. What follows is a breakdown of the petition’s scope, the investor structure behind it, how the FCC review process works, Paramount’s affirmative case to the commission, and what remains before an expected Q3 2026 close.\n\n## Paramount’s FCC petition asks for up to 100% foreign equity authorisation\n\nThe petition filed on 27 April 2026 is a formal request for a declaratory ruling, the FCC’s procedural mechanism for authorising foreign investment in U.S. broadcast licensees above statutory thresholds. Delrahim’s filing asks the commission to approve up to 100% foreign equity or voting ownership in Paramount’s broadcast licence holdings, a figure that reads as dramatic but functions as a regulatory ceiling rather than a statement of planned ownership.\n\nThe actual projected post-close foreign equity in Paramount sits at approximately 49.5%, well below the authorisation request. Filing for the maximum is standard practice in these petitions; it provides the company with flexibility without requiring a new filing if ownership percentages shift marginally over time.\n\n> A Paramount spokesperson characterised the filing as \”customary\” for transactions involving indirect foreign investment in broadcast television stations.\n\nThe petition is not a prerequisite for deal closing. It runs on its own regulatory track. But it creates the formal public record the FCC will evaluate, and it is the document that Team Telecom, the government’s national security review body, will use as the basis for its advisory assessment.\n\n## Three Gulf funds, one governance firewall: how the equity structure works\n\nThe $24 billion in sovereign wealth fund capital comes from three participants, each taking a non-voting equity stake in Paramount post-close.\n\n

| Fund | Country | Projected Equity Stake | Dollar Contribution | Voting Rights |

|---|---|---|---|---|

| Public Investment Fund (PIF) | Saudi Arabia | Not publicly disclosed | ~$10 billion | None |

| L’Imad | Abu Dhabi | Not publicly disclosed | Not publicly disclosed | None |

| Qatar Investment Authority (QIA) | Qatar | Not publicly disclosed | Not publicly disclosed | None |

| Total | ~38.5% | ~$24 billion | None |

\n

\n\nAll three funds receive non-voting equity only. No board seats. No governance rights. The combined $24 billion stake is substantial by dollar value but carries zero influence over editorial, programming, or corporate decision-making.\n\n### Ellison family and RedBird Capital retain exclusive voting control\n\nClass A Common Stock, representing 100% of voting rights, remains exclusively with David Ellison, Larry Ellison, and RedBird Capital. This structure was explicitly highlighted in the FCC petition as the governance safeguard underpinning the declaratory ruling request. David Ellison is set to serve as Chairman and CEO of the combined entity post-close.\n\nThe firewall is the deal’s primary defence against the national security objections raised by U.S. senators. With voting control entirely domestic, the FCC’s assessment shifts from a question of foreign governance influence to one of whether the financial participation itself presents security concerns, a narrower and historically more navigable review.\n\n## What the FCC declaratory ruling process actually means for this deal\n\nThe FCC caps foreign ownership of U.S. broadcast licensees at 25%. Any transaction that would push foreign equity above that threshold requires a formal petition for a declaratory ruling, a waiver process that the commission updated and streamlined in January 2026.\n\nThe process is well-established and follows a defined sequence:\n\n1. Petition filed with the FCC (completed 27 April 2026)\n2. Team Telecom national security review, in which the Committee for the Assessment of Foreign Participation in the United States Telecommunications Services Sector evaluates the foreign investors and advises the FCC\n3. FCC public comment period, during which interested parties (including senators, industry groups, and the public) can submit views\n4. FCC ruling, in which the commission grants, denies, or conditions the declaratory ruling\n\nTeam Telecom’s review runs parallel to the broader merger approval process, not in sequence with it. Paramount confirmed on 27 April 2026 that it is already responding to Team Telecom inquiries, suggesting the national security review is underway.\n\n> FCC Chair Brendan Carr has publicly described the broader Paramount-WBD deal as \”a lot cleaner\” than a prior Netflix proposal for WBD, signalling a disposition that has drawn criticism from senators who characterised the comment as premature.\n\nThe declaratory ruling process does not block deal closing on its own timeline. For investors tracking the Q3 2026 target, the FCC petition is a regulatory step running on a separate track from antitrust clearance, and its procedural nature makes it a standard hurdle rather than an existential one.\n\n## Paramount’s case to the FCC: foreign capital will strengthen local broadcast\n\nDelrahim’s written arguments to the commission centre on a straightforward proposition: reduced barriers to foreign capital will enable Paramount to sustain and expand its broadcast television operations. The filing makes four specific broadcast benefit claims:\n\n- Local news investment: Capital from the deal will support continued investment in CBS-owned local news operations across Paramount’s broadcast licence portfolio\n- Technology infrastructure: Upgraded broadcast technology and digital distribution capabilities funded by expanded capital resources\n- Programming diversity: The filing cites the UFC broadcast rights agreement as an illustration of expanded programming variety resulting from deal synergies with Skydance\n- Competitive positioning: Skydance operational efficiencies combined with the capital injection are positioned to strengthen Paramount’s ability to compete in an increasingly consolidated media environment\n\nThe arguments follow the standard template for successful declaratory ruling petitions, which require the applicant to demonstrate that foreign investment serves the public interest.\n\nThe political environment around the petition is contested. On 23 March 2026, U.S. senators sent a letter to FCC Chair Carr demanding scrutiny of sovereign wealth fund involvement, explicitly raising national security concerns about government-affiliated foreign capital in American broadcast media. Separately, a Hollywood petition opposing the broader merger gathered over 4,000 signatures, including Robert De Niro and Sofia Coppola, citing consolidation concerns and potential impacts on creative diversity.\n\nParamount’s affirmative case will be weighed against these objections on the public record. The strength of the broadcast benefit argument matters because it forms the legal basis on which the FCC can justify approval in the face of political pressure.\n\n## What comes next on the path to a Q3 2026 close\n\nWBD shareholders approved the merger on 23 April 2026. The FCC petition filed today covers the foreign financing component only. Several regulatory milestones remain before the deal can close:\n\n1. Team Telecom national security review completion, the primary open variable affecting the timeline\n2. FCC declaratory ruling on foreign ownership, dependent on Team Telecom’s advisory and the public comment period\n3. FCC broadcast licence transfer approval, covering the transfer of CBS and other broadcast licences to the combined entity\n4. DOJ/FTC antitrust clearance, ongoing with no clearance issued as of 27 April 2026\n5. Deal close, targeted for Q3 2026\n\n### Key dates and milestones at a glance\n\nThe confirmed timeline so far: the merger was announced on 26 February 2026, WBD shareholders voted to approve on 23 April 2026, and Paramount filed its FCC petition on 27 April 2026. The Q3 2026 close target remains the company’s stated expectation, with Team Telecom’s review timeline the single variable most likely to determine whether that window holds.\n\nThe FCC petition filed today is a procedural milestone in a deal that carries significant momentum. The non-voting governance structure, with all Class A voting stock held domestically by the Ellison family and RedBird Capital, was designed specifically to address the national security concerns senators have raised. The genuine open variables remain Team Telecom’s advisory timeline and the DOJ/FTC antitrust outcome, both unresolved as of today. Political pressure on FCC Chair Carr from senators adds a layer of uncertainty to the declaratory ruling process, but the commission’s updated foreign ownership rules and Carr’s own public comments suggest a regulatory environment that is navigable rather than adversarial. The next material signal will come from Team Telecom.\n\nThis article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.” } “`

Team Telecom’s national security review mandate and timeline guidance establishes that the Committee can take up to 120 days to complete its assessment, with a possible 30-day extension, making it the single regulatory variable most capable of compressing or stretching the Q3 2026 close window.

The FCC’s January 2026 update to foreign ownership rules for broadcast licensees formally codified the declaratory ruling petition process and reaffirmed the 25% statutory cap on indirect foreign equity, providing the procedural foundation Paramount’s filing relies on.

The Paramount and Warner Bros. Discovery merger is a $111 billion deal that would become the largest media merger in history, combining two of the world's biggest entertainment companies under a new entity led by David Ellison as Chairman and CEO.

The FCC caps foreign ownership of U.S. broadcast licensees at 25%, so Paramount must file a formal petition for a declaratory ruling to authorise the approximately 38.5% combined equity stake held by three Middle Eastern sovereign wealth funds contributing $24 billion to the deal.

Saudi Arabia's Public Investment Fund (contributing approximately $10 billion), Abu Dhabi's L'Imad, and the Qatar Investment Authority are the three Gulf sovereign wealth funds providing a combined $24 billion in non-voting equity financing for the deal.

No. All three funds receive non-voting equity only, with zero board seats or governance rights. All Class A voting shares remain exclusively with David Ellison, Larry Ellison, and RedBird Capital, which the FCC petition highlights as the key governance safeguard.

The deal is targeted to close in Q3 2026, but the primary variable affecting that timeline is Team Telecom's national security review, which can take up to 120 days plus a possible 30-day extension, alongside pending DOJ/FTC antitrust clearance.