How Hormuz Closure at $104 Oil Is Reshaping Every Asset Class

10 hrs ago

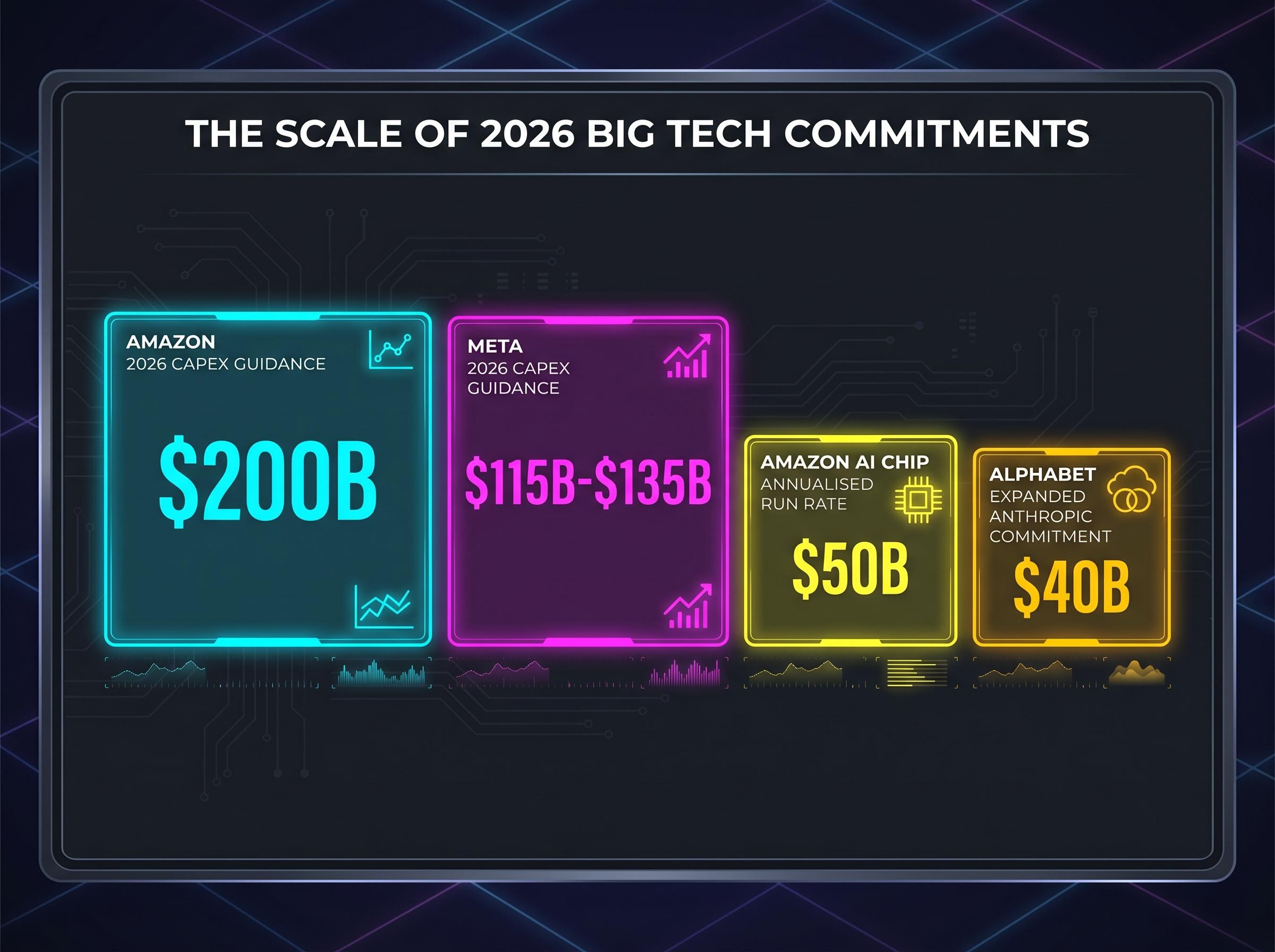

“`json { “fact_checked_full_article”: “Four of the most market-moving companies on earth report earnings on the same afternoon this Wednesday, 29 April, and the arithmetic alone explains why the session matters. Microsoft, Amazon, Meta Platforms, and Alphabet collectively account for more than 18% of the S&P 500 by index weighting. Both the S&P 500 and the Nasdaq Composite entered the week at fresh all-time highs, but the rally has been shaped by tariff uncertainty, questions about whether artificial intelligence spending is converting into earnings growth, and Federal Reserve ambiguity on rate policy. With all four companies reporting in the same after-hours window, Wednesday’s results will offer the clearest read yet on whether Big Tech’s AI investment cycle is accelerating shareholder returns, or compressing margins under the weight of capital intensity. What follows is a company-by-company preview of what analysts expect, the specific narrative threads that will drive post-earnings reactions, and what the collective results could signal for the broader market heading into May.\n\n## Why April 29 is the most consequential single earnings day of 2026\n\nThe weight on the table is difficult to overstate. Four companies, one afternoon, more than 18% of the S&P 500 by market capitalisation.\n\n> Combined S&P 500 weighting: Microsoft, Amazon, Meta, and Alphabet together represent over 18% of the index, meaning their collective after-hours movement can mechanically gap the S&P 500 open the following morning.\n\nBoth indices enter Wednesday at all-time highs, with broad S&P 500 earnings growth for 2026 expected at approximately 18.6%. The AI narrative has rewarded some names selectively while punishing others on capex concerns earlier in the year. That selectivity will be tested when all four report in the same concentrated window, creating a volatility event with no calendar equivalent.\n\nHere is what each company brings to the afternoon:\n\n- Microsoft: Azure cloud growth trajectory and Copilot monetisation as the AI revenue conversion test\n- Meta Platforms: Whether 31% revenue growth can absorb $115B-$135B in capex guidance without compressing free cash flow\n- Alphabet: AI infrastructure spending versus earnings-per-share delivery, plus the $40B Anthropic investment signal\n- Amazon: AWS margin expansion, tariff exposure in retail and logistics, and the $200B capex commitment\n\n## What analysts expect from Microsoft and Meta this Wednesday\n\nThe consensus numbers are the starting point, not the destination. For both companies, the forward guidance and management commentary on AI monetisation will likely move shares more than whether the headline figures land above or below the line.\n\n

| Company | Revenue Consensus | YoY Growth | EPS Consensus | EPS YoY Growth |

|---|---|---|---|---|

| Microsoft | $81.4B | +16% | $4.06-$4.07 | +17% |

| Meta Platforms | $55.49-$55.57B | +31% | $6.65-$6.71 | +3-4% |

\n

\n\n### Microsoft: Copilot and the Azure inflection test\n\nAzure’s company-guided growth rate of approximately 16% at the midpoint is the figure institutional investors will measure everything else against. A beat signals that enterprise AI workload demand is accelerating; a miss reopens the question of whether cloud growth has peaked for the cycle.\n\nBloomberg reported that Microsoft’s decision to charge separately for Copilot, rather than bundling it at no cost within existing software packages, has proven remarkably effective, with the company surpassing what sources described as \”audacious\” internal sales targets in the most recent quarter. That outcome eases the \”software cannibalisation\” concern that weighed on the stock earlier in the year. Meanwhile, Microsoft’s reworked OpenAI partnership, which secured an approximately 27% equity stake and non-exclusive licensing rights, gives the company strategic flexibility in how it manages AI partnership exposure going forward.\n\n### Meta: revenue strength versus capex absorption\n\nMeta’s tension is unusually visible in the estimates themselves. Revenue growth of +31% year-over-year is exceptional by any standard. Yet EPS growth of just +3-4% tells the cost story: $115B-$135B in 2026 capex guidance represents one of the largest infrastructure commitments in corporate history, and it is compressing free cash flow even as the top line surges.\n\nThe 10% workforce reduction announced on approximately 23 April 2026 adds a second layer, with the company reportedly cutting around 8,000 roles in a move that analysts expect to influence near-term profitability. Meta is cutting operating expenses at the labour line while spending aggressively at the infrastructure layer, a combination analysts will parse for operating leverage signals. On the product side, Meta unveiled a substantially rebuilt AI model this month called Muse Spark, which quickly gained traction with users following its launch on 8 April 2026; early adoption metrics could shape how the market models 2027 revenue contribution.\n\n## What analysts expect from Alphabet and Amazon this Wednesday\n\nThe risks here are more distinctive. Alphabet’s numbers tell a story of revenue strength undermined by AI-driven margin compression. Amazon’s carry the added wildcard of direct tariff sensitivity that none of the other three companies face to the same degree.\n\n

| Company | Revenue Consensus | YoY Growth | EPS Consensus | Key Risk / Watch Item |

|---|---|---|---|---|

| Alphabet | $92.22B | +20.6% | ~$2.62 | EPS declining YoY despite revenue growth; AI capex compression |

| Amazon | $177.84B | +14.2% | ~$1.63 | Tariff exposure in retail/logistics; Q2 guidance uncertainty |

\n

\n\n### Alphabet: the AI investment paradox\n\nRevenue growth above 20% coexisting with a year-over-year EPS decline is the paradox that will define Alphabet’s earnings reaction. The explanation is structural: server and data centre buildouts compress margins in the near term while positioning Cloud and Search monetisation for longer-term acceleration.\n\nAlphabet secured a new five-year agreement with Broadcom to develop next-generation Tensor Processing Units (TPUs), custom chips that have found strong demand among Google Cloud customers who value competitive pricing and flexibility. Separately, the company is reportedly preparing to commit a further $40 billion to AI developer Anthropic, adding to the approximately 14% stake it already holds. Anthropic’s Claude model has established itself as a leading AI system, and a potential Anthropic listing in 2026 could generate a substantial return for Alphabet shareholders. The $40B Anthropic investment, announced on 24 April 2026, deepens this dynamic. Alphabet already held an approximately 14% stake; the expanded commitment, alongside its Broadcom TPU partnership, signals a willingness to absorb short-term margin pressure for strategic AI positioning. If margin questions dominate the earnings call, the prospect of an Anthropic IPO in 2026 is the optionality argument management may lean on.\n\n### Amazon: tariffs, AWS, and the $200 billion question\n\nAmazon is the hardest of the four to model, and tariffs are the reason. Retail and logistics operations carry direct cost sensitivity to tariff policy changes, making Q2 guidance more uncertain here than for any peer in the cohort.\n\nShares came under pressure earlier in the year after Amazon disclosed an intention to deploy $200 billion in capital expenditure during 2026, a commitment that unsettled investors at the time. In the annual shareholder letter, CEO Andy Jassy pushed back against that reaction, pointing out that the company’s AI chips business alone is running at an annualised revenue rate of $50 billion and expanding at over 100% per year, and that existing customer commitments already underpin nearly all of the planned 2026 capex outlay.\n\nThree specific items to watch on the earnings call:\n\n1. AWS margin trajectory: The $36.8B revenue consensus is the headline, but margin expansion (or contraction) will determine whether investors view cloud as the earnings engine or a capital sink\n2. Q2 guidance language: How specifically management addresses tariff-related cost headwinds will set the tone for the stock’s reaction\n3. Capex credibility: CEO Andy Jassy stated in the annual shareholder letter that nearly all of Amazon’s planned $200B in 2026 capex is covered by existing customer commitments; how analysts receive that framing will shape the after-hours move\n\nAmazon also reached a deal to purchase satellite operator Globalstar in a transaction valued at $11.57B (announced approximately 14 April 2026), a move designed to bolster its Project Kuiper satellite connectivity ambitions and expand the ways in which the company can reach consumers directly, though it is unlikely to be the primary focus on Wednesday’s call. Jassy’s claim that the AI chip business has reached an annualised run rate of $50B, growing over 100% annually, is the demand-side data point that may carry the most weight.\n\n## The cloud battle hiding inside one earnings afternoon\n\nAzure, AWS, and Google Cloud almost never report in the same after-hours window. On Wednesday, they do. The result is the most direct competitive comparison of cloud growth rates available in a single session all year.\n\nThe benchmarks are set. Azure is company-guided at approximately 16% growth at the midpoint. AWS consensus sits at approximately $36.8B in quarterly revenue. Google Cloud’s trajectory will be embedded in Alphabet’s overall results, requiring investors to isolate the segment from the broader business.\n\nWhat makes this comparison more than a revenue horse race is what it signals about AI workload demand. Enterprise AI spending flows predominantly through these three platforms, meaning cloud growth rates are functioning as proxy demand indicators for the broader AI infrastructure thesis.\n\n- Azure (Microsoft): Guided ~16% growth; AI differentiation through Azure OpenAI Service and Copilot integration; watch item is whether guidance lifts above the midpoint\n- AWS (Amazon): ~$36.8B consensus; differentiation via Trainium chips and Bedrock platform; margin expansion is the key variable\n- Google Cloud (Alphabet): Embedded in overall results; differentiation via custom TPUs and Anthropic partnership; risk is that AI capex compresses segment margins before revenue scales\n\n> Demand signal: CEO Andy Jassy stated that Amazon’s AI chip business has reached an annualised run rate of $50B, growing over 100% annually, a figure that, if confirmed in earnings detail, anchors the supply-side credibility of cloud AI demand.\n\nConvergence in growth rates would suggest the market is expanding broadly. Divergence would indicate that one platform is gaining share at the others’ expense, a signal with direct implications for how investors model multi-year cloud revenue across all three companies.\n\n## Understanding why Big Tech earnings move the whole market\n\nThe S&P 500 is a market-capitalisation-weighted index. That means a company’s share price movement affects the index in proportion to its total market value, not equally alongside every other constituent. A $3 trillion company moving 2% has a far greater index impact than a $10 billion company moving 10%.\n\nThis is why Wednesday afternoon matters beyond the four individual stocks. When companies with a combined weighting above 18% all report in the same session, even a modest uniform reaction, say 3-4% in after-hours trading, can produce a meaningful gap in the S&P 500’s opening price the following morning.\n\n- If all four stocks move +5% after hours, the mechanical index contribution alone could push the S&P 500 higher by roughly 0.9% or more at the open, before any broader market reaction\n- If the reaction is split (two up, two down), the index effect partially offsets, but sector-level volatility still rises\n\nAny investor holding an S&P 500 index fund has automatic, concentrated exposure to these four names through what is commonly referred to as the \”Magnificent Seven\” cohort. Institutional investors typically hedge around concentrated earnings events like this, and that hedging activity, through options positioning and implied volatility adjustments, is itself a source of market movement in the days surrounding the reports.\n\nIn aggregate, Microsoft, Amazon, Meta Platforms, and Alphabet represent more than 18% of the S&P 500, which means the collective verdict from Wednesday’s calls will be scrutinised by anyone with a stake in where technology and the broader market are headed.\n\n## What a strong or weak earnings sweep would signal for the market in May\n\nPredicting outcomes is less useful than preparing for them. Two scenarios frame what Wednesday’s results could mean for the market’s direction into Q2.\n\n1. Bullish sweep: all four beat, guide confidently\n – Revenue beats across the board, accompanied by improving cloud growth rates and forward guidance that signals sustained enterprise AI demand\n – Management tone is confident on return on AI investment, with specific monetisation metrics rather than vague commitments\n – Implication: the AI spending cycle is generating returns, the macro environment has not materially crimped tech budgets, and index strength into Q2 has fundamental support\n\n2. Bearish disappointment: guidance hedges, cloud underwhelms\n – Cloud growth rates disappoint relative to elevated expectations, or tariff commentary from Amazon signals Q2 cost pressure in retail and logistics\n – Meta’s workforce reduction is interpreted as defensive rather than disciplined, and Alphabet’s $40B Anthropic commitment weighs on near-term sentiment because margins disappoint alongside it\n – Implication: the market may interpret the results as confirmation that AI spending is ahead of monetisation, triggering a rotation out of mega-cap tech\n\n### The signal to watch above all others\n\nAzure’s growth rate is the single most-watched data point across the entire afternoon. It anchors the AI monetisation narrative for Microsoft, sets a benchmark for AWS and Google Cloud comparisons, and carries forward guidance implications for the enterprise technology sector broadly.\n\nGuidance language matters as much as the numbers. All four stocks enter Wednesday at elevated valuations following recent all-time highs, which raises the bar for what constitutes a satisfying beat. Confident, specific forward commentary supports the current rally. Hedged or cautious language, particularly around AI return timelines, could shift sentiment quickly.\n\nThis is not a routine earnings week. It is a concentrated, single-afternoon read on whether the AI investment super-cycle is translating into shareholder returns or producing capital intensity without commensurate earnings growth. Azure growth for Microsoft, operating leverage for Meta, EPS trajectory versus Cloud momentum for Alphabet, and tariff sensitivity plus AWS guidance for Amazon: these are the four threads that will unravel or reinforce the market’s thesis by Wednesday evening. The collective tone from these calls will set the narrative for Big Tech through Q2 and likely influence how the broader market prices technology’s resilience heading into summer.\n\nThis article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding earnings expectations and market scenarios are speculative and subject to change based on market developments and company performance.” } “`

Investors exploring whether Amazon’s $200 billion and Alphabet’s expanded AI commitments can translate into operational capacity on schedule will find our full explainer on the physical bottlenecks constraining AI infrastructure delivery, which examines HBM3e memory shortages, grid interconnection queues exceeding 2,100 GW, and TSMC packaging constraints that are already pushing 30-50% of planned 2026 data centre capacity to 2028 or later.

The scale of what is being tested on Wednesday extends beyond four quarterly reports: the $649-$700 billion in combined 2026 capital expenditure committed by Microsoft, Alphabet, Amazon, and Meta, almost entirely directed at AI infrastructure, has no historical precedent as a concentrated corporate capital allocation event, and Wednesday’s calls represent the first serious accountability moment for that commitment.

CRN’s Q4 2025 global cloud market share data from Synergy Research showed AWS holding 28% of the global cloud market and Google Cloud at 14%, establishing the competitive baseline against which Wednesday’s sequential growth figures will be measured by institutional investors tracking share gains and losses across the three platforms.

On 29 April 2026, Microsoft, Amazon, Meta Platforms, and Alphabet all report quarterly earnings in the same after-hours window, making it the most concentrated single-session earnings event of the year for the S&P 500.

The four companies collectively account for more than 18% of the S&P 500 by market capitalisation weighting, meaning even a modest uniform after-hours move across all four can mechanically gap the index open the following morning.

Azure cloud growth is the single most-watched data point: the company guided approximately 16% growth at the midpoint, and a beat or miss on that figure will anchor the AI monetisation narrative for the entire earnings afternoon.

Amazon's retail and logistics operations carry direct cost sensitivity to tariff policy changes, making Q2 guidance more uncertain for Amazon than for any of its three peers reporting on the same afternoon.

Alphabet is reportedly preparing to commit a further $40 billion to AI developer Anthropic, deepening a strategic AI position that may weigh on near-term margins but offers significant optionality if Anthropic proceeds with a public listing in 2026.