Domino’s Falls 9.6% to 52-Week Low After Q1 Miss on All Metrics

15 hrs ago

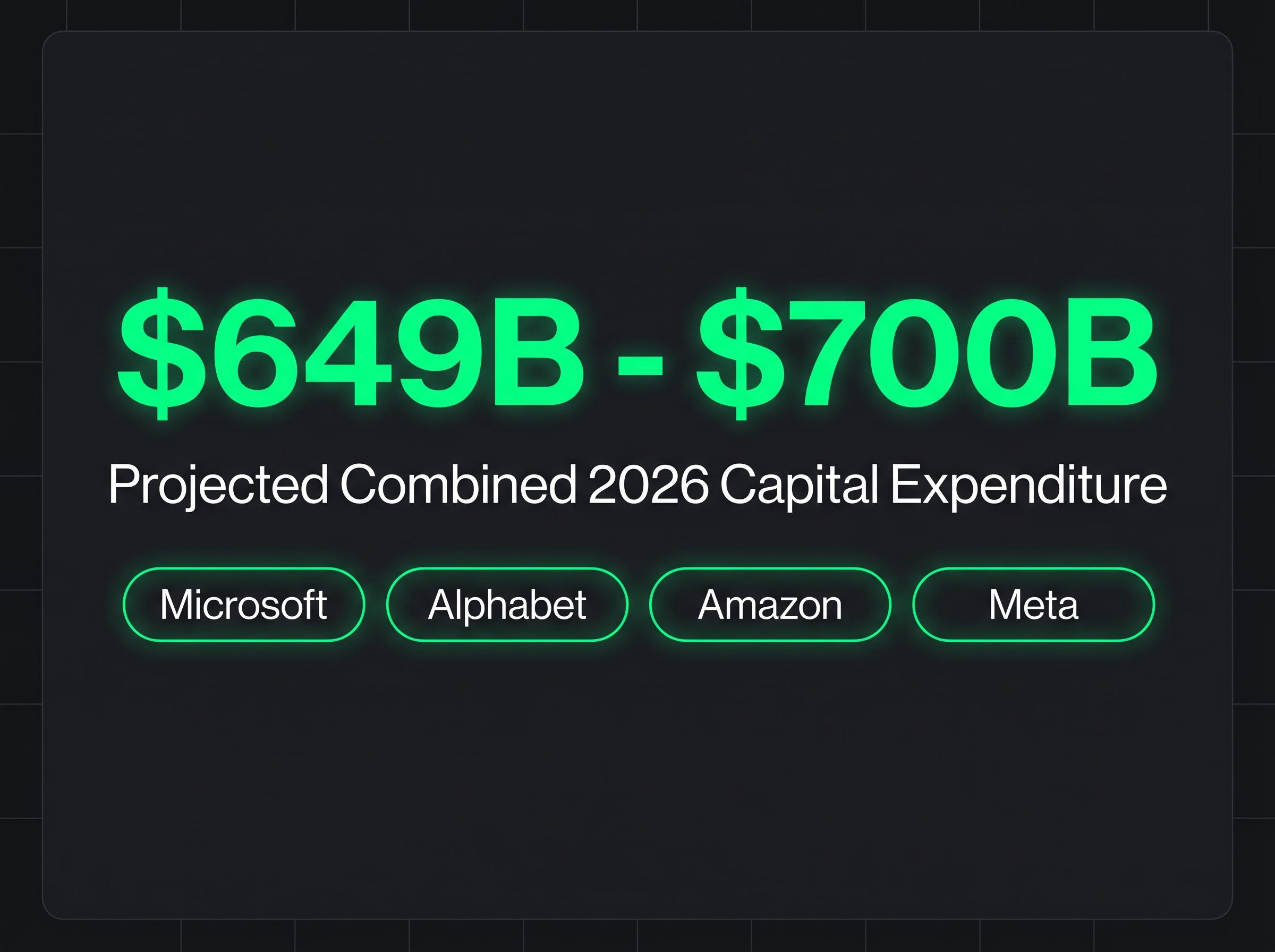

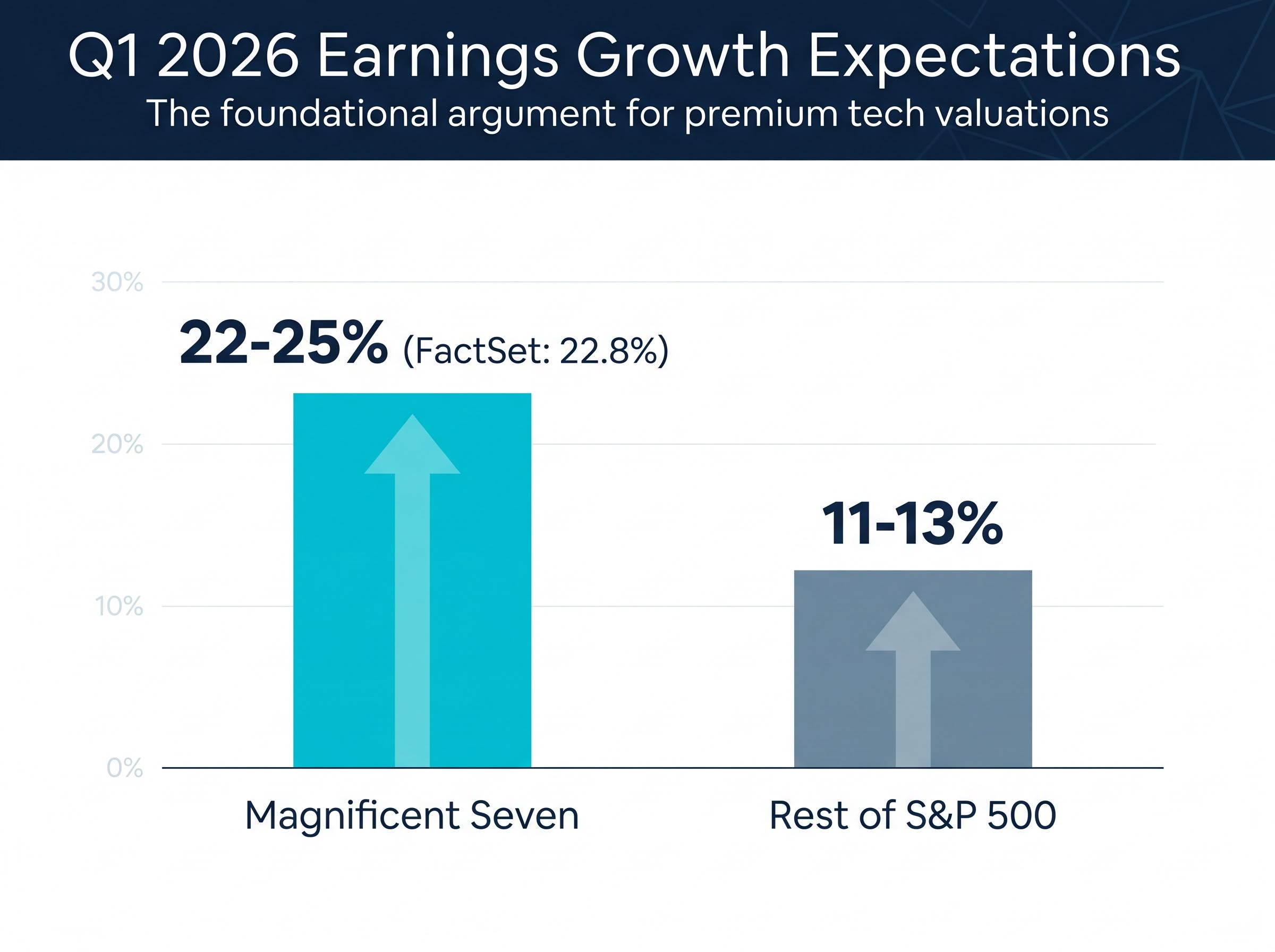

“`json { “fact_checked_full_article”: “Combined 2026 capital expenditure from Microsoft, Alphabet, Amazon, and Meta is projected at approximately $649-$700 billion. This week, investors find out whether that bet is paying off. Between 29 April and 30 April 2026, five of the most closely watched companies in the world report quarterly results in a compressed two-day window, and the stakes extend well beyond individual company performance. After a 10-12% sell-off in Magnificent Seven stocks during March 2026 and a subsequent recovery rally, these earnings reports represent the validation test that market participants have been waiting for. What follows maps the full earnings calendar, unpacks the AI capital expenditure debate at the core of current tech valuations, tracks the contrasting momentum in memory chips, and covers the geopolitical twist that hit Meta before a single result was reported.\n\n## Five companies, two days, and a market looking for answers\n\nFour of the five largest companies by market capitalisation report on the same evening. Alphabet, Microsoft, Amazon, and Meta each release Q1 2026 results on 29 April. Apple follows on 30 April.\n\nThe concentration is unusual, and it arrives at a moment when the market’s recovery narrative has not yet been confirmed by fundamentals. The Magnificent Seven are projected to deliver approximately 22-25% year-on-year Q1 2026 earnings growth (FactSet estimates 22.8%), nearly double the 11-13% expected from the rest of the S&P 500. That differential is the foundational argument for premium tech valuations. If results this week fall short, the argument weakens.\n\n> Growth differential: The Magnificent Seven’s projected 22-25% Q1 2026 earnings growth roughly doubles the 11-13% expected from the remaining S&P 500 constituents.\n\n

| Company | Report Date | Q1 2026 Consensus Revenue | YoY Growth Expectation |

|---|---|---|---|

| Alphabet | 29 April 2026 | ~$106.6B | ~20.6% |

| Microsoft | 29 April 2026 | ~$81.4B | ~16.2% |

| Meta | 29 April 2026 | ~$55B | TBC |

| Amazon | 29 April 2026 | TBC | TBC |

| Apple | 30 April 2026 | TBC | TBC |

\n

\n\n## The $649 billion question: is AI spending going to pay off?\n\nThe number itself is staggering. Microsoft, Alphabet, Amazon, and Meta are collectively projected to spend between $649 billion and $700 billion on capital expenditure in 2026, the vast majority directed at AI infrastructure.\n\n> Combined 2026 capex projection: approximately $649-$700 billion across Microsoft, Alphabet, Amazon, and Meta.\n\nThat scale of commitment triggered part of the March 2026 sell-off, when capex spike announcements helped push Magnificent Seven stocks down by 10-12%. The concern was straightforward: spending is visible and immediate, while AI-driven revenue remains harder to measure and further away. Wellington Management’s Brian Barbetta has noted that sustained investment of this kind can support growth and margins over time, but the \”over time\” qualifier is precisely where investor anxiety sits.\n\nTruist Advisory’s Keith Lerner has framed this earnings week as a test for whether the recent market recovery is justified. The results will be parsed for three specific categories of disclosure:\n\n- Capex guidance updates: any revision to the spending trajectory, up or down\n- Cloud revenue acceleration: whether Azure, Google Cloud, and AWS show AI-linked demand translating into faster top-line growth\n- AI-related revenue disclosure: any new breakouts or metrics that quantify what AI infrastructure is actually generating\n\n## What big tech earnings actually measure: a plain-language explainer\n\nAn earnings report is a quarterly disclosure in which a publicly listed company reveals how much money it brought in, how much it kept, and what it expects going forward. Four components attract the most investor attention:\n\n1. Revenue: total sales for the quarter, the broadest measure of business activity\n2. Earnings per share (EPS): net profit divided by the number of shares outstanding, the single most compared figure against analyst expectations\n3. Operating margin: the percentage of revenue left after operating costs, a measure of efficiency\n4. Forward guidance: management’s projection for the next quarter or full year, often the number that moves the share price most\n\nGuidance matters disproportionately for high-growth companies because their valuations are built on future expectations, not trailing results. A company can report a strong quarter and still see its share price fall if guidance disappoints.\n\nThis week, the consensus estimates provide the benchmark. Alphabet’s Q1 2026 revenue consensus sits at approximately $106.6 billion (up ~20.6% year on year), while Microsoft’s sits at approximately $81.4 billion (up ~16.2%). Note that Microsoft’s fiscal calendar differs from the standard calendar year; its FY26 Q3 covers January to March 2026. A \”beat\” means the reported number exceeds the consensus estimate. A \”miss\” means it falls short.\n\n## Memory chips surge while mega-caps slide: the divergence inside tech\n\nWhile the mega-cap names drifted lower ahead of earnings, a different corner of the technology sector told a sharply different story. Micron gained 4.86% on 27 April 2026. SanDisk rose approximately 1.7% the same session, reaching an intraday open of $1,023.58 and closing at $1,040.98 after recently hitting an all-time high.\n\nThe broader market moved in the opposite direction. The S&P 500 slipped 0.09% and the Nasdaq fell 0.26%.\n\nThe divergence highlights a distinction that headline coverage of \”tech earnings\” often misses. AI infrastructure spending may be an open question for software and platform companies, but for memory chip suppliers, the demand is already translating into near-term revenue. Two forces are driving the gains:\n\n- AI data centre buildouts: large-scale computing infrastructure requires massive memory capacity, and orders are accelerating\n- Storage demand growth: AI model training and inference generate data volumes that compound storage requirements across the supply chain\n\n> Goldman Sachs has noted that Micron alone accounted for 51% of all S&P 500 EPS revisions during a defined recent market period.\n\nMicron’s approximately 168% year-to-date gains confirm this is not a single-session anomaly. Before a single Big Tech earnings report has landed, the memory chip sector is already providing a concrete, data-backed signal about where AI spending is producing measurable returns.\n\n## Meta’s China setback adds a geopolitical dimension to AI dealmaking\n\nOn 27 April 2026, Chinese regulators blocked Meta’s proposed $2 billion acquisition of Manus AI, a Chinese-founded artificial intelligence startup. The deal had been announced in late December 2025. The regulators cited national security concerns.\n\n> Chinese regulators blocked the acquisition on national security grounds, according to reporting from CNN, Reuters, BBC, and Forbes on 27 April 2026.\n\nMeta shares dipped 0.50% in the session. The immediate financial impact was contained, but the strategic implications reach further. The block represents one of the most prominent cross-border AI M&A failures to date, and it introduces a layer of risk that pure financial analysis does not capture. Any Big Tech company seeking to acquire AI assets with Chinese origins or operations now faces heightened regulatory complexity on both sides of the US-China divide.\n\nFor investors tracking Big Tech’s AI strategy ahead of this week’s results, the Manus AI block is a reminder that the barriers to acquiring AI capability are not limited to valuation or integration risk. Geopolitical exposure is now a material consideration.\n\n## The Fed meeting, tariff uncertainty, and what else is moving markets this week\n\nBig tech earnings this week are being interpreted inside a crowded macro environment. Three variables are running in parallel:\n\n- Federal Reserve FOMC meeting (28-29 April 2026): no rate change is widely anticipated, but investor attention is focused on economic commentary and any signals about the inflation and growth outlook\n- Oil prices and geopolitical risk: failed US-Iran diplomatic talks over the weekend pushed crude oil higher and reduced risk appetite, with Strait of Hormuz transit constraints adding to supply uncertainty\n- US-China trade tensions: ongoing tariff and supply chain risks remain a background factor for Big Tech, though company-specific impact data has not yet been confirmed\n\nOn 27 April, the S&P 500 closed at 7,158.70, down 0.09%. The Nasdaq Composite fell 0.26% to 24,772.02. The Dow Jones slipped 0.23% to 49,118.56. None of these moves were severe, but they reflect a market that entered the week cautious rather than euphoric.\n\nEarnings results over the next 48 hours will be read against this backdrop. Distinguishing between company-specific signals and broader market noise will require attention to all three variables simultaneously.\n\n## Looking ahead\n\nThe next 48 hours of earnings results either validate or challenge a market recovery that has been building since the March 2026 sell-off. Three threads are worth tracking closely: whether AI capex commitments show early signs of translating into revenue and improved guidance; whether memory chip momentum continues to serve as a concrete proxy for AI infrastructure demand; and whether the geopolitical dimension illustrated by the Meta-Manus AI block reshapes how investors price Big Tech’s acquisition strategies.\n\nThe Fed decision, earnings beats or misses, and any updated capex guidance will together determine whether the Magnificent Seven’s premium valuation story holds into Q2 2026.\n\nThis article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking projections referenced in this article are subject to market conditions and various risk factors. Past performance does not guarantee future results.\n\n—” } “`

Investors seeking a fuller picture of the forces behind Micron’s gains will find our deep-dive into the semiconductor sector’s April 2026 supercycle rally, which covers the VanEck SOXX ETF’s best monthly return in 25 years, the record $5.45 billion in combined ETF inflows, Micron’s 539% one-year surge, and the key risks including export control uncertainty and the sustainability of 80-90% quarter-over-quarter memory price increases.

The hyperscaler free cash flow trajectory is the metric Societe Generale’s Manish Kabra has identified as the most telling signal to watch alongside guidance, with the bank projecting FCF will turn negative by late 2026 before recovering in Q1 2027, a timeline that frames this week’s capex disclosures as an early checkpoint on whether that inflection holds.

The Magnificent Seven valuation premiums now rest almost entirely on forward earnings expectations rather than trailing results, with Alphabet trading at 17x forward earnings at the cheap end and Tesla at 145x at the expensive end; that spread means a single disappointing guidance update from any one name can reprice the entire group.

The Federal Reserve FOMC meeting calendar for 2026 confirms the 28-29 April policy session as a scheduled event, meaning rate decision commentary and any updated economic projections will land simultaneously with the bulk of Big Tech earnings disclosures, compressing the information load investors must process within a single 48-hour window.

Alphabet, Microsoft, Amazon, and Meta all report Q1 2026 earnings on 29 April 2026, with Apple following on 30 April 2026, creating an unusually compressed two-day disclosure window.

The four companies are collectively projected to spend between $649 billion and $700 billion on capital expenditure in 2026, with the vast majority directed at AI infrastructure.

Investors should focus on three disclosures: any revisions to capex guidance, whether cloud platforms like Azure, Google Cloud, and AWS show AI-linked revenue acceleration, and any new metrics quantifying what AI infrastructure is actually generating.

Chinese regulators blocked Meta's proposed $2 billion acquisition of Manus AI, a Chinese-founded AI startup, on national security grounds, marking one of the most prominent cross-border AI deal failures to date.

Micron gained 4.86% on 27 April 2026 because AI data centre buildouts and growing storage demand are already translating into near-term revenue for chip suppliers, even as the revenue payoff from AI spending remains uncertain for platform companies.