Record Highs Are Not the Risk Most Investors Think They Are

5 hrs ago

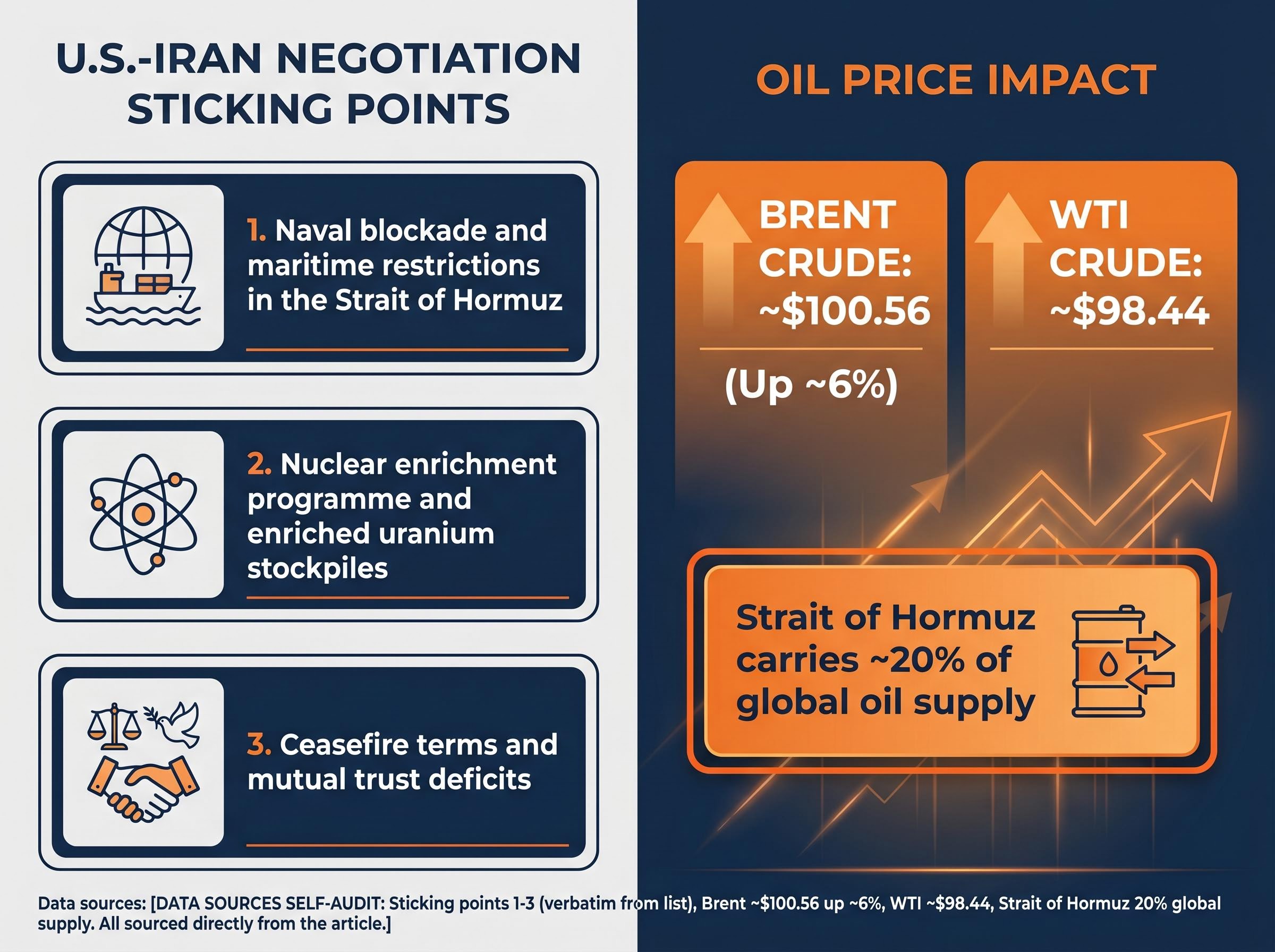

“`json { “fact_checked_full_article”: “Crude oil brushed $100 a barrel on Monday as U.S.-Iran peace talks collapsed over the weekend, pulling all three major U.S. indices lower and raising an uncomfortable question for investors: is last week’s rally already running on borrowed time? The session on 27 April 2026 turned cautious after planned diplomatic negotiations between the U.S. and Iran failed to take place, leaving the Strait of Hormuz under restricted passage and crude prices surging. The move arrived just 24 hours before the Federal Reserve opens its April meeting and days before Apple, Meta, Microsoft, and Amazon all report earnings.\n\nWhat follows is a breakdown of exactly what drove Monday’s pullback in the stock market today, why an oil price shock at the Strait of Hormuz matters well beyond the gas pump, which individual stocks moved sharply, and what the next 48 hours could mean for portfolio positioning.\n\n## Markets pull back as geopolitical shock resets the mood\n\nMonday’s losses were modest by any measure. But they arrived at the worst possible moment for bulls who had spent the prior week building momentum.\n\n- S&P 500: 7,165.08 (+0.80%)\n- Dow Jones Industrial Average: 49,230.71 (-0.16%)\n- Nasdaq Composite: 24,799.64\n- Russell 2000: 2,787.00 (+0.43%)\n\n> The Dow’s -0.16% decline, the sharpest among the major indices, reflected blue-chip caution as energy-cost-sensitive industrials and consumer names bore the brunt of oil-driven selling.\n\nThe pullback was sentiment-driven, not fundamentals-driven. No earnings miss, no economic data release, and no credit event triggered the selling. Instead, the weekend’s diplomatic failure injected enough uncertainty to stall what had been a broad-based advance.\n\nThe Russell 2000’s modest gain stood out. Smaller, domestically oriented companies proved more resilient than their large-cap counterparts, though that resilience owed more to lower direct energy exposure than to genuine risk appetite.\n\n## How a diplomatic failure over the weekend moved markets on Monday\n\nThe chain of events was fast. U.S.-Iran negotiations did not take place over the weekend, and by Monday morning the market had priced in the absence of progress.\n\nThree sticking points brought talks to a halt:\n\n1. Iran’s demand that the U.S. lift its naval blockade and maritime restrictions in the Strait of Hormuz\n2. Disagreements over Iran’s nuclear enrichment programme and enriched uranium stockpiles\n3. Ceasefire terms and mutual trust deficits that neither side could bridge\n\nIranian President Masoud Pezeshkian framed the blockade as the principal obstacle to diplomacy in a 27 April call with Pakistan’s prime minister, reported by Iran’s Mehr News Agency. A day earlier, on 26 April, U.S. envoys Steve Witkoff and Jared Kushner cancelled a planned trip to Pakistan, signalling Washington’s own frustration with the stalemate.\n\nThe multilateral dimension sharpened on Monday. Iran’s Foreign Minister Abbas Araghchi met with Russian President Vladimir Putin on 27 April, seeking diplomatic cover on both the nuclear file and the Strait of Hormuz situation. That meeting complicated an already difficult U.S. negotiating position. Meanwhile, Israeli Prime Minister Benjamin Netanyahu convened consultations the same day, preparing for a full collapse scenario while urging Washington to maintain its naval blockade.\n\n### What the Polymarket signal shows\n\nPrediction platform Polymarket showed an approximately 80-81% probability for U.S.-Iran conflict resolution by 30 April, a figure that had been declining since the weekend’s collapse. A further slide below 75% would likely weigh on equity risk appetite in the near term, particularly in energy-sensitive sectors already absorbing the oil price shock.\n\n## Why an oil price shock at the Strait of Hormuz reaches well beyond the gas pump\n\nThe numbers told the immediate story. WTI crude closed near $98.44, up sharply from recent levels. Brent crude touched approximately $100.56, reported up roughly 6% on the session.\n\n> Brent crude’s approximately 6% surge represented the session’s starkest data point, pushing the global benchmark to its highest level in months and signalling that the market sees no near-term resolution to Strait of Hormuz restrictions.\n\nThe Strait of Hormuz carries approximately 20% of global oil supply. When passage is restricted, the price impact radiates outward from energy into sectors that most investors do not associate with crude oil.\n\n

| Sector affected | Disruption mechanism | Market implication |

|---|---|---|

| Energy | Direct crude supply restriction raises input costs | Energy stocks rally; consumers and industrials face margin pressure |

| Food commodities | Shipping-route dependencies raise freight and fertiliser costs | Agricultural input inflation feeds into consumer staples pricing |

| Pharmaceuticals | Supply chain disruption for petrochemical-derived inputs | Production delays and cost increases for drug manufacturers |

\n

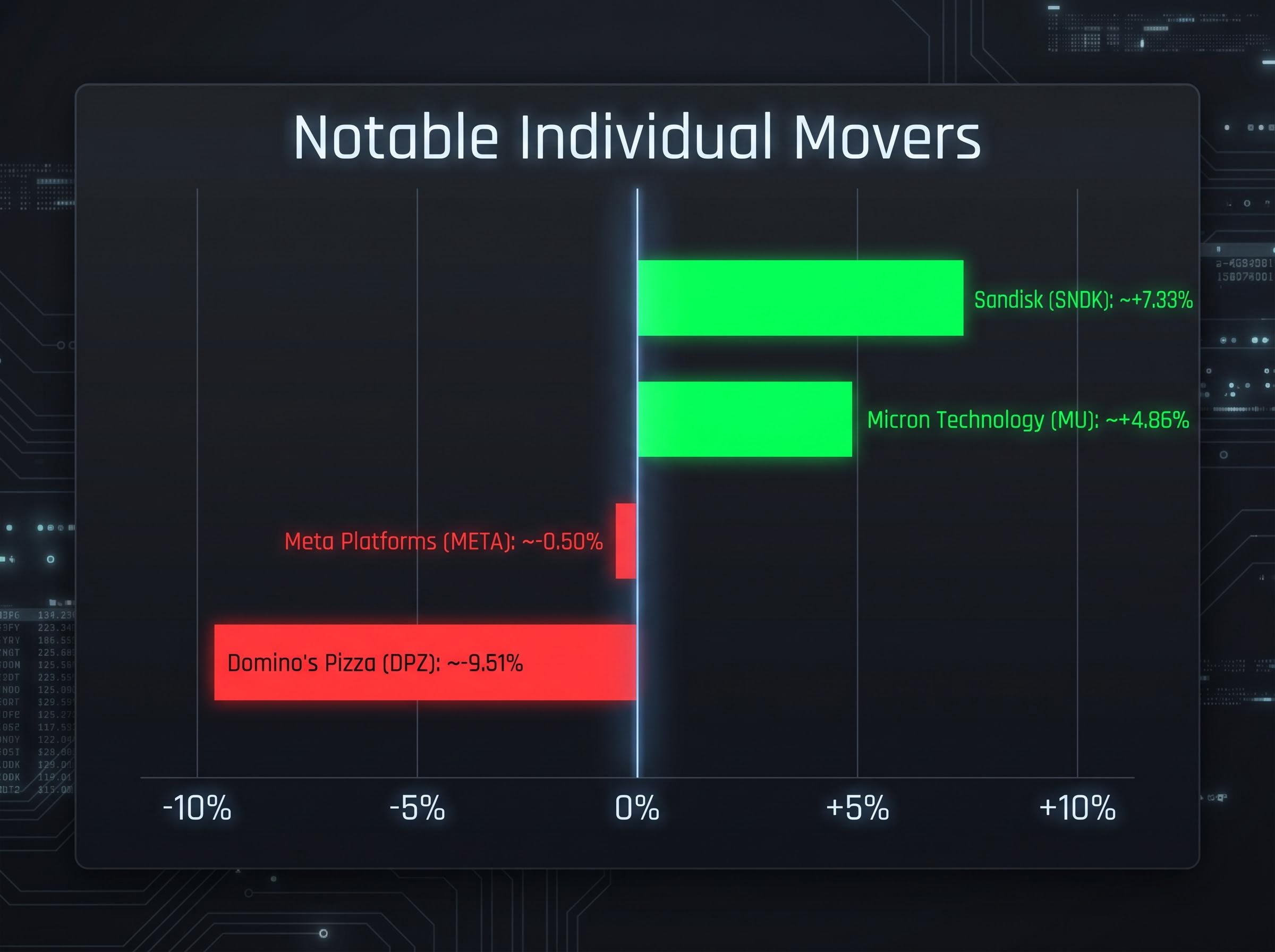

\n\nEnergy stocks rose on Monday while the broader market fell, a divergence that illustrates how the same oil shock creates winners and losers simultaneously. For investors holding diversified portfolios, the risk is not confined to the energy weighting. It sits in the inflationary pass-through to food, healthcare, and consumer goods, the very sectors the Federal Reserve will be watching when it meets this week.\n\n## Individual movers: memory chips surge, Big Tech dips, and Domino’s craters\n\nEven in a flat session, dispersion was high. The gap between the day’s biggest winner and biggest loser spanned nearly 17 percentage points.\n\n- Micron Technology (MU): approximately +4.86%, extending a multi-session rally driven by AI-related memory demand\n- Sandisk (SNDK): approximately +7.33%, lifted by the same structural tailwind in NAND and high-bandwidth memory\n- Meta Platforms (META): approximately -0.50%, pressured by reports that China was set to block Meta’s proposed acquisition of AI startup Manus, adding a company-specific headwind to the broader macro drag\n- Apple (AAPL), Microsoft (MSFT), Amazon (AMZN): all posted morning declines ahead of their earnings releases later this week\n- Domino’s Pizza (DPZ): approximately -9.51% following below-expectations earnings\n\nThe memory sector’s strength was not a one-day event. Micron and Sandisk have tracked higher across multiple sessions as AI infrastructure spending drives demand for high-bandwidth memory chips, a theme that will be tested when Microsoft and Amazon report cloud and AI capital expenditure figures later this week.\n\n### Earnings-day casualty: Domino’s\n\nDomino’s dropped approximately -9.51% after reporting earnings that fell below consensus expectations. The decline served as a reminder that company-specific fundamentals can amplify broader market weakness. For investors holding consumer discretionary names into a potential inflationary environment, where rising oil prices feed through to delivery costs and consumer spending power, the result carried a cautionary signal.\n\n## What comes next: the Fed meeting and Big Tech earnings will set the tone this week\n\nMonday’s geopolitical shock set the stage. The next 48-72 hours will determine whether the pressure compounds or dissipates.\n\n> The CME FedWatch tool showed a 94.8-99% probability that the Federal Reserve will hold rates steady at its 28-29 April meeting, making Wednesday’s statement language, not the rate decision itself, the variable that matters.\n\nThe rate hold is effectively certain. What is not certain is how the Fed characterises the inflation outlook with Brent crude at $100. Any language suggesting the oil shock could delay rate cuts would add hawkish pressure to an already cautious market. Dovish framing, by contrast, could absorb some of the geopolitical drag.\n\nThe earnings slate carries equal weight. AI and cloud revenue acceleration is the primary metric the market is watching across all four names.\n\n

| Company | EPS estimate | Revenue estimate | Key theme |

|---|---|---|---|

| Apple (AAPL) | $1.91 | — | Services growth, iPhone cycle |

| Meta (META) | $6.67 | ~$55.36B | AI advertising, Reels monetisation |

| Microsoft (MSFT) | $4.07 | ~$81.42B | Azure/cloud, AI Copilot adoption |

| Amazon (AMZN) | — | ~$188B (~14% growth) | AWS, advertising, logistics |

\n

\n\nThe risk picture synthesises clearly. A geopolitical oil shock plus hawkish Fed language plus any earnings disappointment would compound pressure across indices. Strong earnings plus dovish Fed commentary could neutralise Monday’s drag entirely. The week is binary in both directions.\n\nMonday’s modest declines were the direct output of a collapsed diplomatic process and an oil price shock, not a fundamental reassessment of U.S. equity values. The losses reversed the prior week’s momentum, but the scale remained contained.\n\nThe next 48-72 hours carry significant risk in both directions. The Fed’s tone on inflation and Big Tech’s AI revenue delivery will together determine whether this week ends higher or lower. Three indicators deserve close attention: Brent crude’s trajectory, Wednesday’s Fed statement, and the first major earnings release of the week.\n\n> This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding Fed policy, earnings expectations, and geopolitical outcomes are speculative and subject to change based on market developments.” } “`

Brent crude’s trajectory from here is best framed not as a point forecast but as a binary distribution: the $70-$82 resolution scenario versus the $114-plus escalation corridor represents the two tails of a price range in which a genuine diplomatic settlement could unwind the geopolitical premium rapidly, while any physical closure or military escalation risks returning to and potentially exceeding the crisis peak recorded on 27 March 2026.

For investors wanting a detailed breakdown of how the supply shock transmits into U.S. household budgets, equity valuations, and the Fed’s rate-path calculus simultaneously, our full explainer on the Hormuz standoff’s implications for U.S. investors examines the near-total shutdown in Strait transits, Goldman Sachs’s analysis of why any announced reopening may be structurally insufficient, and the convergence with this week’s FOMC decision and Big Tech earnings.

The conflict is not a conventional one-sided embargo: the dual-blockade structure currently in force places both Iran and the United States as active enforcers, with Iran restricting vessels linked to the U.S., Israel, and their allies while the U.S. Navy has maintained its own blockade on Iranian port traffic since 13 April 2026. That mutual enforcement dynamic is what makes each side’s preconditions for reopening talks structurally incompatible with the other’s minimum requirements.

The pullback was triggered by the collapse of U.S.-Iran diplomatic negotiations over the weekend, which restricted Strait of Hormuz passage and sent Brent crude surging approximately 6% to around $100 per barrel, dampening investor sentiment.

The Strait of Hormuz carries approximately 20% of global oil supply, so any restriction in passage raises energy costs across multiple sectors including food commodities, pharmaceuticals, and consumer goods, creating broad inflationary pressure that the Federal Reserve and equity markets must absorb.

The CME FedWatch tool showed a 94.8-99% probability that the Fed will hold rates steady at its 28-29 April meeting; the critical variable for markets is the language in Wednesday's statement regarding the inflation outlook with Brent crude near $100.

Sandisk surged approximately 7.33% and Micron gained around 4.86% on AI-driven memory demand, while Domino's Pizza dropped approximately 9.51% after missing earnings expectations and Meta fell around 0.50% on reports that China planned to block its acquisition of AI startup Manus.

Investors should watch AI and cloud revenue figures from Apple, Meta, Microsoft, and Amazon as the primary market-moving metrics, while monitoring Brent crude's trajectory and Wednesday's Fed statement language for signals on whether the geopolitical drag will compound or dissipate.