How Dual-Class Shares Put $24 Billion in Gulf Capital at Arm’s Length

23 hrs ago

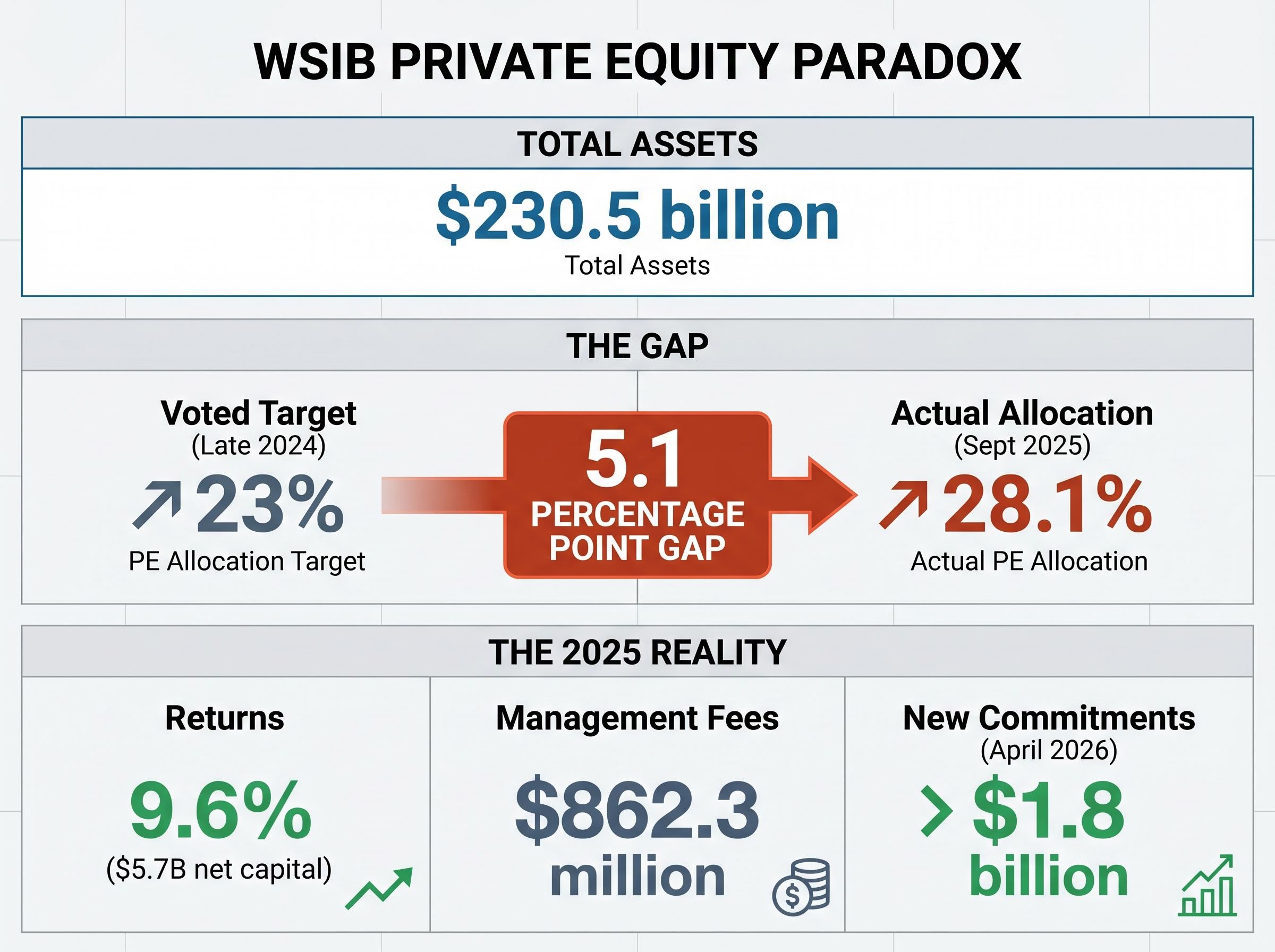

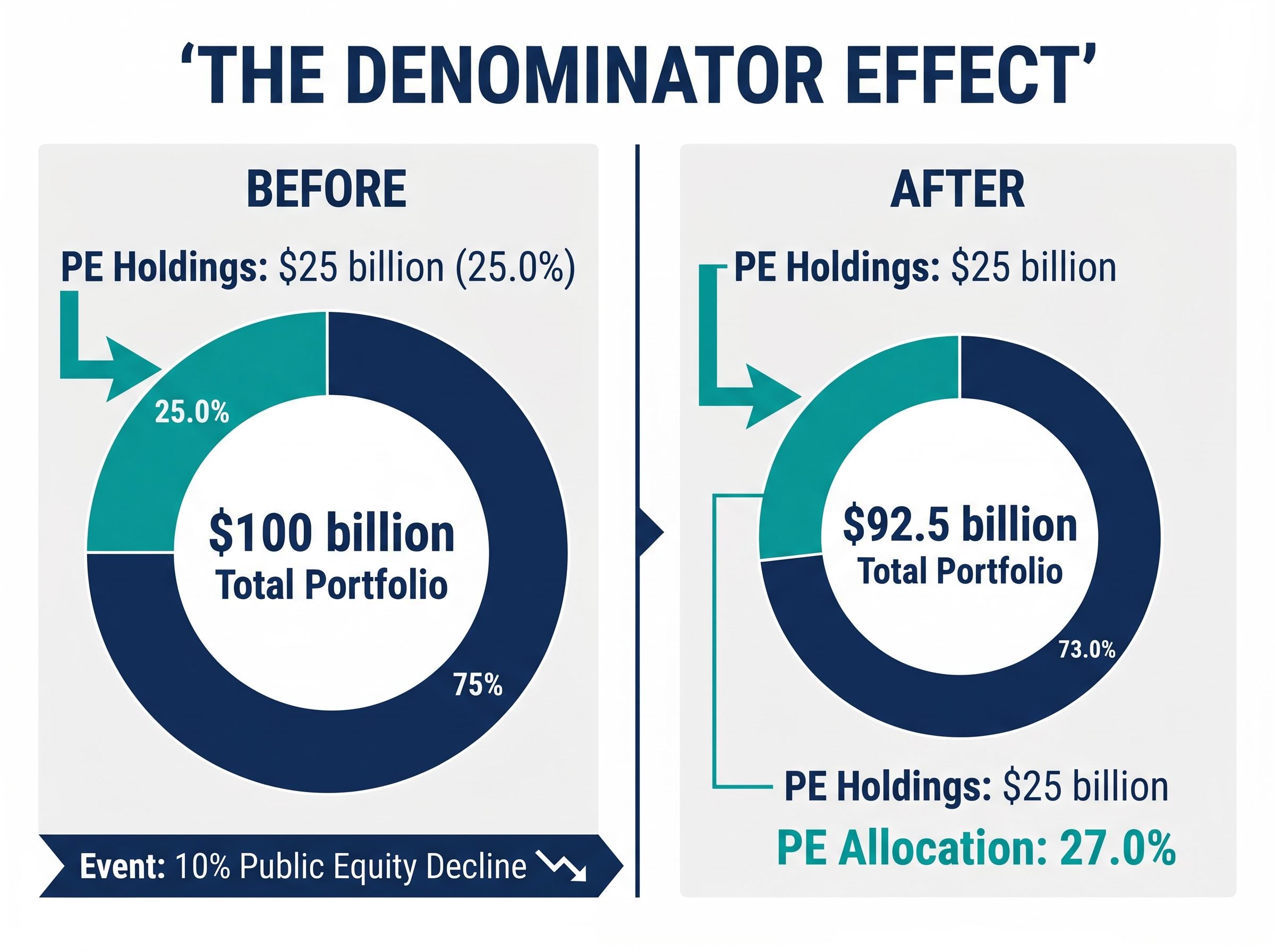

“`json { “fact_checked_full_article”: “Washington State’s pension fund approved more than $1.8 billion in new private market commitments in April 2026, even as its private equity allocation sat 5 percentage points above target and State Treasurer Mike Pellicciotti cast the lone dissenting vote against every recommendation on the table. The Washington State Investment Board (WSIB) holds $230.5 billion in total assets, with roughly 28% locked in private equity, approximately double the national average for US public pensions. The board voted in late 2024 to bring that figure down. The new commitments keep flowing anyway.\n\nThis is not a contradiction unique to Washington. Yale, Harvard, and pension systems in Oregon, Ohio, and Maine have all moved to reduce private equity exposure across 2025 and into 2026, yet the structural mechanics of the asset class make a clean exit nearly impossible on any short timeline. Understanding why requires understanding how pension funds get into private equity in the first place, what locks them in, and what the warning signs look like when the strategy starts to strain.\n\nWhat follows is a structural explanation of that paradox, using WSIB as a live case study alongside the broader institutional picture through early 2026.\n\n## Why pension funds went all-in on private equity\n\nThe logic behind pension fund private equity allocations was, for a long time, straightforward. Pension funds face known future obligations: retiree payouts stretching decades into the future. Meeting those obligations requires projected returns high enough to avoid forcing larger contributions from employers or workers. Private equity, with its historical return premium, offered an answer.\n\n> The theoretical compensation for accepting PE’s lock-up constraints is a 3-5% illiquidity premium over public equities. This figure is the foundational argument pension managers have used to justify the allocation for over two decades.\n\nFour structural reasons drove the allocation trend:\n\n- Illiquidity premium: PE historically offered 3-5% excess returns over public equities, compensating investors for the inability to redeem capital on demand\n- Liability matching: Higher projected returns helped funds close the gap between assets and long-term obligations without requiring larger employer or employee contributions\n- Yield enhancement: In the low-interest-rate environment of the 2010s, fixed income fell short of actuarial return assumptions, making PE’s yield profile particularly compelling\n- Diversification: PE returns have historically shown lower correlation to public market volatility on a reported basis, though valuation lag is a known distortion in that relationship\n\nThe tradeoff, a standard 2% management fee plus 20% carried interest structure, was broadly accepted through the 2010s because net returns appeared to justify it. US public pensions now hold approximately 10-12% average PE allocation, representing over $500 billion in aggregate. WSIB went further. Its PE portfolio generated a 9.6% annual return in 2025, producing $5.7 billion in net capital, and the fund’s PE allocation reached 28.1% as of late 2025.\n\nThe case made sense on paper. The problem is what happens when a fund decides the case no longer justifies the concentration.\n\n## The lock-in mechanics: why you cannot just stop\n\nA pension fund that votes to reduce its private equity target might reasonably expect the allocation to begin declining. In practice, the mechanics of PE work against that expectation at every stage.\n\nThe process follows a three-stage sequence:\n\n1. Commitment made: The pension fund commits capital to a PE fund. This is not a deployment; it is a promise to deliver cash when the GP calls it.\n2. Capital calls drawn over the investment period: Over the next 3-5 years, the GP draws down the committed capital through capital calls as it identifies and executes deals. A commitment made today will be pulling cash from the pension fund for years.\n3. Distributions returned only at exit: Capital comes back to the pension fund only when the GP exits investments, typically through sales, IPOs, or secondary transactions. Fund horizons run 10+ years.\n\nThis cycle creates a structural requirement that confounds any simple plan to reduce exposure. As older PE funds wind down and return capital, pension funds must make fresh commitments or the allocation shrinks faster than intended, disrupting the return profile that the portfolio was built to deliver. WSIB noted explicitly that new commitments are required to replace capital distributions from older funds winding down.\n\nStopping new commitments entirely does not freeze the allocation in place. It sets off an uncontrolled decline as older funds mature, while existing commitments continue drawing capital calls for years. The result is a fund that is simultaneously losing exposure to its highest-returning vintage years and still sending cash out the door on commitments made half a decade ago.\n\n### What the secondary market offers (and what it costs)\n\nThe primary alternative to waiting out the full fund lifecycle is the secondary market, where limited partners (LPs) can sell their PE fund stakes to other investors before the fund winds down.\n\nSecondary market activity grew approximately 20% in 2025, reflecting demand from over-allocated LPs seeking liquidity management tools. That growth, however, reflects the scale of the problem rather than the ease of the solution. Secondary sales typically occur at discounts to net asset value (NAV), meaning every dollar of liquidity comes at a direct cost to the selling fund.\n\nSecondaries are a managed retreat, not a clean exit. They provide a release valve for the most acute concentration problems, but they do not eliminate the fee obligations, the capital call commitments, or the years-long timeline that define PE’s structural grip.\n\n## The denominator effect: when maths makes the problem worse\n\nConsider a pension fund whose private equity allocation reads 25% of total assets on a Monday. By Friday, public equity markets have dropped 10%. The fund made no new PE investments. No capital calls were drawn. No distributions arrived. Yet when the portfolio is recalculated, the PE allocation now reads 27% or higher.\n\nThis is the denominator effect, and it is one of the most underappreciated mechanics in institutional portfolio management.\n\nThe arithmetic is simple: PE holdings are valued on a lag, marked to model rather than market, so they remain nominally stable when public markets fall. The total portfolio value (the denominator) shrinks. The PE allocation (the numerator divided by the denominator) rises mechanically. A fund can breach its policy target without making a single new commitment.\n\n

| Scenario | Total portfolio | PE holdings (lagged valuation) | PE allocation |

|---|---|---|---|

| Before public market decline | $100 billion | $25 billion | 25.0% |

| After 10% public equity decline | $92.5 billion | $25 billion | 27.0% |

\n

\n\nThe 2022 market downturn turned this theoretical risk into a defining constraint. Public market declines caused widespread LP over-allocations, materially reducing new PE commitments across the industry through 2022 and 2023. By 2025, public markets had stabilised and global PE exit activity rebounded to $905 billion, partially restoring LP capacity.\n\n> Despite that recovery, 53% of LPs remained limited in new PE commitments in 2025, citing a combination of denominator effects, capital call obligations, and distribution timing.\n\nFor high-concentration funds like WSIB, the effect’s persistence is visible in the numbers. The fund’s PE allocation declined only slightly, from approximately 29% in December 2024 to 28.1% as of 30 September 2025, despite no aggressive new allocations. The denominator effect turns a strategic intention into a multiyear project rather than a policy switch.\n\n## WSIB as a live case study: voting to reduce while still investing\n\nThe timeline tells the story. In November 2024, WSIB’s board voted to reduce the PE target from 25% to 23%. As of September 2025, the actual allocation stood at 28.1%, a 5.1 percentage point gap above the new target. In April 2026, the board approved over $1.8 billion in new private market commitments.\n\nThe specific commitments approved on 16 April 2026 included:\n\n- Up to 150 million euros for Charterhouse Capital Partners\n- Up to $100 million for Spark Capital and Spark Capital Growth\n- Up to $300 million for Monarch Capital Partners (private credit)\n\nState Treasurer Mike Pellicciotti was the sole dissenting vote on all investment recommendations at that meeting. His prior public warnings about the fund’s vulnerability to PE concentration made the dissent a formal marker of governance tension rather than a procedural disagreement.\n\nWSIB’s total assets stand at $230.5 billion, with PE representing approximately $52 billion. Roughly 55% of the total fund is committed to private markets when private equity, private credit, and real estate are combined.\n\n### The fee dimension: $862 million in a single year\n\nThe cost of maintaining this concentration is visible. WSIB paid approximately $862.3 million in PE management fees in 2025. Oregon’s pension system offers a parallel: alternative investment fees reportedly exceeded $600 million annually, drawing state legislative scrutiny.\n\nFees create a structural drag that compounds the challenge of unwinding high-PE allocations. The cost of staying in is quantifiable and public. The cost of exiting, through secondary discounts, forgone returns on maturing vintages, and opportunity cost, is less visible but equally real. A pension fund considering its options faces a calculation where both paths carry material costs, and the path of least resistance is to keep committing.\n\n## The industry is moving, but slowly: who is reducing and why\n\nWSIB is not acting in isolation. Across 2024 to 2026, a pattern of institutional retrenchment has emerged:\n\n1. Yale University sold up to $6 billion in PE stakes in 2025, one of the largest single LP divestments on record\n2. Harvard University sold $1 billion in PE stakes in 2025\n3. Maine PERS planned PE target cuts in 2026\n4. Oregon PERS reduced PE investments in 2025, amid broader scrutiny of its alternative investment costs\n5. Ohio pensions cut PE exposure across 2025 and into 2026\n\nThe drivers differ by institution type. For endowments like Yale and Harvard, the primary motivators have been liquidity needs and governance recalibration. For public pensions, the calculus involves fee scrutiny, political pressure from state legislatures, and return compression relative to the 2015-2021 period.\n\nOne complication sits beneath the headline figures. As some pensions reduce PE allocations, they are simultaneously increasing private credit exposure. Private credit has grown to approximately $3 trillion globally by 2025, and the asset class carries overlapping risks: limited price discovery, covenant-lite structures, and rising default rates that Moody’s estimated at 1.6-4.7% for 2025, with expectations of a decline below 3% by end of 2026.\n\n> Alyssa Giachino of the Private Equity Stakeholder Project has characterised PE and private credit as the same financial actors offering distinct product structures, a framing that questions whether reallocating from one to the other represents genuine diversification.\n\nMeanwhile, 88% of LPs plan to hold approximately 20% of their portfolios via co-investments by 2030, a strategy designed to reduce fee drag by investing alongside GPs without paying the full fund-level fee structure.\n\n## What the warning signs look like from the outside\n\nThe structural dynamics described above are not invisible. They leave signals in publicly available documents, and a financially literate reader can identify them. Four observable warning signs indicate a pension fund’s PE allocation may be straining:\n\n1. Allocation consistently above target: The actual PE percentage exceeds the investment policy target for multiple reporting periods, despite no intentional increases. This is the denominator effect made visible.\n2. Fees growing faster than net returns: Management fees rising as a percentage of PE returns signal a deteriorating cost-benefit ratio, even if absolute returns remain positive.\n3. Distribution timing mismatches: Pension funds that report cash management strain or increased short-term borrowing may be experiencing gaps between capital call obligations and the timing of PE distributions.\n4. GP concentration increasing: More assets flowing to fewer mega-fund managers (firms such as Blackstone, Apollo, KKR, and Carlyle) reduces diversification benefits. This concentration heightened across 2025.\n\nThe valuation lag that enables the denominator effect also means over-allocation can persist undetected in quarterly reports until public markets stabilise and the denominator expands. WSIB’s 28.1% actual allocation versus its 23% target represents a 5.1 percentage point gap that will take years to close organically, even under the most favourable distribution scenario.\n\n### Why governance signals matter as a leading indicator\n\nBoard dissent, particularly from elected or appointed officials with fiduciary standing, is often the first public signal of a structural concern that internal staff have flagged earlier.\n\nPellicciotti’s pattern is instructive. Prior public warnings about PE concentration preceded his formal lone dissenting vote at the April 2026 meeting. For an outside observer, that dissent is an observable, publicly available data point that precedes any allocation data by months. Board minutes, voting records, and treasurer statements are published. They are worth reading.\n\n## Where this leaves the system\n\nPension funds can vote to reduce private equity targets. The mechanics of the asset class, capital call cycles, lock-up periods, denominator effects, and distribution timing, mean that execution takes years, not quarters. WSIB voted in late 2024 to lower its PE target to 23%. By April 2026, the actual allocation remained at 28.1% and more than $1.8 billion in new commitments were approved.\n\nThe tension is genuine, and it does not resolve neatly. The $5.7 billion in net capital that WSIB’s PE portfolio produced in 2025 is real performance. So are the $862.3 million in management fees and the 5.1 percentage point gap between where the fund is and where it voted to be.\n\nWSIB is not an anomaly. It is a case study in a structural feature of pension fund investing that applies wherever large, long-horizon illiquid allocations have been built up over a decade or more. The funds that built these positions had sound reasons. Unwinding them is a project measured in years, governed by mechanics that do not bend to board resolutions.\n\n> This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.” } “`

The shift from PE toward private credit carries overlapping structural risks that are not always visible in quarterly reports; private credit NAV valuation gaps between fund-reported values and secondary market pricing have reached 25-35% across major vehicles, with redemption gates triggered at nine funds in Q1 2026 alone, suggesting that the diversification case for moving between these two asset classes deserves scrutiny.

Investors wanting to examine the specific governance dimensions in detail, including the Spark Capital portfolio company conflicts and the fee-to-return ratio analysis for beneficiaries, will find our deep-dive into WSIB’s fee drag and governance friction covers the board voting record, Pellicciotti’s documented objections, and the structural limits of unwinding a $52 billion illiquid book.

The illiquidity premium thesis rests on an assumption that is harder to verify than it appears: private equity valuation mechanics rely on GP-controlled internal models rather than independent market prices, meaning reported returns can lag underlying financial reality by quarters or longer and give portfolio valuations an artificial stability that public market holdings never enjoy.

The denominator effect occurs when public market declines reduce a pension fund's total portfolio value while private equity holdings remain stable due to lagged valuations, mechanically pushing the PE allocation percentage higher even without new investments.

Stopping new commitments does not freeze the allocation because existing commitments continue triggering capital calls for years, and as older funds wind down the allocation shrinks unevenly, disrupting the return profile the portfolio was built to deliver.

WSIB paid approximately $862.3 million in private equity management fees in 2025, illustrating the significant and quantifiable cost of maintaining a high-concentration private equity allocation.

Key warning signs include the actual PE allocation consistently exceeding the policy target, fees growing faster than net returns, distribution timing mismatches causing cash flow stress, and increasing concentration among a small number of mega-fund managers.

Yale sold up to $6 billion in PE stakes in 2025 and Harvard sold approximately $1 billion, using the secondary market where limited partners can sell fund stakes before maturity, though typically at a discount to net asset value.