How Dual-Class Shares Put $24 Billion in Gulf Capital at Arm’s Length

11 hrs ago

Four of the most profitable companies in the world are expected to report record or near-record revenues this week, and at least one of them is projected to post a year-over-year decline in earnings per share. That is not a contradiction. It is the clearest expression of a pattern now visible across Microsoft, Alphabet, Meta, and Amazon: AI infrastructure investment on an unprecedented scale is compressing near-term earnings even as it accelerates top-line growth. Together, these four companies represent more than 18% of the S&P 500 and are collectively deploying the largest capital expenditure programmes in corporate history. This article explains the financial mechanics behind the growth-with-compressed-earnings dynamic, what the money is buying, how the company-level data actually looks, and which forward signals matter more than the EPS headline.

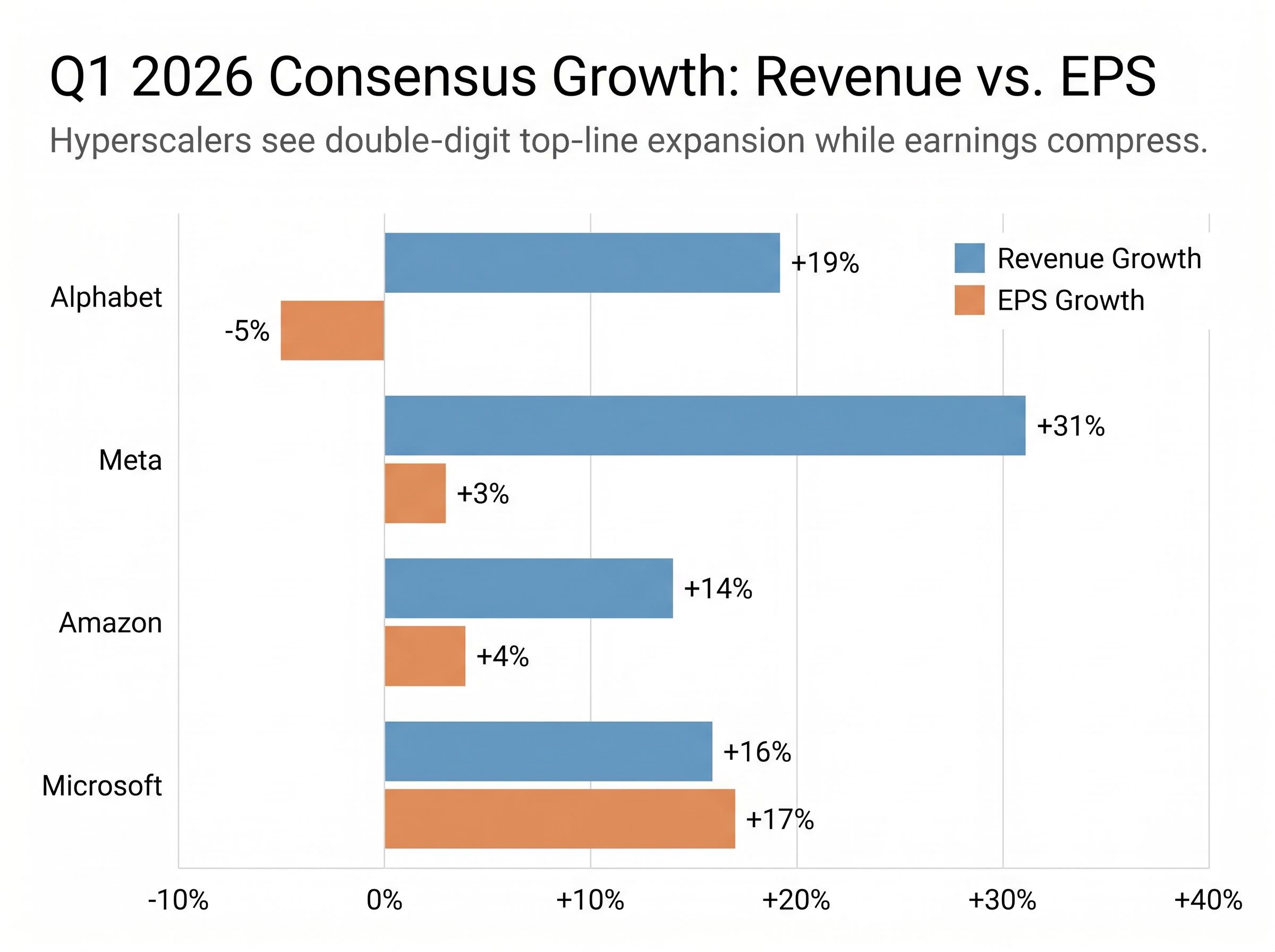

The consensus estimates tell a story that, on the surface, does not make sense. All four companies are expected to grow revenue at double-digit rates in Q1 2026. Three of them are projected to deliver EPS growth of 4% or less.

Alphabet’s projected 5% EPS decline is the sharpest expression, but it is not an outlier. Meta and Amazon sit at the margin of flat earnings growth despite revenue surging. Even Microsoft’s apparently strong 17% EPS growth obscures a structural drag that sits underneath the headline number.

These results arrive after months of elevated volatility, a rotation away from AI-linked equities, and growing investor anxiety about whether the spending will ever generate commensurate returns. The divergence between revenue acceleration and earnings stagnation is not a sign that these businesses are deteriorating. It is a direct, mechanical consequence of how capital expenditure flows through financial statements, and understanding that mechanism is the difference between misreading weakness and recognising investment.

The broad market context heading into earnings week includes Brent crude trading above $100 per barrel on stalled US-Iran diplomacy, pre-Federal Reserve meeting caution, and Big Tech names each down approximately 0.5-1% intraday on 27 April, a backdrop that means any earnings miss carries amplified downside risk relative to what these companies would face in a calmer macro environment.

Three distinct forces are compressing earnings across the hyperscaler group, each operating on a different timeline.

The key to interpreting these results lies in how depreciation mechanics suppress reported earnings during capital buildout cycles: cash leaves the business immediately when a data centre or GPU cluster is purchased, but the income statement absorbs the cost in annual slices spread across the asset’s useful life, creating a widening gap between cash economics and reported profit during any period of accelerating investment.

The result is a timing mismatch that makes healthy, growing businesses look earnings-impaired during the most intense phase of their investment cycle.

Cloud contracts illustrate the lag most concretely. A customer signs a multi-year agreement, then provisions workloads over months, then is billed as usage scales. Revenue is recognised progressively, not at contract signing.

Microsoft’s Remaining Performance Obligations (RPO), which represent the total value of contracted but not yet recognised revenue, reached $392 billion in Q1 FY2026, a 51% increase year over year. That figure reflects committed future revenue that has not yet appeared in earnings. It is a leading indicator of revenue to come, not a current-period earnings contribution, and it underscores why looking at a single quarter’s EPS during a capex supercycle can be misleading.

Meanwhile, Microsoft Cloud gross margin held at 68% despite the infrastructure scaling. The margin is not expanding, but it is not collapsing either, suggesting that capex is containing margin growth rather than destroying it.

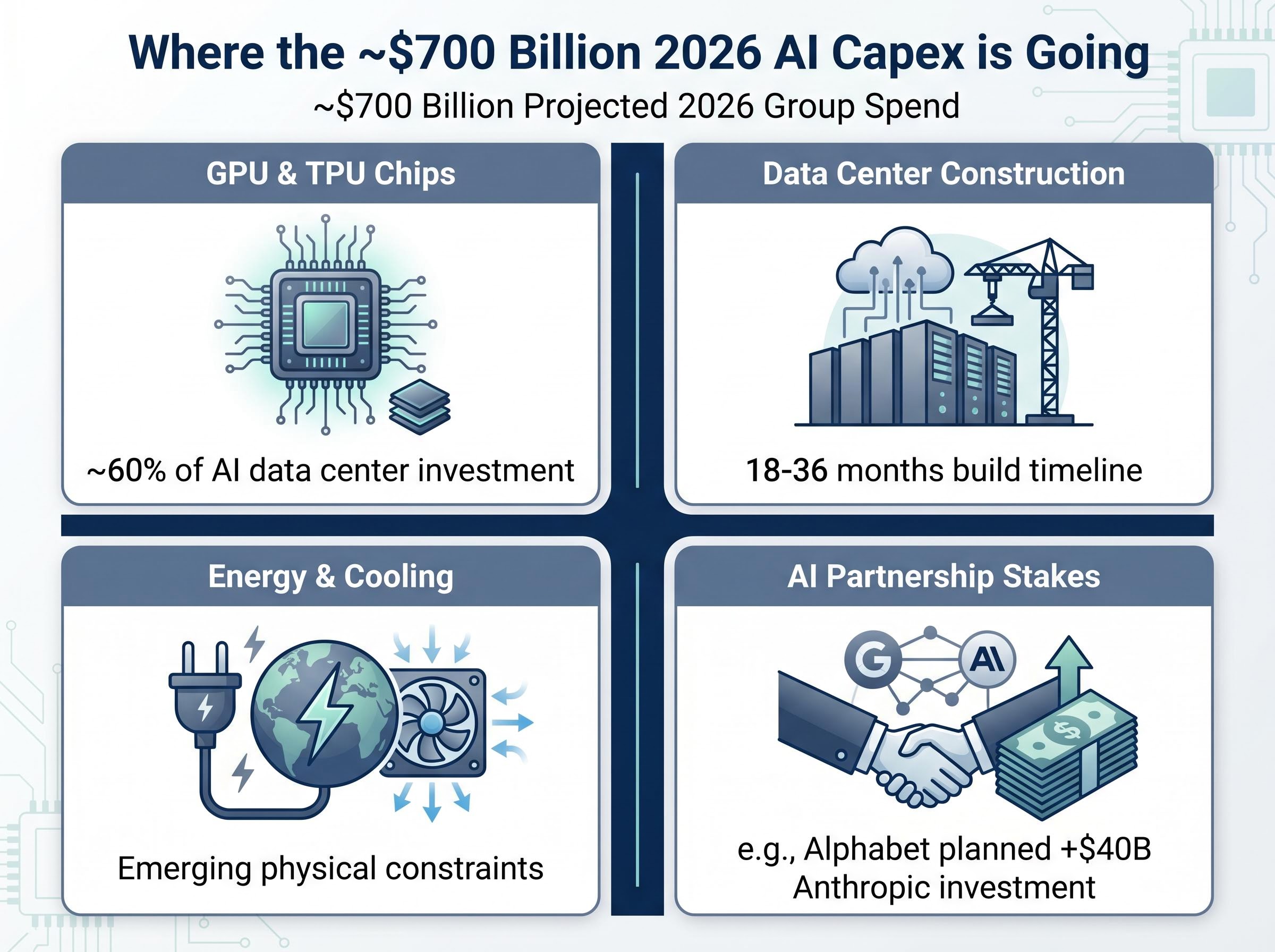

Hyperscalers are collectively projected to spend approximately $700 billion on AI infrastructure in 2026, an escalation from already record levels in 2025.

That figure spans four broad categories, each with a different earnings timing profile:

The spending is not evenly distributed. Meta’s 2026 capex guidance of $115 billion-$135 billion (up from $72.22 billion in full-year 2025) represents the most aggressive single-company escalation. Amazon’s $200 billion total capex plan sits alongside an AI chips business already at a $50 billion annualised revenue run rate, growing more than 100% year over year. Microsoft has cited Azure demand as exceeding supply across workloads as of Q1 FY2026, framing the spending as demand-driven rather than speculative.

The table below captures the core tension. Revenue growth is strong across the board. EPS growth ranges from declining to merely adequate, with capex commitments that explain the compression.

| Company | Q1 2026 Revenue Growth | Q1 2026 EPS Growth | 2026 Capex Commitment | Key Forward Signal |

|---|---|---|---|---|

| Microsoft | +16% | +17% | Demand exceeds supply; scaling aggressively | RPO $392B (+51%) |

| Alphabet | +19% | -5% | +$40B Anthropic investment planned | Cloud margin 30.1% (vs. 17.5% prior year) |

| Amazon | +14% | +4% | $200B total capex plan | CEO: commitments cover nearly full capex |

| Meta | +31% | +3% | $115B-$135B capex guidance | Q4 2025 costs up ~40% YoY |

The pattern is clear: revenue growth of 14-31% across the group is being matched by EPS growth of -5% to +4% in three of four cases. S&P Global analysts cut Alphabet’s Q1 2026 EPS estimates by approximately 4.5% and Amazon’s by approximately 6.7-7%, even as they raised revenue forecasts for both companies. That divergence, raising the top line while cutting the bottom line, is the institutional market’s way of saying it sees the same compression dynamic and is pricing it in.

Microsoft’s +17% EPS growth appears to break the pattern, but the divergence is narrower than it looks. The $3.1 billion OpenAI investment loss in Q1 FY2026 is a direct structural drag that will persist as the partnership continues. Cloud gross margin of 68% is being held rather than expanded, indicating that infrastructure costs are absorbing what would otherwise be margin expansion from Azure’s 40% growth.

Microsoft also revised its OpenAI partnership terms, capping payments received and relinquishing exclusive licensing rights. The shift signals how the economics of AI partnerships are evolving under the weight of the capital commitments required to sustain them. Copilot monetisation, structured as a standalone product, is reported to be meeting internal sales targets, providing an early revenue offset, but the net EPS picture remains one of contained growth rather than earnings acceleration.

During capital-intensive investment cycles, current-period EPS is a lagging indicator. The forward-looking demand signals and margin trajectory tell a more complete story. The following metrics are the ones institutional analysts are tracking:

Jefferies has specifically flagged ROI doubts on current AI spending levels, a named institutional caution that warrants attention alongside the demand signals.

The Federal Reserve’s inability to cut rates in 2026, with PCE inflation holding at 2.8% and approximately two-thirds of investors now expecting rates to remain unchanged through year-end, creates a higher discount rate environment that mechanically compresses the present value of the multi-year earnings recovery that hyperscaler AI investment is designed to produce.

Some AI Cloud revenue growth may partially reflect a self-reinforcing loop: hyperscalers invest in AI startups, and those startups then purchase cloud services from the same hyperscalers. This does not invalidate the revenue, which is real and contractual, but it does affect how investors should weight it when assessing whether demand growth is organic or partially subsidised by the companies’ own investment activity.

The bear case has a name. Analysts at Jefferies have warned of a “capex trap” scenario, where annual per-company spending exceeding $100 billion fails to generate EPS growth within a reasonable horizon, leading to sustained earnings compression without the promised durable revenue payoff.

Jefferies has cautioned that growing ROI doubts on AI infrastructure spending could eventually cap investment levels, describing a scenario in which the current capex trajectory becomes self-limiting if returns do not materialise within the market’s patience window.

A second constraint is physical rather than financial. Grid capacity and power availability are emerging as limits on data centre expansion. If energy infrastructure cannot keep pace with build-out plans, spending may moderate for reasons independent of ROI.

The U.S. Department of Energy projections for data centre electricity demand estimate that AI facilities could consume as much as 9-12% of total U.S. electricity generation by 2030, a scale of power draw that places physical grid constraints alongside financial ROI concerns as a genuine ceiling on hyperscaler expansion plans.

As of the most recent reporting periods (Microsoft Q2 FY2026 in January 2026; Alphabet and Amazon Q4 2025 in February 2026), no hyperscaler has signalled intent to reduce AI infrastructure investment. Amazon CEO Andy Jassy stated that customer commitments already cover nearly the full $200 billion capex plan, directly countering the capex trap narrative. Meta’s guidance of $115 billion-$135 billion for 2026 represents the most aggressive single-company escalation signal in the group.

Analysts expect 2026 could mark the peak of the capex supercycle. The indicators investors should track over the next two to four quarters include:

The apparent contradiction between record revenues and compressed earnings per share across Microsoft, Alphabet, Meta, and Amazon is not a sign of business deterioration. It is a structural feature of an industry-wide, multi-year capital investment cycle in which depreciation drag, revenue recognition lag, and AI partnership losses are simultaneously suppressing bottom-line results even as top-line growth accelerates.

The framework for reading these earnings is now relatively straightforward: track RPO and cloud margins for evidence that spending is translating into committed demand; watch the capex-to-revenue ratio for signs that investment is scaling efficiently; and hold the capex trap scenario as the genuine risk that warrants monitoring rather than either dismissal or alarm.

Investors who understand the difference between earnings compression caused by investment and earnings compression caused by business deterioration are better equipped to interpret the headline numbers without being misled by them. The EPS figure tells part of the story. In this cycle, it may be the least informative part.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced in this article are consensus estimates subject to market conditions and various risk factors. Past performance does not guarantee future results.

AI infrastructure investment refers to the massive capital spending by companies like Microsoft, Alphabet, Meta, and Amazon on GPUs, data centres, and AI partnerships. It suppresses near-term earnings because costs are capitalised and depreciated over years while the revenue those assets generate is recognised gradually, creating a timing mismatch between cash outflows and profit recognition.

Alphabet's consensus EPS for Q1 2026 is projected at $2.67, down approximately 5% year over year, even as revenue is forecast to grow 19% to $107 billion. The decline is driven by depreciation charges from accelerating data centre and chip investment, as well as equity stake losses from AI partnerships such as its planned additional $40 billion investment in Anthropic.

A capex trap is a scenario in which annual capital spending exceeding $100 billion per company fails to generate EPS growth within a reasonable timeframe, leading to sustained earnings compression without a durable revenue payoff. Analysts at Jefferies have flagged this risk, though Amazon CEO Andy Jassy has stated that customer commitments already cover nearly the full $200 billion capex plan, directly countering the concern.

Investors should prioritise Remaining Performance Obligations (RPO) growth, which reflects contracted but unrecognised future revenue (Microsoft's RPO reached $392 billion, up 51%), cloud gross margin trajectory, and the capex-to-revenue ratio trend. These signals indicate whether AI infrastructure spending is translating into durable demand rather than short-term earnings drag.

The four hyperscalers are collectively projected to spend approximately $700 billion on AI infrastructure in 2026, spanning GPU and TPU chips, data centre construction, energy and cooling infrastructure, and equity stakes in AI model developers. Meta alone has guided for $115 billion to $135 billion in capex for 2026, the most aggressive single-company escalation in the group.