How Hormuz Closure at $104 Oil Is Reshaping Every Asset Class

6 hrs ago

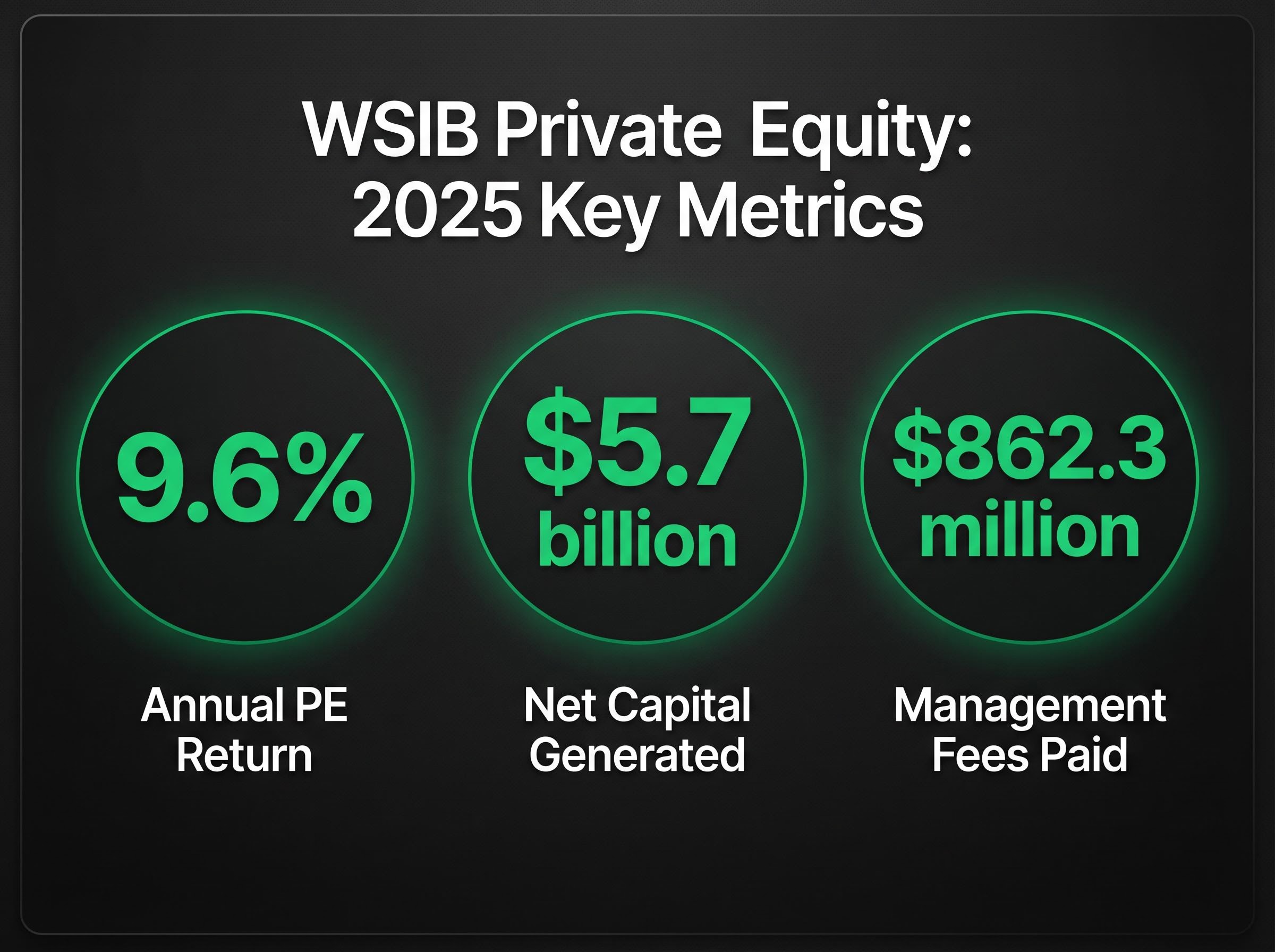

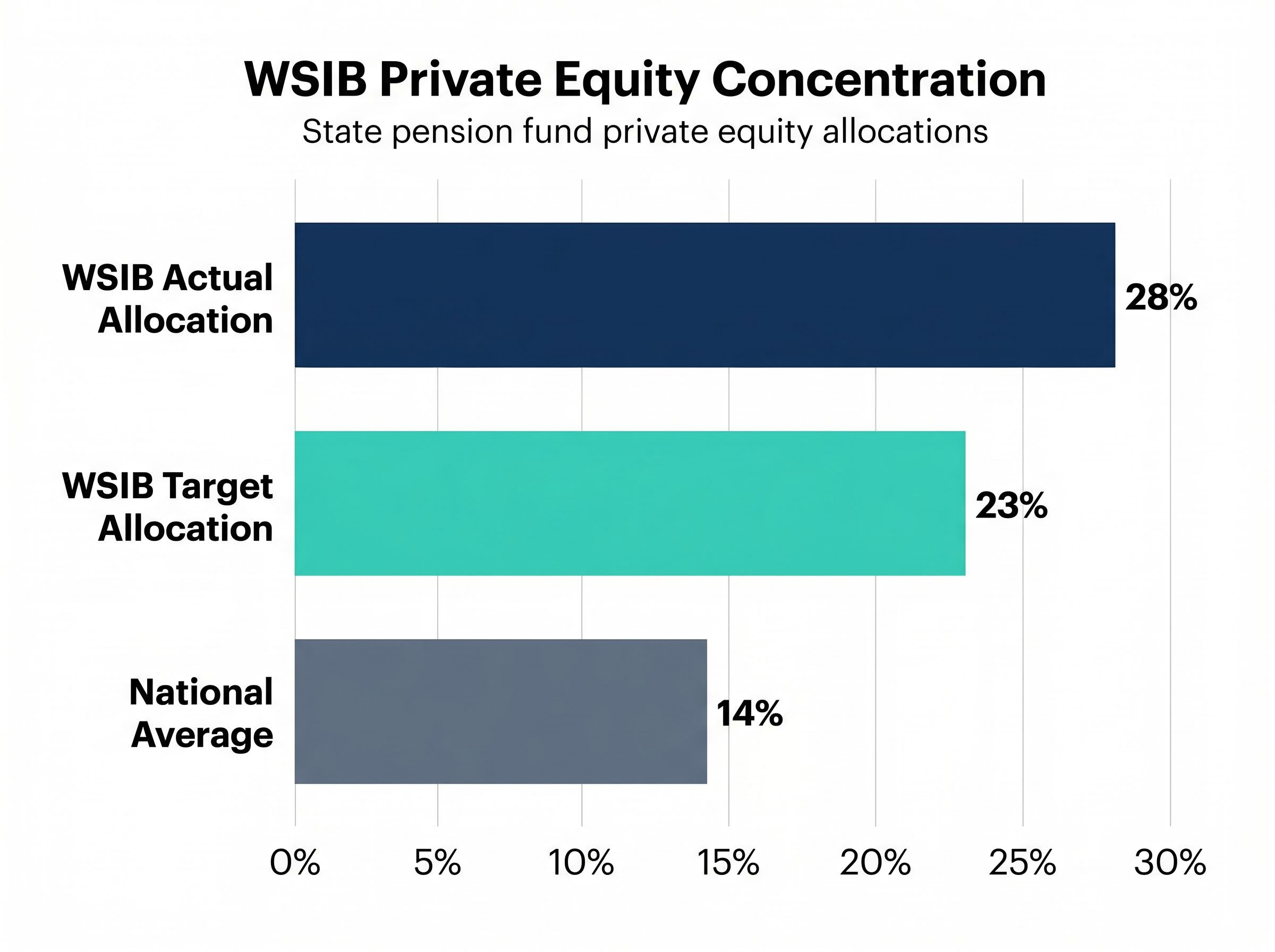

“`json { “fact_checked_full_article”: “Washington State’s pension fund paid $862.3 million in private equity management fees in 2025 while simultaneously voting to reduce its private equity target, and on 16 April 2026, the Washington State Investment Board (WSIB) approved more than $500 million in new private market commitments anyway. State Treasurer Mike Pellicciotti cast the lone dissenting vote. The fund holds roughly 28% of its $174 billion in assets under management in private equity, nearly double the national average for state pension funds. The board voted in November 2025 to lower its PE allocation target from 25% to 23%, yet the pipeline of new commitments continues to flow. The gap between stated direction and actual deployment is not hypocrisy. It is the structural reality of managing a large illiquid book, and the analytical tension at the centre of Washington’s pension strategy.\n\n## Washington’s $187.6 billion pension fund is doubling down on private equity while trying to reduce it\n\nAt the 16 April 2026 board meeting, WSIB approved commitments to three new managers:\n\n- Charterhouse Capital Partners: up to 150 million euros for healthcare and retail buyouts (London-based)\n- Monarch Capital Partners: up to $300 million in private credit targeting energy and technology companies\n- Spark Capital and Spark Capital Growth: up to $100 million combined for venture investments, including artificial intelligence holdings\n\nThe approvals came five months after the board voted to reduce its PE allocation target to 23% from 25%. Private equity’s share of the portfolio has declined from approximately 29% in December 2024 to roughly 28% at the time of reporting, a move in the right direction but one that leaves the fund at approximately double the 14% national average for state pension funds.\n\n> WSIB spokesperson James Aber explained that new commitments are necessary to replace capital being returned from older, winding-down PE funds, a structural requirement of maintaining an orderly drawdown rather than evidence that the reduction target has been abandoned.\n\nThe explanation is mechanically sound. Whether it is sufficient depends on how long that mechanical process takes and what happens to returns along the way.\n\n## Why unwinding a $52 billion private equity book is not a board vote away\n\n### The mechanics of pacing down a large illiquid allocation\n\nClosed-end PE funds operate on drawn-down commitments: capital is called over several years, deployed into companies, and returned through distributions when those companies are sold. A fund that stops making new commitments does not instantly reduce its PE allocation. Three specific dynamics prevent it:\n\n1. Capital call timing: Existing commitments continue drawing capital for years after the board stops approving new ones, meaning PE exposure can rise even after a reduction decision.\n2. Distribution recycling: Distributions from older funds must be partially reinvested to prevent the allocation percentage from overshooting the target in either direction as fund NAV fluctuates.\n3. Denominator effects: If total portfolio value rises (from public equity gains, for example), PE’s share of the portfolio can decline without any PE positions being sold, a passive reduction that is welcome but unreliable.\n\nApproximately 55% of WSIB’s total assets sit in private markets broadly (PE, private credit, real estate), meaning the liquidity constraint is structural across more than half the portfolio.\n\n### Secondary sales as a tool, not a solution\n\nSelling PE positions on the secondary market is possible, and the market has grown significantly. Secondary market volume increased 45% to $162 billion in 2024, and discounts to net asset value have narrowed for high-quality assets, with some flagship strategies trading near par.\n\nScale remains the problem. When Yale explored a $6 billion secondary sale in April 2025, the transaction required months of structuring and negotiation, and Yale’s endowment is among the most sophisticated institutional investors in the world. At WSIB’s scale, an accelerated PE reduction through secondaries would require coordinating sales across dozens of fund relationships, each with its own GP consent requirements and pricing dynamics. Secondaries are a portfolio management tool. They are not a wholesale exit strategy.\n\n## What $862 million in annual fees and 9.6% returns actually tell you\n\nWSIB’s PE portfolio returned 9.6% in 2025, generating approximately $5.7 billion in net capital. The fund paid $862.3 million in management fees for the same period. The fee-to-return ratio is the question that determines whether the programme is earning its cost.\n\n

| Metric | WSIB (2025) | CalPERS (Since Inception, as of Sept 2025) | Key Risk Factor |

|---|---|---|---|

| PE Return | 9.6% annual | 11.3% net IRR | Elevated entry multiples (11.8x EBITDA median) |

| Management Fees | $862.3 million | Not separately disclosed | Fee compression pressure from LP negotiation trends |

| Net Capital Generated | $5.7 billion | 1.5x net multiple | Valuation uncertainty in unrealised holdings |

\n

\n\nMedian PE purchase multiples rose to 11.8x EBITDA in 2025, compressing expected returns for recent vintages. Sluggish exit activity has suppressed distributions across 2019-2022 vintages, meaning a portion of WSIB’s reported return is embedded in unrealised holdings rather than cash returned to the fund.\n\n> Alyssa Giachino of the Private Equity Stakeholder Project has raised concerns that unrealised PE holdings may be marked at inflated values, suggesting that a 9.6% return figure may not fully reflect future realised outcomes.\n\nThe fee figure alone does not indict or vindicate the strategy. Paired with declining return expectations and valuation uncertainty, it frames precisely what the treasurer’s dissenting vote was signalling: a question about whether the risk-adjusted case holds at this concentration.\n\nPast performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.\n\n## The risk profile of Washington’s newest bets: AI companies, energy credit, and a London buyout firm\n\nThe $500 million in new commitments approved on 16 April carries specific, identifiable exposures.\n\n

| Fund/Manager | Commitment Amount | Sector Focus | Key Portfolio Company Controversy |

|---|---|---|---|

| Charterhouse Capital Partners | Up to 150 million euros | Healthcare and retail buyouts (London) | None identified |

| Monarch Capital Partners | Up to $300 million | Private credit (energy, technology) | None identified |

| Spark Capital / Spark Capital Growth | Up to $100 million combined | Venture (AI, technology) | Multiple (see below) |

\n

\n\nSpark Capital’s portfolio includes companies that intersect directly with Washington State’s own regulatory and legal actions:\n\n- Kalshi: Subject of a lawsuit filed by Washington Attorney General Nick Brown in 2026, alleging illegal gambling operations\n- Flock Safety: Prompted Washington state legislation enacted in 2026 regulating licence plate recognition technology\n- Anthropic: Settled a $1.5 billion copyright lawsuit in September 2025\n\nWSIB spokesperson James Aber declined to comment on specific portfolio companies or investment ethics. Neither Spark Capital nor Kalshi responded to media requests.\n\nAt $174 billion, WSIB’s commitment pipeline inevitably includes companies that intersect with the state’s own legal and regulatory apparatus. The governance friction this creates is not a flaw in the process; it is a structural feature of managing a fund this size within a single state’s political economy.\n\n## How Washington’s strategy compares to peers pulling back from private equity\n\n### State pension funds moving away from private equity\n\nWashington is not the only state pension fund reassessing its PE concentration. Maine, Oregon, and Ohio have each reduced PE exposure directionally, and WSIB’s own target reduction to 23% signals recognition of the same pressure.\n\n- Maine: Directional PE reduction reported\n- Oregon: Reduced PE allocation targets\n- Ohio: Scaled back PE commitments\n\n> Washington’s 28% PE allocation stands at approximately double the 14% national average for state pension funds, making it one of the most concentrated PE positions among US public plans.\n\nInstitutional PE allocations reportedly fell approximately 27% quarter-over-quarter to roughly $19.1 billion in Q3 2025, reflecting broader pacing discipline across the sector (though this figure carries source verification caveats).\n\n### Endowments using secondaries as portfolio management tools\n\nThe rebalancing trend is not limited to state pensions. When Yale pursued a $6 billion secondary sale in April 2025, the move represented a deliberate effort to rebalance older vintages rather than any broad withdrawal from private markets. Harvard, with $56.9 billion in assets under management and an 11.9% return in FY 2025, maintains private market allocations as a core strategy while participating actively in secondary market transactions.\n\nThe peer landscape suggests institutions are not abandoning private markets; they are rotating within them. CalPERS committed $500 million to a private credit vehicle in June 2025, and private credit allocations grew approximately 7% quarter-over-quarter to roughly $15.9 billion in Q3 2025. With secondary market volume having risen 45% to $162 billion in 2024, the capacity already exists for WSIB to quicken its pace of reduction should the board decide to deploy that option.\n\n## Understanding why public pension funds stay in private equity even when the case weakens\n\nThe structural logic that keeps large public pensions in PE is not inertia. It is arithmetic. Three forces hold the allocation in place:\n\n1. Liability matching: Public pension funds carry long-dated obligations to retirees that require sustained returns above what public equity and fixed income markets reliably generate over full cycles. PE has historically provided that premium.\n2. Illiquidity as a feature: Because pension liabilities are staggered over decades, the illiquidity embedded in PE is theoretically justified by the fund’s own liability structure. A pension fund, unlike an endowment or sovereign wealth fund, can tolerate multi-year lockups because its outflows are predictable.\n3. Historical return premium: PE has outperformed public markets over long-term horizons across most vintage years, and public pension funds represent nearly one-third of all PE investors globally, according to IPE (May 2024).\n\n> The ILPA Q4 2024 LP Sentiment Survey found that LPs report stability in current PE allocations, with many planning medium-term increases, a finding that complicates the narrative that institutional capital is retreating from the asset class.\n\nThe Bain 2026 Global Private Equity Report frames the central LP challenge as managing the trade-off between liquidity and returns, not exiting PE. LP capital is concentrating among established, top-quartile managers with proven distribution histories, and growing interest in co-investments and separate accounts offers tools to reduce fee drag while maintaining exposure.\n\nPE deal activity in Q1 2026 reached 2,553 deals totalling $568.4 billion, with strategic M&A up 32.4%, indicating that the market continues to function even as individual LPs recalibrate their pacing.\n\nThe fiduciary bind is real. A public pension fund that exits PE too aggressively risks underperforming the return assumptions embedded in its liability structure. A fund that stays too long at elevated concentration risks the fee drag and valuation compression that the treasurer’s vote was intended to flag.\n\nWashington is not making an irrational choice by continuing to commit to PE. The structural logic of liability matching, the mechanical constraints of illiquidity, and the historical return premium all support continued exposure. What the treasurer’s lone dissenting vote signals is a genuine disagreement about whether that logic holds at 28% concentration, with $862.3 million in annual fees, declining return expectations, and specific portfolio company controversies now in public view. Three forces sit in tension: the rationale that keeps the fund in PE, the constraint that makes unwinding slow, and the market environment that makes the current moment a genuine inflection point. Every new $500 million commitment extends the timeline for reaching 23%. Whether WSIB gets there, and on what schedule, is the question that beneficiaries and the board will continue to answer one quarterly meeting at a time.\n\nThis article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.” } “`

The concern raised by Alyssa Giachino reflects a structural feature of private equity accounting: private equity valuation opacity means GPs apply their own internal models to unrealised holdings, and reported returns can lag actual financial conditions by quarters or longer, making a 9.6% headline figure genuinely difficult to interpret without knowing how much sits in marked-up positions that have not yet been tested by a sale.

Pension fund private equity refers to allocations public retirement funds make to private buyout, venture, and credit strategies to earn returns above what public markets reliably generate. Funds like WSIB use PE because long-dated pension liabilities require sustained return premiums, and PE has historically delivered that premium over full market cycles.

WSIB approved over $500 million in new commitments in April 2026 because closed-end PE funds require ongoing capital recycling: distributions from winding-down funds must be partially reinvested to maintain an orderly drawdown rather than an abrupt exit. The board voted in November 2025 to lower its PE target from 25% to 23%, but the structural mechanics of illiquid portfolios mean the reduction happens gradually, not immediately.

WSIB paid $862.3 million in private equity management fees in 2025, during which its PE portfolio returned 9.6%, generating approximately $5.7 billion in net capital. The key investor question is whether that fee level is justified by risk-adjusted returns, particularly given rising entry multiples and valuation uncertainty in unrealised holdings.

Secondary market sales are possible but not a wholesale solution at large scale. Secondary market volume reached $162 billion in 2024, yet when Yale explored a $6 billion secondary sale in April 2025, it required months of structuring; for a fund the size of WSIB, coordinating sales across dozens of GP relationships with individual consent requirements makes rapid exit impractical.

WSIB holds approximately 28% of its $174 billion portfolio in private equity, nearly double the 14% national average for US state pension funds. Peer funds including Maine, Oregon, and Ohio have each taken steps to reduce PE exposure, while CalPERS has simultaneously committed $500 million to private credit, reflecting a broader trend of rotation within private markets rather than outright withdrawal.