Washington Charges 38 Entities in $10M AI Crypto Fraud Sweep

Apr 24, 2026

Neobo Fastigheter posted a 94% occupancy rate in the first quarter of 2026, the highest in company history, while delivering 5% like-for-like rental income growth that positions it ahead of most Swedish residential peers. The results arrived as the broader Swedish property market transitions from multi-year contraction to modest growth, with Neobo’s operational metrics signalling pricing power and tenant demand resilience even as weather-related costs compressed headline profitability.

Rental income reached SEK 233 million for the quarter, driven by rent increases of 3.4% across the residential portfolio and vacancy rates falling from 6.6% to 4.6% year-over-year. Net operating income declined to SEK 103 million from SEK 107 million in the prior year, though this reflects property disposals eliminating their income contribution rather than deteriorating core performance. Profit from property management per share held steady at SEK 0.19, supported by the company’s share buyback programme reducing outstanding shares during a period of operational headwinds.

Investors tracking Swedish residential real estate now face the task of distinguishing between companies posting genuine operational improvement and those benefiting from cyclical recovery alone. Neobo’s results suggest the former, with rental growth exceeding wage inflation and occupancy rates approaching full capacity in well-managed assets.

The 94% occupancy achievement represents Neobo’s strongest tenant retention and demand metrics to date. The company reduced residential vacancy from 6.6% to 4.6% over the twelve months to March 2026, a compression that contributed meaningfully to the 5% comparable rental income growth alongside base rent increases of 3.4%.

Helsingborg illustrates the operational execution driving these numbers. Among 455 apartments in that portfolio, only four units sat vacant at quarter end, with three undergoing renovation. Near-full occupancy in a secondary Swedish city signals that Neobo’s portfolio positioning in growth municipalities is delivering the tenant demand management anticipated when acquiring and developing these assets.

The rental growth mechanics broke down across three components:

The 3.4% residential rent increase reflects Sweden’s Tenancy Act governing reasonable rent levels, which requires landlords to justify adjustments through the Regional Rent Tribunal rather than applying market-rate pricing, constraining the pace at which operators can capture housing shortage premiums through base rent alone.

These operational metrics matter because they demonstrate pricing power in a market where structural undersupply supports landlords. The 5% like-for-like growth rate exceeds Swedish wage inflation forecasts for 2026, indicating Neobo is capturing rent increases that outpace household income growth, a dynamic sustainable only when housing supply constraints persist.

Helsingborg Portfolio Performance Only 4 vacant units among 455 apartments, with 3 undergoing renovation. Effective occupancy approaching 99% in well-managed secondary city assets.

Net operating income fell to SEK 103 million from SEK 107 million in the prior year quarter, a decline explained primarily by two factors unrelated to underlying operational quality. Property disposals executed in prior periods eliminated their NOI contribution from comparable figures, creating a year-over-year headwind that masked the strengthening performance of retained assets.

Weather-related costs surged by SEK 6 to SEK 7 million during the quarter. Sweden experienced unusually severe winter conditions in early 2026, with prolonged cold and heavy snowfall driving heating, snow removal, and maintenance expenses significantly above historical norms. These costs represent a temporary margin compression rather than structural deterioration in the business model.

The SEK 6 to SEK 7 million weather-related cost surge demonstrates how energy price dynamics and inflation pressures translate into property-level operating expenses, particularly during periods of extreme weather conditions that drive heating and maintenance costs above historical norms.

Property management profit reached SEK 26 million, with profit from property management per share holding at SEK 0.19 despite the absolute profit decline. The per-share stability reflects Neobo’s ongoing share buyback programme, which reduced the denominator sufficiently to offset numerator pressure from weather costs and disposal effects.

The stability of profit from property management per share at SEK 0.19 reflects how buyback programmes can offset numerator pressure during periods of operational transition, a dynamic visible across distribution growth metrics in property REITs that prioritise per-share value creation over headline profit expansion.

The two main factors compressing headline profitability, ranked by estimated impact magnitude:

Understanding this distinction matters for accurate valuation. Investors examining only the NOI decline will conclude the business is weakening. Those adjusting for one-off weather costs and disposal effects see a core operation strengthening through rental growth and occupancy gains.

Like-for-like rental growth measures the same properties over time, excluding acquisitions and disposals. This metric isolates operational performance from portfolio composition changes, making it the clearest signal of whether management is extracting value from existing assets or simply growing through capital deployment.

For property company analysis, like-for-like growth matters more than headline rental income because it answers whether the core portfolio is performing. A company can report 10% rental income growth by acquiring properties, while like-for-like growth of 1% reveals the existing portfolio is stagnating. Neobo’s 5% comparable growth demonstrates genuine operational execution.

The company’s 4.7% like-for-like residential rental growth compares favourably to peers and market benchmarks. Fastighets AB Balder, one of Sweden’s largest property companies, reported 2.7% like-for-like rental growth in recent periods. The Swedish rental market averaged 5.5% growth for new rents in 2025, positioning Neobo’s 4.7% residential figure as competitive within a market experiencing strong rental pricing dynamics.

| Metric | Neobo | Balder | Market Average (New Rents) |

|---|---|---|---|

| Like-for-like rental growth | 5.0% | 2.7% | 5.5% |

| Residential portfolio specific | 4.7% | N/A | N/A |

This educational context helps investors benchmark Neobo’s operational execution against peers. Kepler Cheuvreux, a leading equity research house specialising in Nordic real estate, has reaffirmed its buy recommendation on Neobo despite near-term profitability headwinds, signalling analyst confidence that operational metrics justify the investment thesis even when weather costs temporarily compress margins.

Neobo invested SEK 55 million in property improvements during the first quarter, deploying capital across energy efficiency projects, apartment renovations, and sustainability initiatives designed to sustain rental growth and improve margins over time. The yield-on-cost metrics for these investments demonstrate returns that exceed the company’s 3.4% average borrowing cost.

Helsingborg energy efficiency projects are generating approximately 12% yields on invested capital, driven by lower heating costs that flow directly to property-level operating margins. These efficiency investments reduce the building’s energy consumption, cutting operating expenses while maintaining or improving tenant satisfaction, a combination that produces attractive risk-adjusted returns.

Apartment renovations in Helsingborg achieved yields above 5%, with Stockholm renovations producing the most aggressive value creation. Renovated Stockholm apartments commanded approximately 60% rent uplifts relative to pre-renovation levels, reflecting the capital city’s tight housing market and tenant willingness to pay premium rents for upgraded units.

The company completed renovations on 39 apartments during the quarter, a pace suggesting management is actively cycling through the portfolio to capture repositioning opportunities where renovation economics justify the capital deployment.

The three investment categories and their respective yield metrics:

These investment returns matter because they demonstrate Neobo is not harvesting the portfolio but creating value through targeted capital deployment. The 12% yield on energy efficiency projects compares favourably to the company’s borrowing costs, indicating management can leverage the balance sheet to fund improvements that generate returns well above financing costs.

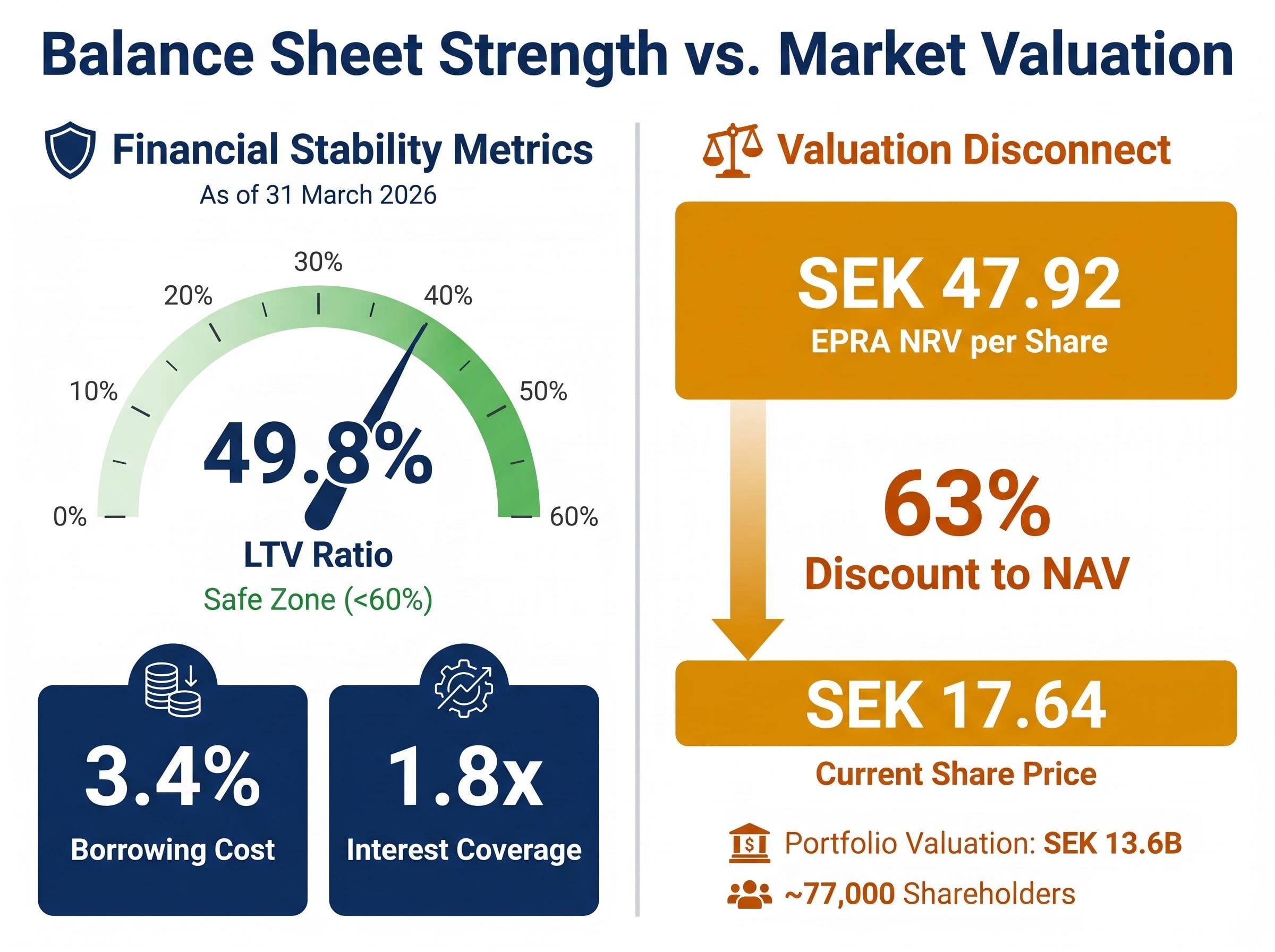

The loan-to-value ratio declined to 49.8% as of 31 March 2026, providing Neobo with acquisition capacity and financial stability as the Swedish property market transitions toward recovery. This LTV level sits comfortably below the 60% threshold that typically triggers covenant concerns or refinancing pressure, giving management flexibility to act on strategic opportunities or weather temporary profitability headwinds without balance sheet stress.

The 49.8% loan-to-value ratio provides Neobo with the balance sheet capacity to pursue strategic opportunities as the Swedish market recovers, positioning the company similarly to acquisition deployment strategies in property portfolios that leverage covenant headroom to consolidate assets during market transitions.

The company’s average borrowing cost of 3.4% remains favourable relative to the portfolio’s net initial yield, creating positive leverage dynamics where property returns exceed financing costs. Interest coverage reached 1.8 times on a trailing twelve-month basis, indicating debt service obligations consume just over half of property-level cash flow before capital expenditure.

The three key balance sheet metrics supporting financial stability:

The Annual General Meeting authorised management to repurchase shares, a decision reflecting the board’s view that Neobo’s stock trades below intrinsic value. The company’s EPRA NRV per share stood at SEK 47.92, while the share price traded at SEK 17.64, creating a discount to stated net asset value of approximately 63%.

Valuation Tension EPRA NRV per share: SEK 47.92 Share price: SEK 17.64 Discount to NAV: Approximately 63%

This significant discount signals either a genuine value opportunity or structural concerns the market has not resolved. Approximately 77,000 shareholders hold Neobo stock, a retail-heavy shareholder base that may contribute to valuation disconnects when institutional investors apply scepticism to property company NAV calculations. The portfolio valuation of SEK 13.6 billion underpins the NAV calculation, with the market’s discount suggesting investors question either the valuation methodology or the company’s ability to realise stated asset values through sales or income generation.

The 63% discount to EPRA NRV creates a valuation tension similar to sector valuations during extended bull runs where market prices diverge sharply from stated asset values, forcing investors to decide whether the disconnect signals opportunity or structural concerns the market has correctly identified.

Investors must weigh operational strength (record occupancy, peer-leading rental growth) against this persistent valuation discount when evaluating whether Neobo represents an opportunity or a value trap.

Neobo Fastigheter’s first quarter results demonstrate operational excellence masked by temporary weather costs and prior-year disposal effects. The company achieved record occupancy of 94% and delivered 5% like-for-like rental income growth that exceeds most Swedish residential peers, positioning management’s execution as best-in-class within a recovering market characterised by structural housing undersupply and improving tenant demand dynamics.

Investors should monitor whether rental growth momentum sustains in coming quarters as the Riksbank navigates inflation risks from elevated energy prices and geopolitical tensions. The proposed April 2026 mortgage regulatory changes, which would increase loan-to-value caps from 85% to 90% and remove extra amortisation requirements, represent a potential catalyst for housing demand and price appreciation that could benefit Neobo’s portfolio valuation.

The Swedish Parliament’s April 2026 mortgage regulatory changes raising LTV caps to 90% and removing extra amortisation requirements passed in March 2026, creating the policy catalyst that could expand household borrowing capacity and accelerate demand for rental alternatives if homeownership remains financially constrained despite looser lending standards.

For global investors tracking Nordic real estate, these results suggest well-managed Swedish residential portfolios can deliver genuine operational outperformance even as the broader market works through the transition from contraction to growth. The significant discount to net asset value creates a risk-return tension that requires careful assessment of whether the market has correctly identified structural concerns or whether Neobo represents a value opportunity trading at a fraction of intrinsic worth.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Like-for-like rental growth measures income from the same properties over time, excluding acquisitions and disposals, so it isolates whether management is genuinely improving the core portfolio rather than simply growing through new purchases. Neobo reported 5% like-for-like growth in Q1 2026, which exceeded the performance of Swedish peer Fastighets AB Balder at 2.7%.

Net operating income fell to SEK 103 million from SEK 107 million due to two temporary factors: prior property disposals removing their income contribution from year-over-year comparisons, and exceptional winter weather costs adding SEK 6 to SEK 7 million in heating, snow removal, and maintenance expenses above historical norms.

As of Q1 2026, Neobo's EPRA NRV per share stood at SEK 47.92 while the share price traded at SEK 17.64, representing a discount to stated net asset value of approximately 63%, which raises the question of whether this signals a value opportunity or structural concerns the market has correctly identified.

The Swedish Parliament passed mortgage rule changes in March 2026 that raise loan-to-value caps from 85% to 90% and remove extra amortisation requirements, expanding household borrowing capacity in a way that could accelerate housing demand and support rental portfolio valuations.

Energy efficiency upgrades in Helsingborg are generating approximately 12% yields on invested capital through reduced heating costs, apartment renovations in Helsingborg are producing yields above 5%, and Stockholm renovations are delivering approximately 60% rent uplifts on refurbished units.