United Slashes 2026 Profit Outlook 40% as Iran War Hits Fuel

4 hrs ago

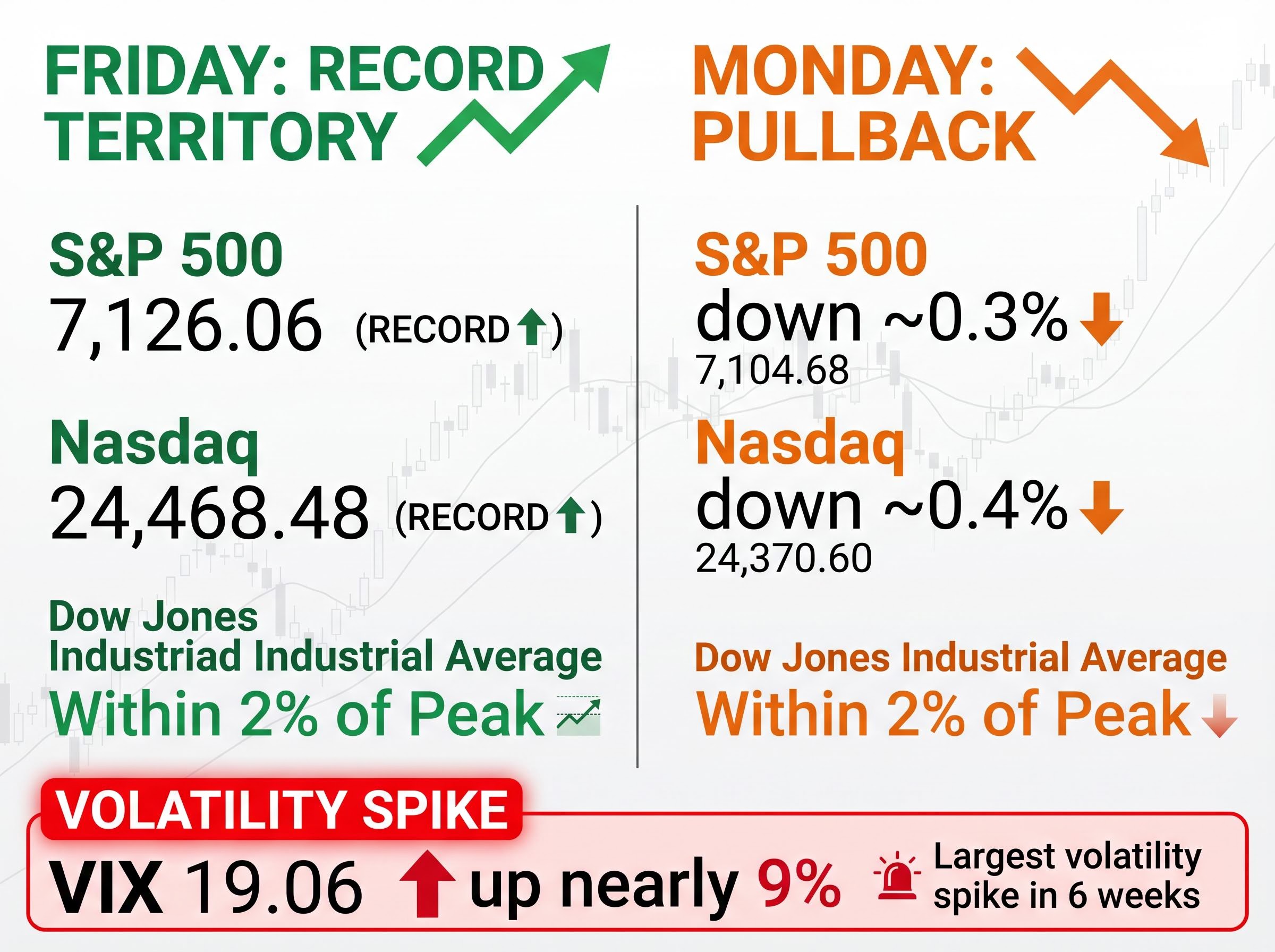

The S&P 500 closed at a record 7,126.06 on Friday, with the Nasdaq reaching an all-time high of 24,468.48. By Monday’s close, both indices had retreated, the S&P 500 falling approximately 0.3% and the Nasdaq declining roughly 0.4%. The VIX climbed nearly 9% to 19.06, marking the sharpest volatility spike since early March. Three simultaneous uncertainties drove the pullback: Iran’s Wednesday cease-fire deadline, Kevin Warsh’s Tuesday confirmation hearing for Federal Reserve Chair, and the Magnificent Seven earnings season beginning next week. What follows is an analysis of what triggered Monday’s decline, why strategists view the move as orderly consolidation rather than a correction signal, and which catalysts will determine whether markets resume their advance or face extended pressure.

Friday delivered record closes across major U.S. equity indices. The S&P 500 hit 7,126.06, the Nasdaq reached 24,468.48, and the Dow held within 2% of its own peak. Monday reversed that momentum, but the character of the decline mattered more than its magnitude.

The S&P 500’s climb to 7,000 on 15 April marked the culmination of a multi-week rally driven by initial cease-fire optimism, a move that established the valuation baseline from which Monday’s pullback is now being measured.

The S&P 500 fell approximately 0.3% from Friday’s record. The Nasdaq declined roughly 0.4% from its all-time high. The Dow remained within 2% of its recent peak. The VIX climbed nearly 9% to 19.06, the largest single-day volatility spike in six weeks.

The VIX’s 9% climb to 19.06 represents the steepest single-day increase since early March, though the index remains below the 20-level threshold that the Cboe VIX methodology white paper identifies as marking sustained market anxiety. Strategists interpret the current reading as elevated caution rather than panic, consistent with profit-taking following record closes rather than defensive repositioning ahead of broader risk.

VIX climbed nearly 9% to 19.06 on Monday, April 21, marking the sharpest single-day volatility increase since early March.

Strategists characterised the pullback as profit-taking following record highs rather than a sentiment shift. The absence of broad-based selling pressure, coupled with the VIX holding below 20, suggested consolidation rather than the start of a deeper correction. Trading volumes remained within normal ranges, and sector rotation reflected tactical repositioning rather than defensive exits.

Friday’s optimism about the Strait of Hormuz evaporated over the weekend. President Donald Trump announced progress toward a temporary cease-fire on Friday, with markets interpreting the development as easing immediate supply risk. By Saturday, Iranian forces had intercepted a cargo vessel in disputed waters, and by Monday morning, Trump stated an extension beyond Wednesday’s deadline was highly unlikely absent a formal deal.

Iran’s pattern of closing and re-opening the Strait, which has occurred twice in the past week alone, creates volatility whiplash where oil prices surge on closure announcements and then partially reverse on re-opening, preventing traders from establishing stable positioning around any single scenario.

The sequence of events compressed into 72 hours:

Oil markets absorbed the uncertainty. U.S. crude rose approximately 5.8% to around $87 per barrel. Brent crude advanced roughly 5.6% to approximately $95 per barrel. Edward Jones analyst noted the risk of oil returning above $100 has diminished compared to a month ago, but the Wednesday deadline keeps short-term volatility elevated.

Oil markets absorbed the uncertainty with U.S. crude rising approximately 5.8% to around $87 per barrel and Brent crude advancing roughly 5.6% to approximately $95 per barrel, price movements Gulf News oil market coverage from 21 April attributed to traders recalibrating the probability of cease-fire extension versus sustained Middle East supply disruption. The $100 per barrel threshold that dominated headlines in March now appears less likely absent a complete breakdown in negotiations, though Wednesday’s deadline keeps short-term volatility elevated.

“An extension is highly unlikely absent a deal,” Trump stated in remarks on Monday, framing Wednesday’s deadline as a hard stop rather than a negotiable timeline.

The geopolitical risk premium re-entered equity pricing. Energy sector positioning shifted toward defensive hedges, and inflation-sensitive sectors absorbed selling pressure as traders recalibrated Federal Reserve rate-cut probabilities against the possibility of sustained oil price strength.

The cross-asset price movements driven by Iran tensions extend beyond equities into Treasury yields, credit spreads, and currency markets, with the correlation between oil price spikes and inflation expectations reaching levels not seen since the 2022 energy crisis.

Monday’s 0.3% to 0.4% declines remain far below the thresholds that define market corrections. Understanding the difference between routine profit-taking and warning signals requires context on how strategists classify market declines.

| Classification | Percentage Decline | Typical Duration | Historical Frequency |

|---|---|---|---|

| Pullback | 3-5% | 2-4 weeks | 3-4 times per year |

| Correction | 10%+ | 2-4 months | Once every 1-2 years |

| Bear Market | 20%+ | 6-18 months | Once every 3-5 years |

Pullbacks following record highs are historically normal. Investors lock in gains after extended rallies, creating temporary selling pressure that resets overbought conditions without damaging the underlying trend. The VIX at 19.06 is elevated compared to its sub-15 readings during the March rally, but it remains below the 20+ level often associated with sustained market anxiety.

Warning signs that would elevate concern include sustained VIX readings above 25, breadth deterioration where declining stocks outnumber advancing stocks for multiple consecutive sessions, and bond market stress signalled by sharp Treasury yield moves. The 10-year Treasury yield held steady at 4.260% on Monday, indicating no credit market stress or flight-to-quality positioning. Pullbacks become corrections when multiple warning signals align, and Monday’s session showed none of those patterns.

For readers wanting to understand portfolio positioning during volatile periods, our dedicated guide to strategies for navigating market volatility walks through defensive sector allocation, options hedging techniques, and cash management approaches that have proven effective during the Iran crisis.

Kevin Warsh faces the Senate Banking Committee on Tuesday for his confirmation hearing as the next Federal Reserve Chair. His prepared testimony includes a statement that the Fed must “accept accountability for inflation” to strengthen its independence, a framing that signals potential divergence from the Powell era’s communication style.

The market’s current comfort rests on the Fed’s 12-member rate-setting committee broadly resisting rate cuts despite political pressure. Powell’s term expires mid-May, creating a narrow window where interim arrangements will bridge to Warsh’s confirmation. Market expectations reflect no rate changes through at least the first half of 2026, a baseline Warsh’s hearing could either reinforce or complicate.

“The Federal Reserve must accept accountability for inflation to strengthen its independence,” Warsh stated in prepared testimony, positioning accountability as the foundation for credible policy.

Warsh’s emphasis on accountability could shift how the Fed communicates forward guidance. If his approach involves more explicit acknowledgment of past policy errors, markets may recalibrate inflation expectations and rate-cut timelines. The Tuesday hearing will reveal whether Warsh’s independence framing aligns with the current committee’s resistance to premature easing or introduces new tensions.

Fed leadership transitions historically create volatility around rate expectations. Warsh’s judicial background and his service on the Federal Reserve Board during the 2008 financial crisis give him credibility on crisis management, but his views on the current inflation environment remain less defined than Powell’s established stance. The hearing’s Q&A session will determine how markets price the transition.

Two primary catalysts will determine whether Monday’s pullback extends or reverses: the Iran cease-fire resolution on Wednesday and the Magnificent Seven earnings season beginning next week.

Ameriprise strategists noted that a cease-fire extension would allow market focus to return to constructive fundamentals, particularly the strong earnings growth projections underpinning current valuations. Without an extension, sustained oil price strength would pressure inflation expectations and delay Federal Reserve rate-cut scenarios, creating headwinds for growth-sensitive sectors.

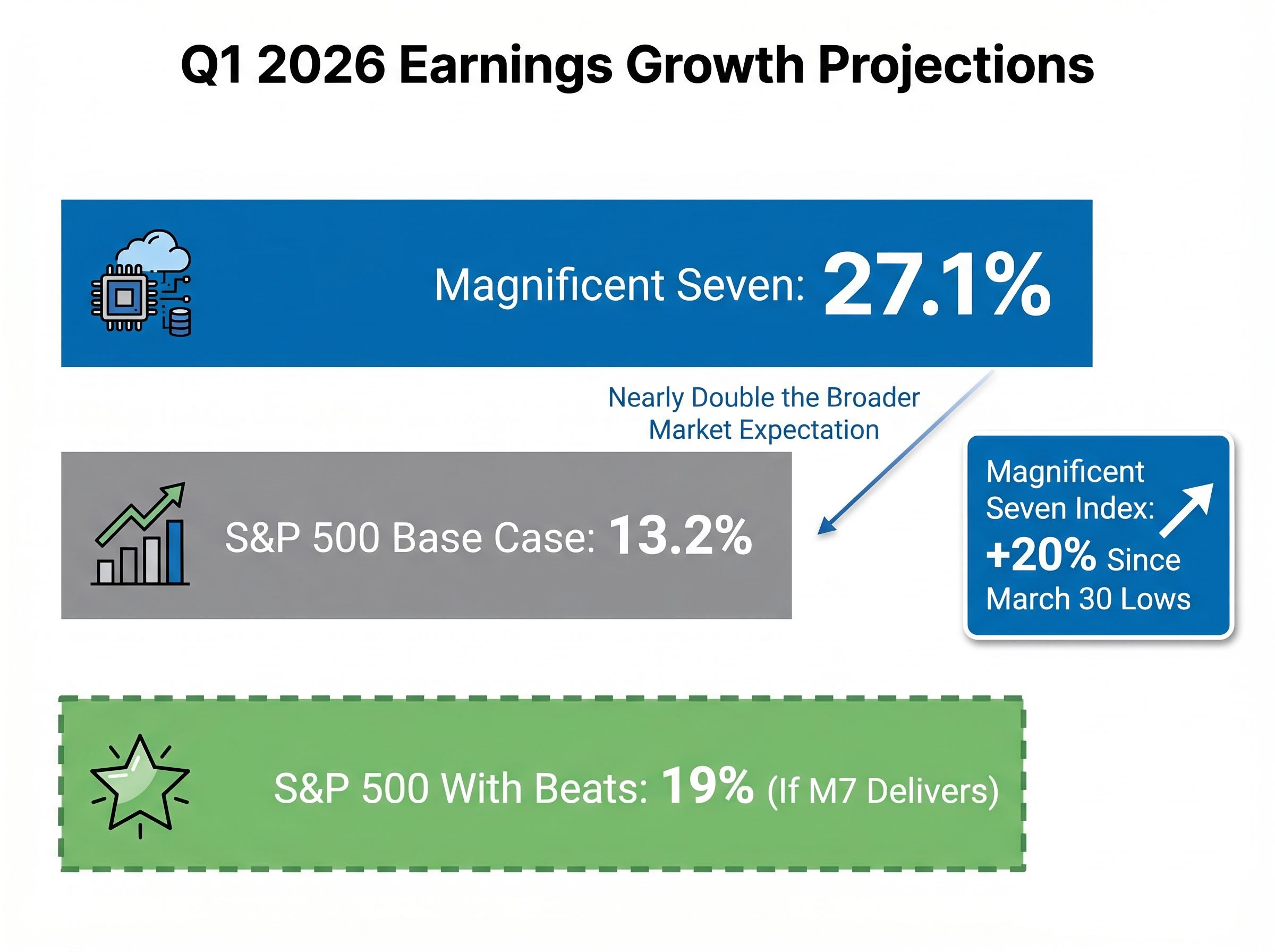

The Magnificent Seven face heightened scrutiny. Consensus projects 27.1% earnings growth for Q1 2026, nearly double the S&P 500’s broader base case of 13.2%. If earnings beats materialise, the S&P 500 could reach 19% growth for the quarter. Tesla is scheduled to report during the week of 20 April, with the remaining members following.

Magnificent Seven Q1 2026 earnings growth projection: 27.1%, compared to the S&P 500’s 13.2% base case.

Key catalysts and timelines:

The Magnificent Seven tracking index has gained 20% since 30 March lows, creating elevated entry points that require strong earnings delivery to justify. If results meet the 27.1% growth expectation and forward guidance remains optimistic, the rally resumes. If results disappoint or guidance reflects caution on AI capital expenditure, the pullback extends.

Monday’s pullback reflects a market digesting multiple uncertainties simultaneously rather than a fundamental shift in the rally’s foundation. The 0.3% to 0.4% declines and the VIX’s climb to 19.06 signal tactical repositioning, not the breadth deterioration or bond market stress that precedes deeper corrections.

The Wednesday cease-fire deadline, Tuesday’s Warsh confirmation hearing, and next week’s Magnificent Seven earnings will determine near-term direction. Strategists view a cease-fire extension as the key unlock that would return attention to the strong earnings fundamentals driving the expansion. Without it, oil price strength and inflation concerns create headwinds that could extend consolidation through the remainder of April.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

A stock market pullback is a short-term decline of 3-5% that typically lasts 2-4 weeks, representing normal profit-taking after a rally. A correction is a steeper decline of 10% or more and is distinct from the minor 0.3-0.4% moves seen on Monday, April 21.

Three simultaneous uncertainties drove Monday's pullback: Iran's Wednesday cease-fire deadline, Kevin Warsh's Tuesday Senate confirmation hearing for Federal Reserve Chair, and the start of Magnificent Seven earnings season the following week.

Strategists generally treat sustained VIX readings above 20 as a sign of elevated market anxiety, with readings above 25 raising more serious concern. Monday's VIX reading of 19.06, while up nearly 9%, remained below those warning thresholds.

If no deal is reached by Wednesday's deadline, sustained oil price strength could push inflation expectations higher and delay Federal Reserve rate cuts, creating headwinds for growth-sensitive sectors. U.S. crude had already risen approximately 5.8% to around $87 per barrel on the uncertainty.

Consensus projects 27.1% earnings growth for the Magnificent Seven in Q1 2026, nearly double the broader S&P 500 base case of 13.2%, making their upcoming results a critical test for whether the market rally resumes or extends its consolidation.