Three Banks Downgrade SKF as Goldman Moves Buy to Sell

Key Takeaways

- Goldman Sachs made the sharpest move, downgrading SKF from Buy to Sell with a reduced price target of SEK 237, while J.P. Morgan cut its target to SEK 215 and RBC Capital moved to Sector Perform, all within days in April 2026.

- SKF's failure to meet the strategic targets set at its 2022 Capital Markets Day has created a credibility gap that analysts say now shadows its newly announced 4.5% organic CAGR and 17% EBIT margin goals for 2025-2028.

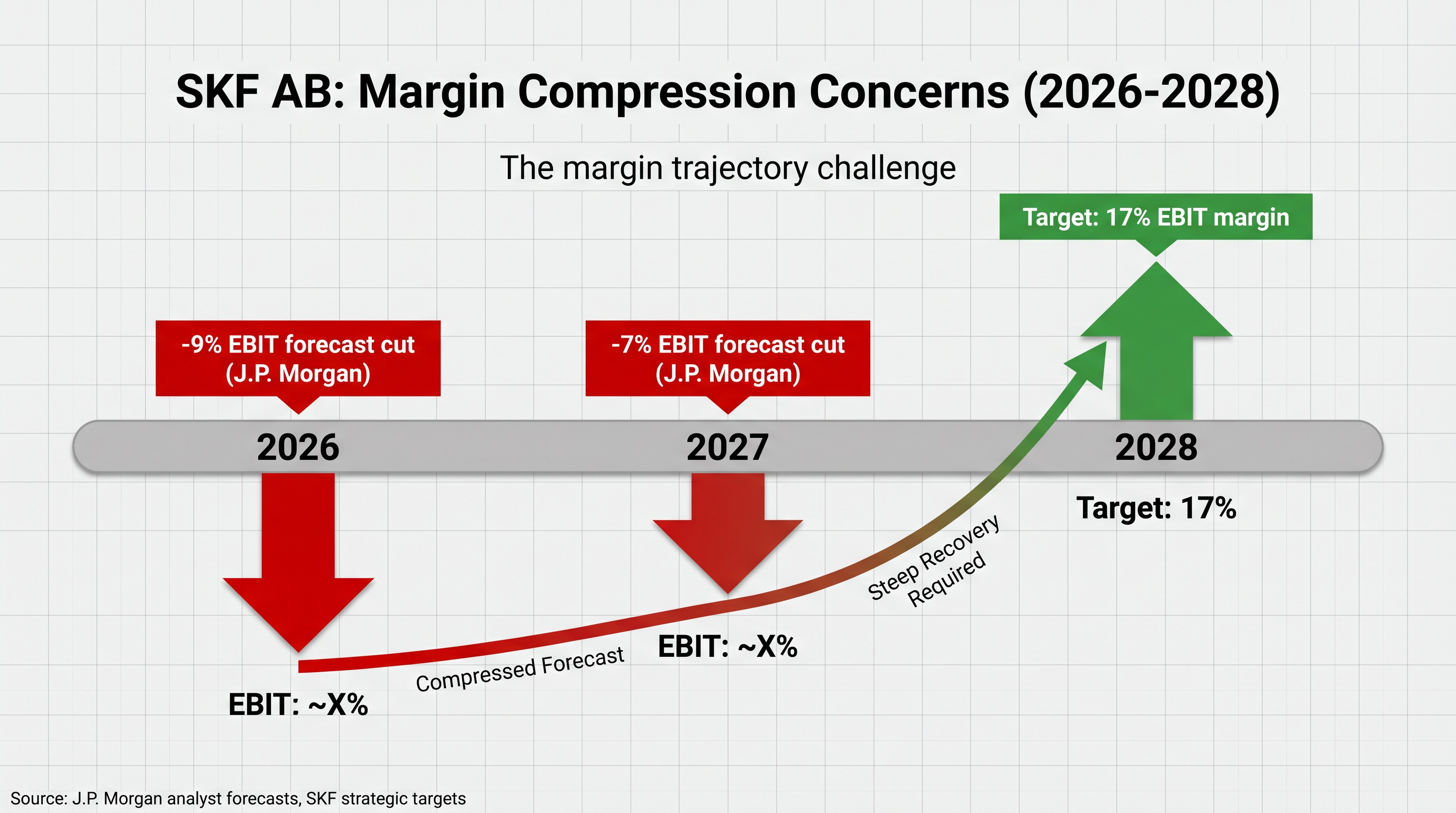

- The delayed automotive division spin-off, now pushed to the second half of 2026, adds execution risk, with J.P. Morgan cutting EBIT forecasts by 9% for 2026 and 7% for 2027 partly on this basis.

- SKF's 32-year consecutive dividend track record and current 2.8% yield offer income continuity, but analysts remain divided on whether the stock's compressed price targets represent a temporary reset or a longer structural reassessment.

- Key catalysts to watch include Q1 2026 earnings results, any management response to the downgrades, and updates on the automotive spin-off timeline and strategic rationale.

Three major investment banks cut their ratings on SKF AB within days in April 2026, with Goldman Sachs moving directly from Buy to Sell and J.P. Morgan slashing its price target by SEK 30. The coordinated downgrades arrive despite SKF shares delivering a 51% gain over the past twelve months, reflecting deep analyst scepticism about whether the bearing manufacturer can achieve its newly announced strategic targets after missing its previous goals. This article breaks down each downgrade, the specific concerns driving the bearish pivot, and what the analyst consensus shift signals for SKF shareholders navigating the months ahead.

Three banks cut SKF ratings in April

The downgrade wave hit with coordinated force. RBC Capital moved first on 20 April 2026, cutting SKF to Sector Perform from Outperform and trimming its price target to SEK 235 from SEK 240. Goldman Sachs followed with the sharpest move, dropping the stock to Sell from Buy and lowering its target to SEK 237 from SEK 251. J.P. Morgan delivered the most aggressive forecast revision, downgrading to Underweight from Neutral and slashing its June 2027 price target to SEK 215 from SEK 245.

The range of severity tells the story. RBC’s Sector Perform reflects caution without outright bearishness. Goldman’s Sell is an explicit call to exit. J.P. Morgan’s cuts extended beyond the rating, with EBIT forecasts reduced by 9% for 2026 and 7% for 2027.

When multiple tier-one banks pivot bearish on the same stock within days, it signals a fundamental reassessment of risk, not idiosyncratic views. Investors need to understand what drove this consensus shift.

Market reactions to earnings beats when forward guidance disappoints often see coordinated analyst downgrades follow within days, as institutional investors reassess valuation based on reduced forward estimates rather than backward-looking results, a pattern that explains sharp post-earnings declines despite headline metric beats.

| Bank | Prior Rating | New Rating | Prior Price Target | New Price Target |

|---|---|---|---|---|

| RBC Capital | Outperform | Sector Perform | SEK 240 | SEK 235 |

| Goldman Sachs | Buy | Sell | SEK 251 | SEK 237 |

| J.P. Morgan | Neutral | Underweight | SEK 245 | SEK 215 |

When big ASX news breaks, our subscribers know first

Missed targets and credibility gaps fuel analyst concern

The downgrades are not about current quarter results. They are about a pattern of strategic underdelivery that makes analysts sceptical even after strong stock performance.

SKF failed to meet the growth and profitability objectives set at its 2022 Capital Markets Day for the 2021 to 2025 period. That miss created a credibility gap that now shadows the company’s newly announced long-term goals. RBC Capital stated the 2025 to 2028 strategic targets deserve significant scepticism given the prior track record. Goldman Sachs acknowledged SKF may still meet its 2025 Capital Markets Day ambitions but questioned the growth trajectory versus capital goods peers.

The 2025 to 2028 targets are ambitious:

- 4.5% organic compound annual growth rate (CAGR)

- 17% EBIT margin by 2028

These goals require execution discipline that the company has not yet demonstrated over a multi-year period. The 51% one-year stock return makes the downgrade timing notable, as analysts are calling the peak despite recent outperformance. InvestingPro analysis suggests slight undervaluation at current prices, but valuation alone does not determine stock trajectory when management credibility is in question.

Turnaround credibility patterns and EBITDA trajectory validation typically require companies to deliver multiple consecutive quarters of operational improvement before analysts upgrade forward targets, a threshold that explains why strong recent stock performance alone does not prevent downgrades when execution risk on new strategic goals remains unproven.

RBC Capital on Strategic Targets “The newly announced long-term goals from the 2025 Capital Markets Day deserve significant scepticism given the company’s failure to meet prior strategic objectives.”

Valuation alone does not determine stock trajectory when management credibility is in question. The credibility gap from missed prior targets shapes how analysts weight forward guidance, a dynamic that affects how new targets are priced into the stock.

Automotive spin-off delays add execution risk

The delayed automotive division separation compounds the credibility concerns already established. The spin-off, originally planned for earlier execution, is now pushed to H2 2026 (second half of 2026). J.P. Morgan specifically cited this delay as contributing to margin risk and downgrade rationale.

Automotive sector consolidation and separation dynamics in 2026 reflect divergent strategic paths, with some companies pursuing acquisitions to gain scale while others pursue spin-offs to isolate underperforming divisions, creating valuation uncertainty until post-transaction performance clarifies which approach unlocks value.

RBC Capital went further, calling the spin-off itself a strategic error. The firm argued the separated automotive bearing business will be small and minimally profitable, leaving questions about whether the restructuring unlocks value or simply isolates a struggling division. The post-spin-off structure positions SKF as a focused bearing manufacturer with healthier profitability, but the separated automotive unit faces an uncertain path.

J.P. Morgan’s margin concerns are specific:

- EBIT forecast cuts: 9% for 2026, 7% for 2027

- Foreign exchange (FX) headwinds creating additional strain on profitability

- Automotive end-market weakness extending pressure on the division awaiting separation

Spin-offs are meant to unlock value, but execution delays and disagreement over strategic merit (with RBC calling it a misjudgement) create uncertainty that weighs on valuation multiples until clarity emerges.

Margin compression risks for 2026 and 2027

J.P. Morgan’s EBIT forecast cuts of 9% for 2026 and 7% for 2027 reflect a view that near-term profitability will deteriorate before the company can execute on its 17% EBIT margin target by 2028. FX headwinds add to the pressure, with currency movements expected to compress margins further in a period when operational execution is already under scrutiny.

The margin trajectory matters because hitting the 2028 target requires not just stabilisation but sequential improvement from a lower base. If 2026 and 2027 deliver weaker margins than previously forecast, the climb to 17% becomes steeper, and the credibility of the long-term target weakens further.

The next major ASX story will hit our subscribers first

What the analyst shift means for shareholders

The consensus price target range now spans from SEK 190 (pessimistic) to SEK 280 (optimistic), a spread that signals material uncertainty about SKF’s forward trajectory. The width of this range reflects divergent views on execution risk, automotive exposure, and whether management can close the credibility gap with delivered results.

Dividend continuity provides some downside support. SKF has maintained its dividend for 32 consecutive years, with a current yield of 2.8%. Income-focused investors may find this track record reassuring, particularly if the company prioritises shareholder returns even as it navigates strategic challenges. Growth-oriented shareholders, however, must weigh whether the compressed analyst targets reflect a temporary reset or a longer structural reassessment of SKF’s position versus capital goods peers.

Dividend Track Record SKF has paid dividends for 32 consecutive years, currently yielding 2.8%, providing income continuity even amid strategic uncertainty.

The absence of management response to the downgrades is notable. As of 20 April 2026, no official company statement has addressed the analyst concerns, the automotive spin-off delays, or the revised price targets. This silence leaves shareholders without updated context on how management views the bearish pivot or what actions might address the execution risks flagged by major banks.

Key watchpoints for shareholders:

- Q1 2026 earnings results and accompanying management commentary

- Updated guidance on the automotive spin-off timeline and strategic rationale

- Management response to analyst downgrades and credibility concerns

- Margin trajectory in upcoming quarters relative to the 17% EBIT target

Income-focused investors may find the dividend continuity reassuring, while growth-oriented shareholders must weigh whether the compressed analyst targets reflect a temporary reset or a longer structural reassessment of SKF’s position versus capital goods peers.

Conclusion

The coordinated April 2026 downgrades from RBC Capital, Goldman Sachs, and J.P. Morgan represent a meaningful inflection point for SKF shareholders. Analysts have moved from optimism to explicit concern over strategic credibility, automotive exposure, and execution risk on the planned spin-off. The 51% one-year gain now faces a reassessment driven by missed prior targets, delayed restructuring, and margin compression forecasts for 2026 and 2027.

Key catalysts to monitor include Q1 2026 earnings, any management response to the downgrades, and updates on the H2 2026 automotive spin-off timeline. Shareholders should reassess their position sizing and risk tolerance in light of the compressed price targets and margin concerns flagged by major banks.

Portfolio diversification strategies during sector-specific downgrade cycles involve assessing whether concentrated exposure to capital goods manufacturers justifies rebalancing into international equities or defensive sectors, particularly when analyst consensus shifts create near-term volatility that may not reflect long-term fundamentals.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

Why did Goldman Sachs downgrade SKF stock?

Goldman Sachs downgraded SKF from Buy to Sell in April 2026, lowering its price target to SEK 237 from SEK 251, citing concerns about SKF's growth trajectory versus capital goods peers and scepticism about whether the company can meet its newly announced 2025 to 2028 strategic targets after failing to deliver on prior goals.

What is the SKF automotive spin-off and why is it delayed?

SKF is separating its automotive bearing division from its core industrial operations, with the spin-off now pushed to the second half of 2026. J.P. Morgan cited this delay as a contributor to margin risk, while RBC Capital went further and called the spin-off itself a strategic error, arguing the separated unit will be small and minimally profitable.

What are SKF's 2028 financial targets?

SKF announced a 4.5% organic compound annual growth rate and a 17% EBIT margin target by 2028 at its 2025 Capital Markets Day, though analysts have expressed significant scepticism about these goals given the company's failure to meet similar targets set at its 2022 Capital Markets Day.

How much have SKF shares gained over the past year despite the downgrades?

SKF shares delivered a 51% gain over the twelve months prior to the April 2026 downgrades, making the analyst pivot notable as banks are effectively calling a peak despite recent outperformance, citing forward execution risk rather than backward-looking results.

Does SKF pay a reliable dividend during this period of analyst downgrades?

SKF has maintained its dividend for 32 consecutive years and currently yields 2.8%, providing some downside support for income-focused investors even as growth-oriented shareholders face compressed analyst price targets and strategic uncertainty.