US vs Europe: Why the Case for American Stocks Just Strengthened

Key Takeaways

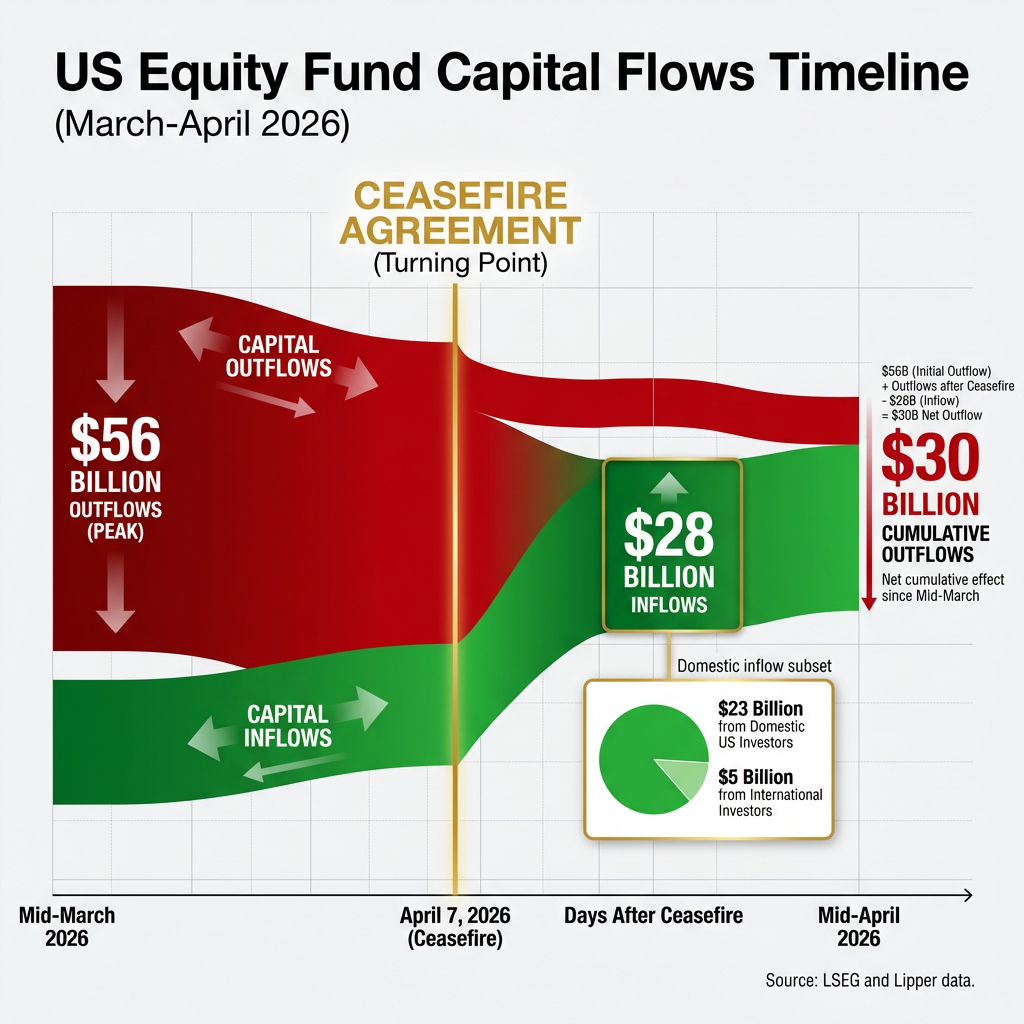

- The April 7 US-Iran ceasefire triggered $28 billion in net inflows into US equity funds, reversing months of outflows and reviving the TINA investment thesis over the competing TIARA framework.

- The S&P 500 crossed 7,000 during the week of 19 April 2026, gaining over 10% in just 11 trading sessions, one of only 15 such occurrences since 2000 according to Deutsche Bank strategist Jim Reid.

- S&P 500 companies are projected to deliver approximately 13.2% earnings growth in Q1 2026, marking a sixth consecutive quarter of double-digit expansion, compared to roughly 4.2% for Eurozone firms.

- Morgan Stanley Investment Management, which oversees nearly $2 trillion in assets, reversed its European overweight position and is considering moving to an underweight, reflecting broader institutional reallocation toward US equities.

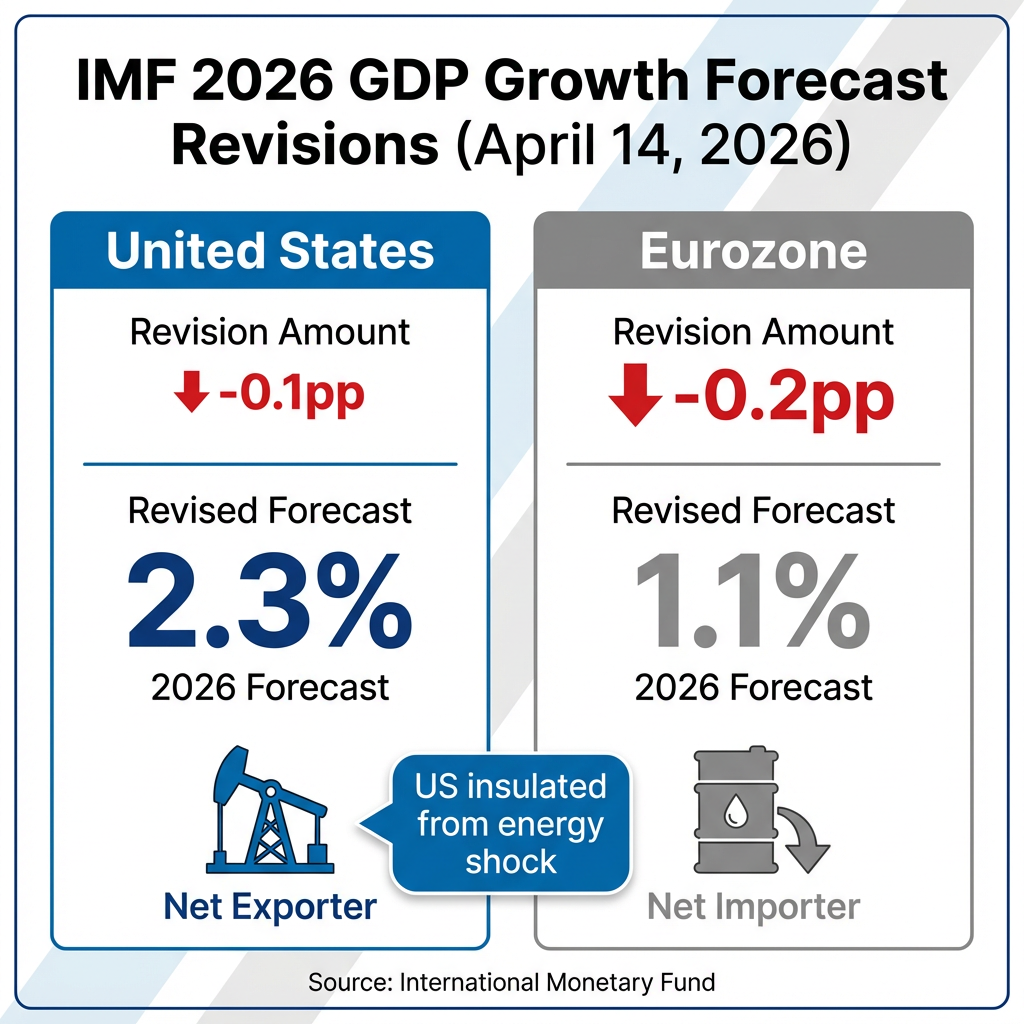

- America's net energy exporter status provided a structural buffer during the oil price spike toward $120 per barrel, with the IMF cutting US 2026 GDP growth by only 0.1 percentage points versus a steeper 0.2 percentage point reduction for the Eurozone.

The April 7 ceasefire between the United States and Iran triggered a capital reallocation of historic proportions. $28 billion in net inflows poured into US equity funds in the days following the truce, reversing months of outflows that had reached $56 billion year-to-date before the announcement. President Trump’s declaration that the Strait of Hormuz crisis had ended sent a clear signal to global investors: the risk-off trade was over, and capital was coming home.

The speed of the reversal startled even seasoned strategists. $23 billion of the $28 billion inflow came from domestic US investors who had rotated into international markets during the conflict. By mid-April, cumulative net outflows from US equities stood at just $30 billion, roughly one quarter of the $56 billion peak reached in mid-March, according to LSEG and Lipper data.

The S&P 500 now trades approximately 2% above pre-conflict levels, outperforming most global indices that merely recovered their war-related declines. The index’s resilience during the crisis and its surge following the ceasefire have reignited a debate Wall Street thought it had settled: US versus European stocks.

TINA vs TIARA: Understanding the Investment Thesis Battle

For years, institutional investors operated under a simple framework: There Is No Alternative (TINA). The thesis held that US equities offered superior risk-adjusted returns compared to any other major market, driven by earnings growth, innovation leadership, and deep capital markets.

Then came January 2025 and the start of Donald Trump’s second presidential term. A competing thesis emerged: There Is A Real Alternative (TIARA). Proponents pointed to dollar weakness, artificial intelligence enthusiasm lifting international technology sectors, and large-scale government expenditure programmes boosting markets in Germany, the United Kingdom, South Korea, and Japan. For the first time in a decade, the consensus began to fracture.

The US-Iran conflict and its resolution killed the TIARA trade. The energy shock exposed a fundamental vulnerability that academic models had underweighted: energy-importing nations face structural disadvantages compared to America’s net energy exporter status. When oil prices spiked toward $120 per barrel, European and Asian markets absorbed the cost directly. The ceasefire did not just end a crisis. It reminded investors why TINA existed in the first place.

The International Energy Agency characterised the crisis as the greatest global energy security challenge in history, a designation that reflects the Strait of Hormuz’s role in transporting roughly 20% of global oil supply before the blockade.

When big ASX news breaks, our subscribers know first

The S&P 500’s Historic Surge Past 7,000

The S&P 500 crossed 7,000 during the week of 19 April 2026, capping a rally that gained over 10% in just 11 trading sessions. The speed caught attention across trading desks and risk committees.

According to Deutsche Bank strategist Jim Reid, a gain of 10% or more within 11 trading sessions has occurred only 15 times since 2000, excluding overlapping periods. The April rally outpaced even the rebound following President Trump’s April 2025 ‘Liberation Day’ tariff announcement, which had itself been considered unusually swift.

The milestone is both psychological and substantive. Crossing 7,000 signals investor confidence in US equity fundamentals, but the VIX at 17.48 suggests the market retains some measure of caution. This is not euphoria. It is conviction tempered by awareness that geopolitical risks persist.

The mechanics of how US equity markets absorbed and reversed the crisis-driven selloff involved coordinated central bank liquidity provisions, sector rotation into energy and defense, and sustained institutional buying during the March drawdown that created the technical foundation for April’s surge.

Institutional Exodus: Why Major Firms Are Downgrading Europe

Morgan Stanley Investment Management oversees nearly $2 trillion in assets. On 10 April 2026, Chief Investment Officer Jim Caron indicated during a virtual roundtable that the firm no longer expects European equities to outperform US stocks, reversing the consensus view MSIM had held through much of 2025. The firm is actively reducing European overweights and considering moving to an underweight position.

Franklin Templeton Institute’s Global Investment Strategist Michael Browne characterised the conflict as the fourth major external shock in six years. His team maintained a more constructive outlook on US equities from the start of 2026, anticipating that the conflict’s economic impact would disproportionately affect Europe and parts of Asia. The thesis has been validated by the data.

Capital outflows from non-US markets accelerated following the ceasefire, according to Bank of America’s weekly report citing EPFR data for the week ending 15 April 2026:

- European equity funds experienced $4.7 billion in outflows, the largest weekly withdrawal since November 2024

- South Korean funds saw record withdrawals of $2.5 billion

- Emerging market equity funds recorded net outflows for the third consecutive week

Several large investment banks upgraded US equity ratings from neutral to overweight in the days preceding 19 April, citing strong corporate earnings, particularly in the technology sector, as a buffer against residual consequences from the Middle East conflict.

The portfolio diversification implications of the TIARA reversal extend beyond simple US overweighting; investors who built international exposure during 2025 now face decisions about whether to fully exit European and Asian positions or maintain reduced allocations as long-term hedges against dollar weakness and future US policy risk.

The Earnings Divide: 14% US Growth vs 4% Eurozone

The capital flow reversal is not sentiment alone. It is backed by a stark divergence in corporate profit growth. S&P 500 companies are projected to deliver approximately 13.2% earnings growth for Q1 2026, according to LSEG and IBES data. Eurozone firms are forecast to grow earnings by roughly 4.2% over the same period.

| Metric | S&P 500 (US) | Eurozone |

|---|---|---|

| Q1 2026 Earnings Growth | ~13.2% | ~4.2% |

| Growth Drivers | Technology, energy, banking (broad-based) | Oil and gas (concentrated) |

| Consecutive Double-Digit Quarters | Sixth straight quarter | N/A |

| Sector Diversification | High | Low (narrow base) |

FactSet’s blended estimate as of early April projected 13.2% year-over-year S&P 500 earnings growth, marking a sixth consecutive quarter of double-digit expansion. US growth is broad-based, spanning technology, energy, and banking sectors. European growth, by contrast, is concentrated in oil and gas, creating vulnerability to sector-specific risks.

Analysts have raised questions about whether oil-driven costs and softening business confidence will pressure Q2 guidance. Final Q1 2026 earnings results have not been reported, but the projection gap is significant enough to drive allocation decisions now.

The next major ASX story will hit our subscribers first

America’s Structural Advantage: Energy Independence in Focus

The United States is a net energy exporter. Europe and Japan are importers. During the conflict, that distinction became a structural moat.

When oil prices spiked, energy-importing nations faced immediate economic pressure. Higher input costs compressed corporate margins, reduced consumer spending power, and triggered growth downgrades. The US, by contrast, benefited from record oil exports that partially offset the broader economic drag from elevated prices.

The International Monetary Fund validated this asymmetry on 14 April 2026 when it revised 2026 GDP growth forecasts. The fund cut US growth by only 0.1 percentage points to 2.3%, while eurozone growth was reduced by 0.2 percentage points to 1.1%. The relatively modest US downgrade reflected America’s greater insulation from the energy shock.

Oil prices have since stabilised at $90.12 per barrel for West Texas Intermediate, down from conflict highs near $120. Iran’s Foreign Minister Abbas Araqchi reported on 18 April that the Strait of Hormuz is “completely open” following the ceasefire. While tensions could resurface, the structural advantage persists regardless of short-term geopolitical noise.

What This Means for Global Investors

The weight of evidence points in one direction. The TINA thesis has been revived by the ceasefire sequence. Institutional capital is repositioning toward US equities based on earnings divergence, energy resilience, and the recognition that structural advantages matter during periods of geopolitical stress.

Yet risks remain. Investors should weigh the following considerations:

- The ceasefire’s extension remains uncertain, with potential expiration looming in the week following 17 April

- Charles Schwab characterised the rally as a “relief rally” without resolution of underlying geopolitical tensions

- Gold at $4,879.60 (up 1.48% on the week) suggests hedging activity continues among institutional portfolios

- The strong US dollar, with the DXY near 100, may pressure earnings for US multinationals with significant international exposure

- Q2 earnings guidance remains uncertain as analysts assess whether oil-driven costs will compress margins

Franklin Templeton’s Michael Browne described the conflict as the fourth major external shock in six years. The observation carries weight. Flexibility and vigilance remain essential as the geopolitical situation continues to evolve. The case for US equities over European stocks is strong for now, but the next shock is always closer than consensus expects.

—

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

For investors seeking tactical frameworks to navigate ongoing geopolitical uncertainty, our comprehensive guide to investing during market volatility in 2026 examines sector rotation strategies, safe-haven asset allocation, and portfolio hedging techniques validated during the February-April crisis period.

Frequently Asked Questions

What is the TINA vs TIARA debate in stock market investing?

TINA stands for There Is No Alternative, the long-held view that US equities offer superior risk-adjusted returns. TIARA, or There Is A Real Alternative, emerged in early 2025 as dollar weakness and international AI enthusiasm made European and Asian markets more attractive; the US-Iran ceasefire has since revived the TINA thesis.

Why are institutional investors moving from European stocks to US equities in 2026?

Major firms including Morgan Stanley Investment Management and Franklin Templeton are reducing European overweights due to a stark earnings gap, with S&P 500 companies projected to grow earnings by roughly 13.2% in Q1 2026 compared to approximately 4.2% for Eurozone firms, compounded by Europe's structural vulnerability as an energy importer.

How did the US-Iran ceasefire affect global capital flows?

Following the April 7 ceasefire, US equity funds received $28 billion in net inflows within days, reversing months of outflows, with $23 billion coming from domestic investors who had previously rotated into international markets during the conflict.

What structural advantage does the United States have over Europe during energy crises?

The United States is a net energy exporter, meaning oil price spikes that compress margins and consumer spending in energy-importing regions like Europe and Japan actually benefit US exporters, a structural moat validated by the IMF cutting US 2026 GDP growth by only 0.1 percentage points versus 0.2 percentage points for the Eurozone.

Is the S&P 500 rally following the ceasefire considered a genuine recovery or just a relief bounce?

The S&P 500 crossed 7,000 and gained over 10% in 11 trading sessions, a pace that has occurred only 15 times since 2000, but Charles Schwab characterised the move as a relief rally without resolution of underlying geopolitical tensions, and the VIX at 17.48 suggests conviction tempered by caution rather than outright euphoria.