Ackman’s $10B Bet: His Market Outlook for H2 2026

Key Takeaways

- Bill Ackman is raising up to $10 billion through a planned summer 2026 IPO, signalling strong conviction that durable growth companies remain attractively priced despite elevated index-level valuations.

- Pershing Square's $11.93 billion portfolio is concentrated in high-conviction positions including Uber, Amazon, and Meta, with recent additions made during temporary sell-offs triggered by capital expenditure announcements.

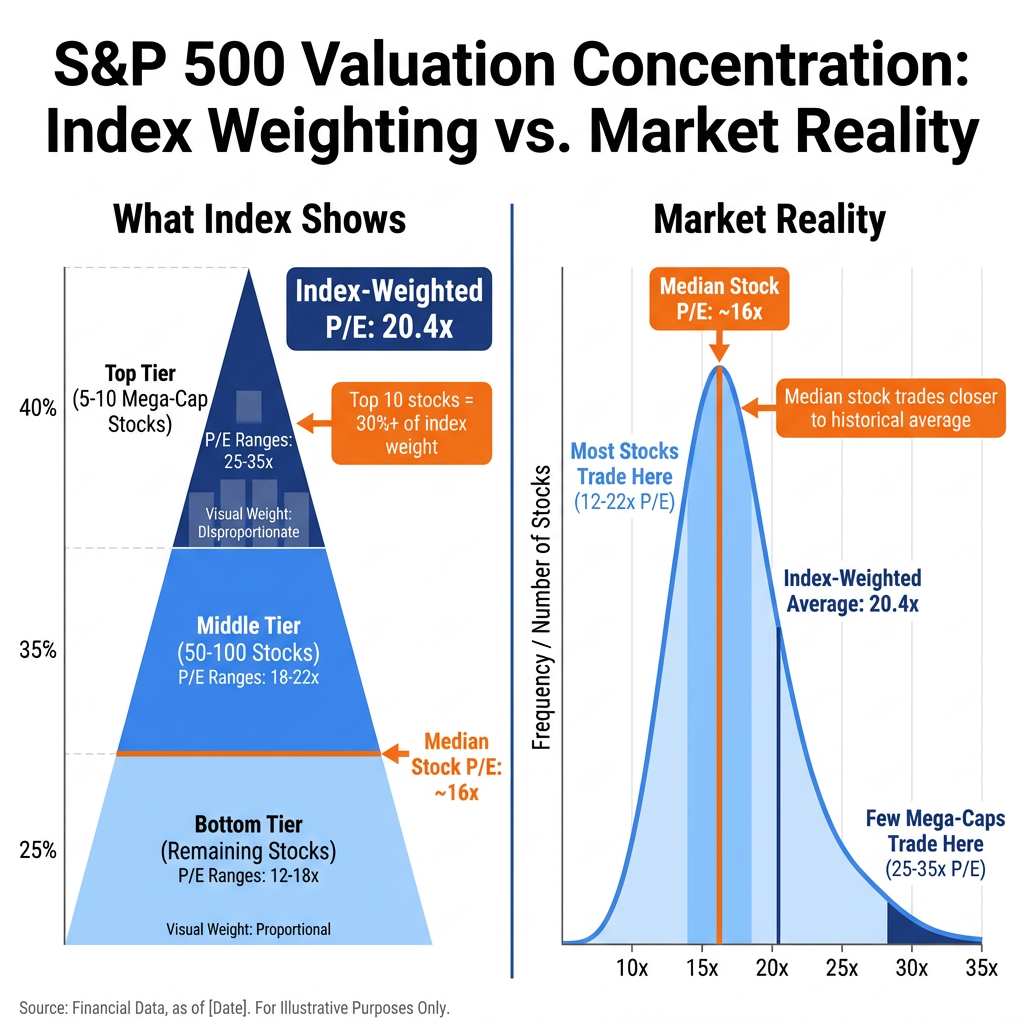

- Ackman argues that the S&P 500's forward P/E of 20.4x overstates broad market expensiveness because a small number of mega-cap companies distort the index-weighted average, making quality mid-cap names more reasonably priced.

- The Fannie Mae position represents a speculative, policy-dependent bet on GSE privatisation with a $193 billion capital deficit, carrying a fundamentally different risk profile than Ackman's core holdings.

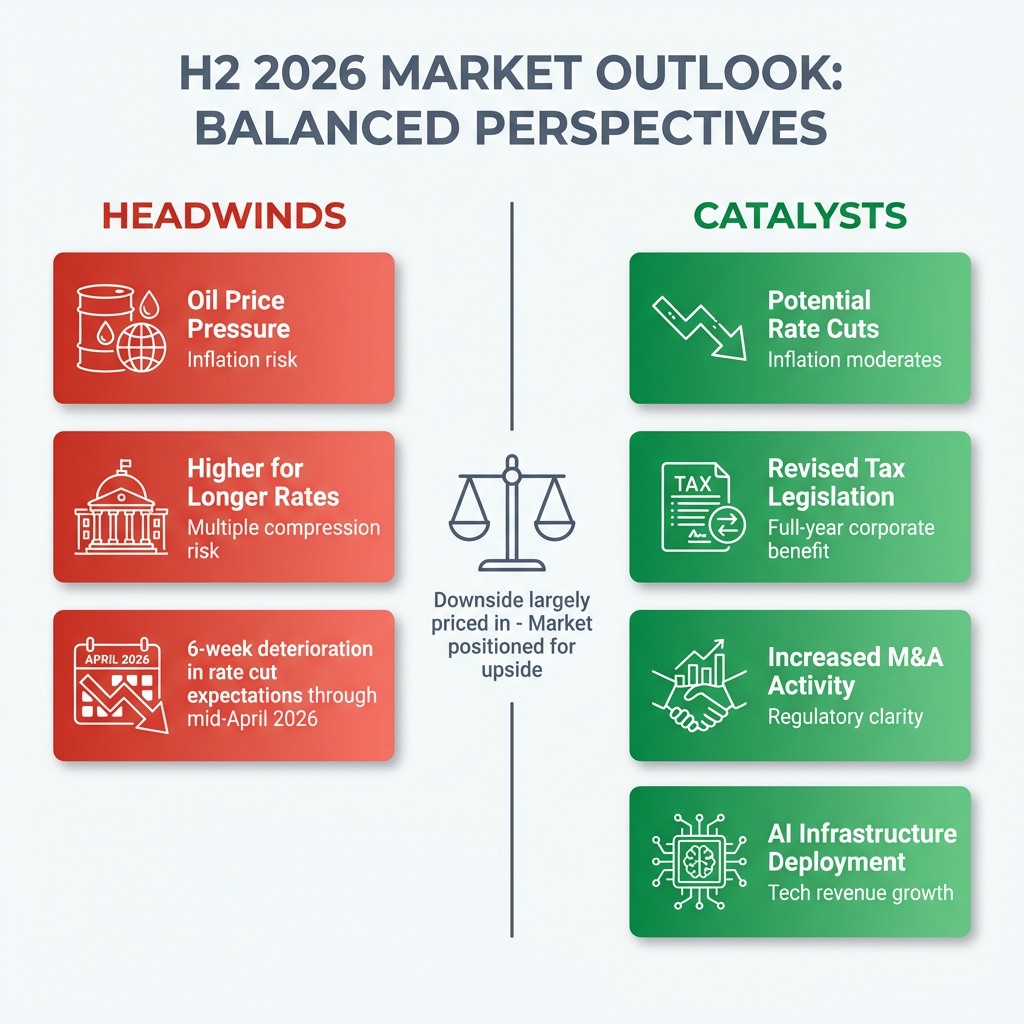

- Ackman identifies potential H2 2026 catalysts including rate cuts, full-year benefits from revised tax legislation, rising M&A activity, and AI infrastructure revenue growth for technology leaders.

With the S&P 500 trading near 7,126 at a forward P/E of 20.4x (well above the historical mid-to-high teens average), many investors are questioning whether elevated valuations signal caution. Hedge fund manager Bill Ackman, who oversees approximately $20 billion in assets through Pershing Square Holdings, is preparing to deploy up to $10 billion in fresh capital through a planned summer 2026 IPO. This raises a central question: what opportunities does one of the world’s most prominent activist investors see in markets that many perceive as richly valued?

Ackman’s approach provides a framework for understanding how selective positioning and a focus on durable competitive advantages can justify premium multiples. This analysis examines his current market outlook, portfolio positioning, macroeconomic views, and the strategic signals embedded in the upcoming Pershing Square U.S. fund launch.

Ackman’s Contrarian View on Market Valuations

Ackman contends that index-level P/E ratios mislead investors because concentration among a handful of dominant companies distorts aggregate metrics. The S&P 500’s forward P/E of 20.4x appears elevated compared to historical averages, but this figure is heavily influenced by a small number of highly valued technology and platform businesses. He argues that companies with durable structural advantages warrant premium multiples.

These structural advantages, often termed economic moats (a framework popularised by Warren Buffett), refer to competitive barriers that protect a company’s market position and pricing power. Characteristics include network effects, brand strength, regulatory barriers, or technological leadership that competitors cannot easily replicate. Ackman applies this framework to identify dominant large-cap companies with scale advantages and industry leadership that can sustain above-average growth rates.

The concentration dynamic works as follows: when a small number of mega-cap companies trade at elevated multiples, they drive up the index-weighted average P/E ratio. This means the median stock in the index may be more reasonably priced than the headline metric suggests. Investors who focus solely on index-level valuations may miss opportunities in quality businesses trading at fair prices relative to their growth prospects.

These dominant firms benefit from enormous capital available for investment in trends like artificial intelligence, reinforcing their competitive positions. Ackman’s thesis is that paying 22x or 32x earnings for companies delivering sustained 20%+ annual EPS growth represents rational valuation discipline, not speculation.

Understanding how to apply valuation metrics and forward P/E analysis to individual stocks helps investors assess whether premium multiples are justified by growth prospects and competitive positioning.

When big ASX news breaks, our subscribers know first

Inside Pershing Square’s Portfolio: Meta, Amazon, and Core Holdings

Pershing Square’s portfolio reflects high-conviction concentration in technology, mobility, and consumer brands. According to the most recent 13F filing dated 31 March 2025, the fund held $11.93 billion across a concentrated group of positions. Recent additions to Meta and Amazon positions demonstrate Ackman’s willingness to buy quality companies during temporary investor pessimism around capital expenditure announcements.

The SEC’s 13F filing requirements mandate that institutional investment managers with at least $100 million in assets under management disclose their equity holdings quarterly, providing investors with transparency into hedge fund portfolio positioning.

| Metric | Amazon (AMZN) | Meta Platforms (META) |

|---|---|---|

| Current Price | ~$238.98 | ~$628.55 |

| P/E Ratio | 32x | 22x |

| Expected EPS Growth | 20%+ | 20%+ |

| Analyst Buy Ratings | 64/68 Buy/Strong Buy | 61/67 Buy/Strong Buy |

| Market Cap | Data not specified | ~$1.7T |

Amazon’s investment thesis centres on AI infrastructure, cloud computing dominance through AWS, and advertising growth. Ackman added to the position when shares sold off following the company’s announcement of $200 billion in capital expenditure plans, viewing the market’s reaction as short-term pessimism that created a buying opportunity. The stock represents 11.76% of Pershing Square’s total portfolio and has delivered 31.54% returns over the past year. Analyst consensus remains overwhelmingly positive, with an average price target of $281.27 implying 17.7% upside.

Meta Platforms’ investment thesis emphasises the company’s strengthening digital advertising moat and strong cash flow generation. Like Amazon, Meta shares were acquired following investor concerns about capital spending plans tied to AI infrastructure investments. The position reflects Ackman’s view that Meta’s competitive advantages in social media and digital advertising justify a 22x earnings multiple, particularly given expected 20%+ annual EPS growth. Analyst consensus remains overwhelmingly positive, with an average price target of $855.68 implying 36.1% upside.

Pershing Square’s other top holdings include:

- Uber Technologies (UBER): Largest position, reflecting conviction in mobility and platform economics

- Brookfield Corporation (BN): Exposure to alternative assets and infrastructure

- Restaurant Brands International (QSR): Consumer brands positioning

- Howard Hughes Holdings (HHH): Real estate and development exposure

- Chipotle Mexican Grill (CMG): Consumer brands and restaurant sector

The Fannie Mae Bet: High-Risk Speculation on Privatisation

Ackman’s public endorsement of Fannie Mae as a potential “10-bagger” represents a fundamentally different risk profile than his core holdings. In late March 2026, Ackman posted on X (formerly Twitter) calling Fannie Mae and Freddie Mac “stupidly cheap” with the potential to become “10-baggers” if privatised. The market response was immediate: FNMA shares rallied 41% the following day, trading at approximately $8.25 per share.

The implied investment thesis centres on asymmetric upside contingent on government privatisation of the GSEs (Government-Sponsored Enterprises). This represents a bet on political and regulatory evolution rather than fundamental business improvement. If the U.S. government moves to privatise Fannie Mae and Freddie Mac, current shareholders could see substantial gains as the entities transition from government conservatorship to private ownership.

The FHFA conservatorship framework established in September 2008 placed Fannie Mae and Freddie Mac under government control to stabilize the housing finance system, creating the regulatory structure that governs any potential privatization pathway and the associated capital requirements.

Key risk factors analysts have identified include:

- Capital shortfall: Fannie Mae faces an estimated $193 billion capital deficit

- Binary outcome: Investment success is dependent on government policy changes

- Speculative nature: The thesis relies on political decisions rather than operational performance

- Housing policy dependence: Privatisation timing and structure remain uncertain

Financial media has cautioned individual investors against blindly replicating this position without understanding its fundamentally different risk profile compared to Ackman’s core holdings. The Fannie Mae endorsement exemplifies high-risk, high-reward speculation rather than the fundamental value investing approach that characterises positions in Meta, Amazon, and Uber.

Macroeconomic Outlook: H2 2026 Catalysts and Headwinds

Ackman expects favourable conditions for equity investors in the second half of 2026, though uncertainty around the Iran conflict and inflation persist. He believes downside risks are largely priced in after rate cut expectations deteriorated materially over approximately six weeks prior to mid-April 2026. This view suggests that markets have already absorbed pessimistic scenarios, creating a foundation for potential upside.

Ackman’s willingness to deploy capital during periods of uncertainty aligns with broader principles for investing during market volatility, where temporary pessimism can create opportunities in fundamentally sound businesses.

Key headwinds include the Iran conflict’s impact on oil prices, which feeds through to inflation and could pressure the Federal Reserve to maintain interest rates above market expectations. Persistently elevated inflation would compress equity multiples by increasing the discount rate applied to future earnings. If the FOMC holds rates higher for longer than currently anticipated, growth stocks trading at premium valuations could face downward pressure.

Rate cut expectations worsened over approximately six weeks leading up to mid-April 2026. Ackman’s assessment is that this pessimism is now reflected in current pricing, meaning markets have limited downside unless conditions deteriorate further. This framework supports his willingness to deploy fresh capital through the upcoming IPO.

Recent examples of market resilience during geopolitical shocks demonstrate how quality equities with strong fundamentals can recover quickly from temporary volatility, supporting Ackman’s view that downside risks are largely priced in.

Positive catalysts Ackman has identified include:

- Potential rate cuts as inflation moderates in the latter half of 2026

- First complete year under revised tax legislation benefiting corporate profits

- Increased M&A activity and business investment as regulatory clarity improves

- AI infrastructure deployment driving revenue growth for technology leaders

Ackman’s view is that high-quality stocks like Meta and Amazon possess sufficient resilience that investors can afford to hold them while awaiting improved market sentiment. The combination of durable competitive moats, 20%+ expected EPS growth, and strong analyst support provides downside protection even if macroeconomic conditions remain challenging in the near term.

The next major ASX story will hit our subscribers first

Pershing Square U.S. IPO: $10 Billion Signal of Conviction

The planned Pershing Square U.S. IPO targeting $5-10 billion in summer 2026 represents a significant signal of Ackman’s conviction that current market conditions offer attractive deployment opportunities. The fund will operate through a dual-listed structure comprising Pershing Square Inc. (PS) and Pershing Square USA (PSUS), with $2.8 billion in commitments already secured as of pre-April 2026 marketing efforts.

The fund economics feature a 2% management fee with no performance fee, structured as permanent capital targeting what Ackman describes as businesses with “extraordinary economic characteristics.” According to shareholder communications, Ackman intends to deploy IPO proceeds within weeks of raising them, indicating confidence in identifying immediate opportunities rather than holding cash for extended periods.

The timing signals a critical strategic judgment. By raising up to $10 billion in fresh capital during a period many investors view as characterised by elevated valuations, Ackman is effectively declaring that durable growth companies are available at attractive prices. This perspective aligns with his view that dominant firms with economic moats warrant premium multiples, and that current market conditions offer selective value despite headline index metrics.

Investor Implications: Applying Ackman’s Framework

Ackman’s framework centres on concentrated bets in companies with durable competitive moats, willingness to buy during temporary pessimism around capital expenditure announcements, and conviction that the second half of 2026 will reward patient investors in quality equities. His approach involves paying fair multiples for businesses with structural advantages rather than seeking low P/E ratios in commoditised sectors.

While Ackman’s concentrated portfolio focuses on U.S. mega-cap technology and consumer brands, investors should also consider portfolio diversification strategies that balance domestic concentration with international exposure.

A critical distinction exists between Ackman’s fundamental value investments (Meta, Amazon, and core holdings) and speculative policy bets (Fannie Mae). The former category reflects long-term conviction in business quality and competitive positioning, supported by analyst consensus and operational metrics. The latter represents asymmetric risk-reward dependent on government decisions, requiring a different risk tolerance and time horizon.

Investors tracking Ackman’s strategy should monitor the mid-May 2026 13F filing for updated position data reflecting activity through 31 March 2026. The summer IPO launch will provide additional signals about capital deployment priorities and specific opportunities Ackman is targeting with fresh capital. As always, investors should conduct their own due diligence and consult with financial professionals before making investment decisions based on hedge fund activity.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Frequently Asked Questions

What is Bill Ackman's current market outlook for 2026?

Ackman expects favourable conditions for equity investors in the second half of 2026, believing that downside risks are largely priced in after rate cut expectations deteriorated over roughly six weeks prior to mid-April 2026, with potential catalysts including rate cuts, tax legislation benefits, and increased M&A activity.

Why is Bill Ackman raising $10 billion through a new IPO if markets look expensive?

Ackman argues that index-level P/E ratios are distorted by a small number of highly valued mega-cap companies, meaning quality businesses with durable competitive moats are available at fair prices; he plans to deploy the IPO proceeds within weeks of raising them, signalling strong conviction in near-term opportunities.

What stocks does Bill Ackman hold in Pershing Square's portfolio?

As of the 31 March 2025 13F filing, Pershing Square's top holdings include Uber Technologies, Amazon, Meta Platforms, Brookfield Corporation, Restaurant Brands International, Howard Hughes Holdings, and Chipotle Mexican Grill, with total portfolio value of approximately $11.93 billion.

Is Bill Ackman's Fannie Mae investment a good idea for retail investors?

Financial media has cautioned individual investors that the Fannie Mae position is a speculative, policy-dependent bet with an estimated $193 billion capital deficit, fundamentally different from Ackman's core holdings in Meta and Amazon, which are supported by operational metrics and analyst consensus.

How does Bill Ackman justify paying 22x or 32x earnings for stocks like Meta and Amazon?

Ackman's framework holds that companies delivering sustained 20%+ annual EPS growth with durable competitive moats, such as network effects, brand strength, and technological leadership, rationally warrant premium multiples because their growth prospects justify the higher price relative to current earnings.