Investment Scam Losses Hit $838M Despite Record ASIC Takedowns

52 mins ago

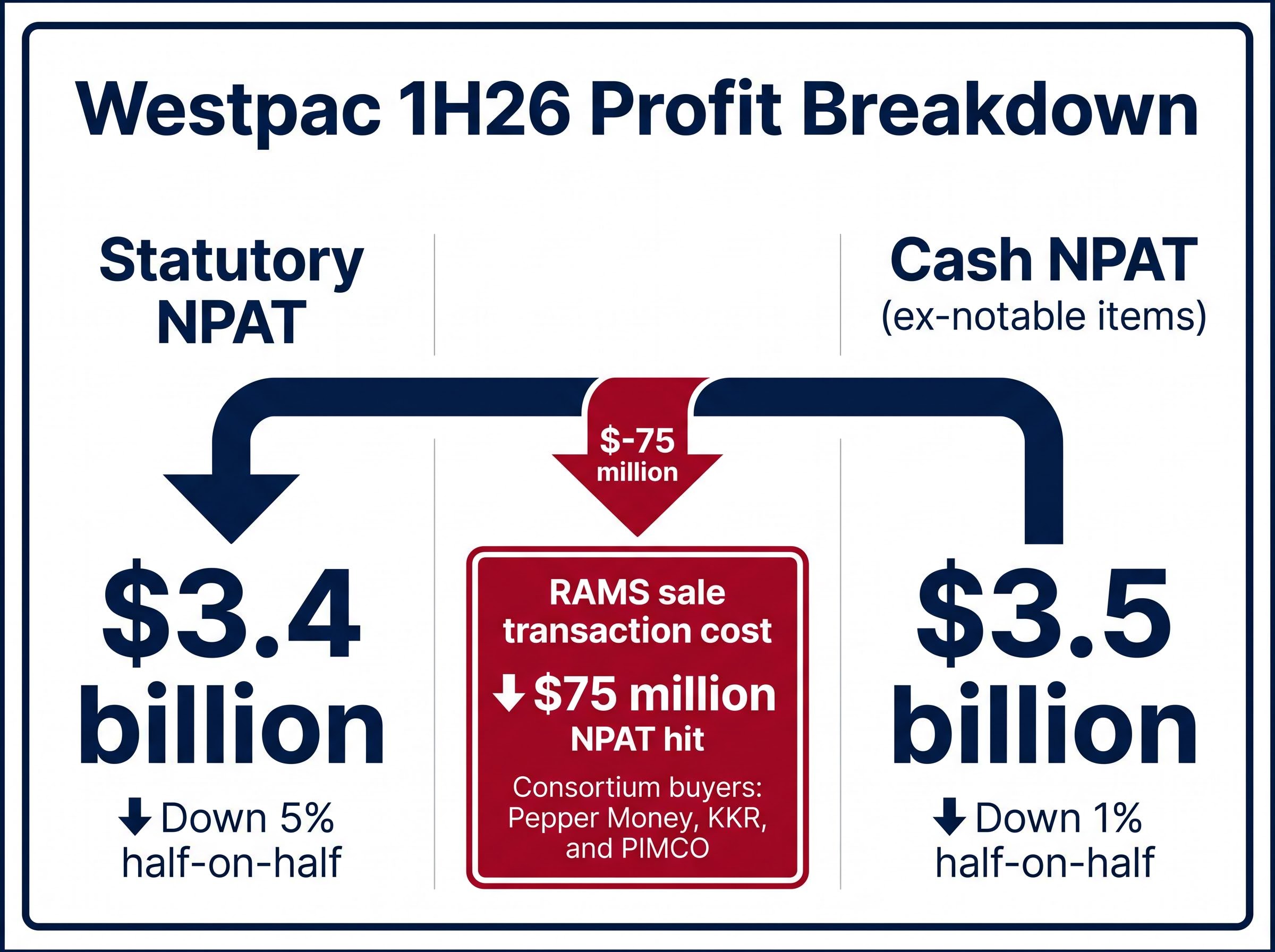

Westpac (ASX: WBC) posted a $3.4 billion statutory profit for the first half of fiscal 2026 this morning, even as margin pressure and a one-off RAMS transaction cost dragged the headline number 5% below the prior half. The result landed on 5 May 2026 against a backdrop of competitive mortgage markets, geopolitical uncertainty flagged by management, and close investor scrutiny of dividend sustainability across ASX bank stocks.

What follows unpacks what the numbers actually mean for WBC shareholders: whether the profit dip is structural or situational, what the maintained dividend signals about the board’s confidence, and whether the early share price lift reflects genuine investor conviction or simply relief that the result contained no nasty surprises.

Westpac shares traded at $38.82 in early session on 5 May 2026, up approximately 1% from the prior close of $38.50. The gain was measured, not euphoric, and the numbers underneath explain why.

The headline requires two readings. Statutory net profit after tax (NPAT) came in at $3.4 billion, down 5% on the second half of fiscal 2025. Strip out notable items, however, and cash earnings were $3.5 billion, down just 1% half-on-half and up 1% on the first half of fiscal 2025.

The gap between those two figures traces back to a single line item.

$75 million NPAT hit from RAMS portfolio sale transaction costs.

That $75 million drag is a transaction cost associated with the sale of Westpac’s RAMS home loan portfolio to a consortium of Pepper Money, KKR, and PIMCO. It is not a reflection of underlying business deterioration, and it will not recur once the sale completes in the second half.

The three headline figures at a glance:

The market’s early verdict reads as a qualified endorsement: a result that met expectations, with the profit decline largely explained by a known one-off cost.

ASX bank sector valuations heading into this result were already under scrutiny, with the financials sector up nearly 9% year to date in 2026 against a backdrop of unanimous sell ratings on CBA and a bearish tilt across three of the four major banks, a disconnect between price momentum and analyst consensus that sharpened investor focus on every line of the May reporting season.

The lending figures inside this result are the kind that get lost behind a profit headline, and they probably should not be. Westpac’s institutional lending grew 23% year-on-year to $131 billion. Business lending rose 16% year-on-year to $120 billion. Australian mortgage growth ran at 1.2 times the system rate, excluding RAMS.

RBA financial aggregates data for March 2026 shows system housing credit growth running at a pace that makes Westpac’s 1.2 times multiple a meaningful outperformance, particularly given that mortgage lending across the major banks has faced consistent pricing pressure from non-bank competitors and smaller lenders.

Customer deposits climbed 7% year-on-year to $379 billion, with business deposits up 5% to $156 billion and institutional deposits up 12% to $137 billion.

| Segment | Metric | Result | Direction |

|---|---|---|---|

| Institutional lending | Year-on-year growth | $131 billion | Up 23% |

| Business lending | Year-on-year growth | $120 billion | Up 16% |

| Customer deposits | Year-on-year growth | $379 billion | Up 7% |

| Australian mortgages | System growth multiple | 1.2x system | Above system (excl. RAMS) |

Those growth rates, particularly in institutional and business lending, indicate Westpac is gaining commercial market share at a pace that materially exceeds what pre-release previews had anticipated as mid-single-digit lending growth.

The lending story runs into a harder truth at the revenue line. Total revenue fell 2% to $11.3 billion, with net interest income down 1% and non-interest income down 3%. Net interest margin (NIM) contracted by 6 basis points over the half.

Three factors contributed to the NIM compression: competitive lending conditions that suppressed pricing power, interest rate timing differences affecting the repricing of assets and liabilities, and subdued Treasury and Markets results. Pre-release previews had anticipated stable core NIM excluding rate timing effects, making the 6 basis point decline a modest negative if confirmed by the full results disclosure.

The lending volumes are genuinely strong. The question for investors is whether that volume growth can eventually offset the margin compression, or whether Westpac is running harder to stay in place.

The number that matters most to income-focused shareholders landed unchanged.

Westpac declared an interim dividend of 77 cents per share, fully franked.

The dividend was flat versus the prior half and up approximately 1.3% on the first-half 2025 equivalent. For Australian tax residents, full franking means the dividend carries a tax credit reflecting the 30% corporate tax already paid on the underlying profit. In practical terms, franking credits reduce the personal tax payable on the dividend income, making the effective yield higher than the headline figure for most retail holders.

The payout ratio of 77.1% is the more telling figure. A board that believed the earnings dip was structural would have trimmed the payout. Instead, the ratio rose slightly, reflecting a deliberate choice to maintain income distribution despite the lower statutory profit.

The maintained dividend reads as a board-level signal that the earnings pressure is situational, not permanent.

Westpac’s CET1 capital position of 12.4%, sitting 115 basis points above the bank’s own internal target, is one of the less-discussed metrics in today’s result but arguably the clearest indicator of the board’s capacity to sustain or grow the dividend beyond the current half.

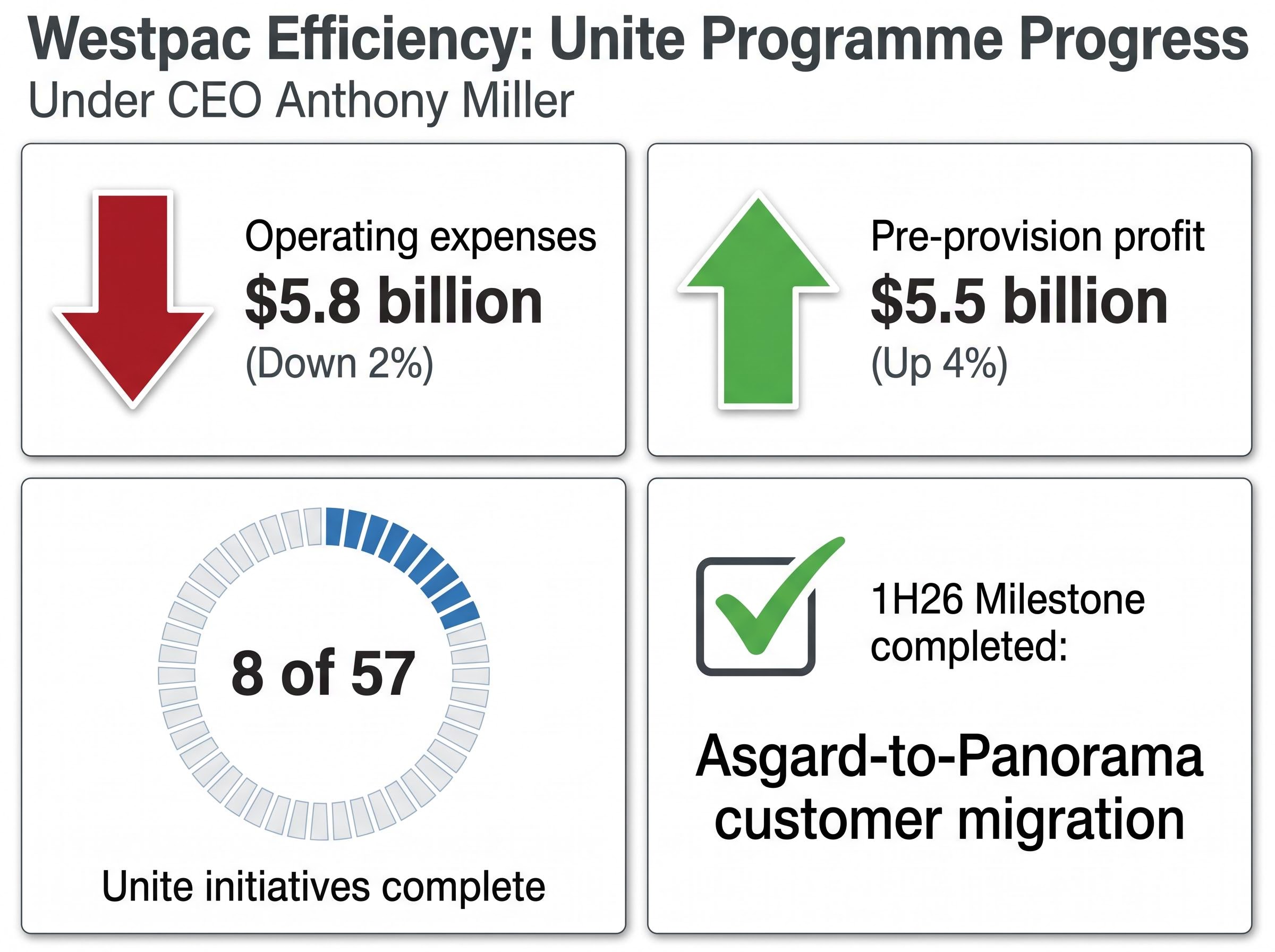

Operating expenses fell 2% to $5.8 billion in the half. That reduction is the single biggest reason the profit result was not materially worse, and it flowed directly into a 4% rise in pre-provision profit to $5.5 billion.

The cost discipline sits within the broader Unite strategy programme, Westpac’s multi-year transformation effort under CEO Anthony Miller. Progress this half included:

Miller flagged artificial intelligence adoption and productivity reform as the two stated priorities for the second half, giving investors a forward-looking lens on where the next efficiency gains may originate.

In a compressed-margin environment, expenses are the lever management controls most directly. The 2% reduction demonstrates that Westpac is pulling it. Whether the Unite programme can sustain that pace across the remaining 49 initiatives will determine how much of the efficiency story is structural rather than one-off.

CEO Anthony Miller specifically cited the Middle East conflict and energy supply chain disruption as the two named geopolitical risk factors affecting customer conditions. The bank established a new provisions overlay for energy-intensive sector exposures during the half, with credit provisions sitting at approximately 10 basis points of gross loans and capital-to-risk-weighted-assets (CAP/RWA) at approximately 129 basis points.

Anthony Miller characterised the customer environment as one where borrowers are showing resilience amid ongoing uncertainty.

The provisioning increase is a forward hedge, not a signal that loan quality has deteriorated. Pre-release previews had flagged improving asset quality trends heading into the result, and the overlay reflects management pricing in risk that has not yet materialised in the loan book.

Three risk factors investors should monitor from here:

The cautious provisioning stance is consistent with a bank managing through elevated uncertainty rather than absorbing realised losses.

For investors unsettled by Miller’s specific references to Middle East conflict and energy supply chain disruption, our full explainer on geopolitical risk and equity markets examines why equity markets have historically absorbed geopolitical shocks more quickly than intuition suggests, using the April 2026 Caspian Pipeline attack and S&P 500 response as a live case study of how markets price probability-adjusted earnings impacts rather than headline severity.

Today’s result pulls in two directions. On one side: 23% institutional lending growth, a maintained 77-cent fully franked dividend, and a 2% reduction in operating expenses. On the other: revenue compression, a 6 basis point NIM contraction, and elevated provisions for geopolitical risk.

The early 1% share price gain to $38.82 reflects the market reading this as a stable-to-mildly-positive result rather than either a breakout or a warning. Pre-provision profit, up 4% to $5.5 billion, is arguably the metric that best captures underlying operating leverage once the RAMS noise is removed.

Three forward-looking items for investors to track:

Comparable results from CBA, NAB, and ANZ were not available at time of publication. Peer data, once released, will provide the broader sector context needed to assess whether Westpac’s margin and lending trends are bank-specific or industry-wide.

Pre-result broker warnings had set a cautious bar for today’s numbers, with Morgans issuing simultaneous sell ratings across all four major banks in late April and flagging rising provisions and earnings downgrades as the twin risks heading into the May reporting season.

Westpac’s first-half result is best read as a bank managing the transition from rate-driven margin expansion to volume-driven earnings growth, with cost discipline bridging the gap. The early share price gain reflects relief that the dividend was protected and lending growth remained strong, rather than conviction that margin pressure has peaked.

Investors monitoring WBC from here should watch for the RAMS sale completion in the second half, any updated broker commentary on price target revisions (none was available at time of publication), and whether the Unite programme’s next phase of initiatives can sustain the 2% expense reduction trajectory.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Westpac shares traded at $38.82 in early session on 5 May 2026, up approximately 1% from the prior close of $38.50, following the release of its first-half fiscal 2026 results.

The 5% decline in statutory net profit to $3.4 billion was largely driven by a one-off $75 million NPAT hit from transaction costs associated with the sale of the RAMS home loan portfolio; excluding this notable item, cash earnings fell only 1% half-on-half.

Westpac declared an interim dividend of 77 cents per share, fully franked, representing a payout ratio of 77.1% and a roughly 1.3% increase on the first-half 2025 equivalent.

Westpac's dividend is fully franked, meaning it carries tax credits reflecting the 30% corporate tax already paid on the underlying profit, which reduces the personal tax payable on dividend income for Australian resident shareholders and makes the effective yield higher than the headline figure.

Investors should monitor the completion of the RAMS portfolio sale to the Pepper Money, KKR, and PIMCO consortium, which will remove the notable item drag from future earnings, as well as progress on the remaining 49 Unite strategy initiatives and whether geopolitical risk provisions translate into actual loan losses.