United Airlines CEO Scott Kirby proposed combining two of the largest U.S. carriers into a single entity, raised the idea directly with President Donald Trump, and watched the plan collapse in public view after American Airlines CEO Robert Isom called it anti-competitive and harmful to consumers. The proposed United-American combination would have reshaped U.S. aviation, but the deal never reached a negotiating table. Isom rejected it publicly before any formal process could begin, and Kirby is now characterising the transaction as low probability following a Reuters interview on the sidelines of the International Air Transport Association (IATA) annual meeting in Rio de Janeiro on 7 June 2026. What follows is a complete account of what the proposed deal involved, why it collapsed, what role the Trump administration played, and what United Airlines plans to do instead.

How the United-American merger proposal came together and fell apart

Kirby’s vision was a full corporate combination between the second and third largest U.S. carriers by capacity. He approached American Airlines about the concept and, separately, briefed President Trump on the idea in February 2026. The proposal never progressed to a formal offer.

The timeline tells the story of how quickly and publicly the plan unravelled:

- February 2026: Kirby raises the merger concept with President Trump.

- April 2026: Kirby publicly discloses that American Airlines refused to engage.

- 7 June 2026: Kirby characterises the deal as low probability in a Reuters interview at the IATA annual meeting in Rio de Janeiro, as reported by Rajesh Kumar Singh and Joe Brock.

American Airlines did not respond with a private counteroffer or a request for terms. Isom declared the deal anti-competitive and harmful to consumers in public, closing off any negotiated path forward before one could open.

Scott Kirby, CEO, United Airlines: A transaction of this scale and unconventional nature could not realistically proceed without the backing of American Airlines’ own management.

Kirby’s framing at the IATA meeting made the structural constraint explicit: a willing counterpart is required. Without one, the proposal was not a failed negotiation. It was a proposal that never became one.

When big ASX news breaks, our subscribers know first

Why American Airlines said no, and what anti-competitive means in this context

Isom’s objection was not a reflexive defensive posture. A full corporate combination between United (second largest U.S. carrier by capacity) and American (third largest) would have concentrated a significant share of domestic and international routes under a single operator. Route overlap at major hubs, reduced gate competition at congested airports, and diminished consumer choice on high-traffic corridors would have formed the core of any antitrust review.

In U.S. airline merger law, “anti-competitive” refers to a transaction that would substantially lessen competition or tend to create a monopoly, the standard the Department of Justice (DOJ) applies when evaluating proposed combinations. Isom’s public use of that language signalled that American’s management viewed the deal as one the DOJ would likely challenge, and that American had no interest in spending years defending a transaction it believed would fail regulatory review.

The antitrust precedent that shapes every U.S. airline merger conversation

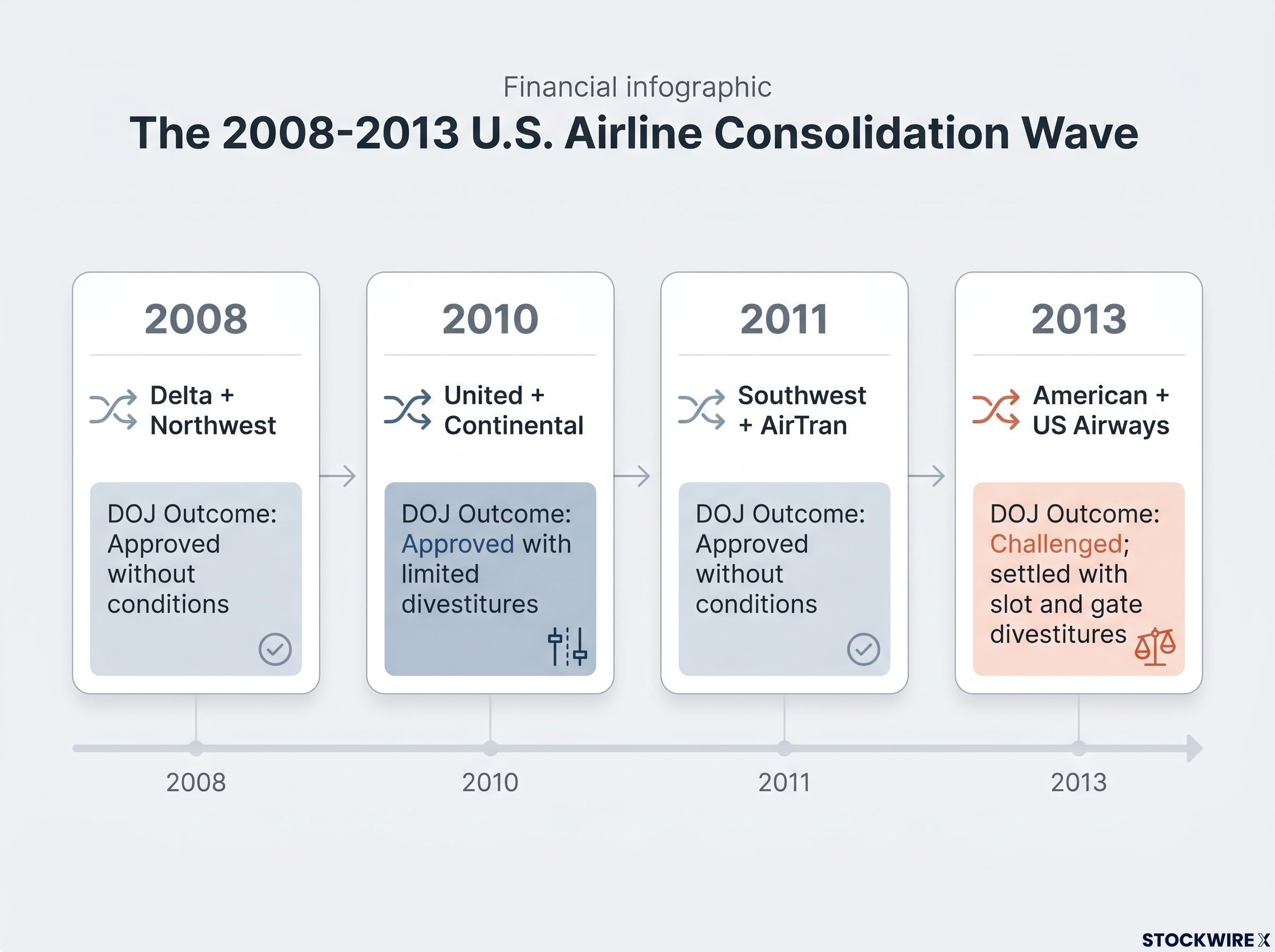

The reference point is the 2013 DOJ challenge to the American-US Airways merger. The DOJ sued to block that transaction, arguing it would reduce competition in hundreds of city-pair markets. The case settled with conditions: American and US Airways agreed to divest slots and gates at key airports, including Washington Reagan National and New York LaGuardia, before the combination was permitted to close.

The DOJ settlement requiring slot and gate divestitures in the American-US Airways case compelled the carriers to relinquish facilities at Reagan National, LaGuardia, and five other key airports before the combination could close, establishing the divestiture template that any future big-carrier merger would face.

That case set the template. Any future big-carrier combination now faces route overlap analysis, hub dominance scrutiny, and consumer-price impact modelling. A merger between the second and third largest carriers would trigger an even more intensive review than the 2013 case, because the resulting entity’s market share would exceed what the DOJ accepted then.

The consolidation wave from 2008 to 2013 produced the current big-four structure: American, Delta, United, and Southwest. Every proposed combination among these four is measured against the conditions that wave established.

| Year | Acquirer | Target | DOJ Outcome |

|---|---|---|---|

| 2008 | Delta | Northwest | Approved without conditions |

| 2010 | United | Continental | Approved with limited divestitures |

| 2011 | Southwest | AirTran | Approved without conditions |

| 2013 | American | US Airways | Challenged; settled with slot and gate divestitures |

Isom’s public framing served a dual purpose. It communicated American’s position to regulators and investors simultaneously, and it made the DOJ review process functionally unworkable: a merger target publicly calling its own acquisition anti-competitive hands the DOJ its opposing argument on a platter.

What Scott Kirby told Trump, and what a government equity stake would have meant

Kirby raised the merger concept with President Trump in February 2026. Based on available sourcing, no formal government policy position, Department of Transportation guidance, or DOJ statement followed from that meeting. The briefing appears to have been informational rather than a request for regulatory endorsement.

The more consequential detail is what Kirby denied. He explicitly stated that United had not held discussions with the Trump administration about granting the U.S. government a special equity stake in a combined United-American entity.

Scott Kirby, CEO, United Airlines: United denied that it had discussed any arrangement involving a government equity stake with the Trump administration.

The denial drew attention precisely because government equity in a private carrier, while unusual, is not without precedent in recent U.S. aviation history. The CARES Act relief programmes during the COVID-19 pandemic gave the U.S. government warrants in major airlines as a condition of financial assistance, creating a temporary government ownership interest in commercial carriers.

Treasury’s CARES Act warrant programme required passenger carriers receiving substantial payroll support awards to provide the U.S. government with financial instruments, including warrants at defined exercise prices, creating a de facto temporary ownership interest that made government equity in commercial aviation a lived reality rather than a theoretical concern.

A permanent government equity stake in a combined United-American entity would raise three distinct structural concerns:

- Governance: Government board representation or voting rights could create conflicts between shareholder interests and public policy objectives.

- Regulatory independence: A government-owned carrier being regulated by government agencies creates an inherent conflict of interest.

- Shareholder dilution: Issuing equity to the government would dilute existing shareholders’ ownership and potentially their dividend entitlements.

Kirby’s denial clarified that the proposed deal, as he envisioned it, was a conventional corporate combination between two private entities, not an unconventional public-private structure.

United’s plan B: gates, slots, and distressed competitor assets

With the mega-merger off the table, Kirby’s attention has turned to a different kind of consolidation. He described United’s openness to opportunistic acquisition of airport gates and slots if financially weaker competitors face distress from elevated fuel costs.

The distinction matters. A full corporate merger between major carriers requires management alignment at both companies, years of regulatory review, and labour integration across multiple union contracts. Asset acquisition is targeted, faces lighter regulatory scrutiny, and can be executed in months rather than years.

- Full corporate merger: High regulatory scrutiny, management alignment required, multi-year timeline, labour integration across unions.

- Asset acquisition (gates, slots): Targeted scope, lower regulatory burden, faster execution, no workforce integration required.

Kirby framed these potential purchases as opportunistic, contingent on whether elevated fuel costs push weaker carriers toward financial distress and force asset sales.

The fuel cost environment underpinning Kirby’s opportunistic asset thesis is not hypothetical: airline sector distress materialised in concrete form when Spirit Airlines permanently closed on 2 May 2026 after a 57% rise in jet fuel costs destroyed its recovery plan, eliminating 17,000 jobs and removing 2% of U.S. domestic capacity from the market.

JetBlue and the distressed-asset opportunity Kirby is watching

On JetBlue Airways specifically, Kirby assessed that a Chapter 11 bankruptcy filing was unlikely, pointing to JetBlue’s available cash and unencumbered asset base as buffers against that outcome. The assessment was measured rather than dismissive: Kirby framed the broader sector as one where distress-driven asset availability remains a real possibility even if JetBlue itself avoids the worst case.

Gates and slots at congested airports are among the most strategically valuable assets in U.S. aviation. Acquiring them from a distressed seller, at distressed prices, would allow United to strengthen its network at key hubs without the regulatory and management-alignment obstacles that killed the American deal.

What this means for the future of U.S. airline consolidation

The big-four structure, American, Delta, United, and Southwest, has been in place since the 2008-2013 consolidation wave ended. Kirby’s proposal represents the first publicly disclosed attempt at a top-tier combination since that wave closed. Its collapse tells investors something specific: the barrier to mega-merger consolidation in 2026 is management alignment, not regulation.

No DOJ or Department of Transportation public statement on the proposed deal has been documented. The regulatory question was never tested because the deal never advanced far enough to require a filing.

Scott Kirby, CEO, United Airlines: United has not permanently abandoned the concept of large-scale consolidation but requires a willing counterpart as a prerequisite for any future attempt.

Kirby’s condition implies three things must align for any future attempt to become viable:

- Management willingness at the target carrier to engage in a negotiated process.

- A supportive, or at least neutral, regulatory environment at the DOJ and DOT.

- Labour union and shareholder backing at both companies.

None of these conditions exist today. Whether they emerge in the future depends on financial pressures, leadership changes, and regulatory posture shifts that remain unpredictable.

The bottom line for airline investors and industry watchers

The United-American merger is low probability, not impossible. The constraint is management alignment at American Airlines, not a regulatory prohibition. Kirby has positioned United on a dual track: closed on the mega-merger for the foreseeable future, open on targeted asset acquisition from distressed competitors.

American’s aggressive public opposition is the defining feature of this story. Isom did not decline privately and leave the door ajar. He framed the deal as anti-competitive in public, a signal that American’s management believes its standalone strategy is competitive and that no premium would justify the combination.

The divergence is clear. United’s management believes consolidation, at some level, remains the correct long-term direction. American’s management believes independence is the stronger position. That disagreement will shape both companies’ capital allocation decisions for the foreseeable future.

Scott Kirby, CEO, United Airlines: A willing counterpart remains the condition that defines whether large-scale U.S. airline consolidation moves from concept to reality.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding potential future consolidation, asset acquisitions, or regulatory outcomes are speculative and subject to change based on market developments and company decisions.