Iran War Energy Stocks: Majors vs Leveraged Plays at $94 Oil

Key Takeaways

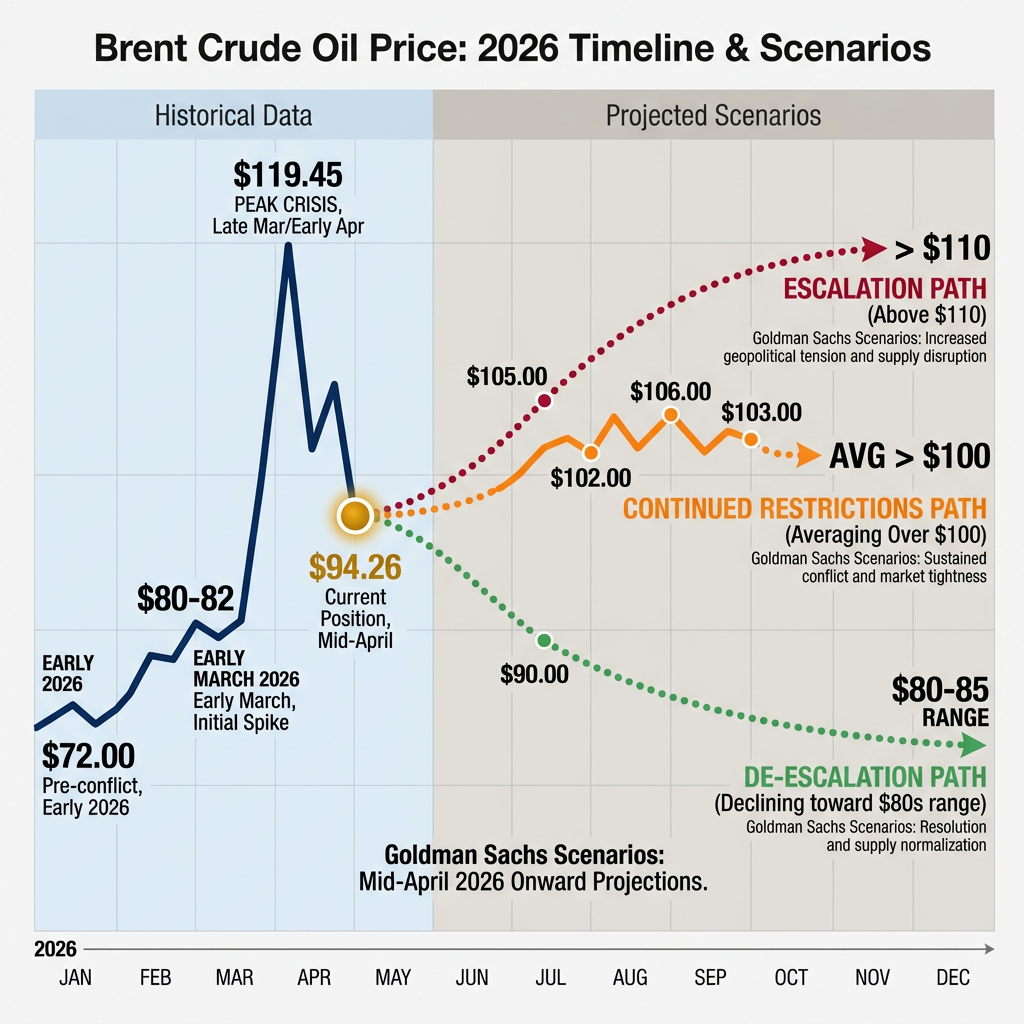

- Brent crude has surged from roughly $72 per barrel before the conflict to a peak of $119.45, settling at $94.26 in mid-April 2026 as ceasefire negotiations in Pakistan remain unresolved.

- Integrated majors ExxonMobil and Chevron are the top analyst picks, offering potential 15-20% free cash flow yields and 8-10% dividend growth if elevated prices persist through 2026.

- Goldman Sachs outlines a binary scenario where de-escalation sends Brent back to the $80s while further escalation could push prices above $110, making disciplined position sizing critical.

- Energy ETFs including XLE and IXC have lagged oil price gains, suggesting markets view the disruption as temporary and creating potential mispricing for investors with a differentiated view on conflict duration.

- Clean energy stocks suffered collateral damage as inflation fears from higher oil prices reduced rate cut expectations, disproportionately pressuring capital-intensive renewable companies.

The Strait of Hormuz remains largely closed as of mid-April 2026, with the Islamic Revolutionary Guard Corps maintaining restrictions on maritime traffic and considering implementing fees for ships seeking passage. Fragile ceasefire negotiations between the United States and Iran are underway in Pakistan, but these talks have produced no definitive resolution. The International Energy Agency has characterised this as the “greatest global energy security challenge in history,” a designation that reflects both the unprecedented nature of the disruption and the absence of immediate alternatives for rerouting the roughly 21% of global petroleum liquids consumption that typically passes through this waterway.

The situation remains highly fluid. Previous disruptions to Hormuz traffic have been brief and limited in scope. The current extended closure represents uncharted territory for global energy markets, creating fundamental uncertainty about timeline and resolution that makes position sizing and quality selection critical for investors navigating the energy sector.

The current extended closure represents uncharted territory for global energy markets, creating fundamental uncertainty about timeline and resolution that distinguishes this from the largest supply disruption in oil market history through its combination of scale, duration, and geopolitical complexity affecting investor positioning.

The Strait of Hormuz Crisis: Where Oil Markets Stand in Mid-April 2026

The IRGC’s control over the strait is not absolute, but it is effective. Restrictions have created severe bottlenecks for tanker traffic, and the consideration of passage fees adds another layer of complexity to an already uncertain operating environment. Ceasefire talks in Pakistan have shown little concrete progress, with both sides maintaining public positions that leave wide gaps between their stated objectives.

What makes this crisis distinct from previous Middle Eastern oil disruptions is its duration and the absence of credible near-term resolution mechanisms. Markets have absorbed supply shocks before, but those shocks typically came with visible pathways to normalisation. The current situation offers no such clarity.

The binary nature of potential outcomes is stark. The situation could de-escalate through successful negotiations, or it could escalate further if talks collapse. Investors face fundamental uncertainty about both timeline and resolution, making the quality of portfolio positions more important than the quantity of energy exposure.

When big ASX news breaks, our subscribers know first

Understanding the Oil Price Surge: From $72 to $119 and Back

Oil prices have followed a dramatic trajectory since the conflict began. Brent crude started 2026 trading around $72 per barrel, reflecting market expectations of adequate global supply and relatively stable demand. By early March, as tensions escalated, prices had jumped to $80-82 per barrel. The peak came at $119.45, driven by maximum disruption fears. As of mid-April 2026, Brent has settled around $94.26 per barrel.

GMO’s Lucas White noted that markets had positioned for a 2025-2026 oil glut. The Iran conflict upended those forecasts entirely. This shift from expected oversupply to acute supply constraints forced wholesale reassessment of energy sector fundamentals, catching many institutional investors off-guard and requiring rapid portfolio repositioning.

| Timeline | Brent Crude Price | Market Catalyst |

|---|---|---|

| Pre-conflict (early 2026) | ~$72 | Baseline expectations of adequate supply |

| Early March 2026 | $80-$82 | Initial escalation and Hormuz restrictions |

| Peak Crisis | $119.45 | Maximum disruption fears |

| Mid-April 2026 | $94.26 | Ceasefire uncertainty and partial retreat |

Goldman Sachs presents a binary scenario analysis for the path forward. In a de-escalation scenario, prices could retreat to the $80s per barrel. In an escalation scenario, prices could surge above $110. If restrictions continue without resolution, Goldman expects Brent to average over $100 per barrel through 2026. Markets are treating current price movements as potentially temporary, creating what Goldman characterises as tactical opportunities in quality energy names positioned to benefit from sustained elevated prices.

The retreat from peak levels does not signal resolution. It reflects market uncertainty about conflict duration and the impact of fragile ceasefire negotiations, balanced against the reality that prices remain substantially elevated compared to pre-war levels due to ongoing Hormuz restrictions.

Integrated Oil Majors: Why ExxonMobil and Chevron Lead the Pack

Analysts strongly recommend exposure to financially resilient integrated energy giants for U.S. investors navigating the current environment. These companies offer diversified business models that generate profits across different market cycles, balancing upside from supply disruptions with downside protection if prices normalise. Goldman Sachs emphasises tactical opportunities in quality energy names amid $100+ Brent scenarios, focusing on firms that can maintain profitability regardless of how the geopolitical situation resolves.

ExxonMobil (XOM) and Chevron (CVX) have emerged as premier investment opportunities during the crisis. Both companies raised dividends and beat earnings expectations amid market volatility. ExxonMobil reached a record high on 30 March 2026, notably the same date Mohamed El-Erian had made risk-off recommendations. Despite disclosing roughly a 6% hit to Q1 2026 global production from the Strait of Hormuz blockade, XOM demonstrated resilience that validated analyst preference for quality over leverage.

The investment case for integrated majors rests on several foundations:

- Potential 15-20% free cash flow yields if elevated prices persist through the remainder of 2026

- 8-10% dividend growth trajectories supported by strong cash generation across upstream and downstream operations

- Active share buyback programmes returning capital to shareholders while maintaining balance sheet strength

- Operational flexibility to adapt production and refining operations quickly to changing market conditions

- Cycle resilience that maintains profitability across various price scenarios, not just peak disruption environments

Analysts recommend selecting companies with strong balance sheets and diversified operations rather than chasing pure upside leverage to oil prices. ConocoPhillips is mentioned in the broader context of quality energy plays, though the focus remains on integrated models that can weather both prolonged high prices and potential rapid normalisation. This approach prioritises risk-adjusted positioning over maximum sensitivity to oil price movements.

High-Yield Leveraged Plays: The Bullish Case for Risk-Tolerant Investors

GMO’s Lucas White presents a contrarian bullish thesis for investors willing to accept higher volatility. White sees the current geopolitical risk premium as underpriced in leveraged oil producers, arguing for a structural shift toward permanently higher oil prices that makes current valuations in selected names particularly attractive. His analysis focuses on companies that offer substantial yield even at conservative oil price assumptions, creating asymmetric upside if elevated prices persist.

White highlights Petrobras and Kosmos Energy as opportunities offering 20%+ yields even at mid-$70s oil prices. With Brent currently at $94, the implied returns are substantially higher. These names are positioned for investors who believe elevated prices will persist and want maximum leverage to that thesis, accepting the volatility that comes with less diversified business models.

The important caveat: this approach carries significantly higher risk than integrated majors. If de-escalation occurs and oil retreats to the $80s or below, leveraged producers face disproportionate downside compared to diversified giants. Position sizing should reflect individual risk tolerance. This represents tactical opportunity rather than core portfolio allocation for most investors.

Energy ETFs and Market Psychology: Reading Between the Lines

The State Street Energy Select Sector SPDR ETF (XLE) has risen modestly overall since the conflict began, but recent sessions have seen dips even as oil prices remained elevated. The iShares Global Energy ETF (IXC) fell 80 basis points on a notable Tuesday trading session. This divergence between oil prices and energy stock performance tells an important story about market expectations and positioning.

The divergence between elevated oil prices and tentative energy equity performance reflects unresolved debate about market resilience versus denial, with institutional positioning suggesting scepticism about sustainability that creates potential mispricing for investors with differentiated views on conflict duration.

Markets are treating current supply disruptions as potentially short-term. Investors appear sceptical about the sustainability of elevated energy prices, reflected in the reluctance of energy equities to fully track oil’s movements. Broader bearishness on global economic activity adds another layer: higher oil prices hurt demand, partially offsetting the positive impact of higher prices on energy stock valuations. The combination creates what some analysts view as potential mispricing.

The oil price surge caught many institutions off-guard. Many had positioned portfolios for stable, relatively low oil prices throughout 2026 based on expectations of adequate global supply. The rapid escalation forced repositioning, but the tentative nature of energy stock gains suggests this repositioning remains incomplete or hedged against reversal.

If you believe restrictions will persist longer than markets expect, this scepticism creates potential opportunity in quality names trading below where they would if investors fully priced in sustained $100+ oil. Conversely, if you expect rapid de-escalation, current energy stock prices may already reflect adequate upside. Understanding this divergence between oil price action and equity performance helps calibrate position sizing and timing decisions.

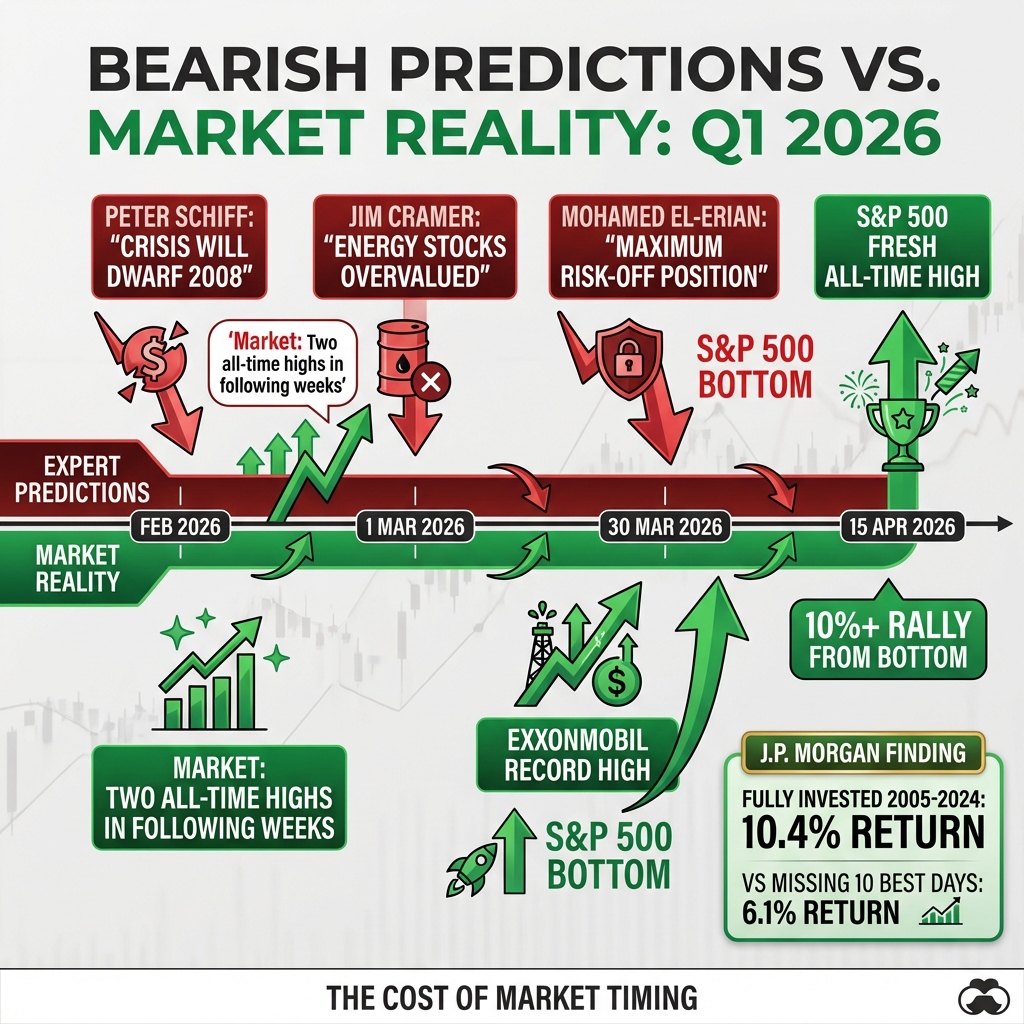

What Happened to the Bearish Predictions: Lessons from Q1 2026

Mohamed El-Erian publicly stated on 30 March 2026 he had shifted to a maximum risk-off position. The S&P 500 bottomed that exact date and rallied over 10% to a fresh all-time high by 15 April. Peter Schiff predicted in February a crisis dwarfing 2008. Markets hit two separate all-time highs in the following weeks. Jim Cramer called energy stocks overvalued on 1 March 2026. ExxonMobil reached a record high on 30 March.

None of these commentators have issued retractions or updates despite dramatic contradictions to their forecasts. Market focus has shifted away from these earlier bearish narratives toward analysing volatility opportunities and positioning for binary geopolitical outcomes. The silence is notable given how publicly these calls were made and how definitively markets moved in the opposite direction.

J.P. Morgan analysis of S&P 500 performance from 2005-2024 shows remaining fully invested yielded 10.4% annualised return. Missing just the 10 strongest trading days reduced returns to 6.1%. The best and worst days tend to cluster during periods of elevated volatility, exactly the environment created by the Iran crisis. Exiting on bearish predictions carries measurable financial penalty, particularly when those predictions coincide with market bottoms rather than tops.

For readers wanting to understand broader defensive strategies beyond energy sector allocation, our full explainer on portfolio positioning during geopolitical volatility covers cross-asset hedging approaches, volatility clustering patterns, and the timing considerations that determine whether energy exposure serves as portfolio insurance or concentrated risk.

The next major ASX story will hit our subscribers first

Clean Energy Spillover: Collateral Damage from the Crisis

Profit-taking hit renewable energy stocks following the outbreak of conflict. Inflation fears triggered by higher oil prices reduced expectations for central bank rate cuts, and higher interest rate expectations disproportionately impact clean energy companies due to their capital-intensive business models requiring significant financing. The spillover effects demonstrate how geopolitical oil shocks ripple through sectors that ostensibly benefit from long-term energy transition themes.

Smaller-cap clean energy names experienced sharper declines due to higher beta characteristics in down markets. This creates potential rebound opportunities if the crisis de-escalates and rate cut expectations reset, but timing depends heavily on geopolitical resolution. For investors with longer time horizons, current weakness in quality clean energy names may present entry points, though the path to normalisation remains unclear while Hormuz restrictions persist and inflation concerns limit central bank flexibility.

Conclusion

The Strait of Hormuz crisis has fundamentally reshaped energy market dynamics and investment positioning. Oil prices remain 30%+ above pre-war levels despite retreating from peak disruption fears. Integrated majors like ExxonMobil and Chevron offer quality exposure with downside protection, while leveraged producers present higher-risk opportunities for conviction plays on sustained elevated prices. Energy ETF performance suggests markets remain sceptical about price sustainability, creating potential mispricing for investors with differentiated views on conflict duration.

The binary nature of potential outcomes requires disciplined position sizing and quality selection. De-escalation could send prices back to the $80s. Escalation could push them above $110. Continued restrictions without resolution support Goldman Sachs’ projection of Brent averaging over $100 through 2026. The lessons from failed bearish predictions earlier in 2026 reinforce the cost of market timing and the value of staying invested through volatility.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

These statements are speculative and subject to change based on market developments and company performance.

Frequently Asked Questions

What are the best energy stocks to buy during the Iran war and Hormuz crisis?

Analysts favour integrated majors like ExxonMobil (XOM) and Chevron (CVX) for their diversified business models, dividend growth, and cycle resilience, while GMO highlights leveraged plays like Petrobras and Kosmos Energy for risk-tolerant investors seeking maximum upside if elevated prices persist.

How high could oil prices go if the Strait of Hormuz stays closed?

Goldman Sachs projects Brent crude could average over $100 per barrel through 2026 if restrictions continue without resolution, with an escalation scenario potentially pushing prices above $110 per barrel.

What is the Strait of Hormuz and why does it matter for oil prices?

The Strait of Hormuz is a critical maritime chokepoint through which approximately 21% of global petroleum liquids consumption passes, meaning any prolonged closure creates severe supply constraints that drive oil prices sharply higher worldwide.

Why are energy stocks not rising as fast as oil prices during the Iran conflict?

Markets appear sceptical about the sustainability of elevated oil prices, treating the supply disruption as potentially short-term, while broader concerns about higher inflation limiting central bank rate cuts also weigh on energy equity valuations.

What lessons can investors take from failed bearish predictions during the 2026 Iran crisis?

High-profile bearish calls from commentators including Mohamed El-Erian and Peter Schiff coincided with market bottoms rather than tops, reinforcing J.P. Morgan data showing that missing just the 10 strongest trading days between 2005 and 2024 reduced annualised returns from 10.4% to 6.1%.