Nikkei Hits Record as BOJ Prepares a 30-Year High Rate Hike

2 hrs ago

Total equity value at Lululemon Athletica dropped over the past five years, resulting in an estimated $17 billion to $20 billion loss in market capitalisation according to founder Chip Wilson. This staggering wealth evaporation sits at the centre of a complex corporate governance dispute. The immediate crisis environment in April 2026 follows former chief executive Calvin McDonald’s departure in January 2026.

Investors now face a tense holding period before a new leader arrives in September 2026, with a looming shareholder showdown threatening to upend the current boardroom structure. The underlying Lululemon controversy extends far beyond a standard leadership transition. The dispute exposes deep fractures between management’s operational trajectory and the original elite positioning of the activewear brand.

What follows is an analytical breakdown of the strategic missteps, structural governance disputes, and external market headwinds driving this internal conflict.

The scale of the financial deterioration provides the necessary context for evaluating the current leadership crisis. Historical highs have given way to severe valuation compression, grounding the founder’s aggressive interventions in hard market data. The stock closed at $142.39 on 28 April 2026, representing a stark 44% year-on-year decrease.

This decline dragged the company’s total market capitalisation down to $16.49 billion. The fundamental catalyst for this revaluation lies in a severe geographic revenue divergence rather than a temporary cyclical dip. The core North American market, historically the brand’s profit engine, reported a 4% revenue contraction in the fourth quarter of fiscal 2025.

The company’s official fiscal 2025 financial results confirm this troubling regional disparity, demonstrating that robust international expansion is currently unable to fully offset the deteriorating pricing power in domestic retail channels.

Capital rotated away from the stock as investors digested this regional weakness. Strong international growth partially offset the domestic bleeding, with Chinese market revenue increasing by 24% over the same period. However, this overseas expansion could not mask the fundamental weakness in the brand’s primary geography.

Readers must weigh the exact magnitude of this financial bleeding to determine if the proposed structural interventions are justified.

| Metric | Recent Performance | Founder’s Assessment |

|---|---|---|

| Stock Price | $142.39 (as of 28 April 2026) | Reflects an equity drop from highs |

| Market Capitalisation | $16.49 billion | Highlights a $17 billion to $20 billion value loss |

| Regional Revenue (Q4 FY25) | North America down 4%; China up 24% | Signals fatal loss of core market pricing power |

Understanding how corporate power struggles function behind the scenes transforms this boardroom drama into a clear structural battle for control. The conflict centres on the mechanics of a classified directorial election system. In a classified or staggered board, only a fraction of directors stand for election each year, making it mathematically impossible for dissenting shareholders to replace the entire board in a single vote.

According to reports, only 10% of S&P 500 corporations still utilise staggered directorial terms, as governance advocates typically argue the structure entrenches incumbent management. Wilson is leveraging this proxy contest to force a public referendum on current leadership. His primary governance critique targets board independence, specifically focusing on private equity connections.

Current directors share professional affiliations with private equity group Advent International L.P. The founder argues this concentration of influence stifles objective oversight and alienates retail shareholders.

The escalating Lululemon proxy fight relies heavily on declassifying the board, an activist campaign strategy designed to replace entrenched directors who may prioritize private equity interests over retail shareholder value.

Founder Allegation on Corporate Demands “The corporate leadership demanded a $1 million escrow payment simply to secure a standard non-disparagement agreement during our negotiations.”

To dismantle the current power structure, an alternative slate of director candidates has been proposed. These nominees bring specific track records of driving financial growth at major consumer enterprises.

The structural governance friction ultimately stems from a deeper crisis regarding the emotional core of the brand. Investors and consumers alike are questioning whether recent corporate partnerships signal a drift toward mass market mediocrity. The loss of premium exclusivity stands as the foundational strategic misstep driving the current internal rebellion.

This anxiety amplified following the appointment of Heidi O’Neill as the incoming chief executive. O’Neill will officially take charge on 8 September 2026, bringing experience from Nike. While her resume shows operational scale, the founder expressed immediate concern that a volume-driven background conflicts with an elite product vision.

Market reaction to this leadership transition was swift and severe, contributing directly to a $20 billion drop in shareholder equity as investors questioned the shift from upscale prestige to mass market volume.

Recent corporate collaborations illustrate this perceived brand dilution. The company launched a high-profile product partnership with The Walt Disney Company in late 2025, complete with a dedicated store opening in the Downtown Disney District.

Industry analyst Randal Konik expressed deep confusion regarding the strategic value of the Disney alliance, suggesting it alienated the core consumer base. Executive hiring decisions and marketing collaborations directly impact the perceived value and pricing power of a luxury athletic brand.

Traditional elite positioning relied on scarcity, technical superiority, and high-margin demographics. Recent mass market moves emphasise volume partnerships, broad demographic appeal, and licensed entertainment merchandise.

Even if the governance issues find resolution, the victor inherits a brutally competitive retail environment. The internal boardroom chaos is currently colliding with an external surge in formidable competitors. The United States activewear market has reached a state of deep saturation, leaving little room for unforced strategic errors.

Financial analysts remain highly cautious about the company’s near-term recovery prospects. Research firm Stifel maintained a “Hold” rating on the stock through the spring of 2026, noting the current depressed valuation accurately reflects the elevated execution risks. These external pressures are compounding as consumers migrate toward rising premium brands.

Intensifying competition from Vuori, HOKA, On Holding, and Deckers is steadily eroding market share. These rivals are successfully capturing the premium tier that the incumbent brand appears to be vacating.

Comprehensive sporting goods industry analysis reveals that major incumbents have steadily lost ground to agile challenger brands since 2019, creating a highly fractured landscape where strategic errors are severely punished.

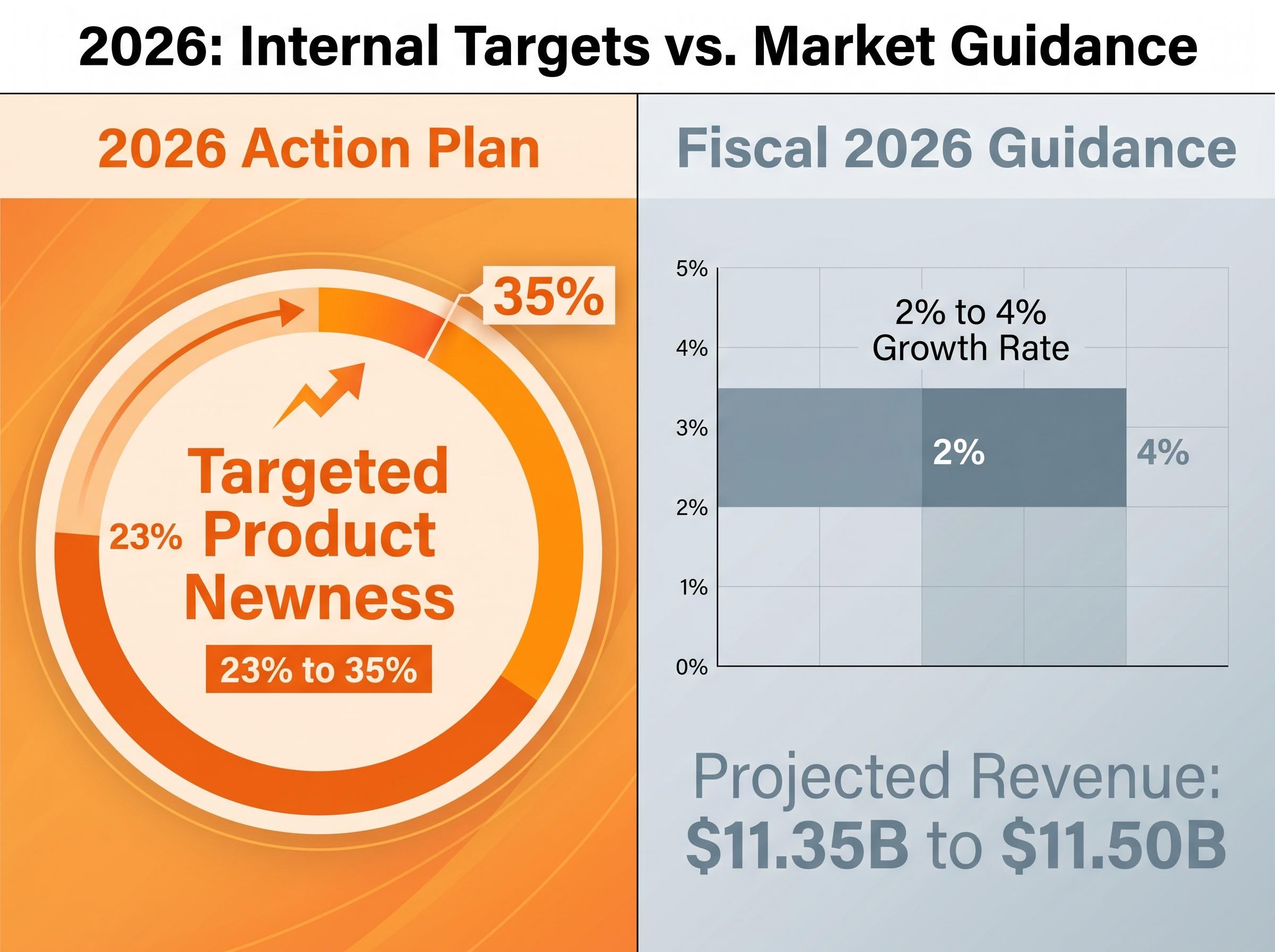

To combat product staleness, interim co-CEOs Meghan Frank and Andre Maestrini introduced a defensive operational strategy. Their 2026 Action Plan aims to aggressively increase product newness from 23% to 35% across the retail assortment.

However, these internal recovery targets contrast sharply with the company’s own forward projections. Fiscal 2026 guidance forecasts a highly conservative 2% to 4% growth rate, projecting revenues between $11.35 billion and $11.50 billion. This single-digit growth guidance panicked the market in March 2026, signalling that management expects the competitive headwinds to persist throughout the fiscal year.

The clash between management’s operational trajectory and the founder’s vision has pushed the activewear pioneer to a definitive juncture. The proxy battle mechanics, market saturation, and brand dilution fears all converge on one impending milestone. The 8 September 2026 start date for the new CEO stands as the ultimate test of the brand’s future direction.

Investors must interpret the upcoming earnings reports and shareholder votes through this specific analytical lens. The structural governance fight will determine whether the board prioritises mass market volume or a return to exclusive pricing power. The market’s response over the next two quarters will reveal if the brand has permanently lost its exclusive economic moat.

Alternatively, this period of heavy discounting and strategic confusion may simply represent a temporary lapse in execution. The resolution of this boardroom conflict will dictate the company’s competitive posture for the remainder of the decade.

For readers interested in how other retail giants are navigating similar periods of stagnation, our full explainer on Starbucks’ turnaround strategy outlines how revamped digital engagement and store innovation can help revive depressed stock performance.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. These statements are speculative and subject to change based on market developments and company performance.

The Lululemon controversy centers on an estimated $17 billion to $20 billion loss in market capitalization, prompting founder Chip Wilson to initiate a corporate governance dispute over strategic direction and board independence.

Lululemon's stock price dropped 44% year-on-year by April 2026, driven by a 4% revenue contraction in the North American market during Q4 FY25 and concerns over leadership transitions and strategic direction.

Chip Wilson is advocating for declassifying Lululemon's board of directors and replacing entrenched members to address perceived conflicts of interest and better align with retail shareholder value.

Heidi O'Neill's appointment as CEO, effective September 2026, has raised investor concerns due to her background at Nike, which some fear indicates a shift towards mass-market appeal rather than Lululemon's traditional elite positioning.

Lululemon faces significant external challenges including a saturated US activewear market and intensified competition from rising premium brands like Vuori, HOKA, On Holding, and Deckers.