ASX 200 Surges 138 Points as US-Iran Ceasefire Reports Hit Markets

6 hrs ago

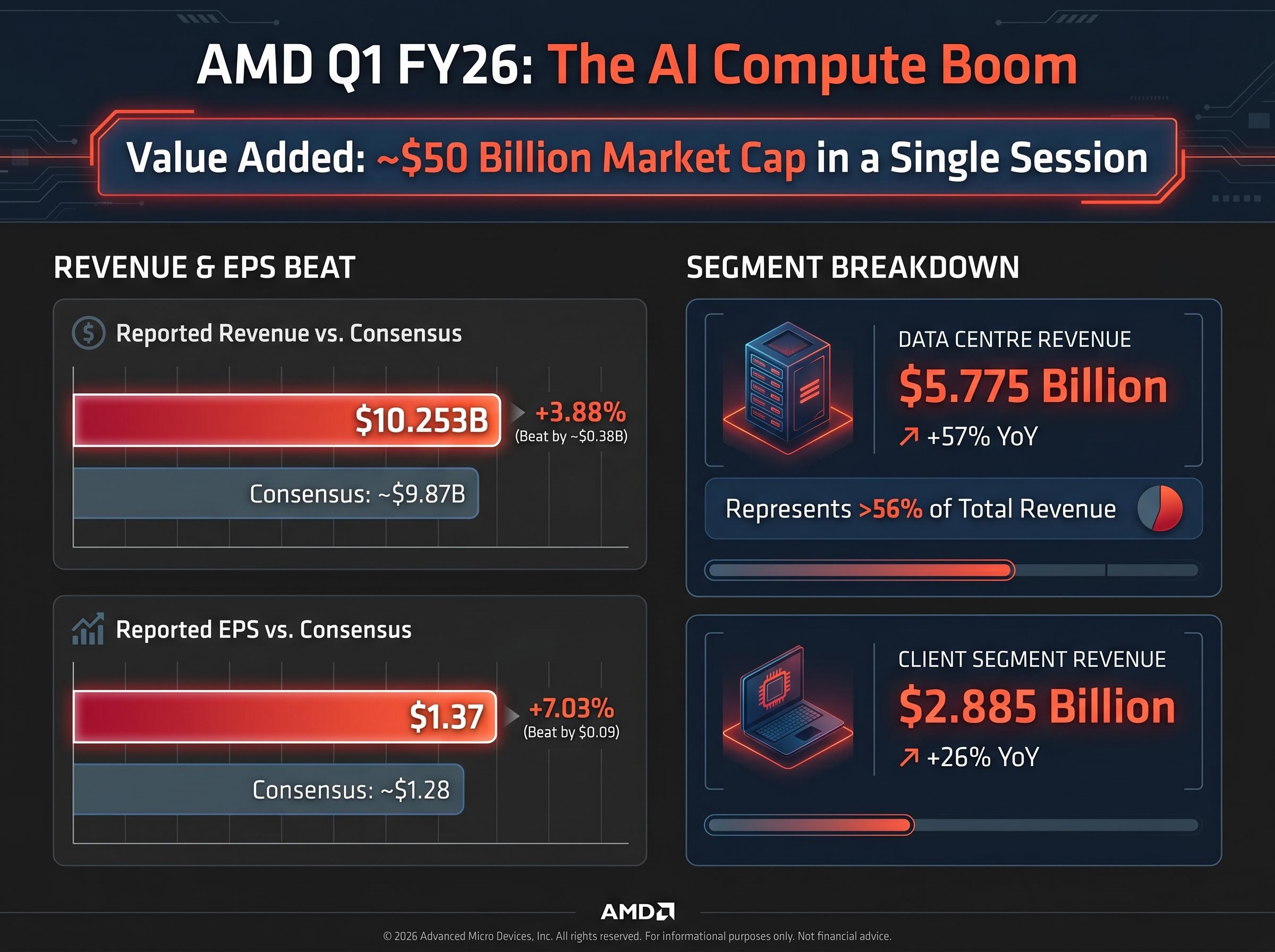

AMD added roughly $50 billion in market capitalisation in a single session after reporting Data Centre revenue of $5.775 billion, up 57% year on year, a figure that landed well above what even the most optimistic analysts had pencilled in. The result arrived alongside three separate corporate announcements that collectively reinforced the same message: AI infrastructure capital expenditure is not slowing.

Alphabet’s $40 billion investment in Anthropic, Anthropic’s 300-megawatt compute deal with SpaceX, and Nvidia’s manufacturing expansion with Corning all surfaced within a 48-hour window. For Australian investors, the combined signal arrived ahead of the ASX 200 open on 7 May 2026, with futures pointing to a 95-point gain. What follows unpacks what AMD’s record result reveals about competitive dynamics in the AI chip market, how the partnership announcements support the broader investment thesis, and what it means for Australian investors tracking AI-exposed equities.

The scale of the beat was difficult to dismiss. AMD reported quarterly revenue of $10.253 billion against analyst consensus estimates of approximately $9.87 billion, a miss that went in management’s favour by roughly 4%. Non-GAAP earnings per share came in at $1.37, beating consensus of approximately $1.28 by 7-8%.

The stock rose approximately 4% in after-hours trading on 6 May 2026, with intraday gains reaching as high as up to 16% on 6 May 2026.

| Metric | AMD Q1 FY26 Reported | Analyst Consensus | Beat |

|---|---|---|---|

| Revenue | $10.253 billion | ~$9.87 billion | ~4% |

| Non-GAAP EPS | $1.37 | ~$1.28 | ~7-8% |

| Data Centre Revenue | $5.775 billion | ~$5.6 billion | ~3% |

The headline numbers matter, but the composition matters more. Data Centre revenue of $5.775 billion now represents over 56% of total AMD revenue, making it the single segment that defines the company’s investment thesis. The 57% year-on-year growth rate outpaced the Client segment’s 26% growth ($2.885 billion) by a wide margin.

CEO Lisa Su pointed to the MI450 Series and Helios rack-scale pipeline as “exceeding expectations” and noted that supply scaling would allow “server growth to accelerate meaningfully.” That language positions Q1 not as a peak quarter but as a staging point.

For the past two years, the AI chip market has been discussed as a single-vendor story. Nvidia held dominant share, and every competitor was framed relative to that dominance. AMD’s Q1 result complicates that framing in a way that matters for portfolio positioning.

The MI450 Series and Helios rack-scale architecture represent AMD’s bid to compete at the infrastructure layer, not just the component layer. Management described the pipeline as exceeding internal projections, and the CFO characterised Data Centre momentum as “outstanding.” These are not hedged statements from a company managing expectations.

CEO Lisa Su, AMD Q1 FY26 Earnings Call: The MI450 Series and Helios pipeline is “exceeding expectations,” with supply scaling positioned to allow “server growth to accelerate meaningfully.”

Brokerage notes dated 6-7 May 2026 reflected a reassessment, not a mechanical earnings revision, with analyst price targets moving into the $200-plus range. The competitive implication is straightforward: AI chip demand is broad enough to sustain two large players simultaneously, and investors tracking Nvidia need to account for AMD’s accelerating trajectory in the same analysis.

AI hardware stocks outside the US are capturing a growing share of the same infrastructure capital, with Samsung Electronics crossing a $1 trillion market cap on the same day AMD reported its record quarter and SK Hynix holding an estimated 52-70% of Nvidia’s HBM memory orders, a concentration that shapes how institutional capital is rotating across the semiconductor supply chain.

The partnership announcements covered in the next section carry more weight when the mechanics behind AI infrastructure demand are clear. AI training workloads, the process of teaching large models on massive datasets, require three layers of physical infrastructure working in concert.

AMD’s 57% Data Centre revenue growth is a direct measure of capital flowing into the compute layer.

GPU compute is increasingly available. Power infrastructure and high-speed optical cabling remain constrained. The Nvidia-Corning partnership targets the optical connectivity bottleneck directly, while the Anthropic-SpaceX deal for 300 megawatts from the Colossus 1 data centre reflects an AI lab sourcing power capacity from unconventional infrastructure partners because traditional cloud capacity cannot keep pace.

Power capacity constraints are increasingly the variable that determines which AI labs can scale fastest, with US data centres projected to consume 9% of domestic electricity by 2030, up from 4% in 2023, a trajectory that explains why Anthropic chose to source 300 megawatts from SpaceX’s Colossus 1 facility rather than waiting for traditional cloud providers to build out equivalent capacity.

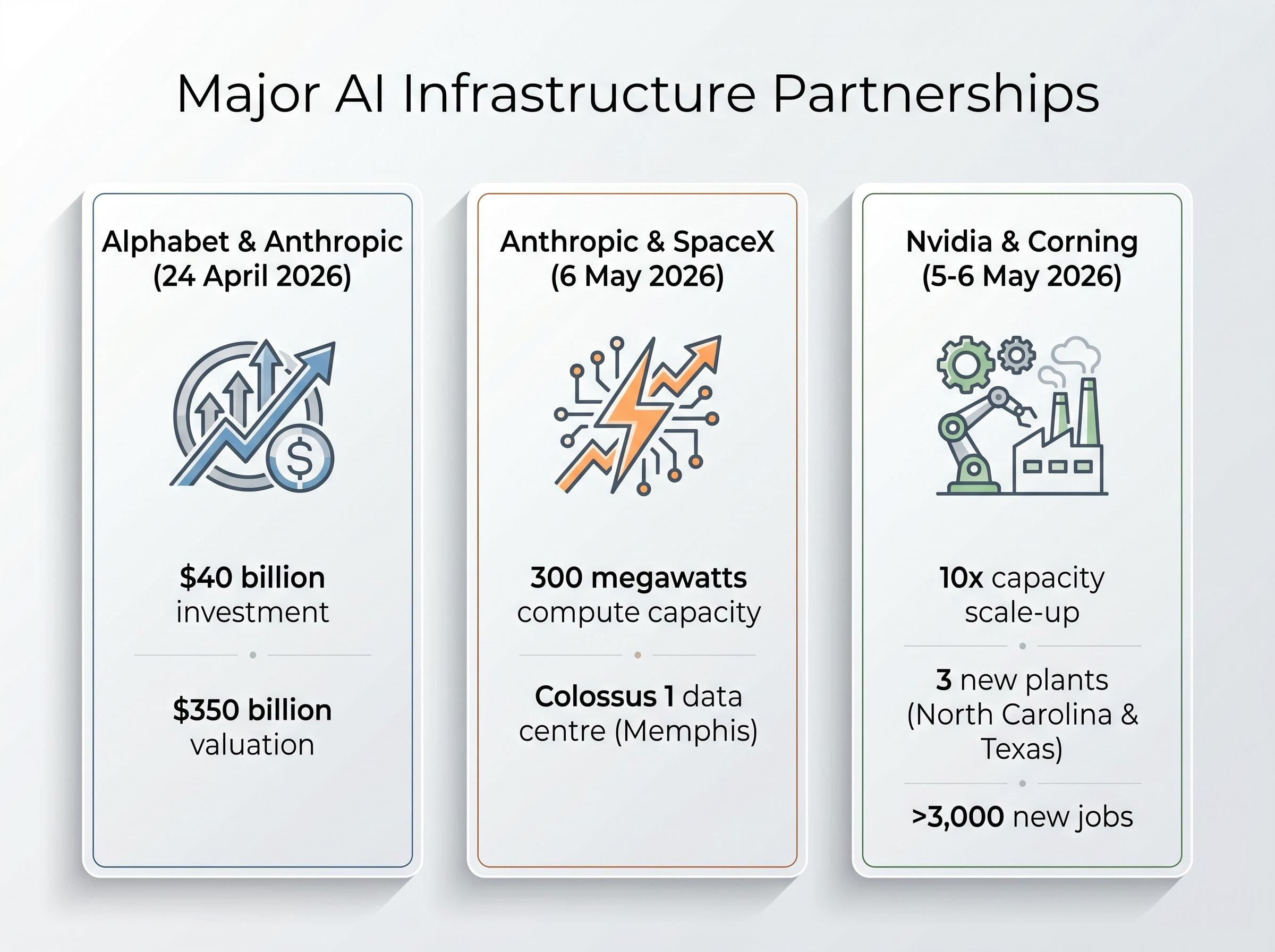

Three separate announcements, from different parts of the AI supply chain, converged within a 48-hour window. Taken individually, each is a corporate partnership. Taken together, they form a pattern: the largest AI players are locking in infrastructure access before capacity becomes the binding constraint on model development.

Alphabet announced a $40 billion investment in Anthropic on 24 April 2026, valuing the AI lab at $350 billion and deepening an existing cloud and chip arrangement that dates to 2023. This is commitment at a scale that signals long-term strategic entrenchment.

On 6 May 2026, Anthropic signed a deal with SpaceX for access to over 300 megawatts of compute capacity from the Colossus 1 data centre in Memphis. The deal illustrates a new dynamic: AI labs are sourcing compute from unconventional partners when traditional cloud providers cannot supply sufficient capacity.

Nvidia and Corning announced a long-term manufacturing partnership on 5-6 May 2026, with plans for three new plants in North Carolina and Texas, a 10x manufacturing scale-up, and over 3,000 new jobs. The partnership addresses the optical interconnect layer that enables GPU clusters to function as unified systems.

| Parties | Deal Type | Key Figure | Significance |

|---|---|---|---|

| Alphabet / Anthropic | Strategic investment | $40 billion | Hyperscaler entrenchment in AI model development |

| Anthropic / SpaceX | Compute access | 300 megawatts | AI labs sourcing capacity beyond traditional cloud |

| Nvidia / Corning | Manufacturing partnership | 10x capacity scale-up | Supply-side response to interconnect demand |

The pattern is consistent: supply constraints, not demand, are the binding concern in AI infrastructure.

Hyperscaler capital expenditure across Amazon, Microsoft, Alphabet, and Meta reached $130 billion in Q1 2026 alone, with full-year 2026 guidance pointing to $725 billion combined, a figure that provides the demand floor underpinning AMD’s forward revenue projections and Lisa Su’s characterisation of Q1 as a staging point rather than a peak.

The US session delivered a clear directional signal. The S&P 500 closed at approximately 7,233 and the Nasdaq closed at approximately 25,495 on 6 May 2026, with the Nasdaq rising 2.02% to a fresh record.

ASX 200 Futures: Up 95 points (approximately 1.08%) as of 8:10 am AEST on 7 May 2026.

For ASX-listed equities, the translation mechanism runs through a small number of names with direct or indirect AI infrastructure exposure:

AI infrastructure investment on the ASX is increasingly concentrated in a small number of operators, with NextDC securing a 250MW contract at its S4 facility and signing an MoU with OpenAI for a Stargate data centre valued at approximately A$6.75 billion, though Australian investors should note those commitments carry distinct risk profiles depending on whether exposure is through colocation, property, or network services.

Readers should verify live price data on ASX.com.au or through their broker before acting on overnight US moves. No verified intraday ASX price data for the 7 May 2026 session was available at the time of publication.

ASIC’s guidance on high-risk retail investment offers sets out the regulator’s expectations for how volatile, sentiment-driven products are presented to Australian retail investors, a relevant backdrop for anyone assessing ASX-listed AI-exposed equities after sharp overnight US moves.

AMD’s Data Centre segment delivered $5.775 billion in revenue, up 57% year on year. Three independent partnerships, from three different parts of the AI infrastructure stack, announced within 48 hours, point to the same conclusion: capital deployment into AI infrastructure is accelerating, not plateauing.

$5.775 billion in AMD Data Centre revenue, up 57% year on year, represents the cleanest single-quarter expression of sustained AI infrastructure spend in the current cycle.

The counterpoint deserves honest acknowledgement. AI stocks have experienced sharp de-rating episodes when sentiment shifted in prior cycles, and a single quarter’s results, even one this strong, does not eliminate that risk.

What distinguishes this moment is the breadth of the signal. The spend is coming from hyperscalers (Alphabet’s $40 billion commitment), AI labs sourcing from non-traditional infrastructure partners (Anthropic-SpaceX), and hardware supply chain expansion (Nvidia-Corning’s 10x manufacturing scale-up). That diversification reduces single-point-of-failure risk in the investment thesis. Whether this proves to be a sustained new leg or a sentiment-driven session depends on what comes next: AMD’s Q2 FY26 guidance and subsequent hyperscaler earnings will either corroborate or challenge the trajectory Lisa Su outlined in her Q1 commentary.

Australian investors monitoring the local transmission of this theme should watch NextDC and ASX-listed technology names as the most direct beneficiaries of continued US AI infrastructure momentum.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AMD reported Data Centre revenue of $5.775 billion in Q1 FY26, up 57% year on year, representing over 56% of total company revenue. This figure is a direct measure of capital flowing into AI compute infrastructure and signals AMD is establishing itself as a credible competitor alongside Nvidia in the AI chip market.

AMD's blowout quarter contributed to a broadly positive US tech session on 6 May 2026, with ASX 200 futures pointing to a 95-point gain ahead of the 7 May 2026 open. ASX-listed companies with direct AI infrastructure exposure, particularly NextDC, have historically moved 2-5% in sympathy with strong US AI sessions.

On 6 May 2026, Anthropic signed a deal with SpaceX for access to over 300 megawatts of compute capacity from the Colossus 1 data centre in Memphis. The deal illustrates a new trend where AI labs are sourcing power and compute from unconventional infrastructure partners because traditional cloud providers cannot supply sufficient capacity.

Alphabet announced a $40 billion investment in Anthropic on 24 April 2026, valuing the AI lab at $350 billion. The scale of the commitment signals long-term strategic entrenchment by a major hyperscaler and supports the broader thesis that AI infrastructure capital expenditure is accelerating, not slowing.

NextDC is the most directly exposed ASX-listed company to AI infrastructure themes, operating data centres and having secured a 250MW contract at its S4 facility alongside an MoU with OpenAI for a Stargate data centre valued at approximately A$6.75 billion. WiseTech Global and Macquarie Group offer indirect exposure through enterprise software and technology investment respectively.