The ASX closed calendar 2025 with 92 new listings, a 37% jump from 2024, raising $6.3 billion in capital and delivering an average return of 24.2% across the cohort. For investors watching the local exchange, the Australian IPO window is wide open again.

After a bruising 2022-2024 stretch marked by withdrawals, weak institutional demand, and below-issue-price flops, the Australian IPO market has staged its most significant recovery in years. The momentum carries into the 2026 financial year, with new floats landing each month and a pipeline of named candidates building across technology, healthcare, and resources. What follows identifies the standout ASX IPOs from the current FY 2025-2026 window, explains what drove their performance (and what dragged others down), and maps the sectors and candidates investors should be watching for the rest of 2026.

Why the ASX IPO market roared back in 2025-2026

The 2022-2024 period was lean. Elevated volatility, persistent risk aversion, and valuations that fell short of issuer expectations conspired to suppress listing volumes. Mid-cap technology, financial, and consumer names shelved their offers. Withdrawals and postponements became routine.

The 2022-2024 ASX cycle compressed a full sequence of drawdown, stabilisation, and sector rotation into roughly two years, and the IPO drought was one of its most visible consequences: issuers shelved offers rather than accept valuations that reflected the bear-market discount, and institutional demand for new equity dried up as capital rotated into defensives.

Three conditions shifted to break the drought:

- Stabilising interest rates, which removed the pricing uncertainty that had frozen deal-making for two years

- ASX 200 levels near record highs, giving issuers and underwriters confidence in market appetite

- Returning investor risk appetite, as the memory of 2022-2023 losses faded and capital began flowing back into new equity

The numbers confirm the turnaround. According to the ASX Capital Markets 2025 Year-in-Review, calendar 2025 produced 92 new listings, raising $6.3 billion (up 54% from 2024) and adding $38.8 billion in market capitalisation. Six new listings exceeded $1 billion in market cap.

The ASX Capital Markets 2025 Year-in-Review confirms the scale of the recovery: 92 new listings across calendar 2025, raising $6.3 billion in capital (up 54% from 2024) and adding $38.8 billion in quoted market capitalisation, with six new entrants exceeding $1 billion at listing.

The average return across all 2025 new ASX listings was 24.2%, the strongest cohort performance since the post-pandemic recovery.

That headline figure frames every individual listing that follows, but as the next section explains, it also conceals significant variation.

When big ASX news breaks, our subscribers know first

What ASX investors need to know before buying into an IPO

An initial public offering (IPO) is a company’s first sale of shares to the public on a stock exchange. On the ASX, it is the moment a private company becomes publicly traded, giving retail and institutional investors the ability to buy and sell its shares on the open market for the first time. For investors evaluating the current cycle, however, understanding what an IPO is matters less than understanding how IPO returns actually behave.

How IPO returns vary within the same market year

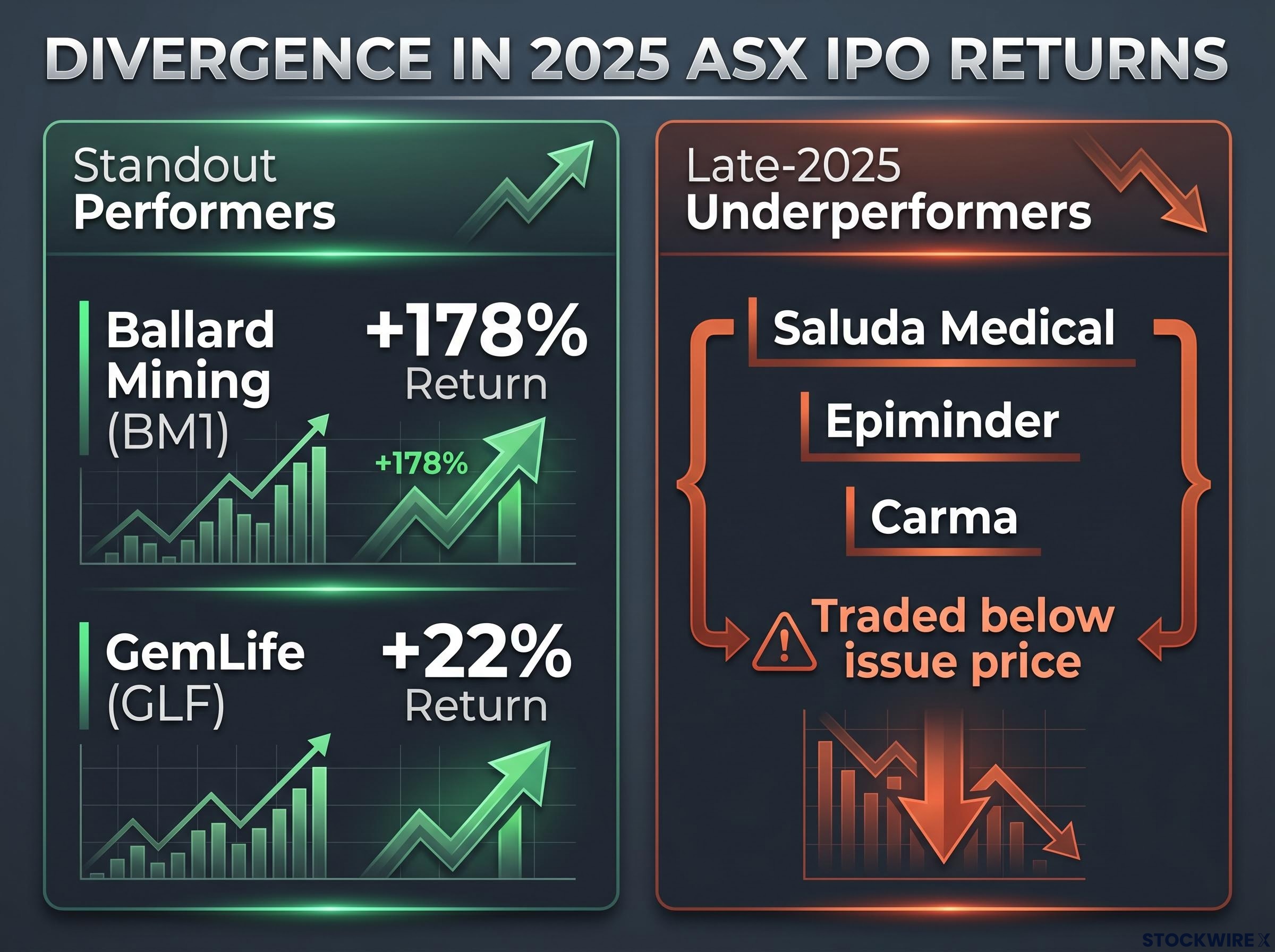

A cohort average of 24.2% smooths over extreme outliers in both directions. Within the same 2025 listing year, Ballard Mining returned 178% from its issue price, while Saluda Medical, Epiminder (backed by Cochlear), and Carma (a used-car retailer) all traded materially below their issue prices by late 2025. The AFR’s Chanticleer column described the late-2025 flops as having “spoilt a momentum-building year.”

The contrast is instructive. Timing, pricing, and sector all shape outcomes, and the gap between the best and worst performers in any given year can be enormous.

| IPO | Sector | Issue Price | Approx. Return |

|---|---|---|---|

| Ballard Mining (BM1) | Resources / Mining | $0.25 | +178% |

| GemLife (GLF) | Real Estate | $4.16 | +22% |

| Saluda Medical | Healthcare | N/A | Below issue price |

| Epiminder | Healthcare (Cochlear-backed) | N/A | Below issue price |

| Carma | Consumer / Retail | N/A | Below issue price |

Investors with commercial intent should treat the 24.2% average as context, not expectation. The distribution beneath it is where the real story sits.

Ballard Mining (ASX: BM1): the standout performer of FY 2025-2026

- Listed: July 2025

- Issue price: $0.25

- Capital raised: $30 million

- Market cap at listing: $46 million

- Return from IPO: 178%, closing at $0.70

Ballard Mining delivered a 178% return from its $0.25 issue price, the strongest individual performance of the FY 2025-2026 IPO cohort.

The listing raised $30 million at a $46 million market capitalisation, placing it squarely in the small-cap resources bracket that dominated ASX IPO volumes during the period. According to the HLB IPO Watch Australia report published in January 2026, 22 of 35 smaller IPOs in 2025 were in the materials and mining segment. Ballard Mining was the cohort’s clearest illustration of the asymmetric upside available in that space.

The resources sector’s dominance among smaller floats reflects sustained appetite for exposure to critical minerals, gold, and base metals. For investors, the 178% return demonstrates what small-cap IPOs can deliver when sector tailwinds, pricing discipline, and timing converge; it also underscores that these results sit at the tail end of the distribution, not the centre.

GemLife Communities Group (ASX: GLF): the large-cap IPO that delivered

- Listed: July 2025

- Issue price: $4.16

- Capital raised: $750 million

- Market cap at listing: $1.58 billion

- Return by end-2025: 22%

Where Ballard Mining rewarded investors who took a small-cap resources bet, GemLife Communities Group showed that strong returns were not confined to speculative mining plays. The $750 million raise made it one of the year’s largest listings, and its $1.58 billion market capitalisation at listing placed it among only six new 2025 entrants to exceed the billion-dollar threshold.

A 22% return from a $4.16 issue price is less dramatic than Ballard Mining’s triple-digit gain, but the context matters. Large-cap IPOs typically carry lower volatility, tighter pricing, and institutional-grade due diligence. A 22% gain from a listing of this scale is consistent with strong large-cap IPO norms and broadens the investment case for the current cycle.

Real estate was one of the high-profile larger-deal sectors in 2025, alongside energy and industrials. GemLife’s performance suggests that institutional-quality floats with established revenue profiles can deliver meaningful returns alongside their smaller, higher-risk counterparts.

The L1 Gold Fund listing, which secured approximately $900 million in commitments before its April 2026 ASX debut under ticker LGF, illustrates the institutional appetite that has returned to the large-cap end of the market, with L1 Capital founders personally committing $120 million in an unusually direct alignment of manager and shareholder interests.

The sectors and names to watch for the rest of 2026

Materials and resources remain the dominant sector by listing count, with critical minerals and energy transition assets expected to stay prominent through the back half of 2026. The sector’s pipeline shows no signs of thinning.

The ASX critical minerals sector has provided the commodity backdrop for much of the small-cap IPO activity in this cycle: spodumene concentrate prices reached US$2,500 per tonne by May 2026, and materials stocks including Pilbara Minerals and Liontown Resources hit 52-week highs, reinforcing the demand signal that underpins exploration-stage listings like those arriving in June 2026.

Confirmed floats arriving before 30 June 2026

Three small-cap exploration listings are already scheduled for June 2026, consistent with the broader resources theme:

| Company | Ticker | Sector | Raise Size | Issue Price |

|---|---|---|---|---|

| Boresight Ltd | BST | Resources | $8 million | $0.20 |

| Daly Resources | DLY | Fluorite / Copper / Zinc | $12 million | $0.25 |

| Neu Horizon Uranium | NHU | Mineral Exploration | $15 million | $0.20 |

All three are early-stage exploration plays with raise sizes between $8 million and $15 million, reflecting the small-cap resources profile that has characterised the bulk of ASX IPO volume in this cycle.

Larger candidates building toward a 2026 ASX debut

Market commentary has named several larger candidates across sectors that would broaden the 2026 cohort beyond resources, though listing dates remain unconfirmed:

- Technology: Firmus Technologies, Morse Micro

- Healthcare: I-MED Radiology

- Consumer / Services: Greencross

These names, cited in analyst and market commentary, signal an anticipated broadening of sector mix. If technology and healthcare issuers follow through, the second half of 2026 could look meaningfully different from the resources-heavy first half. Investors should treat these as candidates to research further rather than confirmed opportunities.

The risks the headline returns do not show you

The 24.2% average masks damage at the other end of the distribution. Saluda Medical, Epiminder, and Carma all traded materially below their issue prices by late 2025, and the consequences extended beyond those individual stocks.

Wilson Asset Management noted in January 2026 that these underperformers cast “a pall over the 2026 pipeline,” increasing investor selectivity heading into the new calendar year.

Three specific risk factors recur in broker and analyst commentary on the current IPO cycle:

- Valuation expectations from issuers: Companies seeking to list often price at levels that leave limited upside for early investors, particularly when market conditions soften between pricing and listing day.

- Global macro sensitivity: Broker commentary describes deal timing as “highly sensitive” to global macro conditions and local rate expectations. A shift in either can stall a pipeline that appeared healthy weeks earlier.

- Timing risk: The gap between prospectus lodgement and first-day trading exposes investors to market moves they cannot hedge, a structural feature of IPO investing that the 2025 underperformers illustrated clearly.

The AFR’s Chanticleer column described the late-2025 flops as having “spoilt a momentum-building year.” For investors considering new floats in the months ahead, these three risk factors serve as a due diligence checklist rather than a reason to avoid the market entirely.

The 2026 ASX IPO cycle is real, but it rewards selectivity over enthusiasm

The ASX IPO recovery is genuine. Calendar 2025’s 92 listings, $6.3 billion in capital raised, and 24.2% average cohort return validate the opportunity in aggregate. Ballard Mining’s 178% gain and GemLife’s 22% return demonstrate that strong outcomes are available across both small-cap resources and large-cap institutional floats.

The pipeline is building across resources, technology, and healthcare, and conditions (rate environment, equity market levels) remain broadly supportive. Yet Saluda Medical, Epiminder, and Carma are reminders that not every listing delivers. Investor selectivity, informed by the 2025 underperformers, is the appropriate posture.

Investors considering participation in upcoming floats should monitor the ASX upcoming floats page for confirmed listings and conduct independent due diligence on any named candidate before committing capital.

Investors exploring the structural mechanics behind these return patterns will find our full explainer on IPO mechanics for retail investors, which covers how allocation works in practice, why retail buyers typically enter after institutions have been allocated at the offer price, and what the expectations gap means for companies that debut on strong business fundamentals but still disappoint public-market buyers.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.